Sample Category Title

Fed Minutes To Show Willingness To Hike In December

Market pricing in close to 90% probability of a December hike

The USD is weaker on Tuesday after American markets were off Monday due to the Columbus Day holiday. The currency had posted gains after a strong inflationary signal in the September jobs report but geopolitical risk over the weekend and the prospect of a declaration of independence Catalonia earlier today drove markets to seek safety. Hawkish rhetoric from the European Central Bank (ECB) about starting to scale back its stimulus program had the EUR bid. The USD will be looking at the Fed for support this week. The US central bank has already raised interest rates twice in 2017 and has signalled another rate hike could happen this year.

The U.S. Federal Reserve will release the minutes from its September Federal Open Market Committee (FOMC) meeting on Wednesday, October 11 at 2:00 pm EDT. The CME FedWatch tool is showing a 89 percent probability of a 25 basis points hike on December 13. FOMC members have been supported the move, with a few doves urging for more patience until inflation recovers.

Later this week the next hurdle for a December rate lift will come with the release of retail sales and consumer price index (CPI) data on Friday, October 13 at 8:30 am EDT. Inflation has met the flat expectations and given the market will be focusing on the CPI for clues that validate or weaken a case for a Fed December hike.

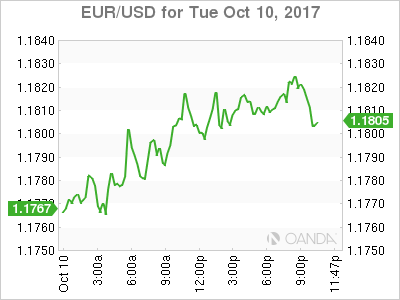

The EUR/USD rose 0.53 percent on Tuesday. The single currency is trading at 1.1803 after the end of the President of Catalonia speech before parliament where the decision to suspend the results of the referendum to set up talks with the central government of Spain. Earlier comments from ECB executive board member Sabine Lautenschlaeger about the tapering of the QE program in 2018 took the EUR higher. The European central bank appears ready to launch the program but has been uncomfortable with the naming and could rebrand it as something else to avoid triggering a “taper tantrum”.

US economic indicators have been impacted negatively by the tropical storms in September leaving the US dollar at the guidance of the Trump administration. The tax reform proposal is not seen as a slam dunk as it is facing criticism from both sides of the political spectrum and the President’s actions and comments on North Korea have further incensed the situation.

Market events to watch this week:

Wednesday, October 11

2:00pm USD FOMC Meeting Minutes

Thursday, October 12

8:30am USD PPI m/m

8:30am USD Unemployment Claims

10:15am EUR ECB President Draghi Speaks

11:00am USD Crude Oil Inventories

Friday, October 13

8:30am USD CPI m/m

8:30am USD Core CPI m/m

8:30am USD Core Retail Sales m/m

8:30am USD Retail Sales m/m

Gold Improves on Catalonia Crisis, US-Turkey Spat

Gold prices continue to head higher this week, as the metal has posted considerable gains on Tuesday. In the North American session, the spot price for an ounce of gold is $1291.43, up 0.59% on the day. There are no major US releases on the schedule.

The Catalan constitutional crisis has shaken up Spain, and it remains unclear whether Catalan President Carles Puigdemont will unilaterally declare independence from Spain. Catalonians voted in favor of independence, but the national government has refused to negotiate with the Puigdemont about session. On Sunday, a demonstration against the referendum attracted some 350,000 people, in a show of support for the Spanish government. If Puigdemont declares independence, Spanish Prime Minister Mariano Rajo has promised to take drastic action, which could include dissolving the Catalan parliament and even arresting lawmakers. Investors are casting a nervous eye on the economic ramifications of the crisis, which has been good news for gold. Two major banks, Caixabank and Sabadell, as well as several large corporations have announced they are relocating their legal headquarters from Barcelona to Madrid. The tensions have not affected the euro so far, but that could change if Catalonia defies Madrid and declares independence.

