Sample Category Title

EUR/AUD Weekly Outlook

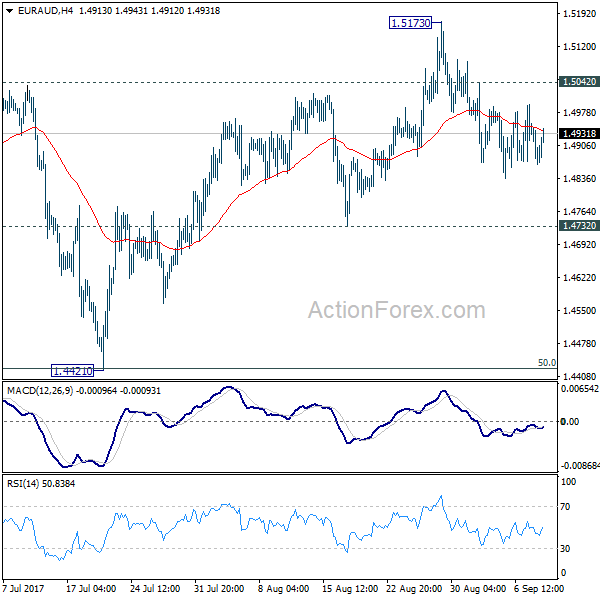

EUR/AUD was bounded in tight range last week but outlook is unchanged. With 1.5042 minor resistance intact, deeper decline is expected to 1.4732 support. Decisive break there confirm that fall from 1.5173 is the third leg of consolidation pattern from 1.5226. In that case, further fall should be seen to 1.4421 again. But we'd expect strong support from there to contain downside and bring rebound. On the upside, above 1.5042 minor resistance will turn bias back to the upside for 1.5173/5226 resistance zone instead.

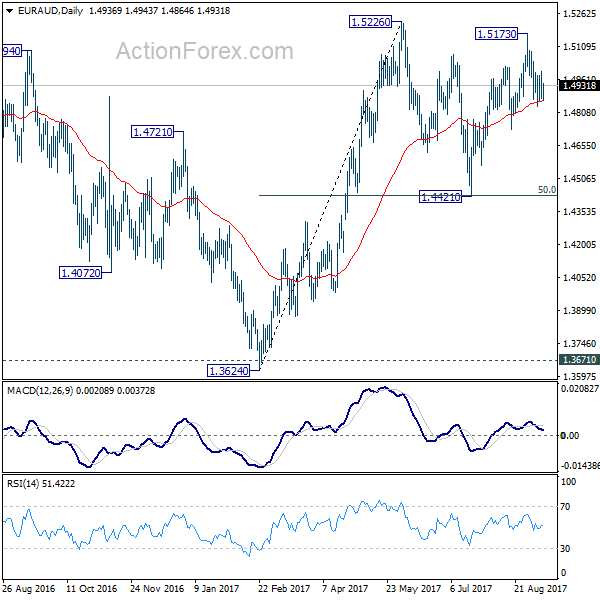

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. The corrective structure of the price actions from 1.5226 is affirming this view. Above 1.5226 will target a test on 1.6587 key resistance. However, break of 1.4421 support will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

In the longer term picture, the rise from 1.1602 long term bottom isn't over yet. We'll keep monitoring the development but there is prospect of extending the rise to 61.8% retracement of 2.1127 to 1.1602 at 1.7488 and above. However, sustained trading below 1.3671 should confirm trend reversal and target 1.1602 long term bottom again.

