Sample Category Title

Weekly Market Outlook: BoE, SNB Policy Meetings, US and UK CPIs, Other Key Data in Focus

Next week's market movers

- The main event is probably the BoE gathering. We don't expect any action at this meeting, given the stagnant business investment for Q2.

- We expect the SNB to repeat that the franc remains significantly overvalued and that the Bank will remain active in the FX market as necessary in order to curb any gains in the currency.

- In the US, the core CPI rate is expected to have declined somewhat, which could drag further down the probability for another Fed rate hike by year-end to drop further.

- On the other hand, we see the case for both the headline and core CPI rates in the UK to have risen. One of the reasons for that may be the recent depreciation of the pound against the euro.

- We also get more key economic data from Sweden, Australia, the UK, the US, and China.

On Monday, there are no major events or indicators on the economic calendar.

On Tuesday, Sweden's CPI data for August are coming out. Expectations are not public yet, but we believe that both the headline CPI and CPIF rates may have pulled back. We base our view on the fact that since June, SEK has appreciated notably against both the dollar and the all-mighty euro, something that may have eventually weighted on Sweden's inflation. That said, we believe that market participants will place all their attention to the CPIF print, given that at its latest gathering, the Riksbank decided to adopt inflation measured in terms of the CPIF with the target staying at 2%, but with a variation band of 1-3%.

We get CPI data for August from the UK as well. With no forecast available yet, we believe that both the headline and the core rates may have rebounded somewhat. Our view is based on the nation's services PMI, which showed that firms increased their average prices charged in August at the highest rate since April. The recent depreciation of the pound against the euro supports further the case for accelerating inflation. Even though a rebound in the CPI rates could revive some speculation with regards to a BoE rate hike this year, we remain skeptical on that prospect. (See BoE policy meeting below).

On Wednesday, the UK employment report for July is coming out. No forecast is available at the moment, but we see the case for the unemployment rate to have fallen further. The services PMI showed that jobs growth rose to a 17-month high, while the Markit/REC report on jobs, showed that permanent placements increased to the greatest extent in 27 months. What's more, the Markit jobs report showed that starting salaries continued to rise in the month, with the rate reaching a 20-month record. This makes us believe that wages may have accelerated, which would be pleasant news for BoE Governor Carney, who a few months ago noted that a rate hike may depend mainly on firming wages and improving business investment. Having said that though, the fact that business investment was stagnant in both quarterly and yearly terms during Q2 will most probably keep BoE hands off the easing button on Thursday.

On Thursday, the main event will be the Bank of England policy decision. The consensus is for the Bank to keep its policy unchanged via a 6-2 vote. At its latest meeting, when alongside the rate decision and the meeting minutes, the BoE published its quarterly Inflation Report, the Bank reiterated that policy may need to be tightened to a somewhat greater extent over the next 3 years than what was implied by market pricing at the time. Nevertheless, it signaled little urgency for a hike in the next months, while it revised lower its inflation and economic growth forecasts.

Since then, CPI data showed that both the headline and core inflation rates remained unchanged in July, but as we noted above there is the possibility for a rebound in August's prints. Meanwhile, although we expect wages to have accelerated in July, the 2nd estimated of GDP confirmed that economic growth was only +0.3% qoq in Q2, and most importantly business investment prints for the quarter were stagnant in both quarterly and yearly terms.

As such, we don't expect the Bank to proceed with hiking rates at this meeting, neither at one of the remaining ones until the end of the year. At the time of writing, the UK Overnight Index Swaps (OIS) suggest that the probability for a hike by year-end is 24%. Even though this appears low at first glance, having the aforementioned economic developments in mind, we thing that it is still overly optimistic.

The key risk to our view remains the same as back in August. Despite economic developments suggesting a relatively low likelihood for a hike in the near-term, the BoE may want to revive speculation on that front in order to support the pound and thereby, curb inflation. In this case, Carney could say that the MPC discussed the prospect of a hike, but decided against it for now.

In Switzerland, the SNB will announce its rate decision as well. Economic developments have been somewhat decent since the Bank last met. On the inflation front, the CPI rate dropped notably in June, rebounded thereafter and in August it matched its May levels. The unemployment rate remained unchanged in July, while growth is expected to have accelerated, but slightly, in Q2. As for the all-important franc, it weakened notably against the euro, but it remained relatively unchanged against the dollar. However, the recent weakness against the euro has failed to boost Switzerland's economic outlook in a meaningful way, evident by the disappointing KOF indicator and Credit Suisse investor sentiment index, both for August.

