Sample Category Title

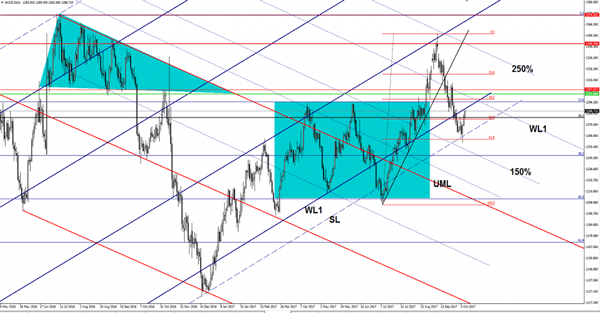

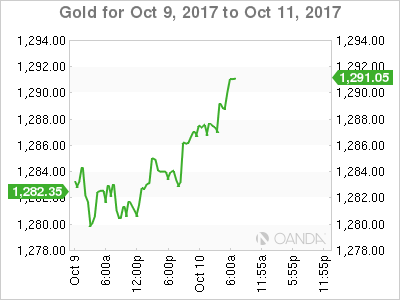

Gold Is The Retreat Completed?

The yellow metal increases further on the short term and is almost to reach the WL1 of the ascending pitchfork, where it could find resistance again. The current increase is natural after the false breakdown below the sliding line (SL). Gold has found support much above the 61.8% retracement level, signaling that the retreat has ended. Personally, I believe that only a minor consolidation will bring it enough energy to be able to take out the next upside targets.

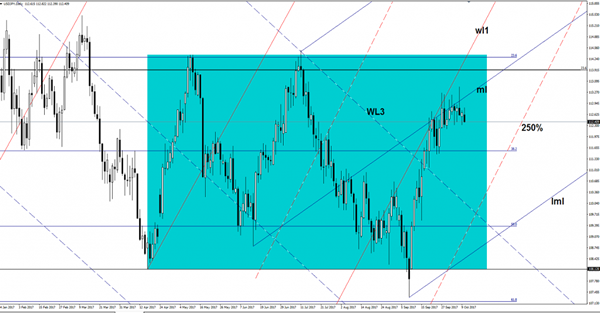

USD/JPY Under Pressure

The currency pair seems undecided on the short term. It's moving sideways on the short term and needs a spark to be able to start a significant move. USD/JPY is trading in the red right now and is almost to reach the 112.32 yesterday's low. Technically, it is expected to drop towards new lows as the USD is punished by the USDX's drop.

The Yen is going up versus the greenback on the short term, even if the Nikkei stock index has rallied in the morning and has reached fresh new highs. The index jumped above the 20756 previous high and reached the 20826 level. The Nikkei is pressuring a dynamic resistance, a valid breakout will confirm a further increase and a Yen's depreciation.

The Yen increased versus the USD also because the Japanese data have come in better, the Current Account was reported at 2.27T, higher versus the 1.98T estimate and versus the 2.03T in the former reading period, while the Economy Watchers Sentiment increased from 49.7 to 51.3 points, exceeding the 49.9 estimate.

The price decreased and could drop much deeper if the USDX will slide further and if the JP225 will lose altitude. I've said in the yesterday's article that the rate should approach the 38.2% retracement level in the upcoming days after the false breakout above the median line (ml). Price needs to recapture more directional energy to be able to start another bullish momentum.

High Noon For Catalan Lawmakers

Tuesday October 10: Five things the markets are talking about

In Spain, Catalan lawmakers will meet today to consider a declaration of independence that risks a tight-fisted backlash from PM Mariano Rajoy in Madrid.

Market attention will focus on what words will used by Catalan President Puigdemont, who is due to address the parliament in Barcelona at noon EDT.

