Sample Category Title

NZD/USD Hovers Above Critical Support

NZD/USD increased today and still tries to close the yesterday's gap down, but failed to stay near 0.7087 today's high and now could reach the 0.7053 horizontal support if the USDX will squeeze a little after the morning drop. Price hovers above the 0.7053 support and below the median line (ml) of the minor descending pitchfork. It could come to retest the median line (ml) before will drop much deeper, the perspective is bearish as long as is located below this level.

Only a breakout above the median line (ml) will announce an increase towards the upper median line (uml).

EUR/GBP Downside Uncertain

EUR/GBP posted humble gains today and still could drop in the upcoming days. Is trading in the green and tries to recover after the yesterday's drop. Technically, it should drop after the retest of the median line (ML) of the ascending pitchfork.

Only a valid breakout above the median line (ML) and above the 0.9000 psychological level will announce a further increase towards the 0.9226 static resistance.

US Indices Target Further Records on Tuesday

- Spanish assets under pressure on Catalonia independence rumours;

- GBP rebounds on decent economic reports;

- Gold remains well supported despite falling 5% from last month's highs;

- FOMC speeches eyed after bank holiday weekend.

It's been a relatively quiet start to the trading week, with the bank holiday in the US and Canada on Monday taking some of the spark out of the markets but futures are pointing higher once again which could pave the way for more record highs.

Once again, the Spanish IBEX is lagging behind its peers in Europe – down around 1% on the day – as speculation that Catalan leader Carles Puigdemont may be preparing to declare independence today continues to grow. The uncertainty is weighing heavily on risk appetite but it currently only appears to be directly impacting Spanish assets, with the euro showing little or no sign of being negatively affected.

The pound is rebounding against the dollar at the start of the week after having come within touching distance of 1.30 on Friday following the US jobs report. Decent retail sales data from BRC overnight and better than expected manufacturing production data this morning is helping to further support the pound although ultimately, both face significant headwinds in the coming months and years and sterling is strongly reliant on the Bank of England following through on a rate hike at these levels.

The dollar's losses are commodities gains today, with Gold, Silver and oil, among many others, enjoying some relief as the greenback pares recent gains. While Gold has fallen around 5% from its peak last month, it role as a safe haven means it remains relatively well supported in what continues to be a heightening political and geopolitical risk environment. The Catalonia referendum and what will follow is just another in a long list of downside risks for the EU while tensions between the US and North Korea may appear to have been but continue to bubble under the surface.

The calendar is looking a little light this week as far as economic data is concerned but we will get plenty of views from a range of central bankers in the coming days as well as the release of the minutes from the September FOMC meeting on Wednesday. Robert Kaplan and Neel Kashkari will both offer their views today, both of whom are voters on the FOMC for the remainder of this year.

The US Dollar Reserves the Right to Grow

- The US Dollar is still interesting and attractive to investors, despite the statistical fluctuations.

- The US labor market statistics in September was surprising, but not as impressive as it might have been.

- Improvements in the Unemployment Rate and the Average Hourly Earnings will allow the US Federal Reserve to tighten its monetary policy.

The first October week was quite effective for the American Dollar. The main currency pair updated the low at 1.1668 it reached on August 17th and then was corrected bit, but made perfectly clear that there might be more declines. If there is a reason, the "bears" will come quickly.

The US labor market statistics in September is astonishing. The numbers were expected to be quite high, but the market was really surprised by the readings it saw. The Unemployment Rate was 4.2% in September after being 4.4% the month before. This is the lowest value of the indicator since 2001, over 16 years. It's highly unlikely to be a mistake: the Participation Rate increased up to 63.1% against 62.9% in August. It appears that the labor market is really feeling good.

Another positive thing is the growth of the Average Hourly Earnings. In September, it expanded by 0.5% m/m after adding 0.2% m/m in the previous month and against the expected reading of 0.3% m/m. On YoY, the indicator increased by 2.9%. That's a very good result.

However, this is where good news ended. The Non-Farm Payrolls decreased by 33K, although it was expected to expand by 82K after adding 169K the month before. The report says that the decline in some industries likely reflected the impact of hurricanes Irma and Harvey, which made the country nervous last month. But if one takes a closer look at the NFP numbers published in July and August, one can see that the indicator was revised downwardly twice. If one adds the September reading to this period of time, the overall picture won't be very promising. Still, the fact that the US labor market is usually pretty stable makes all above-mentioned numbers look not so horrible. It means that the September decline will be eliminated in October or November, unless there are some serious stresses of course.