Therefore, we don't expect the SNB to change tune. We think policymakers are likely to repeat the usual mantra – that the franc remains significantly overvalued and that the Bank will remain active in the FX market as necessary in order to curb any gains in the currency.

As for the economic indicators, during the Asian morning, Australia's employment data for August are due out. Our own view is that the labor market may have posted another month of solid employment gains, something supported by the ANZ job ads indicator, which showed advertisements rising for the 6th consecutive.

From China, we get retail sales, industrial production and fixed asset investment, all for August. Expectations are for retail sales as well as industrial production to have accelerated in yearly terms, while fixed asset investment is expected to have slowed somewhat. The forecasts for retail sales and industrial production are supported by the nation's official manufacturing PMI, which showed that output growth was faster compared to a year ago. What's more, the production sub-index was much higher than August 2016.

In the US, we get CPI data for August. Given the increasingly concerned remarks on Wednesday by Brainard and Kashkari over inflation and interest rates, this set of CPI data is likely to attract more attention than usual, as it could prove critical on whether the FOMC will indeed proceed with another rate hike this year. Expectations are for the headline rate to have ticked up, but for the core rate to have ticked down. This combination makes us believe that the rise in the headline rate may be owed primarily to movements in volatile items, such as energy-related products and food. Therefore, as long as core inflation remains subdued, we doubt that the headline print will be enough to drag forth expectations for the next Fed hike. Actually, we believe something like that may be the reason for the number of concerned policymakers around inflation to increase at the upcoming Fed meeting, and for the probability for another rate hike by year-end to drop further. According to the Fed fund futures, that probability currently stands at around 30%.

Finally on Friday, we get the US retail sales for August and expectations are for both the headline and core rates to have declined somewhat. That said, both the nation's consumer sentiment indices for the month did not paint a clear picture. Even though the U o M print declined, the Conference Board index continued to rise, making us hesitant to place too much faith in the forecast.

Weekly Market Outlook: JPY Ignoring North Korea

- Investors Beware: Risk Is Underpriced! - Peter Rosenstreich

- Draghi Passes The Hot Potatoe - Arnaud Masset

- JPY Ignoring North Korea - Peter Rosenstreich

- Cryptocurrency Miners

FX Market - Investors Beware: Risk Is Underpriced!

Central banks are suppressing the true price of risk in rates, which in turn are distorting all other risk measures. For instance, while Greece 2-year yields were at 9.5% seven months ago, now they stand at 2.67%. That is on par with dysfunctional Argentina's debt and only 60 basis points above that of AA-rated New Zealand's! Ok, the view is that Greece will be backstopped by the ECB (bolstered by German Chancellor Merkel's pro-EU election platform and French President Macron's speech yesterday in favour of EU integration). Nonetheless, investors should be wary of Central Banks 'miracle solution' for managing debt and avoiding default: the unadulterated creation of raw capital.

Concern about this is surprisingly low. The VIX index of volatility is trading at a modest 12, despite lingering concerns of nuclear war with North Korea. Capital continues to flow out of the USD and into emerging markets. The trend is accelerating, as Chinese trade data suggest, with a 5.5% year on year jump in exports and whopping 13.3% year on year surge in imports. This is boosting currencies such as the INR, SGD and IDR. However, we continue to "make hay while the sun is shining" however we are sensitive to the markets artificial comfort level.

So if there is no any longer credit risk, any return is a good return. Which is why shares in the Swiss National Bank stock (yes, the SNB is a publicly traded company) continues to rally. Printing francs to buy Euros and equities is a great business model.

Economics - Draghi Passes The Hot Potatoe

In spite of huge market expectations, Mario Draghi gave little information during the conference that followed the last ECB meeting, playing for time once again. As broadly anticipated by market participants the European Central Bank did not change the level of any of its three key interest rates. However, investors were hoping that Draghi will come with a plan regarding the future of the central bank's quantitative easing program. The ECB's president chose to leave this announcement for the end of the year as he declared the QE will run as such until December or even beyond if necessary.

