Sample Category Title

BoE Stands Pat On Interest Rates, Signals At An Interest Rate Hike In Coming Months

For the 24 hours to 23:00 GMT, the GBP rose 1.42% against the USD and closed at 1.3403, after the Bank of England (BoE) struck a hawkish tone at its latest monetary policy meeting.

The BoE, as widely expected, left the benchmark interest rate unchanged at a record low of 0.25%, with two of its nine policymakers voting for an immediate interest rate hike. Further, the central bank maintained its asset purchase facility at £435.0 billion. In a post meeting statement, the BoE Governor, Mark Carney, acknowledged that possibility of a rate hike has definitely increased and some “calibration” of monetary stimulus will be needed in the coming months. According to minutes of the meeting, majority of officials expressed the view that interest rates are likely to rise at a faster pace in the coming months, to combat inflation and as the economy continues to strengthen.

In the Asian session, at GMT0300, the pair is trading at 1.3392, with the GBP trading 0.08% lower against the USD from yesterday’s close.

The pair is expected to find support at 1.3229, and a fall through could take it to the next support level of 1.3067. The pair is expected to find its first resistance at 1.348, and a rise through could take it to the next resistance level of 1.3569.

Going ahead, traders will keep a close watch on the BoE’s quarterly bulleting report, scheduled to release in a few hours.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the USD slightly declined against the JPY and closed at 110.43.

In the Asian session, at GMT0300, the pair is trading at 110.16, with the USD trading 0.24% lower against the JPY from yesterday’s close, as investors lured to safe haven currency after North Korea fired its second missile over Japan, shortly after the United Nations approved sanctions against Kim Jong-Un’s regime.

The pair is expected to find support at 109.95, and a fall through could take it to the next support level of 109.74. The pair is expected to find its first resistance at 110.51, and a rise through could take it to the next resistance level of 110.86.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

SNB Left Its Key Interest Rate On Hold

For the 24 hours to 23:00 GMT, the USD rose 0.36% against the CHF and closed at 0.9667.

Yesterday, the Swiss National Bank (SNB) kept the key interest rate unchanged at -0.75%. Additionally, the central bank reiterated its commitment to “intervene in the foreign exchange market as necessary”.

In the Asian session, at GMT0300, the pair is trading at 0.9633, with the USD trading 0.35% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9605, and a fall through could take it to the next support level of 0.9577. The pair is expected to find its first resistance at 0.9675, and a rise through could take it to the next resistance level of 0.9717.

Moving ahead, traders will focus on Switzerland’s SECO economic forecasts report and the nation’s trade balance data, both set to release next week.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

Canada’s New House Prices Advanced As Expected In July

For the 24 hours to 23:00 GMT, the USD rose 0.14% against the CAD and closed at 1.2179.

In economic news, Canada's new house price index rose 0.4% on a monthly basis in July, in line with market expectations. In the prior month, the index had recorded a rise of 0.2%.

In the Asian session, at GMT0300, the pair is trading at 1.2180, with the USD trading slightly higher against the CAD from yesterday's close.

The pair is expected to find support at 1.2169, and a fall through could take it to the next support level of 1.2159. The pair is expected to find its first resistance at 1.2189, and a rise through could take it to the next resistance level of 1.2199.

Ahead in the day, market participants will focus on Canada's existing home sales data for August.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

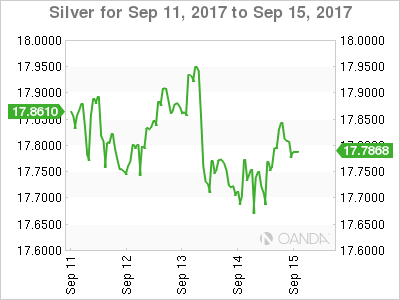

Gold And Silver Yawn At North Korea

Gold and Silver continue their healthy consolidations as we reach the week’s end, ignoring North Korea’s latest missile test.

Gold

Gold rose slightly this morning after the latest North Korea missile test, but overall, the reaction was muted. Gold touched 1334.00 before falling back just as quickly to the unchanged level of 1330.00 in Asia trading. We would expect dips to be sought after in Asia and North America today as trader put on weekend risk hedges, but it would appear that a certain level of North Korea apathy has set in as the big dollar marks time into the end of the week.