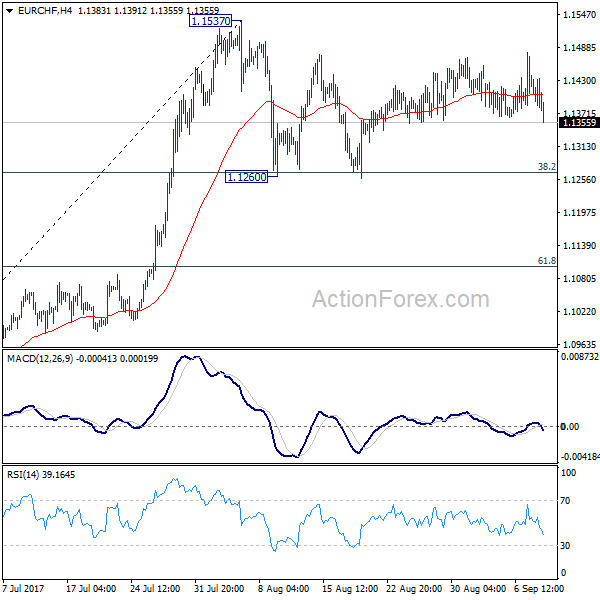

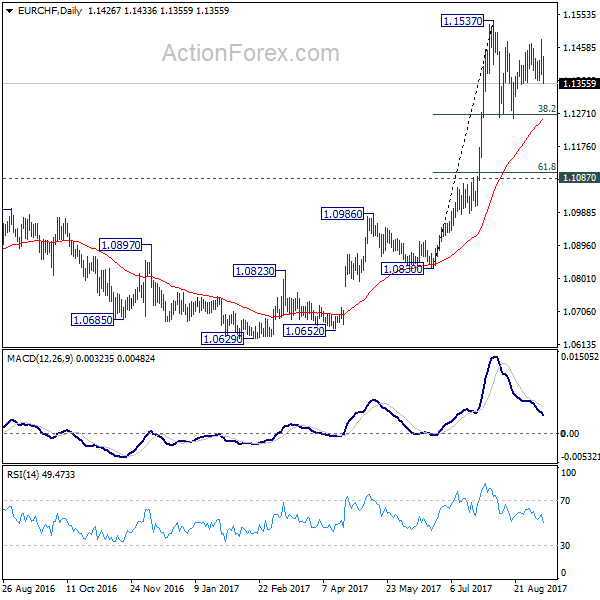

EUR/CHF Weekly Outlook

EUR/CHF edged higher to 1.1480 last week but reversed since then. But after all, the cross remained inside range of 1.1260/1537. Initial bias remains neutral this week first and more consolidation could be seen. On the upside, break of 1.1537 resistance will confirm resumption of larger rally from 1.0629. In that case, EUR/CHF should target 1.2 key resistance level next. On the downside, firm break of 38.2% retracement of 1.0830 to 1.1537 at 1.1267 will extend the correction to 61.8% retracement at 1.1100 before completion.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1087 resistance turned support holds.

Dollar Selling Picked Up Again on Geopolitical Tensions, Trump and Fed Uncertainties

Dollar ended the weak as the weakest major currency as weighed down by a number of factors. Judging from the fact that Yen and Swiss Franc were the strongest ones, risk aversion was a key factor in driving the greenback down. There is so far no resolution to the geopolitical tension between the US and North Korea yet. While US is calling for United Nations Security Council to vote on fresh sanctions against North Korea, it's effectiveness is in heavy doubt. There were also fears that North Korea will launch another missile to celebrate its foundation day on September 9, that is today. Also, not long after hurricane Harvey left, another one Irma is expected to land this weekend too. Some estimated the dame of Irma to be as much as USD 200b, topping Katrina that slammed into New Orleans back in 2005.

Geopolitical tensions, Trump, and Fed uncertainty to weigh down Dollar

In addition to geopolitical tensions and hurricanes, the greenback is also weighed down by falling treasury yield and fading chance of another rate hike by Fed this year. Talking about Fed, the surprised announcement of early resignation of Fed Vice Chair Stanley Fischer also raised doubts on what the group of Fed officials would become next year. Fed Chair Janet Yellen's term will expire next February and she could follower her closest ally Fischer and leave. It's reported that top contender, White House economic advisor Gary Cohn, is already out of the race. So, who's going to lead Fed next? It's question probably US President Donald Trump cannot answer himself.

Meanwhile, Trump just signed legislation on Friday to suspend the debt limit and that would keep the government running through December 8. USD 15.25b of hurricane relief funding will also be provided. However, it should be noted that it's a deal that was struck between Trump and Democrats. 90 Republicans have indeed voted in opposition in the House. Trump also overruled his treasury secretary, Steven Mnuchin, who's in the middle of a proposal for long term fix to the debt ceiling problem. Mnuchin was left to explain the deal to furious House Republicans before the vote. The handling of debt ceiling issue is another indication of Trump's disagreements with his own party Republicans. And this just add more to the doubt on whether Trump is able to push through the long awaited tax reforms and infrastructure spending.

The negative factors will continue to weigh on the greenback and any interim rebound would be temporary, until we see some fundamental changes in the situation.

So far, there is no change in the expectation that Fed is going to announce the plan to unwinding its USD 4.5T balance sheet on September 20. Comments from Fed officials last week regarding further rate hike were quite balanced. But the markets were simply getting more unconvinced Fed fund futures are now pricing in only 27.3% chance of a 25bps hike in December. A month ago, that was close to 50%.