Investors were also expecting a reaction to the euro appreciation of the last few months as it creates some significant downside risk for growth and inflation. Once again they were quite disappointed as Draghi only declared that the "euro volatility represents a source of uncertainty." He didn't appeared too worried about the recent euro strength and did not suggest it will interfere extensively on the central bank policy. Therefore investors will have to wait until the ECB next meeting in October or most likely in December to get answers to their questions regarding the EUR/USD spiked to $1.2059 during the press conference and continued to rally during the Asian session, consolidating at around $1.2050. The fact that Draghi appeared not too concerned about the euro strength was interpreted as a bullish signal by investors. They quickly forgot that he did not provide any hint about tapering, which is definitely not a sign of confidence in growth and inflation outlook but rather a hint that Draghi wants maximum flexibility.

With the ECB meeting behind us, investors will now focus on the next big event that is the FOMC meeting on September 20th. Although the Fed hiking cycle seems on pause for now, with investors not pricing any interest rate hike before next year, investors are impatiently awaiting the Fed to finally reveal the starting date of its balance sheet unwinding programme.

In the meantime, the US dollar may continue to lose ground as investors discount Trump's reflation trade and an aggressive pace of tightening from the Federal Reserve. However, the huge amount of short dollar position suggests that the downside is rather limited, especially considering that Yellen could hardly disappoint expectations since there is none. The risk is therefore skewed to the upside ahead of the FOMC meeting.

Economics - JPY Ignoring North Korea

We remain perplexed by the steady appreciation of the JPY. Tensions around North Korea remains at a worryingly high level. South Korean Prime Minister Lee has suggested that North Korea might be planning a missile launch test on Saturday, which follows last week's thermonuclear test. Judging from market volatility indicators there is minimal concern across markets. However, unnerved by the threat, South Korea took delivery and deployed of four THAAD anti-missile defense launchers. Clearly, South Korea has a different view of the situation. In the FX market, JPY shrugged off the news and led the week's FX outperformers.

Traders seems to continue to see JPY as a "safe-haven" trade despite Japan being clearly in North Korea's cross hairs. We are seeing slight JPY wobbles on geopolitical disturbances but the currency quickly recovers. Markets are blissfully unaware of the tails in these circumstances.

The yen has been trading on interest rate differential and markets are unwilling to release this driver in-spite of mounting risks. The BoJs strategy of yields curve control has been successful in yields pinned to a low level. All the while, US yields have been shifting lower, narrowing key interest rate differentials. Persistently low domestic yields should force Japanese investors to look abroad for opportunity, yet that is no longer happening. Domestically, there is increase probably that Prime Ministers Abe early resignation could derails the BoJ policy. Which could explain why we are not seeing aggressive rotation out of JGBs into foreign assets. However, Kuroda's doves control the BoJ, so while no additional easing is likely, the BoJ is not going to move-off their yield curve control. Given the current logic, the JPY trend will be dependent on foreign central banks normalization strategy.

While the Fed interest rate path has decelerated, we anticipate a policy hike in December. In our view, the miscalculations of risk emulating form North Korea combined with higher US rates should provide plenty of upside to USDJPY.

Themes Trading - Cryptocurrency Miners

The world of cryptocurrency is exploding. The utility of alt-coins has been exhaustively debated, with the overall result positive on the outlook for virtual currencies. While it remains uncertain which coin or token will become the dominant currency, what is clear is that the ecosystem will continue to thrive.

Cryptocurrencies might only exist virtually, but real-world technology is the driving force behind them. Mining, the process by which new coins enter the system, is very IT-intensive. Implemented in massive data centers with significant server computing power, mining demands the most innovative processors, graphics cards and memory chips available. The staggering price of Bitcoin and Ethereum, alongside numerous other alt-coins (Dash, LiteCoin, etc.), has led to a ground war for computing power, with miners competing for the biggest and best technology. This new client segment has pushed established vendors and FinTechs to create products to satisfy demand. AMD's Computing and Graphics segment, which includes its Ryzen processors and Vega graphics processors, saw revenues increase by 19% in Q2 2017, to $1.22 billion.

Week Ahead – BoE MPC Vote Eyed Amid Slowing UK Growth; US CPI and Retail Sales in Focus Before...