Although gold has fallen from extremely overbought levels in the short term, the longer term picture will remain constructive. Pleasingly, the Relative Strength Index (RSI), has now fallen from stratospheric overbought levels to neutral ones. We cannot rule out further corrections and a retest of the pull back lows of 1315.00, but the technical picture remains constructive as Long as the 1296.00/1300.00 breakout levels remain intact on a daily closing basis.

Gold has nearby resistance at 1335.00 followed by 1347.00, a level unlikely to be seen ahead of the weekend. Given it has held up very well in light of the overnight higher U.S Core CPI data, Traders will be closely watching this evenings Retail Sales numbers. Another better than expected number could lead to U.S. dollar strength and continue to cap gold into the weeks end.

Silver

Silver meanwhile, continues its corrective pullback as well.Overall it has held up better then gold but faces short-term resistance at 17.8800, just above its current 17.7900 trading level. Beyond there looms the 18.2500 area, the previous high, which will be a far more formidable test.

While its RSI has also moved back to neutral, a retest of 17.6000 support cannot be ruled out. However longer term support at 17.2800 is the key technical support and Silver’s longer-term picture remains sunny as long as this holds.

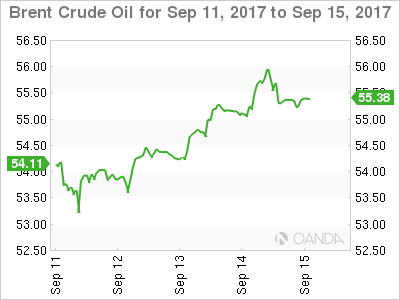

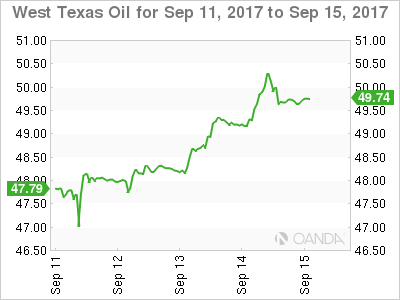

Brent Crude’s Moment Of Truth Looms

Exciting times for oil as we head towards the end of the week, with WTI rallying over 1.0% and Brent 0.5% as North Korea's missile test iced the cake of a bullish technical picture for both contracts.

Late New York saw WTI spot spike through the $50.00 mark to touch $50.50 before falling back to a more sedate $49.85 in Asia mid-session trading. Brent scrambled to $56.10 before settling at a still respectively $55.70 during the Asia session. WTI's move in particular, looked very stop loss driven as the $50.00 mark broke. But there shallowness of the pullback in both contracts can be seen as positive.

With the EIA upgrading oil consumption forecasts, U.S refining quickly recovering from hurricane induced shutdowns and OPEC suggesting inventories are falling, the picture has been one of good news this week for crude generally.

Brent

From a technical perspective Brent in particular though is approaching its moment of truth. It is now just one dollar away from the mega resistance region of 56.50/57.00 that has capped gains for all of 2017. Another failure here would imply a potentially deep correction could be on the cards, while a daily close above sets the stage for a test of 60.00 which would no doubt bring smiles to the faces of Saudi Aramco's IPO team.

Longer term support is at 52.15 where Brent's 200-day moving average and its Long-term trandline support meet today. In the bigger picture, Brent remains technically constructive above this level.

WTI

WTI spot has broken out of its range between its 100 and 200-day moving averages but must close above the 50.00 mark to give bulls renewed energy. Initial resistance is at the overnight high at 50.50 followed by the May highs at 51.65. Critical support is at 49.30 today. This being a previous triple TOP and the 200-day day moving average.

Market Morning Briefing: The Aussie Continues To Hold Above Support At 0.7950

STOCKS

Dow and Dax look strong while the other indices may trade sideways or try to come off a bit in the near term.

Dow (22203.48, +0.20%) is trading higher, breaking the previous high of 22200. If the rise sustains, the index could rally towards 22300-22400 soon.

Dax (12540.45, -0.10%) is stable and could move higher towards 12750-13000 in the medium term as mentioned yesterday. Also note there could be a slight pause near 12675 levels.

Nikkei (19826.84, +0.10%) is trading slightly lower but overall looks bullish towards 20000-20100 in the coming sessions. However, we could see some sideways movement above 19750 for sometime.

Shanghai (3360.12, -0.34%) made an intra-day low of 3345, but has not been able to sustain those levels today. A sustained break below 3350 is seen could take the index down towards 3325 in the coming sessions.