TNX and DXY extended decline

10 year yield was dragged down by both safe haven flow as well as fading change of Fed hike. TNX extend the correction from 2.621 to as low as 2.034 last week. Near term outlook will remain bearish as long as 2.167. Further decline should be seen through 2.000 handle to 50% retracement of 1.336 to 2.621 at 1.978 next.

Some support was seen in the dollar index around 91.91/3 cluster support (38.2% retracement of 72.69 to 103.82 at 91.93). But that was brief and weak. The decline from 103.82 extend last week as dollar met fresh selling. As noted before, such decline is seen as corrective whole up trend from 72.69 (2011 low) to 103.82 (2017 high). Further fall is now expected as long as 94.14 support holds to 50% retracement at 88.25. It's a bit early to judge. But further downside acceleration could drag the index to next key cluster support at 84.75 (61.8% retracement at 84.58) before turning it into sustainable rebound.

Loonie support by BoC hike and job data

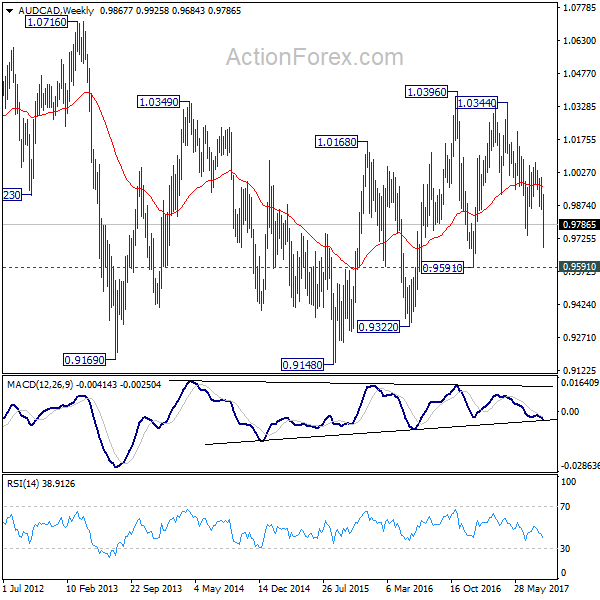

While risk aversion dragged down Aussie and Kiwi to some extents, against other major currencies, Canadian Dollar survived and ended as the third strongest one. The loonie was given a strong boost by the surprised interest rate hike by BoC. More in BOC Surprisingly Hikes Rate For Second Consecutive Meeting. Canadian was also supported by solid employment data released on Friday. USD/CAD could be losing some downside momentum as it approaches long term fibonacci level at 1.2048. But Canadian dollar is still looking bullish against other commodity currencies. For example, AUD/CAD's break of 0.9735 support indicates that fall from 1.0344 has resumed and deeper decline should be seen to 0.9591 support in near term at least.

Euro mixed after ECB meeting

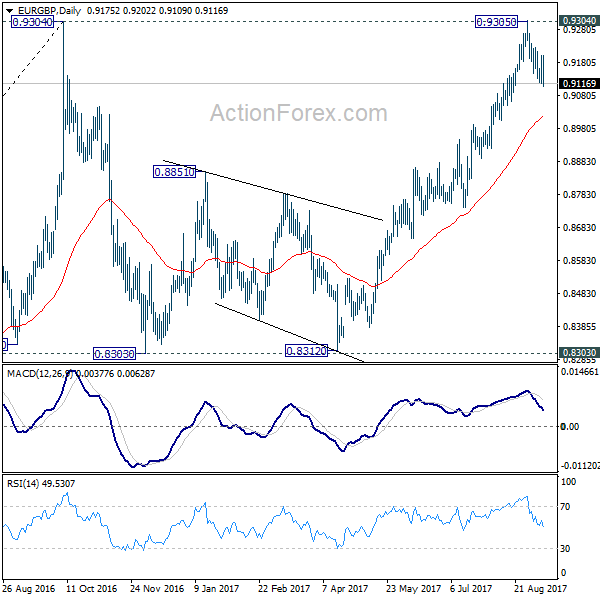

Euro was lifted against dollar last week after ECB meeting. ECB President Draghi indicated that the decision on "calibration" of the QE program will likely be made in October. More in Draghi Showed "Disaffection" Over Subdued Inflation, Admitted Discussions on QE Tapering. However, it should be noted that Euro has indeed ended the week down against, Yen, Swiss Franc, Canadian as well as Sterling. In particular, EUR/GBP's rejection from 0.9304 key resistance will likely extend lower in near term and that would limit rally attempt in the common currency against others.