Industrial output and retail sales data will dominate the economic calendar week, and inflation and employment will also be in focus. However, the week looks set to be a less dramatic one from the past seven days with policy meetings by the Bank of England and the Swiss National Bank unlikely to bring much surprises.

Australian employment report to be watched as aussie rallies

The Australian dollar is on track to end the week 1.5% higher against its US counterpart despite a neutral RBA policy meeting and a mixed batch of data. Next week's jobs numbers will be important in assessing whether the Australian economy is gaining sufficient momentum to warrant the RBA's view that growth will reach 3% in the coming months, having expanded at an annual rate of 1.8% in the second quarter. The August employment figures are out on Thursday and before that, the NAB business confidence and Westpac consumer sentiment gauges will be looked at on Tuesday and Wednesday respectively.

Steady as she goes in China

China posted a sixth straight month of year-on-year growth in exports in August, cementing expectations that the economy will avoid a sharp slowdown in growth in the second half of the year as the government cracks down on risky lending. The better-than-expected performance in 2017 has not only eased downside pressure on the yuan but has also enabled the People's Bank of China to lift the currency's mid-point versus the US dollar to its highest in 16 months this week. Data due next week on industrial output, fixed asset investment and retail sales are not expected to upset this picture. Industrial production (+6.6% y/y) and retail sales (+10.5% y/y) are forecast to improve slightly in August from the prior month, while fixed asset investment (+8.2% y/y) is expected to slow marginally.

Japanese machinery orders to bounce back

A bigger-than-anticipated downward revision to Japan's GDP growth rate for the second quarter this week did not cause much alarm for investors as all the indications are that the world's third largest economy is on course to expand for the seventh consecutive quarter in the third quarter, making it Japan's longest streak of expansion this century. This should be evident next Monday, with machinery orders forecast to rebound by 4.4% month-on-month in July. Also to watch next week are corporate goods prices for August on Tuesday and the final industrial output figures for July on Thursday.

SNB likely to remain dovish

Data out of the Eurozone will be scarce next week with industrial output numbers for July being the only major release (due on Wednesday). The euro rallied to a fresh 2½-year high against the dollar after the ECB's policy meeting this week. Against the Swiss franc, a high of similar period was reached in early August, bringing much relief to the Swiss National Bank, which has long argued that the Swissie is "significantly overvalued".

However, the franc has gained 7% against the dollar in the year-to-date and the recent bout of geopolitical risks has brought safe havens back in favour. The SNB is therefore not expected to be satisfied with the Swissie's broader value and is forecast to keep its three-month LIBOR target rate unchanged at -0.75%. Recent data out of Switzerland has been on the weak side, with second quarter GDP sharply missing estimates to grow by just 0.3% over the quarter and annual inflation running at a paltry 0.5%. This points to the SNB maintaining its dovish tone and exchange rate warning when it meets for its latest policy decision on Thursday.

Bank of England under spotlight as rate hike odds diminish

The Bank of England will have gotten its hands on the latest UK inflation and jobs data before concluding its two-day monetary policy meeting on Thursday. Inflation numbers are out on Tuesday and annual CPI is expected to tick higher again, rising to 2.8% in August. The core rate is also forecast to edge upwards, to 2.5%. Unemployment data due on Wednesday will likely show the jobless rate holding steady at 4.4% in the three months to July. Average weekly earnings growth is forecast to accelerate slightly to 2.3% y/y during the same period, though this remains below the level of headline inflation, meaning real incomes continue to decline.

Attention will shift onto the Bank of England on Thursday, with the Monetary Policy Committee retuning to its full nine-member board as the new Deputy Governor, Sir Dave Ramsden, attends his first meeting. The Bank shocked markets in June when three MPC members voted for a rate hike. That figure fell to two in August and it will be interesting to see which way the newest member will vote. Following the replacement of Kristin Forbes by the more dovish Silvana Tenreyro, if Ramsden also joins the doves, it will be difficult to foresee a rate hike before 2019, as per economists' latest projections. This could be negative for the pound's medium-term outlook, though progress in the Brexit negotiations will also strongly influence sterling's path over the next year, with the related uncertainty already dampening UK growth this year.