Nifty (10086.60, +0.07%) is stable just below immediate resistance near 10140 and while that holds, a small dip from current levels is possible. Only on a break above 10140, we would look for fresh bullish possibilities just now.

COMMODITIES

Brent (55.24) saw a high near 55.99 yesterday and might try for higher levels as well if it manages to remain above near term Support near 54.65. The WTI (49.68) may also try to move up towards 52 in the coming weeks if it manages to remain above 49 now.

The Gold-WTI ratio (26.88) has been dipping from long-term Resistance at 28.51 at the beginning of the month. Need to see if it holds above near-term Support at 26.00 or not.

Gold (1335) has bounced from 1319.50 yesterday. There can be some debate as to where it has Support now - whether just below 1320 or deeper down near 1310. The bearish possibility of 1300 mentioned yesterday might be a little overdone.

Copper (2.964) stalled in its downtrend a bit yesterday but is likely to continue to lose ground towards 2.90.

FOREX

August US CPI came in at 1.9% yesterday, compared to expectation of 1.8% and 1.7% in July. This sent the Euro (1.1911) down momentarily to 1.1836 and Dollar-Yen (110.18) up to 111.04. The Dollar Index (92.13) rose to 92.66.

However, as it turns out, the Euro remained above Support at in the US session itself, in line with expectation. And then today's early morning missile firing by North Korea pushed it up further. The Yen also strengthened and the Dollar Index came down well below 92.50 again.

We now need to watch the German-US 10Yr Yield Spread (-1.77%) of course. This has held above the Support at -1.79% and is indicative of Euro strength, which can move up to 1.1950+ again. Likewise, the Dollar Index can come down towards 91.80 or lower.

Dollar-Yen (110.18) may be ranged between 110.70-109.70 today. The Euro-Yen (131.19) saw a dip to 130.50 yesterday and remains well below the Resistance at 132.00. Expect a range of 132.25-130.00 for the next few days.

The Pound (1.3389) surprised by jumping up after the BOE hinted at a rate hike to a high of 1.3405. However, it would be good to be wary of long-term Resistance between 1.3415-65.

The Aussie (0.7995) continues to hold above Support at 0.7950 and has decent chances of seeing 0.8025 over the next two-three days.

Increasing chances that Dollar-Yuan (USDCNY = 6.5476) will move up towards 6.60 over time. In Dollar-Rupee, we see 60% chances that the Range Resistance at 64.20 will hold good today.

INTEREST RATES

UK Yields had been rising since the beginning of the week, possibly in anticipation of a hint of a rate hike by the BOE. But, there is Resistance near the current levels on the 20Yr (1.746%) and on the 10Yr (1.23%). So, it might seem that the rate hike prospect is priced in for now.

Looking at the larger trend in the German 30Yr (1.22%), UK 20Yr (1.746%) and Japanese 10Yr (0.02%) yields, there are Resistances available just overhead on all of them.

The US 10Yr (2.18%) and US 30Yr (2.76%) have not moved up much after the slightly higher than expected US CPI data. Resistances at 2.25% and 2.80% remain valid and intact for now. The 2Yr (1.36%) has moved up a bit compared to 1.34% earlier.

Let us see if US yields move up further from here. The market will possibly go into wait and watch mode ahead of the FOMC meeting on 20th September, next week.

Tightening Back On The Agenda

Global coordinated monetary policy tightening is back in play after a hawkish shift and the BOE and a bump in US fortunes. The pound soared after the MPC while the New Zealand dollar lagged. The Asia-Pacific calendar is light later but there are rumors of a North Korean launch. Our Premium long in GBPUSD hit its final target for 230 pip gain.

The MPC said some withdrawal of stimulus is likely in the coming months in a move that came as somewhat of a surprise. The pound climbed 150 pips on the headlines and added another 50 when Carney revealed he too thinks the possibility of a hike has “definitely increased.” Cable ran to 1.3400 in a fresh cycle high and finished at the best levels of the day.

The US dollar caught a bid early in the day after CPI rose 1.8% compared to 1.7% expected. Not long after the data, the questions started to mount. Wage numbers were soft and it appeared inflation was boosted by an unusual jump in shelter prices.