A bit week for GBP with BoE and CPI

Talking about Sterling, the upcoming week will be an important one in UK. CPI will be released on Tuesday, followed by job data on Wednesday and BoE rate decision on Thursday. There is little chance for BoE to hike interest rate this time. The focus will stay on vote splits. Hawks Michael Saunders and Ian McCafferty are staying as hawks based on recent comments. But markets would be interested to see if they change their mind if CPI data disappoints again. In addition to that, rhetorics regarding Brexit will heat up again and UK and EU officials are preparing for the fourth round of talk to start on September 18. SNB will also meet this week but we're not expecting any surprise there.

GBP/CHF continued to engage in medium term consolidation that started back at 1.1635. It's usually very hard to trade this kind of sideway medium to long term sideway patterns, especially during the very middle phase. For now, despite recent rebound, near term outlook stays bearish in GBP/CHF for deeper fall. The decline from 1.3067 could extend to 100% projection of 1.3067 to 1.2239 from 1.2852 at 1.2024 before completion.

Trading strategies

Regarding trading strategies, our EUR/USD long (bought at 1.1846) was closed at market at 1.1880 last week, making 34pts profits. That was before EUR/USD eventually surged to as high as 1.2091. While it looks a wrong decision to close that early, the concepts behind was not wrong at all. Euro has indeed ended the week mixed, as dragged down by the decline in EUR/GBP and EUR/JPY. EUR/AUD was, to a certain extent, weak, too. Nonetheless, admittedly, we didn't expect that Dollar was that weak. Meanwhile, we bought CAD/JPY at market at 88.10 last week, but was stopped out quickly at 87.90, losing 20 pts. . Similar, not long after we're stopped out, CAD/JPY surged to as high as 87.53.

Given that we don't know what North Korean leader Kim Jong-Un would do in the big Foundation Day, we'll refrain from giving any strategy first.

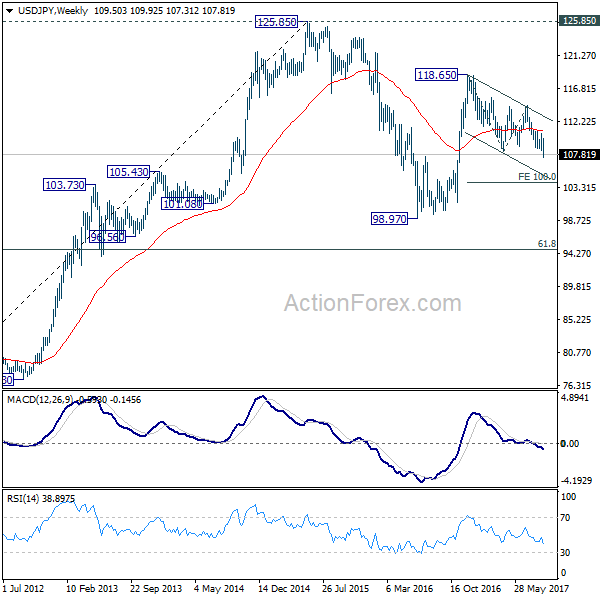

USD/JPY Weekly Outlook

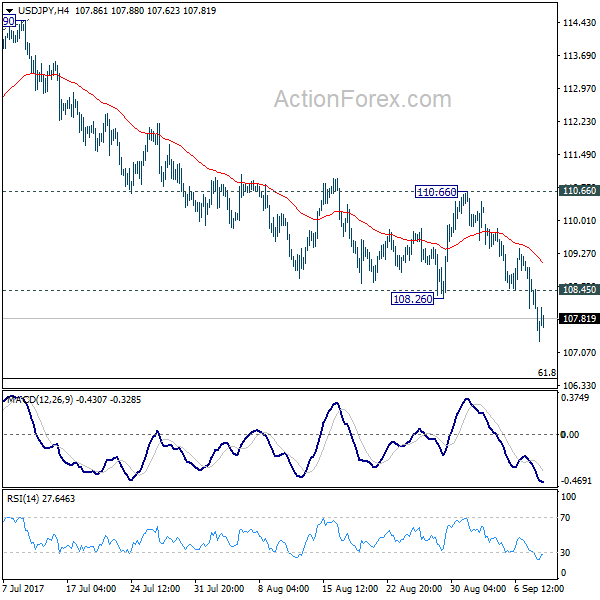

USD/JPY's medium decline from 118.65 finally resumed last week and reached as low as 107.31. Initial bias stays on the downside this week for 61.8% retracement of 98.97 to 118.65 at 106.48 first. We'd look for support from there to bring rebound. But firm break of 106.48 will extend the decline to 100% projection of 118.65 to 108.12 from 114.49 at 103.96 or below. On the upside, above 108.45 minor resistance will turn intraday bias neutral first. But outlook will now stay bearish as long as 110.66 resistance holds.