US inflation and retail sales eyed

As traders price out another Fed rate hike this year, economic data may nevertheless provide some support to the hammered dollar, which has fallen to 2½-year lows this week. The US calendar will start with the July JOLTS job openings on Tuesday and August producer prices will follow on Wednesday. Inflation data will be scrutinized on Thursday as subdued prices pressures continue to puzzle Fed policymakers. The annual CPI rate is forecast to rise from 1.7% to 1.8% in August, but the core rate is expected to ease to 1.6%. Retail sales figures are due on Friday and are expected to show a month-on-month gain of 0.4% in August, down from 0.6% in July. The August CPI and retail sales numbers will be the last before the September FOMC meeting on September 19-20. Also out on Friday are industrial output data and the University of Michigan's preliminary reading of consumer sentiment for September.

Weekly Focus: Focus on Inflation Prints

Market Movers ahead

- In the US, we expect inflation pressure remained muted in August.

- In the euro area, wage cost growth in Q2 will probably have been constrained by still broad labour market slack.

- We expect the Bank of England to keep the Bank Rate unchanged at 0.25% with a vote count of 7-2 (vs 6-2 in August; one extra member this month).

- In China, we pay more attention to the details of the industrial production release for August, as electricity generation and steel output should reflect the rebound over the summer in the Chinese economy.

- The August inflation prints in Denmark and Norway will likely show a lower inflation rate than the previous month while going up a bit in Sweden.

- In Norway, Norges Bank's preferred measure of economic activity, the regional network survey, is likely to rise on the back of solid momentum in the Norwegian economy.

Global macro and market themes

- Combination of strong global PMIs and postponement of US debt limit risk are good for equities.

- Trump's debt limit deal means that return of USD scarcity is postponed, likely till 2018.

- Any dips in EUR/USD should be shallow and short-lived. EUR yields to range trade before rising next year, as markets price in an ECB tapering premium.

- Fed to begin quantitative tightening at upcoming meeting but direction next year uncertain due to vacant seats.

WTI Oil Price Eased Below $49.00

WTI oil price eased below $49.00 on Friday after repeated upside rejections at $49.40/31 in previous two days and Thursday's action being shaped in Doji, signaling indecision.

In addition, strong build in crude inventories last week added to pressure on oil price which was inflated by increased demand for oil on restart of Texas refineries which were shut on Hurricane Harvey.

Current easing could be seen as correction of larger bull-leg from $45.57 on overbought studies and ahead of attack at strong barriers at $49.62 (200SMA) and psychological $50.00 barrier.

Dips should be ideally contained by supports at $48.00 zone, provided by daily cloud top and Fibo 38.2% of $45.57/$49.40 upleg).

Focus is shifting to three other hurricanes that are approaching the US Gulf coast and may disrupt refining process again and reduce demand for oil again that would further boost oil prices.

Another supportive factor for oil price would be decision of Saudi Arabia to cut supplies in October by 350.000 barrels per day.

Res: 49.24; 49.40; 49.62; 50.00

Sup: 48.72; 48.50; 48.00; 47.65

Sterling Breaks 1.32 ahead of BOE Meeting; Yen Extends Gains as North Korean Risks Linger

The dollar continued to trade weak during the European session with most of its peers hovering near fresh highs they reached in the Asian session. The pound and the yen extended their earlier gains, with the former hitting above the 1.32 key level against the greenback, while the latter reached the price of 107 per dollar for the first time since November 2016.

With Hurricane Irma heading towards Florida, after it devastated the Caribbean islands and while other two hurricanes have been observed moving in the Atlantic, the Federal Emergency Management Agency (FEMA) is worried whether its budget would be enough to cover additional damage, increasing the likelihood that the Congress might provide more funding during the next days.

In the meantime, markets are cautious to see whether North Korea will launch another intercontinental missile test on Saturday when it will celebrate its founding day, raising the risks of a dangerous military conflict between the US and the isolated regime. Late on Thursday, Trump argued that a military response is an "option" if North Korea continues developing its nuclear weapons.

The dollar index sank to a fresh 32-month low of 90.65 during the session, despite a fiscal policy relief on Wednesday when Trump and congressional Democrats agreed unexpectedly to raise the government's debt ceiling but only for the next three months.

Dollar/yen bottomed at a ten-month low of 107.31 before it climbed to 107.82 as risk-off sentiment was rising among investors.