Turkish President Tayyip Erdoğan once promised a "no enemies" foreign policy, but Erdogan would be more hard-pressed to name some allies. The maverick Turkish leader now finds himself in a spat with none other than President Trump, after Turkey arrested a Turkish national at the US consulate in Istanbul. The US responded by suspending visa services, and Turkey has responded in kind, suspending visas for US citizens. The Turkish lire and Turkish stock markets have fallen, and nervous investors have responded by buying safe-haven gold.

The Federal Reserve stayed on the sidelines at its September policy meeting, but the markets are clearly expecting one final rate hike in December. According to CME FedWatch, the odds of a December rate hike are currently at 86%, compared to just 31% a month ago. Why the huge turnaround? A strong US economy has helped raise the odds, but the primary reason for the huge shift in market sentiment can be attributed to the Fed policymakers that have come out in support of a rate hike, notably Fed Chair Janet Yellen. The lack of inflation remains the most significant impediment to raising rates, but Yellen and other FOMC members have insisted that strong economic conditions will lead to higher inflation levels. Even if inflation does not move higher before 2018, the Fed now appears ready to press the rate trigger.

Dollar Extends Losses as North Korea Story Gets Complicated; Euro Strengthens ahead of Catalonia’s Possible Independence Declaration

The dollar tumbled to just a shade above the 93 key-level against a basket of major currencies in the wake of news that North Korean hackers had stolen military documents from the South Korean defence ministry in September 2016, including South Korean/US war plans which involved to some part the formation of a military unit to eliminate the North Korean leader, Kim Jong Un. Moreover, speculation over North Korea launching a long-range missile test over the coming days also weighed on the greenback.

Meanwhile, in the US, a dark cloud shaded the future of tax reforms after officials from Trump's inner cycle expressed their concerns that the president's feud with the Republican Senator Bob Corker could hamper his efforts to turn tax proposals into law and therefore could add another legislative failure to Trump's agenda.

Market watchers are also waiting for the minutes of the Fed's September meeting to be released on Wednesday for more details on the path of interest rates and balance sheet reduction plans.

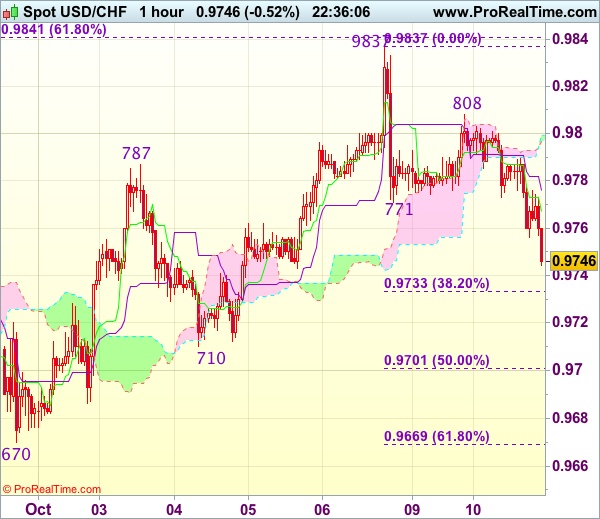

Safe-haven assets advanced as investors were seeking for less risky investments, with dollar/yen falling by 0.51% to 112.06, dollar/swissie retreating by 0.54% to 0.9743 and gold surging by 0.70% to $1,292.40 per ounce.

The euro reached a 1-½ week high of $1.1817 before it fell back to $1.1805 as traders were eyeing encouraging data out of the Eurozone, leaving political issues on the side for a while. Specifically, traders were pricing German upbeat performance in export activities which posted the highest growth since January 2017 in August and therefore eased concerns related to the rising euro acting as a drag on exporters. Moreover, improved business confidence in the block and recommendations from the ECB executive member Sabine Lautenschlaeger for the central bank to gradually start tightening asset purchases next year contributed positively to the euro.

On the political front, the Catalan leader, Carles Puigdemont, will address the regional parliament today at 1600GMT. The Spanish government fears that Catalonia's parliament will unilaterally declare independence. Armed Catalan police forces have surrounded the area, while according to sources with a knowledge on the issue, Spanish police authorities are prepared to arrest Puigdemont if he declares separation from Spain.