In the bigger picture, rise from 98.97 (2016 low) is now seen as the second leg of the corrective pattern from 125.85 (2015 high). It's unclear whether this this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don't expect a break there on first attempt.

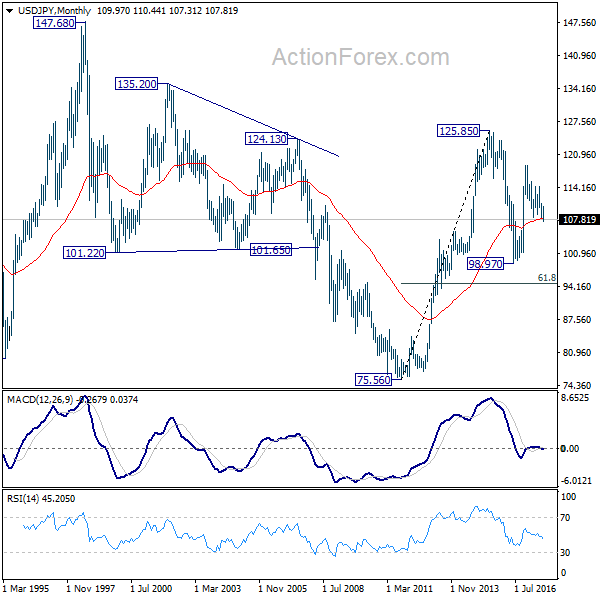

In the long term picture, the rise from 75.56 (2011 low) long term bottom to 125.85 top is viewed as an impulsive move, no change in this view. Price actions from 125.85 are seen as a corrective move which could still extend. In case of deeper fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77. Up trend from 75.56 is expected to resume at a later stage for above 135.20/147.68 resistance zone.

Summary 9/11 – 9/15

Monday, Sep 11, 2017

[php_everywhere] [/php_everywhere]

Tuesday, Sep 12, 2017

[php_everywhere] [/php_everywhere]

Wednesday, Sep 13, 2017

[php_everywhere] [/php_everywhere]

Thursday, Sep 14, 2017

[php_everywhere] [/php_everywhere]

Friday, Sep 15, 2017

[php_everywhere] [/php_everywhere].

Weekly Economic and Financial Commentary: Here Comes the Story of the Hurricane(s)

U.S. Review

That's Great it Starts With an Earthquake

- The economy took a backseat to the simultaneous approach of three hurricanes in the Atlantic basin and a magnitude 8.1 earthquake off the coast of Mexico. The influence of the storms is starting to soak into the economic data.

- Perhaps the most impactful economic news of the week came from the (pre-storm) factory orders report. While not typically a headlining economic indicator, it offered an indication of stronger business spending in July. Later in the week we learned that the ISM non-manufacturing index also improved, suggesting the momentum carried into August.

Here Comes the Story of the Hurricane(s)

Before the waters have fully receded in Houston, national attention has turned to the approach of Hurricane Irma barreling toward Florida and the southeastern United States. Our primary concern of course is for the people in the Caribbean who are still coming to grips with the devastation and that of our neighbors in Irma's path who are still in harm's way. In a recent special report "Impact of Hurricane Harvey" we consider the economic implications of the still undetermined damage in Houston.

The first hard-data reflection of the storms was manifested in this week's report on first-time claims for unemployment insurance. Jobless claims jumped to 298K from 236K in the prior week. The Labor Department reported an unadjusted increase of roughly 52K claims in Texas. The top chart show initial claims for the past 20 years and you can see the spike in 2005 related to Hurricane Katrina (circled in red), and the subsequent drop-off in claims that followed. The most important point though is that claims were only briefly affected at that time.

Using Katrina as a proxy, we can reasonably expect claims to continue to rise in coming weeks. That said, it is too early to tell yet what impact the storms will have on other measures of economic growth, but we will be monitoring the situation and will provide some thoughts where we can offer analysis rather than conjecture. In the meantime, we can unpack what this week's economic indicators tell us about the current condition of the expansion, starting with the factory orders report.

Shipments of core capital goods orders increased 1.2 percent in July, lifting the 3-month annualized growth rate to 5.4 percent. This is consistent with our forecast for gradual firming in equipment investment in the third quarter.