Chatter about a weak retail sales report on Friday also did the rounds, in part due to skews from Hurricane Harvey. Finally, Mnuchin sounded a worried note no growth late in the day that contributed to USD/JPY selling down to 110.25 from a high of 111.04.

Finally, Bitcoin fell 13% after China announced it will shut all local exchanges by the end of the month. It last traded at $3348.

Gold Shrugs as CPI Beats Estimate, Unemployment Claims Dip

Gold has ticked higher in the Thursday session. In North American trade, the spot price for an ounce of gold is $1325.07, up 0.13%. On the release front, CPI and Core CPI both improved in August. CPI gained 0.4%, edging above the forecast of 0.3%. Core CPI gained 0.2%, matching the forecast. There was more good news from the labor market, as unemployment claims fell to 284 thousand, well below the forecast of 303 thousand.

Gold prices are linked to interest rate moves, so gold investors are keenly following the Federal Reserve and looking for hints regarding a rate policy. What can we expect from the Federal Reserve in the fourth quarter? Earlier in 2017, the Federal Reserve was full of optimism that a strong US economy would warrant three rate hikes during in 2017. Fast forward to September – the economy has generally performed well, but the US continues to grapple with weak inflation levels. A strong labor market has not helped push inflation higher, as wage growth remains soft. Fed policymakers have retreated from their earlier optimistic forecasts, and have been counseling caution and patience regarding rate increases. As for a December hike, the odds have been below 50% for months. Currently, the odds are pegged at 46%, which is an improvement from last week. However, the positive August CPI data could be a sign that at long last, inflation is moving in the right direction. If the markets feel this is the case, the odds of a December hike should increase.

Gold has posted two straight winning weeks, but that streak could be over, as the metal is down about 1 percent this week. Much of the loss can be attributed to the easing of tensions in the Korean peninsula. As a safe-haven asset, gold had moved higher in recent weeks, as tensions increased over North Korea's nuclear program. North Korea fired missiles over Japan and tested a nuclear device, drawing sharp reactions from the US, Japan and South Korea. However, a lull in the crisis has seen investors return to risk assets, triggering lower gold prices. Still, North Korea remains a geopolitical hot spot, and investors could flock back to gold if the war of words between US President Trump and North Korean President Kim Jong-un escalates and Kim decides to shake things up in the region with a missile launch or nuclear test.

Pound Jumps Above 1.34 as BoE Hints at Rate Hike

The British pound has surged in the Thursday session. In North American trade, GBP/USD is trading at 1.3393, up 1.40% on the day. On the release front, the Bank of England held the benchmark rate at 0.25%, but hinted at a rate hike before the end of the year. In the U.S., CPI and Core CPI both improved in August. CPI gained 0.4%, edging above the forecast of 0.3%. Core CPI gained 0.2%, matching the forecast. There was more good news from the labor market, as unemployment claims fell to 284 thousand, well below the forecast of 303 thousand.

As expected, Mark Carney & Co. opted to hold interest rates at 0.25%, where they have been pegged since August 2016. There have been calls for the BoE to raise rates in order to fend off high inflation levels, but most policymakers are of the opinion that current economic conditions do not warrant a rate hike. However, what surprised the markets was the minutes of the September rate decision, in which the BoE said that if current economic conditions continue, then "withdrawal of monetary stimulus is likely to be appropriate over the coming months in order to return inflation sustainably to target". The strong guidance from the BoE was unusual, and set the stage for a likely rate hike in November, when the BoE holds its next policy meeting. Investors reacted positively to the hawkish message from the bank, sending the pound sharply higher. At the same time, Monetary Policy Committee (MPC) members have remained consistent in their views on interest rate hikes – seven members voted to hold rates, with two members favoring a rate hike. This outcome was identical to the market forecast of the MPC interest rate vote.

Earlier in the year, the Federal Reserve was full of optimism that a strong US economy would warrant three rate hikes during in 2017. Fast forward to September – the economy has generally performed well, but the US continues to grapple with weak inflation levels. A strong labor market has not helped push inflation higher, as wage growth remains soft. Fed policymakers have retreated from their earlier optimistic forecasts, and have been counseling caution and patience regarding rate increases. As for a December hike, the odds have been below 50% for months. Currently, the odds are pegged at 46%, which is an improvement from last week. However, the positive August CPI data could be a sign that at long last, inflation is moving in the right direction. If the markets feel this is the case, the odds of a December hike should increase.