In other news, the Netherlands, the fifth largest Eurozone economy, has agreed on a four-member coalition deal seven months since the elections that took place in March. The coalition will be composed of the ruling center-right VVD, the liberal D66 party, the centrist Christian Democrats and the conservative Christian Union and hold just a shade of majority – 76 seats in the 150-seat parliament.

Better than expected August readings on British industrial production gave a lift to the pound, though August's trade deficit touched a record high, putting a break to the pound's uptrend. Manufacturing output increased by 0.4% m/m, above the 0.2% expected. Construction output turned positive after four months of declining, expanding by 0.6% m/m compared to the -1.0% seen in the previous month and the projected 0.1%. Overall, industrial production matched expectations, rising by 0.2%, below the previous upwardly revised mark of 0.3%. Regarding trade balance, the goods and services deficit increased unexpectedly by 1.31 billion pounds to 14.24 billion.

Dollar/loonie changed hands at 1.2498, losing 0.40% on the day on the back of a weaker dollar and a mixed stream of housing data out of Canada. The loonie was also supported by rising energy prices. Canadian housing starts rose by 217.1k in September instead of the expected 210k, whereas building permits unexpectedly experienced the largest contraction since May 2016, falling by 5.5%.

Oil prices were heading higher during European trading hours in response to optimistic comments made by the OPEC's Secretary General Mohammed Barkindo on Tuesday at the India Energy Forum in New Delhi. Particularly, Barkindo reiterated that some "extraordinary measures" might be needed to be taken next year in order to rebalance the market in the long term. However, he did not specify what these measures would be and if these include a further extension of the already-in-place cuts for an additional nine months after the pact expires in March. Besides that, Saudi Arabia's statement on Monday of cutting November's oil allocations by 560,000 bpd according to an oil spokesman helped boost oil prices. WTI crude was trading 2.50% up at $50.82 per barrel and Brent surged by 1.83% to $56.81 per barrel.

Pound Gains Continue as UK Manufacturing Production Beats Estimate

The British pound has posted gains in the Tuesday session. In North American trade, GBP/USD is trading at 1.3194, up 0.56% on the day. On the release front, British Manufacturing Production gained 0.4%, above the forecast of 0.2%. The UK trade deficit jumped to GBP 14.2 billion, much higher than the forecast of GBP 11.4 billion. The NIESR GDP Estimate remained unchanged at 0.4%. In the US, there are no major events on the schedule. We'll hear from FOMC members Neel Kashkari and Robert Kaplan. On Wednesday, the US releases JOLTS Job Openings and the Federal Reserve releases the minutes of the September policy meeting.

Last week was disappointing for the pound which declined 2.4 percent. Weak PMI reports and concern about Theresa May holding onto her job as Prime Minister pushed the pound lower. However, the currency has rebounded this week, gaining 1.0 percent. On Tuesday, the pound received a boost as Manufacturing Production gained 0.4% in August, its second best gain in 2017. As well, the NIESR GDP Estimate for third quarter came in at 0.4%, a notch better than its gain of 0.3% in the second quarter. Despite pessimistic forecasts from the Bank of England, and some analysts, the British economy has weathered the Brexit storm and remains in good shape. However, the Brexit talks have not gone well, and a scheduled negotiation session on Tuesday was cancelled. The Department for Exiting the European Union continues to put on a brave face and insists that the talks have made progress, but European negotiators have sounded less enthusiastic. If significant progress is not made by the end of the year, there will be further pressure on May to take Britain out of the EU without a deal.

The Federal Reserve stayed on the sidelines at its September policy meeting, but the markets are clearly expecting one final rate hike in December. According to CME FedWatch, the odds of a December rate hike are currently at 86%, compared to just 31% a month ago. Why the huge turnaround? A strong US economy has helped raise the odds, but the primary reason for the huge shift in market sentiment can be attributed to the Fed policymakers that have come out in support of a rate hike, notably Fed Chair Janet Yellen. The lack of inflation remains the most significant impediment to raising rates, but Yellen and other FOMC members have insisted that strong economic conditions will lead to higher inflation levels. Even if inflation does not move higher before 2018, the Fed now appears ready to press the rate trigger