In a positive sign for future spending prospects, core capital goods orders also increased in July, growing 1.0 percent, which puts the 3-month annualized rate for that series at 5.1 percent. After having been a drag on growth in 2015 and 2016 when low oil and commodity prices acted as a damper on spending plans, equipment outlays have been gradually firming and added to topline growth for three-straight quarters.

Speed it up a Notch

As the bottom chart shows, during the 2015-2016 period, activity in the service sector handily outpaced activity in the factory sector. Both measures are in expansion territory today and we learned this week that the service-sector measure improved to 55.3 from 53.9 previously.

In a bit of role-reversal, the past few months have been characterized by activity in the manufacturing sector outpacing that of the service sector. ISM non-manufacturing tends to be a useful proxy of future core retail sales growth.

On that basis, our forecast for firming equipment spending in the second half and a softening in the pace of retail sales growth is consistent with what the survey data are signaling at present.

U.S. Outlook

CPI • Thursday

Consumer price growth remained subdued in July. Both headline and core CPI rose 0.1 percent on the month and 1.7 percent over the year. July's monthly figure was an improvement from the previous two months, however, as prices declined in May and were flat in June. Energy prices were a drag on the headline over the past three months, which we can expect to reverse in coming months as gas prices reflect the damage from Hurricane Harvey on the heart of the domestic energy sector. Retail gasoline prices surged around September 1, so August headline CPI is likely in the clear.

Looking to the trend, we expect below-target inflation to continue into next year. We expect only two rate increases by the FOMC in 2018—not the three the FOMC has currently projected, as the outlook for core inflation remains modest.

Previous: 0.1% Wells Fargo: 0.3% Consensus: 0.3% (Month-Over-Month)

Industrial Production • Friday

Industrial output rose 0.2 percent in July, though the increase was entirely due to mining and utilities output. Manufacturing output has been up one month and down the next, with July falling in the latter, down 0.1 percent. The sawtooth pattern is consistent with our forecast for continued modest, but steady growth. Taking a longer view, manufacturing output is up 0.8 percent, year to date.

Industrial production data are likely to be affected by Hurricane Harvey in coming months, as the storm knocked out utilities and mining operations. The shutdown of petrochemical plants and other key nodes in the domestic supply chain may extend the impact to longer than just one month, though IP recovered rather quickly following Katrina in 2005. Hurricane Irma may also have repercussions on manufacturing production operations that lay in its path this weekend, though to a smaller extent as it is not currently aiming at the heart of U.S. oil production.

Previous: 0.2% Wells Fargo: 0.2% Consensus: 0.1% (Month-Over-Month)

Retail Sales • Friday

July marked a strong start to the third quarter for retail sales, which rose 0.6 percent while June's decline was revised to a gain. Personal consumption expenditures in Q2 GDP also received an upward revision, pushing growth to 3.0 percent. Revisions show the domestic consumer was on solid footing in Q2 and had good momentum at the start of Q3. The strong showing for control group sales, which enters into the GDP calculation, gives more credence to our call for a strong consumer for the rest of the year.

Retail sales are also a series likely impacted by Harvey and Irma, though it is difficult to predict whether Hurricane Harvey will show in next week's advanced estimate for August. The impact will likely be more apparent in the revisions. September will also likely be skewed by both Harvey and Irma, and Florida's missed tourism dollars may weigh on year-over-year sales in subsequent months.

Previous: 0.6% Wells Fargo: 0.1% Consensus: 0.1% (Month-Over-Month)

Global Review

Strong Growth Leads Bank of Canada to Hike Rates

- The Bank of Canada surprised many analysts this week by announcing its second 25 bps rate hike since July. The Bank cited strong economic growth as a reason for hiking rates. The Canadian dollar rose to a two-year high against the U.S. dollar this week.

ECB Remains on Hold, For Now

- The ECB did not make any changes to its policy stance this week. However, the expansion in the Eurozone is becoming increasingly self-sustaining, and we look for the Governing Council to announce a further reduction in the monthly pace of its bond purchases at its next policy meeting on October 26.

Strong Growth Leads Bank of Canada to Hike Rates

The Bank of Canada (BoC) surprised many analysts this week by hiking its main policy rate by 25 bps, the second rate hike since mid-July (see graph on front page). The rate hike brings the main policy rate back to 1.00 percent, the level that prevailed in January 2015 before the Canadian economy slid into a mild recession. In announcing the rate hike, the BoC said that "recent economic data have been stronger than expected" and that growth "is becoming more broad-based and self-sustaining." That said, the BoC noted that the outlook is subject to a number of risks and that future policy moves "are not predetermined."