Note: Catalan region President Puigdemont is to hold a news press conference at 08:00 EDT (12:00 GMT)

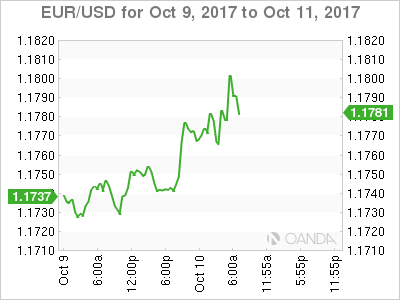

For the present, the EUR (€1.1800) remains supported in a sign of confidence that for now the risk of Catalonian independence is just a Spanish problem.

To date, the 'single' unit has reacted very little to the political events, but it could become rather vulnerable if risks of Catalonia separating become more imminent.

Nevertheless, market consensus is seeking a 'symbolic statement' rather than a declaration of independence as signs of disagreement are starting to emerge within the regional government itself, with more moderate members fearing the consequences of a further step towards independence, given the lack of support from the E.U, and moves by various corporations and financial institutions leaving the region itself.

However, if Catalonia declares independence and Spanish government triggers Article 155 of the constitution, the end result could be higher market volatility – pro-independence groups are expected to paralyze activity in major Catalan cities.

Stateside, the 'big' dollar is waiting for tomorrow's FOMC minutes, which may provide more details on the path of interest rates and balance sheet tapering.

1. Stocks mixed results

In Japan, the Nikkei share average moved closer to a 21-year high overnight after a three-day weekend as expectations for continued strength in the U.S. economy supported sentiment. The index rallied +0.6%, while the broader Topix gained +0.47%.

Down-under, the S&P/ASX 200 was little changed while South Korea's Kospi staged a catch-up rally after a weeklong holiday gaining +1.64% overnight.

In Hong Kong, stocks rallied, bolstered by telecom and property firms. The Hang Seng index rose +0.6%, while the China Enterprises Index gained +0.3%.

In China, stocks erased an early fall, helped by consumer and healthcare firms. The blue-chip CSI300 index, which at one point was down -0.7%, rose +0.2%, while the Shanghai Composite Index added +0.3%.

Note: China data in the coming weeks is expected to show solid growth continued into September, though many analysts maintain there will be some loss of momentum in coming months in response to higher borrowing costs and a cooling housing market.

In Europe, regional bourses trade lower across the board with notable weakness in the FTSE and Spanish IBEX. Focus remains on Spain with Catalan President Puidgemont's speech to the regional parliament at noon EDT today.

U.S stocks are expected to open little changed.

Indices: Stoxx600 -0.1% at 390.0, FTSE +0.1% at 7513, DAX -0.2% at 12947, CAC-40 -0.1% at 5362, IBEX-35 -0.6% at 10179, FTSE MIB -0.7% at 22309, SMI +0.1% at 9267, S&P 500 Futures flat

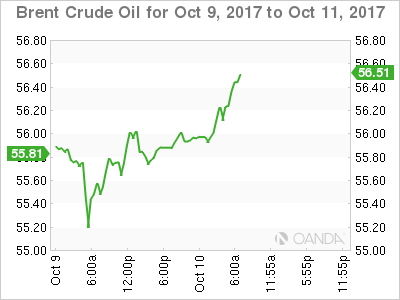

2. Oil prices rally as OPEC says market is rebalancing, gold shines

Oil prices have edged up overnight as OPEC said there were clear signs the market was rebalancing and as U.S production remained offline following Hurricane Nate.

Brent crude futures are up +12c, or +0.2% at +$55.91 a barrel, while U.S West Texas Intermediate (WTI) crude futures are trading at +$49.65 per barrel, up +7c, or +0.1% from their last close.

The OPEC-led production cuts started in January and are set to expire at the end of March 2018. Prices are supported as OPEC said oil markets were “rebalancing fast” after years of oversupply.

Stateside, +85% of U.S Gulf of Mexico oil production, or +1.49m bpd, remains offline following Hurricane Nate, according to the U.S Department of the Interior's Bureau of Safety and Environmental Enforcement.