Chance of Rate Hike in UK Increases

The EUR/USD is gaining positions following positive news on the German trade surplus which in August reached 21.6 billion euro which is 0.8 billion euro more than expected. Exports in the largest European economy increased by 3.1% and imports expanded by 1.2%. The annual rate of export growth declined to 7.2% which is 0.8% worse than in July. The greenback is feeling some pressure from disappointing data on NFIB small business index which reduced to 103.0 in September against 105.1 forecasted. Investors are waiting for the release of the FOMC meeting minutes tomorrow and in case of hawkish comments regarding a rate hike in December, we may see the EUR/USD slip downwards. At the same time traders are closely watching the news from Catalonia and in case of easing tensions in Spain we may see a rise in euro quotes.

The British pound kept growing amid positive news on manufacturing production growth in the country by 0.4% in August which is twice more than forecasted. On the other hand, the latest report on wage growth in the second quarter of 2.4% compared to 1.6% in the previous reading resulted in an increase in confidence for the start of monetary tightening by the Bank of England in 2017 and two more rate hikes during the next year.

The Australian dollar keeps consolidating in anticipation of new drivers. Traders' mood today may be influenced by the report from Westpac on consumer sentiment in Australia at 23:30 GMT.

EUR/USD

The price has broken through the inclined resistance line and in case of overcoming the closest resistance at 1.1825 the chances of continued growth will significantly increase. In this case the immediate targets will be at 1.1925 and 1.2000. If the fall resumes, the next goals within the negative trend will be at 1.1750 and 1.1620.

GBP/USD

The sterling is confidently rising and the recent breaking through the upper boundary of the descending channel may become the basis for continued price growth to 1.3250 and 1.3400. According to the RSI on the 15-minute chart, the upward momentum is not yet exhausted. We also do not exclude the price dropping to the 1.3000-1.3050 range in the near future.

AUD/USD

The aussie quotes are consolidating within the 0.7740-0.7800 range. In order to change the current trend to positive, the price has to gain a foothold above 0.7800. In the reverse scenario, breaking through the local low at 0.7740 may become a trigger for the fall acceleration to the 0.7700 and 0.7600 range. After the end of consolidation, we are likely to see a rise in volatility.

Trade Idea Wrap-up: USD/CHF – Sell at 0.9770

USD/CHF - 0.9744

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9763

Kijun-Sen level : 0.9769

Ichimoku cloud top : 0.9799

Ichimoku cloud bottom : 0.9797

New strategy :

Sell at 0.9770, Target: 0.9670, Stop: 0.9805

Position : -

Target : -

Stop : -

As the greenback has dropped again after brief recovery, adding credence to our view that top has possibly been formed at 0.9837 last week and consolidation with mild downside bias is seen for weakness to 0.9730-35 (38.2% Fibonacci retracement of 0.9565-0.9837), however, break there is needed to retain bearishness for test of previous support at 0.9710 and later towards 0.9669-70 (61.8% Fibonacci retracement and previous support) which is likely to hold from here.

In view of this, would not chase this fall here and we are looking to sell dollar on recovery as previous support at 0.9771 should turn into resistance and limit upside. Only break of resistance at 0.9808 would signal an intra-day low is formed and indicate the pullback from 0.9837 has ended, bring retest of this level later.

Catalonia Independence Unlikely to Cause Major Issues

Given the uncertainties of Spain and Catalonia, we can see money has been pouring into Bitcoin, but despite this, Equities are not really experiencing large risk-off, but sentiment can change quickly to the downside. Nonetheless, Catalonia's Independence is unlikely to cause major issues for the EU trading bloc, but it is likely to cause structural economic changes within the Spain/Catalonia region.

The biggest opportunity now for traders is to trade the Spain's IBEX index. At this point its obviously sell on rallies. If the price gets to 10.205 it could probably be sold towards next support.

Elliott Wave Analysis: USD Index Intra-day Update

Good day traders! Let's look at USD Index.

