Sample Category Title

GBP Soars on BoE Rate Hike Admission

The Bank of England threw its name into the hat of central banks that could still raise interest rates this year when released the minutes from its monetary policy meeting today.

While traders were initially looking for a change in the voting – which remained at 7-2 in favour of no change – the clues were actually in the minutes, resulting in a sharp u-turn from the initial moves. Traders were anticipating at least one more vote in favour of a rate hike which would have represented a potential shift of power within the MPC but instead it was the minutes that were used to signal a possible hike in the coming months, the result being that sterling's drop was immediately reversed and the currency is now up around 1% on the day against the dollar and the euro.

The admission that some withdrawal of stimulus is likely over the coming months, inflation will now likely rise above 3% and spare capacity has been absorbed faster than expected thereby reducing policy makers tolerance of above-target inflation is very hawkish and strongly suggests a rate hike is coming. It seems policy makers are not willing to wait and see whether the above-target inflation is in fact transitory or if it has become more ingrained but I guess the actions taken last year allow them the opportunity to act while remaining as accommodative as they were prior to the Brexit vote.

The question now is how far can the pound go. The next test against the dollar is 1.35, a break of which would be very surprising as it would signal a move back towards the kind of levels we were seeing prior to the Brexit vote. Against the euro, we've broken back below 0.90 and currently trade below 0.89 and so the next test below could come around 0.8850 and 0.88 below that.

With the BoE now joining the Bank of Canada and the Federal Reserve is contemplating rate hikes and the ECB looking to withdraw more stimulus, it's going to be a very interesting end to the year.

Turkey’s Central Bank Holds Rates Steady

Turkey's central bank held its main interest rates steady this morning, in line with expectations.

The Monetary Policy Committee (MPC) kept the one-week repo rate at +8%. It held the overnight lending rate at +9.25% and held the overnight borrowing rate at +7.25%.

Note: Policy makers also kept the late-liquidity lending rate at +12.25% – the surcharge premium charged to domestic banks to borrow.

"The central bank will continue to use all available instruments in pursuit of the price stability objective. Tight stance in monetary policy will be maintained until inflation outlook displays a significant improvement," the central bank said in a statement.

Hawkish Rate “Hold” Elevates Sterling

Investors who were anticipating that soaring inflation in the UK would convert some BoE doves, were left slightly disappointed on Thursday, after the MPC voted 7-2 in favor of keeping the rate unchanged.

The initial disappointment triggered a knee-jerk reaction lower on the GBPUSD, before prices rebounded higher, as market players digested the hawkish policy statement. With the central bank stating that it could "reduce stimulus in the coming months" if inflationary pressures continue to mount, Sterling is likely to remain supported this week.

While the Bank of England has indicated that interest rates could rise faster than markets expect, if the economy keeps growing, actions will always speak louder than words. It should be kept in mind that the unsavory combination of rising inflation, subdued wage growth and Brexit uncertainty has placed the central bank in a very tight spot. It becomes a question - will the BoE eventually raise rates to tame inflation, which is currently squeezing UK household? Or will tepid wage growth, concerns over the health of the UK economy and Brexit uncertainty keep the central bank on standby?

Things could get more interesting for Sterling moving forward, with more volatility expected as the currency becomes increasingly sensitive to monetary policy speculation.

From a technical standpoint, the GBPUSD bulls have won the battle this week, as the currency trades to a fresh yearly high above 1.3320. Prices are bullish on the daily charts, with today's hawkish boost by the BoE likely to support a further incline towards 1.3400. This bullish setup remains valid, as long as prices can keep above the 1.3150 higher low.

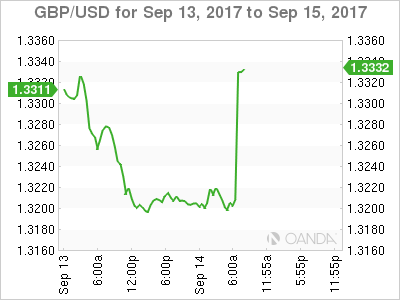

GBPUSD Spikes after BoE Minutes

The GBPUSD pair has moved to trendline resistance, hitting 1.3310, after the Bank of England Minutes revealed that BOE policy makers think that 'some withdraw of monetary stimulus will likely be appropriate over the coming months'.

Sterling had earlier spiked lower to 1.3153, as the BOE kept interest rates on-hold, with Monetary Policy Committee members voting 7-2, which was in-line with most economist's expectations.

The GBPUSD pair has regained bullish momentum, with traders now looking for further daily time-frame price closes above the key 1.3268 level, for further confirmation of continued upside.

Key technical resistance above the 1.3310 level is located at 1.3328, 1.3348 and 1.3380. Above the 1.3380 level, the GBPUSD pairs 100-week moving average is located at 1.3398.

Key intraday GBPUSD technical support below the key 1.3300 level is located at 1.3289, 1.3268 and the pairs daily pivot point, at 1.3252.

USDJPY Awaits US Data

The USDJPY recent risk-reversal remains intact, with price-action still well bid around the 110.40 level, after the pair moved to its highest trading level since July 16th, hitting 110.73 during the Asian session.