Note: U.S API and EIA crude data are delayed to Wednesday and Thursday, respectively, because of Monday's U.S holiday.

Ahead of the U.S open, gold has rallied to a one-week high, but U.S rate hike prospects are curbing those gains. Geopolitical tensions and a softer U.S dollar has pushed the 'yellow' metal up +0.3% at +$1,287.31 an ounce.

3. Sovereign yields little changed

Catalan President Puidgemont's speech to the regional parliament today could prove crucial for the bond markets, as it may give the “all-clear” that a declaration of independence is not imminent. But this may not be enough to trigger losses in haven bunds, and boost yields.

Holders of eurozone government bonds or debt will receive around €100B of maturity payments until the end of the month, therefore investors should remain keen to buy product on dips. Germany's 10-year Bund yield fell -1bps to +0.44%, the lowest in two-weeks.

Elsewhere, the yield on 10-year Treasuries dipped -1 bps to +2.35%, while U.K's 10-year Gilt yield gained +1 bps to +1.365%.

4. Dollar under pressure

This morning's EUR (€1.1800) rally is a sign of confidence that for now the risk of Catalonian independence is just a Spanish problem. EUR gains are small, but still EUR/CHF (€1.1526) has managed to print a two-week high ahead of the U.S open.

In the U.K, sterling (£1.3200) continues to recover from last week's drop after U.K's PM May has won public support from Brexit hardliners in her cabinet after outlining contingency plans for leaving the E.U without a deal.

5. U.K's trade deficit widens

Data this morning showed that the U.K.'s trade deficit widened in August, which suggests that trade was still a drag on growth in Q3 despite a weak pound.

The deficit in goods trade widened to -£14.2B, compared with a revised -£12.8B in July. This is the widest deficit on record.

Digging deeper, the data including services saw the deficit for August at -£5.6B compared with -£4.2B in the previous month. Import volumes also rose +4.2% on the month, with gains in chemicals and machinery, while exports rallied only +0.7%.

The data highlights the U.K's hopes for rebalancing of their economy towards 'exports and investment' and away from 'consumption' continues to remain somewhat tenuous.

DAX Shrugs Off Strong German Trade Surplus

The DAX has ticked lower in the Tuesday session. Currently, the index is at 12,965.50, down 0.06% on the day. On the release front, Germany’s trade surplus climbed to EUR 21.6 billion, above the forecast of EUR 19.8 billion.

The robust Germany economy continues to hum in the third quarter. There was positive news on Tuesday, as the trade surplus hit a 12-month high. Manufacturing numbers have impressed, as Industrial Production surged 2.7%, the second-highest gain in 2017. Last week, Factory Orders gained 3.6%, its best performance since December 2016. Strong global demand for German goods, in particular automobiles, has been a boon for German industrial and manufacturing output. September PMIs were also solid, as the services and manufacturing sectors continue to show expansion. It could be smooth sailing for the robust Germany economy, with projections that the economy will expand 1.9% in 2017 and 2.0% in 2018. On Wednesday, the German government will release its forecast for GDP growth, as well as employment and inflation forecasts.

The Catalan constitutional crisis has shaken up Spain, and it remains unclear whether Catalan President Carles Puigdemont will unilaterally declare independence from Spain. Catalonians voted in favor of independence, but the national government has refused to negotiate with the Puigdemont about session. On Sunday, a demonstration against the referendum attracted some 350,000 people, in a show of support for the Spanish government. If Puigdemont declares independence, Spanish Prime Minister Mariano Rajo has promised to take drastic action, which could include dissolving the Catalan parliament and even arresting lawmakers. Investors are casting a nervous eye on the economic ramifications of the crisis. Two major banks, Caixabank and Sabadell, as well as several large corporations have announced they are relocating their legal headquarters from Barcelona to Madrid. The tensions have not affected the euro so far, but that could change if Catalonia defies Madrid and declares independence.