USD Index is making a new sharp decline away from 94.30 region, where bigger degree wave 5 was completed. We now see a five-wave fall in play with price trading at the start of a corrective wave. Ideally blue wave four will rise for a three-wave move and later search for resistance and a new turning point lower around the Fibonacci ratio of 38.2 or 50.0. From there a new drop lower, into wave five may come in play.

USD Index, 1H

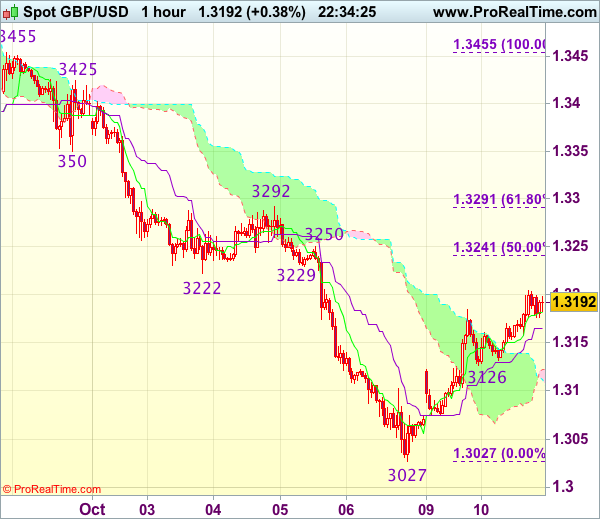

Trade Idea Wrap-up: GBP/USD – Stand aside

GBP/USD - 1.3213

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 1.3187

Kijun-Sen level : 1.3172

Ichimoku cloud top : 1.3122

Ichimoku cloud bottom : 1.3112

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Cable has edged higher again and near term upside risk remains for the corrective rise from 1.3027 (last week’s low) to bring retracement of recent decline, hence gain to 1.3220-25 cannot be ruled out, however, reckon upside would be limited to 1.3240-50 (50% Fibonacci retracement of 1.3455-1.3027 and previous resistance), however, further sharp move beyond 1.3270 should not be repeated and price should falter below 1.3291-92 (61.8% Fibonacci retracement and previous resistance), bring retreat later.

In view of this, would not chase this rise here and would be prudent to stand aside for now. Below 1.3150-60 would bring test of support at 1.3126, break there would signal an intra-day top is formed but break of 1.3100 is needed to signal the rebound from 1.3027 has ended, then fall to 1.3070-75 would follow.

No Negative Impact from Catalonia on the Euro (Yet)

- European equities trades listless, but marginally negative with underperformance of Madrid and Milan. US equities open with modest gains eyeing again the all-time highs, with energy outperforming.

- The IMF raises its 2017 and 2018 GDP growth forecast for the U.S., China, euro area and Japan in its October World Economic Outlook published in Washington. It warned policy makers not to get too comfortable.

- French president Macron's plans to make common cause with Germany to reform the eurozone have suffered an early setback as Berlin pushes proposals for sovereign debt write-downs that Paris fears could shatter investor confidence in the single currency. Help from the euro area's bailout fund should always be conditional on a government restructuring its debt and putting investors in line to suffer losses.

- The ECB said holdings of Greek sovereign bonds acquired under its SMP programme had resulted in €7.8bn of net income interest between 2012-2016. These profits are redistributed across all EMU central banks.

- The UK's core trade deficit widened by £2.9bn to £10.8bn in the three months to August, the ONS said. Stripping out erratic items such as gold and ships, the goods deficit expanded by £3.8bn compared to the previous three-month period, while the services surplus offset that slightly, widening by £800m

- Output in the UK's industrial sector improved for a 3th straight month in August, with an much better than expected improvement in manufacturing pushing growth to its highest level since February. Production increased 1.6% Y/Y, versus 0.8% Y/Y expected.

- French industrial production disappointed in August, dropping 0.3% M/M to be up a modest 1.1% Y/Y, following a sharp upwardly revised 0.6% M/M and 4.1% Y/Y in July. Italian production, on the contrary, defied consensus estimates for a second month in a row. Production rose strongly by 1.2% M/M and 5.7% Y/Y in August. .