Traders will now look to next large directional move in the U.S dollar index, following the upcoming release of key U.S inflation and weekly jobs data.

The USDJPY pair is starting to make a bullish inverse head and shoulders pattern on the lower time frame price charts, with a three-hundred and fifty pip upside projection.

Key intraday technical resistance is found at the 100-day moving average, at 110.82 and the July swing high, at 111.04. Further resistance is found at the 200-day and 200-week moving average, at 111.53-54.

Key intraday technical support is located at the USDJPY 50-day moving average, at 110.25, and the pairs daily pivot point, at 109.90.

Once below the 109.90 level, further support is located at the 100 and 200-hour moving averages, at 109.47 and 109.47.

China: Don’t Trust the Weaker Data Too Much

Chinese growth data disappointed overnight pointing to weaker growth in both industrial production, fixed investment and retail sales. While we have expected China to slow down this year, I believe there are reasons to take the data with a grain of salt as they do not fit with what you see in for example PMI manufacturing and metal prices, which both pointed to a rebound into the summer. As often the case, Chinese data seems to be pointing in different directions at the moment.

We do expect growth to slow in China over the next 12 months as housing - and most likely infrastructure investment - cools on the back of policy tightening. But we are not sure the slowdown is happening already as the official data today says.

So what did the data say: Industrial production fell to 6.0% y/y in August (consensus 6.6% y/y) from 6.4% y/y. Fixed asset investments (in current prices) fell to 7.8% y/y in August (consensus 8.2% y/y) from 8.3% y/y. Retail sales dropped to 10.1% y/y in August (consensus 10.5% y/y) from 10.4% y/y. So disappointments across the board pointing to more slowdown than expected.

However, the reason we are a bit sceptical is illustrated below.

First, headline industrial production has not been in line with the signals from PMI manufacturing since 2012. And according to these numbers Chinese manufacturing has seen broadly flat growth since 2015 (apart from a temporary lift higher) although there is plenty of evidence that activity has gone up. PMI is up, profits are up, producer prices are sharply up and not least global metal prices (of which China consumes 50%) are much higher since early 2016. Metal prices have increased a lot over the summer as well.

Second, we trust more some of the sub-components in the industry numbers. For example steel production. This has increased a lot in recent months in line with the increase in PMI and metal prices.

Third, electricity generation has rebounded again lately after falling earlier in the year. Hence, the same picture as PMI and steel production as well as metal prices.

So where does this leave us? We are sceptical that China has really slowed during the summer - even though it would have been better in line with our own scenario. But it simply doesn't fit with all the indicators we trust the most when it comes to China? Why do we trust them more? Because they are statistics that are independent of each other yet highly correlated and painting a similar picture - and in line with what we see in commodity markets that tend to be correlated with activity in China.

When it comes to overall fixed asset investments they have shown a steady decline since 2010. It fits well into a rebalancing story in China, but it does not fit well with the indicators I mention above. A lot suggests that investments in construction and infrastructure have driven a pick-up in overall investments over the past year. Something we expect to fade soon due to the tightening measures from PBoC and the regulators.

The retail sales data also disappointed today - but overall the numbers have been moving sideways for the past 2-3 years. So not worsening but also not improving.

Stronger-than-Expected Australian Labor Data Push Aussie Higher

The aussie was hovering around a 10-day low of $0.7970 during early Asian hours when upbeat labor figures out of Australia for the month of August lifted the currency slightly above the $0.80 key-level. However, improving conditions in the labor environment are said to do little for interest rates to rise from record-low levels as price pressures remain subdued. According to the Australian Bureau of Statistics, the economy added 54,200 jobs in August instead of the 15,000 expected and almost twice the previous mark, posting an increase for 11 months in a row. Regarding full-time positions, those jumped by 40,100 after falling by 19,800 in July (downwardly revised from 20,300). Although 269,000 positions were created this year, the unemployment rate in August remained flat at 5.6% as the labor force also rose by a similar amount of 257,000. The participation rate picked up by 0.2 percentage points to a 5-year high of 65.3%, surprising analysts who anticipated the rate to stand flat at July's mark of 65.1%.

Despite the labor market building momentum, recent figures showed that wage growth was stuck at a record-low level of 1.9% y/y in the second quarter. In the same timeframe, inflation dropped unexpectedly to 1.9% y/y, far below the RBA's target range of 2-3%. A reasoning behind this could be that jobs are mostly rising in service sectors (which represent two-thirds of the labor market), where firms tend to pay less. Moreover, consumers are seeing their disposable incomes squeezed as they are struggling to repay their record level of mortgage debts. Therefore, a rate hike in October is unlikely to emerge given the weakness in prices and the record-high household debts even though the economy has been growing for 26 years without a recession. In the forex markets, the aussie partially reversed Wednesday's losses, jumping by 0.56% to $0.8015 during the Asian trading hours. However, a stream of disappointing Chinese data published a few hours later weighed on the currency, driving it lower to $0.8005.

UK Gilts Yields Rise, GBP Higher, FTSE Lower

Yields on U.K. government bonds have rallied across the curve as the Bank of England adopts a more "hawkish" tone.