Euro Gains Ground, All Eyes On Catalonian Crisis

The euro has recorded gains on Tuesday. Currently, EUR/USD is trading at 1.1781, up 0.34% on the day. On the release front, Germany’s trade surplus climbed to EUR 21.6 billion, above the forecast of EUR 19.8 billion. French Industrial Production declined 0.3%, missing the forecast of a 04% gain. There are no major events out of the US. On Wednesday, the US releases JOLTS Job Openings and the Federal Reserve releases the minutes of the September policy meeting.

The Catalan constitutional crisis is going down to the wire, as it remains unclear whether Catalan President Carles Puigdemont will unilaterally declare independence from Spain, after Catalonians voted in favor of independence. The national government has refused to negotiate with the Puigdemont about session, and on Sunday, a demonstration against the referendum attracted some 350,000 people, in a show of support for the Spanish government. If Puigdemont declares independence, Spanish Prime Minister Mariano Rajo has promised to take drastic action, which could include dissolving the Catalan parliament. Investors are casting a nervous eye on the economic ramifications of the crisis. Two major banks, Caixabank and Sabadell, as well as several large corporations have announced that they are relocating their legal headquarters from Barcelona to Madrid. The tensions have not affected the euro so far, but that could change if Catalonia defies Madrid and declares independence.

The Federal Reserve did not raise rates at the September meeting, but the markets are clearly expecting one final rate hike in December. According to CME FedWatch, the odds of a December rate hike are currently at 86%, compared to just 31% a month ago. Why the huge turnaround? A strong US economy has helped raise the odds, but the primary reason for the huge shift in market sentiment can be attributed to the Fed policymakers that have come out in support of a rate hike, notably Fed Chair Janet Yellen. The lack of inflation remains the most significant impediment to raising rates, but Yellen and other FOMC members have insisted that strong economic conditions will lead to higher inflation levels. Even if inflation does not move higher before 2018, the Fed now appears ready to press the rate trigger.

May Strengthens Her Hand | Turkish Spat Continues | Catalonian Crisis Could Explode

Asian equities have outperformed the US stock markets this year

Theresa May has the support of her party and from the public

The weaknesses in the dollar could be a short-term thing

Prime Minister Rajoy would have no choice but to use the force to restore the order

The US is blaming Turkey for the recent crisis

Investors are increasingly optimistic about global stocks and this has pushed the global equity markets near a record high. Traders are constantly looking for a value play. Although Asian equities have outperformed the US stock markets this year, they are still relatively cheaper. Hence they may be more attractive. The German trade balance data released today showed further improvement and this is keeping the euro-dollar pair in the positive territory.

The bettering for Sterling comes to an end after traders realised that Prime Minister Theresa May has the support of her party and from the public. After every setback, she tends to make a comeback and this tells you something about her strong character. The tactic which won her this support was by highlighting that the UK could leave the EU without any Brexit deal. But the question remains how long it will take her to change her stance and until when this support will last? Moreover, Theresa May presented a different story to her party leaders; the EU leaders are keen to discuss and negotiate a deal with Britain. Her contrasting views reappeared when she told business leaders that the transition period could last for two years and they should curve up a strategy accordingly. These mixed messages would surely keep any upward move capped for the currency.

The mighty Dollar is experiencing some weakness against a basket of currencies ahead of the FOMC minutes (due this week). The weaknesses in the dollar could be a short-term thing and this is purely because the economic numbers have been strong despite the strong influence of the hurricane misery. The broader picture for the US economic health is improving somewhat and therefore, we do anticipate that there might be some more juice left for the dollar rally. The inflation data is also showing signs of life and this supports the Fed Hawkish stance. For instance, the ISM paid prices number not only confirmed the above argument but the reading came in at the strongest level since 2011. The average hourly number, the Fed’s favourite gauge for the labour market strength, experienced the largest jump since 2009. This pretty much confirms that the upcoming FOMC minutes could be on the hawkish side.