Rates

Core bonds remain in wait-and-see mode

The return of US traders didn't bring more animus than yesterday. Sideways bund trading with a slight negative tone in the afternoon reverses yesterday's gain. The eco calendar remained unattractive and the data were as expected largely ignored. German trade surplus was larger than expected as exports spurted ahead. French production disappointed and Italian one exceeded expectations (both August). US NIFB small business optimism disappointed in September, but was overlooked too. No main impetus from equities either (small losses), nor from oil that digests a modest downside correction after a strong September rally. Auctions went well, but didn't affect overall bond sentiment. All in all, despite a high number of data releases and fresh supply, there wasn't much for traders to get excited about. End-investors are waiting for US key eco releases on Friday and headline event news starting this evening with the Catalan parliament meeting, followed tomorrow with the FOMC Minutes, central bank speakers and more supply.

At the time of writing, German bond yields are up 0.5 (2-yr) to 1.4 bp (10-yr), erasing yesterday's modest declines. US Treasuries are virtually unchanged. Also, the intra-EMU bond market trading remained lethargic ahead of a key meeting of the Catalan parliament. The German-Spain 10 yr yield spread is unchanged. Other spread changes vary between +1 bp (Italy) and -1 bp (Portugal/Greece).

The Slovak debt agency successfully launch a new €1B 30-yr benchmark (2% 17 Oct 2047) at mid-swap +45 from an initial price target of low to mid 50s and is priced 75 bps over DBR 1.25% August 2048. The book was a multiple of the issue size. The new issue is a significant lengthening of the Slovak curve. Finland sold €1B of its 0% 2022 bonds at a yield of -0.267% (average price 101.21). The 1.50 bid/cover was in line with the result at the April auction. Germany sold 0.799B of its 0.1% April 2026 IL bunds at an average yield of -1.04%. Bundesbank retained about 20.1% for its market regulation fund. Total bids amounted to €1.516B or a bid/cover of 1.9.

Currencies

No negative impact from Catalonia on the euro (yet).

There was again little high profile news to guide USD trading. The dollar traded soft in Asia and this bias persisted during the EMU and US sessions. Investors keep an eye at the developments in Spain, but for now, it has no negative impact on the euro. EUR/USD trades in the 1.1790 area. USD/JPY hovered close to mostly slightly below the 112.50 handle.

Overnight, equity sentiment improved gradual throughout the session. The PBOC fixed the yuan strong against the dollar. PBOC officials aim for a more market-based regime for the yuan. Yuan strength weighed on the dollar overall. EUR/USD traded in the 1.1775 area at start of European trading. USD/JPY initially outperformed the other cross rates and stabilized in the 112.50/70 area.

German August trade balance data were strong. The euro briefly gained a few ticks after the release, but as is usually the case, it was no game-changer for EUR/USD trading. USD softness persisted during the European session. EUR/USD jumped temporary north of 1.18. Changes in core yields were limited. If anything interest rate differentials narrowed slightly in the disadvantage of the dollar. USD/JPY cede the 112.50 floor and dropped to the 112.30 area. The US NIFB small business confidence unexpectedly declined from 115.3 to 113 (115 was expected). However, it was ignored, probably as investors assumed that it was affected by the hurricanes. US equity indices continue their record race at the opening. However, for now it doesn't support USD gains. There is still no negative impact from the potential turmoil after the meeting of the Catalonian Parliament this evening. EUR/USD trades in the 1.1790 area. USD/JPY hovers at about 112.40.

Sterling going nowhere on mixed eco data

Moves in sterling were modest today despite plenty UK eco data. Those data painted a diffuse picture. UK (manufacturing) production rose at a fairly healthy pace for the second consecutive month in August (0.4% M/M) and Y/Y figures jumped higher due to revisions of earlier data. At the same time, the August UK trade deficit printed at a record -£14 245 mln as imports rose much more than exports. So at least for now, the UK economy doesn't profit from the decline of sterling after the Brexit decision. This set of conflicting data had no noticeable impact on sterling trading. EUR/GBP held a very tight range close to, mostly slightly below 0.8950. USD softness caused some modest further gains for cable. The pair trades currently in the 1.3175 area. Today's data won't change to BoE intention to raise its policy rate in the coming months.