The euro paused its uptrend versus the greenback, trading at $1.2026 after it managed to break above 1.21 in Asian trading. This came after the ECB decision on Thursday to hold interest rates unchanged and provide further hints on tapering its quantitate easing program most likely in October. However, unknown sources who have knowledge on the topic said that ECB plans to cut monthly asset purchases from 60bn euros currently to 20-40bn euros from the start of 2018 for a period of six to nine months.

The pound was in focus today as it surged by 1% on the day to a more than a 1-month high of $1.3213 on the back of a weaker dollar. Upbeat manufacturing data released out of the UK on Friday provided some support to the currency as well. On a monthly basis, manufacturing production in July rose by 0.5 percentage points to 0.5%, recording the highest growth since February, while analysts had projected an increase of only 0.3%.

This comes a week before BOE policymakers gather on Thursday to decide on monetary policy. However, markets anticipate the MPC members to follow their European counterparts and keep rates steady as recent economic evidence showed that the fifth biggest economy in the world continued growing slowly relative to its European peers after it posted the lowest growth since 2012 in the first quarter. The British Chambers of Commerce said on Friday that the British economy was "treading water" ahead of the divorce day in March 2019, while it also added that since the Brexit vote the pound's weakness did little for the exporters. The UK trade data published in the middle of the session justified this argument as the trade deficit widened by 0.05bn pounds to 11.58bn pounds, while forecasts were for the trade deficit to increase by an even bigger 0.42bn pounds.

Elsewhere, August jobs data out of Canada released today, showed the country's economy adding 22,200 positions during the month. This was better than the 19,000 which was expected by analysts and above July's 10,900. The unemployment rate ticked down to 6.2% from the 6.3% that was recorded in the previous month, which also coincided with economists' expectations. August's unemployment rate is the lowest the nation has experienced since October of 2008. The participation rate remained constant at 65.7%. On the downside, the positions added were attributed to part-timers, as full-time positions fell during the month. Another report released at the same time, showed industrial capacity utilization rising to 85.0% in the second quarter from 83.3% in first. The Canadian dollar weakened as the data went public with dollar/loonie advancing. The pair last traded 0.3% up on the day, while earlier in the day it fell to a fresh near 28-month low of 1.2060.

In commodities, oil prices were mixed. WTI crude was down by 0.65% at $48.77 per barrel while Brent was up by 0.15% at $54.63 per barrel.

Gold declined by 0.10% at $1,347.50 per ounce.

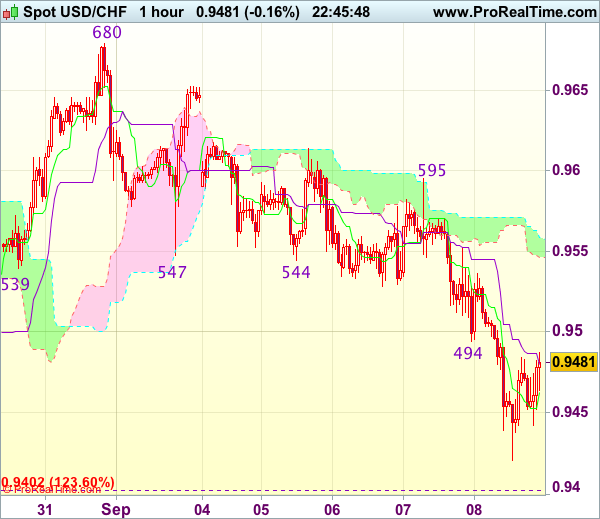

Trade Idea Wrap-up: USD/CHF – Hold long entered at 0.9450

USD/CHF - 0.9472

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 0.9466

Kijun-Sen level : 0.9479

Ichimoku cloud top : 0.9558

Ichimoku cloud bottom : 0.9546

Original strategy :

Bought at 0.9450, Target: 0.9550, Stop: 0.9415

Position : - Long at 0.9450

Target : - 0.9550

Stop : - 0.9415

New strategy :

Hold long entered at 0.9450, Target: 0.9550, Stop: 0.9420

Position : - Long at 0.9450

Target : - 0.9550

Stop : - 0.9420

As the greenback has dropped again and has remained under pressure, marginal weakness from here cannot be ruled out, however, loss of near term downward momentum should prevent sharp fall below 0.9415-20 and prospect of a rebound remains, ab one the Kijun-Sen (now at 0.9496) would bring subsequent gain to 0.9550 but dollar needs to penetrate resistance at 0.9595 to signal low is formed.