Over in Europe, just when you thought that the Catalonian crisis is over, things have taken a turn for the worse. Carles Puigdedemont could escalate the tensions during his address to Spanish leaders. A gradual independence has been dubbed by him so far and if he does make that announcement in the parliament it would mean more adverse pressure on the Spanish markets. Prime Minister Rajoy would have no choice but to use the force to restore the order. Investors’ sentiment is already adverse and foreign money is taking a step back as several companies have moved their operation.

The geopolitical tensions have faded, it is only calm before the storm. The US is blaming Turkey for the recent crisis and demanding an explanation for the arrest of the two employees at the American Embassy in Turkey. Both countries are NATO allies and any further rift between the two would only mean more trouble on the global investment stage. The Turkish Lira was the worst currency among emerging market currencies yesterday.Today it is no longer the worst but the third underperforming currency among emerging market currencies. The precious metal is still well above its recent low of $1260 and the technicals are suggesting that we could see more upside move for the metal.

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD, GOLD, WTI CRUDE, DJIA, FTSE100, DAX

EUR/USD

The EUR/USD pair managed to advance modestly this Monday, as half a holiday in the US, with Wall Street working, but pretty much everything else closed in the country, keeping majors within limited ranges. The pair ended the day marginally higher around 1.1750, merely 20 pips above Friday's close, with trading also restricted ahead of first-tier events that will take place later this week, starting this Tuesday, with the possibility of Catalonia declaring its independence from Spain, something the markets fear, but are still underestimating. Mid week, the Fed will release the Minutes of its latest meeting, while on Friday, it will offer final September inflation figures.

Data released this Monday in Europe was EUR-supportive, as German industrial production rose by more than expected in August, posting its biggest monthly increase in more than six years, up by 2.6% in the month, bouncing from July's 0.1% decline. When compared to a year earlier, production rose by 4.7%, from 4.2% in July. Also, the EU Sentix investor confidence jumped to 29.7 in October, its highest in 10 years, beating expectations of 28.5.

From a technical point of view, the pair has gained some bullish traction in the short term, but would take the price to settle above the 1.1820/30 strong static resistance area to see the pair actually turning positive and bulls daring for more. In the meantime, the 4 hours chart shows that the price advanced above 1.1730, which in the mentioned chart presents its 20 SMA, while the level also represents the 23.6% retracement of the April/September rally. Indicators in the mentioned chart head modestly higher after entering positive territory, supporting some additional gains up to the 1.1780 region, the immediate resistance. Below the mentioned Fibonacci support, on the other hand, the risk turns towards the downside, with scope then for a retest of the 1.1660 price zone.

Support levels: 1.1730 1.1695 1.1660

Resistance levels: 1.1780 1.1825 1.1850

USD/JPY

Following an early slide down to 112.31, the USD/JPY pair recovered, to end the day unchanged from Friday's close in the 112.60 region. The Japanese yen gapped higher at the weekly opening, on headlines indicating that North Korea is preparing to test a long-range missile that could reach the US West Coast, although with Japan on holidays, the movement was short-lived. Furthermore, US Treasury yields held near recent highs, with the 10-year note yield ending the day barely lower at 2.36% from Friday's 2.37%. In the macroeconomic front, Japan will release its current account and trade balance data for August, both expected below July's levels, whilst BOJ's Governor Kuroda is scheduled to speak, although there are little chances that he would add something new to its monetary policy stance. The pair has been trading uneventfully ever since reaching the 113.00 region, confined to a tight consolidative range for more than two weeks already, after adding around 600 pips from its September bottom, waiting for a catalyst that will give it the next directional impulse. Short term, the pair presents a neutral-to-bullish stance, give that the price is holding above its moving averages, with the 100 SMA heading higher around 112.30, providing an immediate support, followed by 112.00, the 23.6% retracement of the September run. Technical indicators in the mentioned chart, however, continue lacking directional strength, holding around their mid-lines. The pair would need to advance beyond 113.45, the high set last week, to be able to extend its bullish run during the following sessions.