The Unemployment Rate and the Average Hourly Earnings data shows that the inflation in the USA is rising. This, in its turn, supports the Federal Reserve in its intentions to tighten the monetary policy. After they published the September reports on the employment, expectations relating to the key rate increase in December 2017 increased up to almost 80%, according to the CME futures. This was the reason why the USD rose.

The best way to see investors' attitude to the USD is the EUR/USD pair behavior. Let's take a look at the H4 chart, which shows the downtrend. The key element of the current movement is the price's consolidating around the support level, and one of the most possible scenarios implies that it may return to the upside border of the descending channel. One of the targets close to the resistance level is the retracement of 61.8% at 1.1875. If this scenario continues, we can expect the price to rebound from the upside border and resume falling to reach 1.16. also, we shouldn't exclude a possibility that the instrument may break the current resistance level and start forming a new rising impulse. The main short-term target of this impulse will be the local high at 1.2092.

CAC Steady, Investors Await Catalan Decision

The CAC index is unchanged in the Tuesday session. Currently, the CAC is trading at 5,360.50, down 0.12% on the day. On the release front, there are no major events on the schedule. French Industrial Production declined 0.3%, missing the forecast of a 04% gain. This marked the indicator's second decline in three months.

France's powerful unions have declared a countrywide strike on Tuesday, in protest of the government's plans to dismiss 120,000 public sector workers and reduce sick leave benefits. Millions of French workers are expected to stay home, and the strike represents a serious challenge to the French President Emmanuel Macron's plans to reform the economy and trim the public sector. The French economy has rebounded in 2017, but the government says that more reforms are needed in order to make the French economy more competitive.

What's next for Catalonia? Later on Tuesday, Catalan President Carles Puigdemont will address the Catalan parliament, but it's not clear whether lawmakers will endorse a declaration of independence from Spain. Catalonians voted in favor of independence in a referendum last week, but the national government has refused to negotiate with the Puigdemont about session. Pro-independence lawmakers had hoped for international intervention, but the European Union has refused to mediate the crisis, and France other countries have said they will not recognize an independent Catalonia. On Sunday, a demonstration against the referendum attracted some 350,000 people, in a show of support for the Spanish government. If Puigdemont declares independence, Spanish Prime Minister Mariano Rajo has promised to take drastic action, which could include dissolving the Catalan parliament and even arresting lawmakers. Investors are casting a nervous eye on the economic ramifications of the crisis. Two major banks, Caixabank and Sabadell, as well as several large corporations have announced they are relocating their legal headquarters from Barcelona to Madrid. The tensions have not affected European stock markets so far, but that could change if Catalonia defies Madrid and declares independence.

GBPUSD Continues to Advance

The British pound has moved towards the 1.3200 level against the U.S dollar, after the United Kingdom released better than expected manufacturing and industrial production figures for the month of August.

Intraday trading sentiment surrounding the GBPUSD pair on Tuesday supports further gains, after better than expected economic data and price-action remains supported above the key 1.3150 level.

At present, the 1.3200 level is proving strong resistance for the GBPUSD pair, failure to close the next daily price candle back above the 1.3220 level may encourage selling towards the 1.3150 level.

The outcome of today's Catalan parliament session will likely dictate the next directional move in the GBPUSD pair, as the British pound follows the euro's reaction.

Key intraday technical resistance above the 1.3200 level is found at 1.3220 and 1.3243. Above the 1.3243 level, the 1.3268 and 1.3300 offer further strong resistance.

Key intraday technical support is found at 1.3185 and the former swing low, at 1.3158. Once below the 1.3150 level, further support is seen at 1.3130 and 1.3118.

USDJPY Tests Range Support

The USDJPY pair has fallen towards the lower-end of its recent trading range, hitting 112.27, as the U.S dollar index starts to slip lower across the board and U.S bond yield come under selling pressure.

Today's trading sentiment surrounding the USDJPY pair remains neutral, as the pair continues to hold its 10-day trading range between 113.43 and 112.25.

Traders are likely to see the USDJPY pair moving in increasingly tight range-bound trading conditions until a clear market moving catalyst emerges.

Going forward, the USDJPY pair has now recovered price-action towards the 112.45 region, and may proceed to test the upper boundaries of its current range if the pair can break above the 112.64 level.

Key intraday USDJPY support is found at the 112.25 level, and the pairs 50-week moving average at 112.02. Once below 112.03, further key support is found at the 111.89 level, and the pairs crucial 200-week moving average at 111.74.