The Canadian dollar, which is up more than 10 percent vis-à-vis the U.S. dollar since the beginning of the year, rallied in the immediate aftermath of the surprise rate hike and rose to a twoyear high versus the greenback (top chart). We look for the BoC to hike rates twice in 2018. Our currency strategy group expects the loonie will continue to trend higher versus the greenback going forward, albeit not as rapidly as in recent months.

ECB Remains on Hold, For Now

The European Central Bank also held a policy meeting this week. Unlike the BoC, the ECB Governing Council decided to keep its policy rates on hold, which was widely expected. The Governing Council also decided to keep the flow of its quantitative easing (QE) program unchanged at €60 billion per month, which was also widely expected.

In the policy statement that followed the meeting, the Governing Council acknowledged that the economic expansion in the euro area "continues to be solid and broad-based across countries and sectors." Indeed, the year-over-year rate of GDP growth in Q2, which was originally reported as 2.2 percent, was revised up this week to a six-year high of 2.3 percent.

There is not much "hard" data out of the third quarter yet, but the purchasing managers' indices remain well above the demarcation line separating expansion from contraction. Industrial production (IP) in Germany was flat in July relative to the previous month, but the year-over-year rate of growth remained buoyant at 4.0 percent (bottom chart). French IP rose 0.5 percent in July relative to the previous month, bringing the year-over-year growth rate up to a two-year high of 3.7 percent.

The ECB has had a QE program in place for more than two years, which has led to a doubling in the size of its balance sheet over that period (middle chart). In March, the Governing Council announced that it would dial back its monthly purchase rate of bonds from €80 billion per month to €60 billion per month, where it has subsequently been maintained. With the expansion becoming increasingly self-sustaining, we look for the Governing Council to announce a further reduction in its monthly purchase rate at its October 26 meeting. By the middle of next year, we expect that the ECB will cease buying bonds altogether. However, the Governing Council does not appear to be in any hurry to hike rates. With CPI inflation well below 2 percent at present, we look for the ECB to keep rates on hold until the end of 2018.

Global Outlook

Eurozone Industrial Prod. • Wednesday

The Eurozone grew at a relatively healthy clip in Q2 2017, up 0.6 percent seasonally adjusted (not annualized) and by an upwardly revised 2.3 percent year-over-year rate. Furthermore, we have seen some forward momentum on the Markit manufacturing PMI, which printed 57.4 in August, matching the highest reading for the series recorded in June of this year. At the same time the ECB kept monetary policy unchanged (read more on this on our Global Review section on the previous page).

With this information in the background, the industrial production index declined 0.6 percent in June after a very strong month in May, up 1.2 percent. Thus, markets will be anticipating if the industrial production index recovers in July to see if the economy kept its momentum at the start of the third quarter.

Previous: -0.6% Consensus: 0.0% (Month-Over-Month)

China Industrial Prod. • Wednesday

The year-over-year uptick in the Chinese industrial production index compared to last year has not gone unnoticed by the rest of the global economy with industrial production and export growth improving across the globe. Thus, when the Chinese industrial production index for August hits the airwaves on Wednesday it could impact markets. Consensus expectations call for the index to have improved from 6.4 percent for the year ending in July to 6.6 percent year-on-year in August, a marginal increase but positive nonetheless. At the same time, consensus expects the index to have increased 6.8 percent on a year-to-date basis in August.

Also on Wednesday we get Chinese retail sales for August and markets are also looking for a slight increase for the year-over-year measure, from 10.4 percent in July to 10.5 percent in August.

Previous: 6.4% Consensus: 6.8% (Year-Over-Year)

Brazil Economic Activity Index • Thursday

Although the Brazilian political corruption crisis continues to amaze friends and foes alike almost on a daily basis, the Brazilian economy seems to have finally detached from the travails of its political malaise and is primed for a continuation of growth. Of course, the political risks could still potentially, once again, derail the current recovery. However, the recovery is sustained by the economic collapse of the last several years. That is, economic numbers are coming from such a low base that it will be difficult for the economy not to continue to show improvement.

Case in point will be the release on Thursday of the monthly economic activity index for July. Although the index has not been consistently positive on a month-on-month or even on year-over year basis, the economic activity index has improved considerably compared to the last several years.