Support levels: 112.30 112.00 111.65

Resistance levels: 113.00 113.45 113.80

GBP/USD

The Pound was among the best performers against the greenback this Monday, correcting part of last week's slump. The GBP/USD pair jumped to 1.3183 early London, following news that after the UK’s Office for National Statistics announced a correction of employment inflation data, raising the Q2 unit labor costs to 2.4% from the previous estimate of 1.6% YoY. Later on the day, UK's PM Theresa May delivered a speech to the parliament on Monday, as usual full of hopes. This time, she said that the "ball is in their court," referring to the EU negotiators so it's their time to make proposals at a new round of talks opening the way to the next stage of negotiations. She additionally said to business leaders that companies should thing of a two-year transition period as assured. After the early advance, the pair retreated modestly, but held on to gains at the end of the day, entering the Asian session with a short-term positive technical outlook, as in the 4 hours chart, indicators aim higher, entering positive territory, whilst the price settled above an anyway bearish 20 SMA. The same chart shows also that the price was unable to rally beyond the 38.2% retracement of last week's decline, at 1.3170, now the immediate resistance.

Support levels: 1.3110 1.3065 1.3025

Resistance levels: 1.3170 1.3210 1.3250

GOLD

Gold prices extended their advance at the beginning of the week, with spot edging up to $ 1,285.40 a troy ounce, to close it modestly below the level. Gains were triggered by resurgent demand from safe-haven assets on renewed concerns over the US-North Korea conflict. A softer greenback across the board, added to the metal's gains. These last two-day's recovery seems corrective as the price currently stands around the 23.6% retracement of the September/October slide. Daily basis, technical indicators have lost oversold conditions, but pared their recovery within negative territory, whilst a strongly bearish 20 DMA offers an immediate resistance at 1,288.70. In the same chart, the price has managed to regain ground above a flat 100 DMA after bottoming around the 200 DMA last week, a sign that the bearish momentum eased long term. In the 4 hours chart and for the upcoming sessions, the risk is slowly gyrating towards the upside, as indicators aim north within positive territory, whilst the price has surpassed its 20 SMA. Further gains beyond the 1.288.70 level are required to confirm a stepper advance that can extend up to 1,297.45, the 38.2% retracement of the mentioned slide.

Support levels: 1,268.30 1,260.50 1,252.90

Resistance levels: 1,282.15 1.294.25 1,303.95

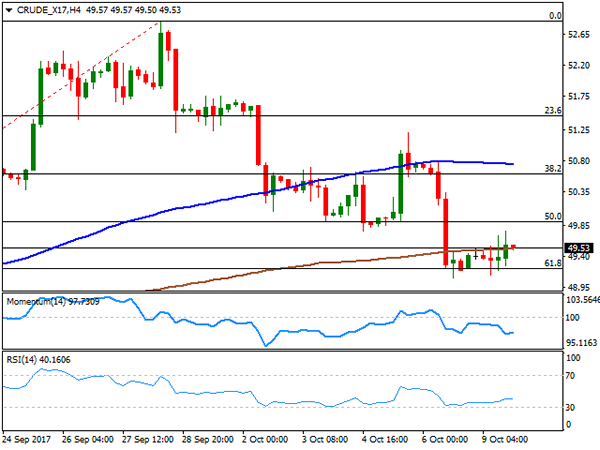

WTI CRUDE OIL

West Texas Intermediate crude oil futures edged higher, ending the day at $49.54 a barrel, after trading as high as 49.77 intraday, on comments from OPEC's secretary general Mohammad Barking, who said that the oil market is rebalancing fast and has almost entirely erased the glut of refined products. Furthermore, the organization signaled the possibility of an extension of its output cut deal. The daily chart for the US barrel shows that the price held within Friday's range lower end, but above a major Fibonacci support around 49.20, the 61.8% retracement of its latest bullish run. Indicators in the mentioned time frame lost their bearish strength, but hold flat within negative territory, suggesting buying interest remains limited at the time being. Shorter term and in the 4 hours chart, the upward potential is also limited, with indicators lacking directional strength within negative territory, and the price hovering around its 200 SMA. The commodity needs to advance above 49.90, the 50% retracement of the mentioned decline, to have a more constructive outlook for the upcoming sessions.