To the upside, key intraday resistance is found at 112.50 and the pairs daily pivot point, at 112.64. Further technical support is found at the weekly pivot point, at 112.80 and the key 113 level.

Technical Outlook: USDTRY Is Consolidating, Techs Continue To Point Higher

USDTRY pair stands lower and consolidating within 3.67/3.70 range on Tuesday, following spike to 3.80 zone on Monday on rising political issues between the USA and Turkey.

Bullish techs keep the upside in focus for fresh rallies which may result in full retracement of 3.9414/3.3883 pullback, as Monday’s action closed above 50% retracement of 3.4914/1.3883 downleg after spiking near Fibo 76.4%.

Dip-buying remains favored while the price holds above weekly cloud top at 3.5875.

Today’s action is holding above initial support at 3.6696 (rising daily Tenkan-sen).

Res: 3.7078, 3.7301, 3.7853, 3.8109

Sup: 3.6696, 3.6512, 3.6000, 3.5875

Market Update – European Session: Catalonia Day Of Reckoning, UK Aug Trade Deficit Hits Record

Notes/Observations

Focus on Catalan President Puidgemont's speech to the regional parliament Tuesday; might provide an "all-clear" that a declaration of independence was not imminent - UK Aug trade deficit of -£14.2B is the highest on record

Overnight

Asia:

Bank of Japan (BoJ) Gov Kuroda reiterated view that expects CPI to pick up pace towards 2% target; o maintain QQE with YCC for as long as needed to reach 2% inflation in stable manner. BOJ to expand monetary base until CPI overshoots 2%. Reiterated view that domestic economy is expanding moderately and would adjust monetary policy as needed to maintain economic momentum

PBOC Gov Zhou: China must press on with a "trinity" of reforms to fully realize an open economy. must embrace free trade and investment, let the market decide the yuan's currency value, and scrap capital account controls

China Stats Bureau Chief: China had no problem meeting 2017 GDP growth target of ~6.5%, might beat target

Europe:

Eurogroup Chief Dijsselbloem: primary discussion was regarding role of ESM; confirmed election of new Eurogroup chair on Dec 4th (Dijsselbloem to serve out current term as Chair through mid-Jan). Ministers saw possible ESM role to play in preventing crises by giving bailout fund new instrument; ESM could be used to backstop single resolution fund

German position paper on ESM: the fund should monitor country risks in the same way the IMF does. New mandate should include predictable debt restructuring mechanism to ensure fair burden sharing between ESM and private creditors

ECB's Lautenschlaeger (Germany): the time has come to put unconventional tools back into the box; should begin scaling back bond purchases at start of next year

Catalan separatists reportedly have offered Socialists a partnership to seek removal of PM Rajoy from power

Catalan President reportedly to declare a 'gradual independence'. Declaration would not lead to parliamentary vote and to insist on Catalonia's wish to negotiate with central govt and the need for mediation

UK PM May: Govt has made clear we have no intention of revoking Article 50; sought a creative solution to new economic relationship with EU post-Brexit

According to ORB poll 57% of voters want PM Theresa May to remain as prime minister until the end of the Brexit process

(UK) Sept BRC LFL Sales y/y: 1.9% v 1.3% prior (fastest pace of growth in 2017)

Energy:

OPEC' Sec Gen Barkindo called for new members shall join output cuts, urged friends in the shale basins in North America to take this shared responsibility

Economic data

(CH) Swiss Sept Unemployment Rate: 3.0% v 3.0%e; Unemployment Rate (Seasonally Adj): 3.1% v 3.2%e

(DE) Germany Aug Current Account Balance: €17.8B v €17.0Be; Trade Balance: €21.6B v €19.5Be; Exports M/M: 3.1% v +1.1%e; Imports M/M: +1.2% v +0.5%e

(FI) Finland Aug Industrial Production M/M: No est v 0.4% prior; Y/Y: No est v 2.7% prior

(NO) Norway Sept CPI M/M: 0.6% v 0.7%e; Y/Y: 1.6% v 1.7%e

(NO) Norway Sept CPI Underlying M/M: 0.5% v 0.6%e; Y/Y: 1.0% v 1.2%e

(FR) France Aug Industrial Production M/M: -0.3% v +0.5%e; Y/Y: 2.7% v 1.5%e

(FR) France Aug Manufacturing Production M/M: -0.4% v +0.6% prior; Y/Y: 2.7% v 2.7%e