In view of this, we are holding on to our long position entered at 0.9450. Below 0.9415-20 would risk weakness to 0.9390-00, having said that, further sharp fall below 0.9370-75 should not be repeated and reckon 0.9350 would hold from here, bring rebound later.

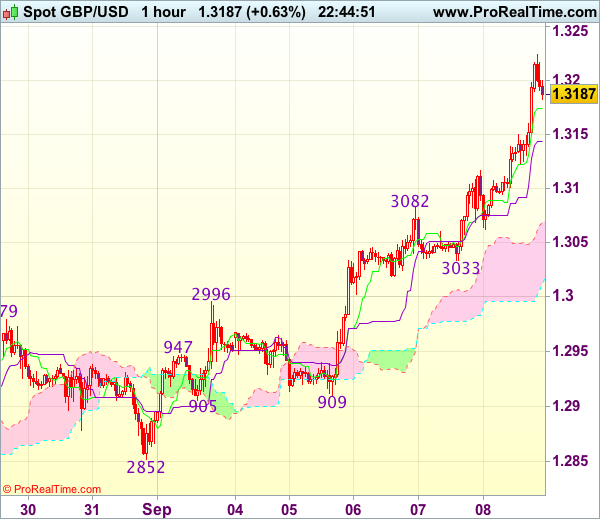

Trade Idea Wrap-up: GBP/USD – Buy at 1.3125

GBP/USD - 1.3189

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3175

Kijun-Sen level : 1.3143

Ichimoku cloud top : 1.3071

Ichimoku cloud bottom : 1.3018

Original strategy :

Buy at 1.3125, Target: 1.3225, Stop: 1.3090

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.3125, Target: 1.3225, Stop: 1.3090

Position : -

Target : -

Stop : -

As cable has surged again after brief pullback, adding credence to our bullish view that recent upmove from 1.2774 is still in progress and upside bias remains for further gain to 1.3225-30, then towards 1.3250, however, loss of near term upward momentum should prevent sharp move beyond latter level and price should falter below recent high at 1.3269, bring retreat later.

In view of this, would not chase this rise at current level and would be prudent to buy cable on subsequent pullback as 1.3120-25 should limit downside. Only below 1.3082 (previous resistance turned support) would abort ad suggest top is possibly formed, risk test of 1.3062 but reckon support at 1.3033 (yesterday’s low) would hold.

Elliott Wave Analysis: GBPJPY and Crude Oil

Good day traders! Today's focus will be on GBPJPY and Crude oil.

GBPJPY is making a new intra-day rise, which can be an indication that maybe blue wave two correction is completed and now sub-wave i) of three is in play. If that is the case, then more gains may follow on the pair.

GBPJPY, 1H

Crude oil is still trading sideways, now ideally in sub-wave d) of a triangle correction. Hopefully wave e) will unfold in the near-term as well and the whole correction will find support near the former wave four at the 48.50 level and make a new reaction higher.

Crude oil, 1H

Trade Idea Wrap-up: EUR/USD – Buy at 1.1985

EUR/USD - 1.2023

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 1.2045

Kijun-Sen level : 1.2039

Ichimoku cloud top : 1.1985

Ichimoku cloud bottom : 1.1968

Original strategy :

Buy at 1.1985, Target: 1.2090, Stop: 1.1950

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1985, Target: 1.2090, Stop: 1.1950

Position : -

Target : -

Stop : -

As the single currency has retreated after rising to 1.2093 earlier today, suggesting consolidation below this level would be seen and pullback to 1.2000 is likely, however, reckon minor support at 1.1984 would limit downside and bring another rise later, above 1.2070-75 would bring retest of said resistance at 1.2093 but break there is needed to extend recent upmove to 1.2130-40, having said that, loss of upward momentum should limit upside to 1.2150-55 (61.8% projection of 1.1119-1.1910 measuring from 1.1662), bring correction later.

In view of this, would be prudent to buy euro on further pullback as support at 1.1980-84 should limit downside and bring another upmove later. Below 1.1950 (previous resistance turned support) would signal a temporary top is formed instead bring weakness to 1.1925-30 first.