Support levels: 49.20 48.80 48.30

Resistance levels: 49.90 50.60 51.10

DJIA

The Dow Jones Industrial Average rallied to a record high early Monday, but closed in the red, as well as all US major indexes, in a dull trading session. The index lost 12 points, to end the day at 22,761.07, while the S&P lost 4 points, to end at 2,544.73. The Nasdaq Composite also lost ground down 10 points to 6.579.73. Within the Dow, Wal-Mart Stores was the best performer, up 1.80%, followed by IBM which added 0.61%. General Electric, on the other hand, was the worst performer, down 4.37% after an activist shareholder was appointed to the board of directors. Nike followed, down by 1.71%. The Dow peaked at 22,802 a new all time high before trimming intraday gains, confined anyway to a tight range amid a holiday in the US and Canada. Technical readings in the daily chart still favor additional gains ahead, as indicators picked up within overbought readings, whilst the price remains far above all of its moving averages. In the short term, however, the index is barely holding above its 20 SMA, meeting buying interest around it, the immediate support at 22,735, while the Momentum indicator retains its downward strength, heading south around its mid-line, as the RSI consolidates around 68, all of which favors a downward extension for this Tuesday, on a break below the mentioned support.

Support levels: 22,743 22,695 22,651

Resistance levels: 22,790 22,850 22,900

FTSE100

The FTSE 100 lost roughly 15 points, to end the day at 7,507.89, as local equities suffered from a stronger Pound. Market rumors indicating that PM Theresa May could reshuffle its cabinet to recover her lost authority brought some relief after speculation she may be forced to call for a snap election. The political situation is still unclear, and will be a weight for both, the currency and the index, beyond intraday moves. In London, Reckitt Benckiser was the best performer, up 1.49%, followed by Admiral Group, which added 1.195. Anglo American was the worst performer, down 3.38%, followed by Rio Tinto that shed 2.24%, as mining-related equities couldn't shrug off Chinese negative news. Technically, the movement seems barely corrective according to the daily chart, as indicators are retreating from overbought territory, whilst the index holds above its 20 and 100 DMAs. In the 4 hours chart, and for the shorter term, further slides are likely, as the index ended the day a few points above its 20 SMA, whilst technical indicators retreated further from overbought levels, losing downward strength within positive territory, but still leaning the scale towards the downside.