(HU) Hungary Sept CPI M/M: 0.1% v 0.2%e; Y/Y: 2.5% v 2.7%e

(DK) Denmark Sept CPI M/M: +0.1% v -0.1%e; Y/Y:1.6% v 1.4%e

(DK) Denmark Sept CPI EU Harmonized M/M: +0.1% v -0.4% prior; Y/Y: 1.6% v 1.4%e

(IT) Italy Aug Industrial Production M/M: 1.2% v 0.1%e; Y/Y: 5.7% v 2.5%e; Industrial Production WDA Y/Y: 5.6% v 2.9%e

(UK) Aug Industrial Production M/M: 0.2% v 0.2%e; Y/Y: 1.6% v 0.9%e

(UK) Aug Manufacturing Production M/M: 0.4% v 0.2%e; Y/Y: 2.8% v 1.9%e

(UK) Aug Visible Trade Balance: -€14.2B v -€11.2Be (largest deficit on record); Overall Trade Balance: -£5.6B v -£2.8Be; Trade Balance Non EU: -£5.8B v -£3.6Be

Fixed Income Issuance:

(EU) EFSF opened its book to sell €3.0B in Oct 2023 Bond; guidance -25bps to mid-swaps; order book over €8.0B

(ES) Spain Debt Agency (Tesoro) sold total €4.94B vs. €4.5-5.5B indicated range in 6-month and 12-month Bills

(ID) Indonesia sold total IDR7.0T in 3-month and 12-month Bills & 2-year,4-year,7-year and 15-Year Project-based Sukuk (PBS)

(SK) Slovakia Debt Agency (Ardal) opend its book to sell €1.0B in 30-year bonds; guidance seen +50bps to mid-swaps

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.1% at 390.0, FTSE +0.1% at 7513, DAX -0.2% at 12947, CAC-40 -0.1% at 5362, IBEX-35 -0.6% at 10179, FTSE MIB -0.7% at 22309, SMI +0.1% at 9267, S&P 500 Futures flat]

Market Focal Points/Key Themes: European Indices trade lower across the board with notable weakness in the FTSE MIB and Spanish Ibex, while the FTSE trades in positive territory following better Industrial production data. Focus remains on Spain with focus on Catalan President Puidgemont's speech to the regional parliament later today. On the earnings front LVMH and Christian Dior trade higher after strong Q3 results, Dominos Pizza UK trades sharply higher following their trading update, as does Robert Walters after lifting its outlook. Retailer Pets-at-Home trades sharply lower after KKR sells 12.2M shares, while while Dassault Systems leads the decliners in France after Falcon 5X plane development issues.

Equities

Consumer discretionary [Christian Dior [CDI.FR] +2.1% (Earnings), LVMH [MC.FR] +2.3% (Earnings), Dominos Pizza [DOM.UK] +13.6% (Trading update), Robert Walters [RWA.UK] +8.2% (Earnings), Marston [MARS.UK] +4.7% (Earnings), Givaudan [GIVN.CH] +3.4% (Earnings), Pets at Home [PETS.UK] -7.6% (KKR sells 12.2% stake), Johnston Press [JPR.UK] -16% (Updates on strategic review: approaches largest bondholder to form ad hoc committee of bondholders)]

Industrials: [ Bossard Hlds [BOSN.CH] +3% (Earnings), Dassault Aviation [AM.FR] -4.2% (concerns about the development plans for the Falcon 5X plane)]

Healthcare: [Evotec [EVT.DE] +1.9% (Milestone payment)]

Speakers

President of European Parliament Tajani letter to ECB's Draghi: deeply concerned about how decision on new bad loan guidelines has been undertaken

German IG Metall union recommended collective bargaining round of 6.0% for metal and electrical industry

BOJ Quarterly Regional Report (Sakura) raised its view in 4 of 9 regions ( remainder unchanged). Main factors for improvement in assessment due to stronger momentum in exports and production, private consumption growth, and public investment support from the implementation of the FY16 second supplementary budget

Russian Lawmaker: North Korean leadership claims to possess a ballistic missile with a range of 3,000 km and following modernization will be able to reach a US territory

Currencies

EUR/USD rebounded from recent losses after ECB's Lautenschlaeger struck a hawkish note in her commentary on Monday in which she called for ECB to roll back asset purchases in 2018. Dealers did note that political overhang did persist in the region with focus on Catalan President Puidgemont's speech to the regional parliament Tuesday. The recent split in the regions appetite for independence might provide an "all-clear" that such a declaration was not imminent. EUR/USD trading at 1.1780 just ahead of the NY morning.