Previous: -0.6% (Year-Over-Year)

Point of View

Interest Rate Watch

Slower Reflation, Slower Tightening?

The FOMC is likely to lay out a more gradual path for inflation in its next set of projections, due after the committee wraps up its Sep. 19-20 meeting.

As of its June meeting, FOMC members expected headline PCE inflation to reach 1.6 percent by year end. That continues to look reasonable due to the jump in gasoline prices expected for September, but expectations for core inflation will likely be revised lower. In June, the median forecast for core inflation was 1.7 percent. To be achieved, monthly inflation readings for the remainder of the year would need to average 0.2 percent a month—twice the pace of gains so far this year. That could be a tall order, especially since core inflation has tended to post smaller gains in H2.

Reaching 2.0 percent by the end of 2018, the current median FOMC estimate, also looks tougher. While recent base effects will not need to be factored in to officials' 2018 estimates, the soft patch in core inflation since the Spring has some Fed officials questioning the traditional emphasis on resource slack. At the July FOMC meeting, participants discussed the efficacy of such framework. This week Fed Governor Lael Brainard highlighted the disconnect between inflation and an economy operating near full employment, casting doubt on resource utilization as a reason for low inflation.

As Fed officials go through a rethink, we expect to see a shallower path of inflation laid out. While resource utilization still plays an important role in inflation, the weakness of recent months have highlighted it is not the only driver. Expectations, influenced by the recent trend in inflation, remain key and are still at historically low levels. As a result, it may be harder for services inflation to break out of its current trend channel despite further tightening in the labor market. Core goods prices should get a boost from a weaker dollar and rising inflation abroad. The lift, however, will be limited by declining prices for autos. The question for Fed officials in the coming months will be whether the slowdown is significant enough to warrant a slower pace of future rate hikes.

Credit Market Insights

The Beige Book Credit Outlook

The Fed's most recent Beige Book conveyed healthy economic conditions throughout the twelve Federal Reserve Districts. Credit conditions appear to be broadly stable throughout the United States. In its August 2017 report the Fed noted, "business and consumer loan demand grew at a modest pace in most districts, with a number of banks reporting rising competition from both other banks and non-bank lenders."

There were modest changes in loan demand across the districts. Richmond and Chicago reported slight growth in loan demand, and both the Philadelphia and Dallas districts reported a faster pace of demand compared to the previous reporting period. There was steady loan demand reported in New York, Cleveland, and Kansas city.

Modest loan growth has been attributed to an increase in competition among banks and non-banking institutions, and the uncertain political climate. The limited supply of homes for sale has caused mortgage activity to slow in some districts. Several districts also reported concerns regarding the decline in auto lending, attributed to a slowdown in auto demand. Delinquency rates appear low to moderate across the districts. Loan portfolios were considered healthy, with no significant signs of concern.

The modest growth depicted in the Beige Book has left sentiments about future business activity and loan demand largely positive.

Topic of the Week

Fischer to Leave Fed in October

Stanley Fischer, who has served as the Vice-Chairman of the Federal Reserve Board since May 2014, announced this week that he would be resigning "on or around October 13." Before joining the Fed, Fischer did stints as a Professor of Economics at MIT, Chief Economist of the World Bank, Deputy Managing Director of the IMF, and Governor of the Bank of Israel. He is widely respected due to his deep knowledge of economics and monetary policymaking.

There currently are only four members on the sevenmember Board of Governors, and the headcount will fall to three once Fischer leaves. His departure will complicate matters a bit for the Fed, but it will not hamstring the organization. The Board can still have a quorum as long as a majority of members are present. In a three-member Board, two members would need to be present to have a quorum. Besides, President Trump nominated Randal Quarles to fill one of the vacant board seats in July, and the Senate has already held confirmation hearings. Assuming Quarles is confirmed by the Senate, the number of board members would increase again to four. Marvin Goodfriend, the former research director at the Richmond Fed, has been rumored to be in line for a Fed board seat but Trump has not yet formally nominated him.

Fischer's announcement brought back into focus the question of who will be the next Fed Chair once Janet Yellen's term expires in February 2018. Gary Cohn, the current Director of the National Economic Council, was seen as the frontrunner, but the Wall Street Journal reported this week that Cohn has recently lost favor with Trump. Other potential candidates include Yellen, Larry Lindsey, Kevin Warsh and John Taylor. Lindsey and Warsh both have Fed experience, and Taylor is a wellrespected academic economist. President Trump will need to make a decision by the end of the year. For further reading see "The Contenders: Prospects for the Next Fed Chair" which is posted on our website.