Support levels: 7,444 7,408 7,371

Resistance levels: 7,513 7,552 7,599

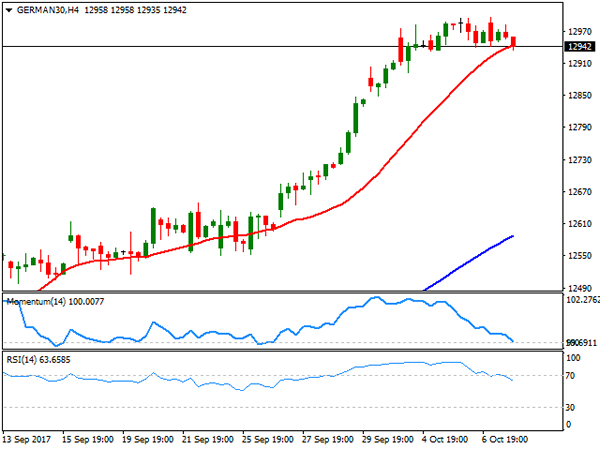

DAX

The German DAX added 20 points, or 0.16% this Monday, to end at 12,976.40, as European equities edged marginally higher on a recovery of the Spanish IBEX. Fears that Catalonia may declare its independence from Spain on Monday, eased partially ahead of the key parliamentary meeting that would take place this Tuesday, as anti-separatists marched in Barcelona on Sunday. In Germany RWE AG was the best performer, up 2.34%, followed by E.ON which added also 2.34%. Deutsche Bank led decliners, down by 1.94%, followed by Linde that lost 1.66%. The daily chart for the index shows that it settled at the lower end of its latest range, but still at record highs, and while technical indicators eased partially from overbought readings, the index remains far above all of its moving averages, suggesting that the long-term ruling trend remains firm in place. Shorter term, and according to the 4 hours chart, the downward potential increased, as the index is pressuring its 20 SMA, the Momentum indicator heading south around its 100 level, whilst the RSI retreats strongly from overbought levels, now around 63.

Support levels: 12,935 12,893 12,849

Resistance levels: 12,971 13,015 13,045

Technical Outlook: WTI OIL – Recovery Extension Cracks $50 Barrier

WTI Oil holds firm tone on Tuesday and extends recovery from correction lows at $49.09/12 (Fri/Mon lows), to test psychological $50.00 barrier.

Monday's close above 200SMA was bullish signal for further upside, with fundamentals also being supportive, as OPEC said on Monday that there is clear evidence the market is rebalancing after few years of oversupply which depressed oil prices.

Close above $50 will be another positive signal with extension above $50.52 (Fibo 38.2% of $52.84/$49.09 pullback / converged 10/20SMA's) to generate initial reversal signal.

Near-term action is holding in thick hourly cloud and eyeing cloud top at $50.15, with cloud base at $49.64, offering solid support and expected to ideally contain dips.

Only return below 200SMA ($49.42) would generate bearish signal and risk retest of recent lows at $49.12/09, reinforced by 55SMA.

Res: 50.06; 50.52; 50.80; 50.97

Sup: 49.64; 49.42; 49.09; 48.35

Technical Outlook: SPOT GOLD Extends Recovery On Geopolitical Tensions, Higher Demand

Spot Gold remains in green for the third straight day and extends recovery, driven by weaker dollar, persisting geopolitical tensions over North Korea in increasing physical demand from India and China.

Fresh upside action on Tuesday broke above barrier at $1287 (50% retracement of $1313/$1260 downleg) and approaching $1290 (4-hr cloud top. Break here would expose key resistances at $1297 (Fibo 38.2% of entire $1357/$1260 descend) and $1302 (daily cloud top).

Initial support lies at $1282 (session low) with stronger corrective dips to be contained by broken 10SMA ($1278).

Res: 1290, 1293, 1297, 1301

Sup: 1282, 1278, 1275, 1272

Technical Outlook: AUDUSD: Daily Cloud Base Limits Recovery Attempts For Now

The Aussie dollar regained positive tone on Tuesday and extended recovery near key barrier at 0.7800 (daily cloud base / Tenkan-sen). Sustained break here is needed to generate stronger bullish signal for further recovery.

The notion is supported by daily RSI / slow stochastic which turned higher after touching oversold territory boundary.

Close above daily cloud base would signal recovery extension towards pivotal barrier at 0.7874 (Fibo 38.2% of 0.8102/0.7732 downleg / 04 Oct lower top).

However, overall bullish structure and thick daily cloud weigh on the price and may limit recovery.

The downside is expected to remain under increased risk while the price remains below the cloud and could start fresh downside action on completion of current consolidation phase.

Break below last Friday’s new low at 0.7733 (the lowest since 14 July) would open way for continuation of broader downtrend from 0.8124 and expose next strong support at 0.7670 (200SMA).

Res: 0.7800, 0.7820, 0.7874, 0.7917

Sup: 0.7774, 0.7747, 0.7733, 0.7670