GBP/USD was firmer ahead of Aug trade and production data. Dealers saw this was the last bit of 'hard data' ahead of UK Q3 GDP. The Industrial and Manufacturing data did beat expectations for the YoY readings. The market brushed aside the record breaking trade deficit for Aug. GBP/USD trading around 1.3185 just ahead of the NY morning.

Fixed Income

Bund futures trade at 161.55 up 10 ticks as markets eagerly await on Catalan President Puidgemont's speech to the regional parliament. Continued downside targets 161.03 while upside resistance stands initially at 162.07, followed by 163.27.

Gilt futures trade unchanged at 123.96 following better than expected Industrial Production and Manufacturing data. Continued downside eyeing 123.26. Upside targets 124.90 then 125.24.

Tuesday's liquidity report showed Monday's excess liquidity fell to €1.791T from €1.798T and use of the marginal lending facility dropped to €185M from €195M.

Corporate issuance saw no issuance

Looking Ahead

(PT) Bank of Portugal releases Data on Banks

(MX) Mexico Sept ANTAD Same-Store Sales Y/Y: No est v 4.0% prior

05.30 (UK) Weekly John Lewis LFL sales data

05:30 (EU) ECB allotment in 7-day Main Financing Tender (MRO) tender

05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

05:30 (BE) Belgium Debt Agency (BDA) to sell €1.3-1.7B in 3-month and 12-month bills

05:30 (UK) DMO to sell £2.5B in 1.75% 2037 Gilts

06:00 (US) Sept NFIB Small Business Optimism: 105.0e v 105.3 prior

06:00 (FI) Finland to sell up to €1.0B in 0% Apr 2022 RFGB bonds; Avg Yield: % v -0.168% prior; Bid-to-cover: x v 1.53x prior (Apr 26th 2017)

07:30 (CL) Chile Sept Trade Balance: $0.4Be v $0.6B prior; Total Exports: $5.6Be v 6.1B prior; Total Imports: $5.0Be v $5.5B prior; Copper Exports: No est v $3.0B prior

07:30 (CL) Chile Sept International Reserves: No est v $38.5B prior

08:00 (UK) Sept NIESR GDP Estimate: No est v 0.4% prior

08:00 (BR) Brazil CONAB crop report

08:00 (RO) Romania Central Bank (NBR) Oct Minutes

08:00 (UK) Baltic Dry Bulk Index

08:15 (CA) Canada Sept Annualized Housing Starts: 211.0Ke v 223.2K prior

08:30 (CA) Canada Aug Building Permits M/M: -1.0% v -3.5% prior

09:00 (RU) Russia Q3 Preliminary Current Account Balance: -$2.8Be v +$2.8B prior

09:00 (EU) Weekly ECB Forex Reserves

09:00 (RU) Russia announces weekly OFZ bond auction

10:00 (MX) Mexico Weekly International Reserves

10:00 (US) Fed's Kashkari (dove, voter)

10:00 (DE) German Chancellor Merkel with France President Macron in Frankfurt

11:00 (ES) Catalan parliament speaker calls plenary session

11:30 (US) Treasury to sell 3-Month and 6-Month Bills

11:30 (US) Treasury to sell 4-Week and 52-Week Bills

14:00 (CA) Bank of Canada (BOC) Wilkins

16:00 (US) Weekly Crop Condition report

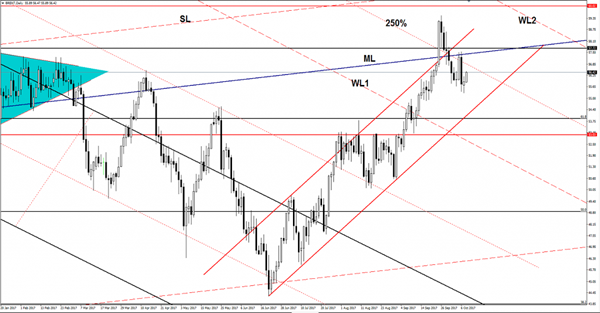

Brent Oil Retest Expected

The price increased and extends the yesterday’s little gains. It should retest the 250% Fibonacci line soon and could drop further, having the first target at the downside line of the minor ascending channel. However, the rate could approach and reach also the median line (ML) of the major ascending pitchfork. A larger drop will be confirmed after a breakdown below the red uptrend line.