The majority of Monetary Policy Committee members think "some withdrawal of monetary stimulus is likely to be appropriate over the coming months."

Also supporting yields is the BoE now expects inflation to rise above +3% in October.

Two-year gilt yields have rallied to +0.32%, their highest level since July and sharply up since levels of +0.13% only last week. Five, 10 and 30-year yields are also backing up.

The FTSE 100 is trading down -0.36% as GBP/USD trades up +0.8% at £1.3320 and EUR/GBP is down -0.82% at €0.8926.

BoE Inflated Pound for Strong Acceleration

Cable spiked lower to session low at 1.3148 on knee-jerk reaction after BoE's left no surprise on 7-2 vote for rate hike on today's meeting. The Bank of England left interest rates and QE unchanged at 0.25% and 435 billion pounds respectively, which disappointed traders who expected more hawkish voting configuration. However, comments from BoE sounded optimistic and inflated pound for strong acceleration which returned above 1.3300 barrier and probes above yesterday's high at 1.3328. BoE MPC's policymakers said their first interest rate rise in more than a decade, was likely to be needed in coming months if economy growth and inflationary pressures continue to build. Markets took BoE's message as hawkish that sent pound into strong bullish acceleration, signaling that corrective phase off 1.3328 high is over. Bullish techs and renewed positive sentiment after BoE are supportive for acceleration towards target at 1.3473, provided by weekly cloud top.

Res: 1.3336; 1.3385; 1.3457; 1.3473

Sup: 1.3268; 1.3200; 1.3148; 1.3121

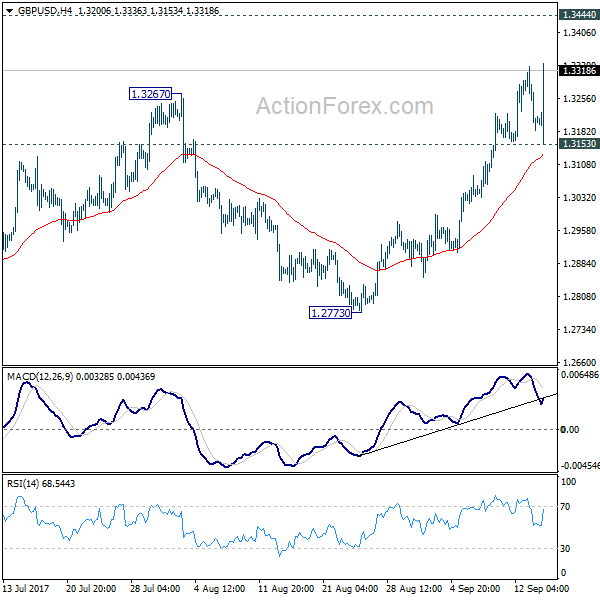

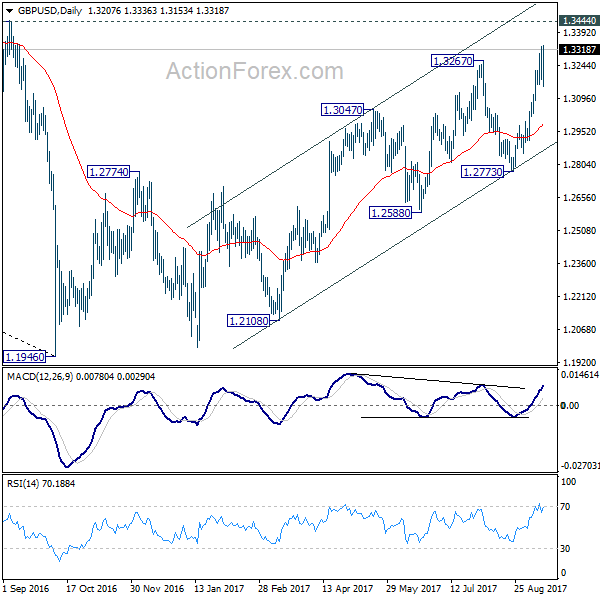

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3150; (P) 1.3240; (R1) 1.3297; More...

GBP/USD's rally resumes after brief retreat, breaking 1.3328 to as high as 1.3336 so far. Intraday bias is back on the upside for 1.3444 key resistance next. Still, we'd maintain that price actions from 1.1946 are still seen as a corrective pattern. Hence, we'd expect strong resistance from 1.3444 to limit upside to bring larger down trend reversal eventually. Break of 1.3153 support will raise the chance of reversal and turn bias to the downside for 55 day EMA (now at 1.2987) first. However, on the upside, firm break of 1.3444 will carry larger bullish implication and target 1.3835/5016 resistance first zone next.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern. While further rise cannot be ruled out, larger outlook remains bearish as long as 1.3444 key resistance holds. Down trend from 1.7190 (2014 high) is expected to resume later after the correction completes. And break of 1.2773 support will be the first sign that such down trend is resuming. However, considering bullish convergence condition in monthly MACD, firm break of 1.3444 will argue that whole down trend from 2.1161 (2007) has completed. And stronger rise would be seen back to 38.2% retracement of 2.1161 to 1.1946 at 1.5466.