Sample Category Title

Trade Idea Wrap-up: USD/JPY – Sell at 108.65

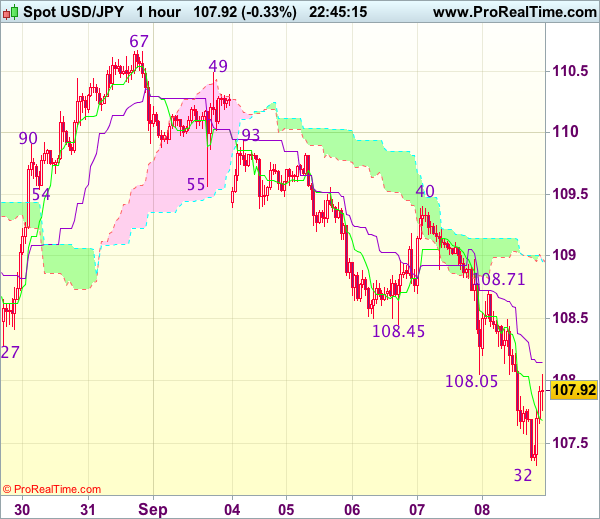

USD/JPY - 107.96

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 107.69

Kijun-Sen level : 108.15

Ichimoku cloud top : 108.98

Ichimoku cloud bottom : 108.96

Original strategy :

Sell at 108.45, Target: 107.45, Stop: 108.90

Position : -

Target : -

Stop : -

New strategy :

Sell at 108.65, Target: 107.65, Stop: 109.00

Position : -

Target : -

Stop : -

As the greenback has recovered after falling to 107.32, suggesting consolidation above this level would be seen and test of the Kijun-Sen (now at 108.15) is like, however, reckon upside would be limited to 108.50 and resistance at 108.71 should hold, bring another decline later, below said support at 107.32 would extend recent decline to 107.00-10, however, oversold condition should limit downside and reckon 106.80-82 (61.8% projection of 114.50-108.27 measuring from 110.67) would hold from here, bring rebound later.

In view of this, we are still looking to sell dollar on recovery as resistance at 108.71 should limit upside. Only above 108.95-00 would abort and suggest an intra-day low is formed, bring a stronger rebound towards indicated resistance at 109.40 but break there is needed to provide confirmation.

Trade Idea: EUR/GBP – Sell at 0.9200

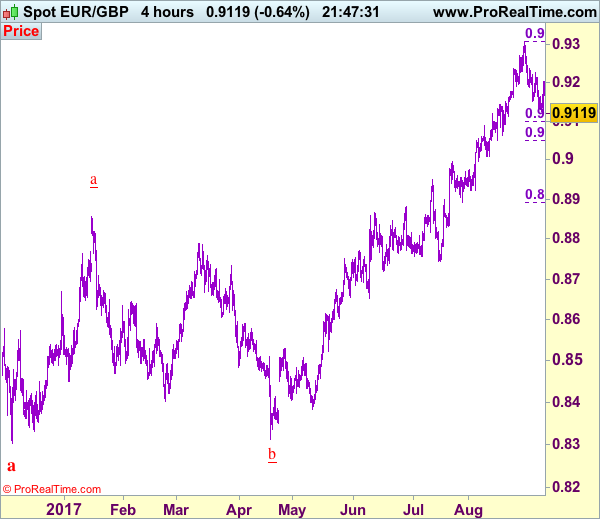

EUR/GBP - 0.9120

Original strategy :

Sell at 0.9225, Target: 0.9100, Stop: 0.9265

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9200, Target: 0.9060, Stop: 0.9240

Position : -

Target : -

Stop : -

As the single currency has slipped again after brief bounce to 0.9203, suggesting the fall from 0.9307 is still in progress and mild downside bias remains for this move from temporary top of 0.9307 to bring retracement of recent upmove to 0.9095-00 (50% Fibonacci retracement of 0.8892-0.9307), then towards 0.9050 (61.8% Fibonacci retracement), however, near term oversold condition should prevent sharp fall below latter level and price should stay well above support at 0.9008.

In view of this, we are inclined to sell euro on recovery as resistance at 0.9203 should limit upside. Above 0.9235-40 would suggest low is formed instead, bring a stronger rebound to 0.9270 but only above said resistance at 0.9307 would revive bullishness and extend recent upmove to 0.9325-30 and possibly towards 0.9350, however, loss of upward momentum should limit upside and price should falter below 0.9390-00.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Trade Idea: USD/CAD – Sell at 1.2240

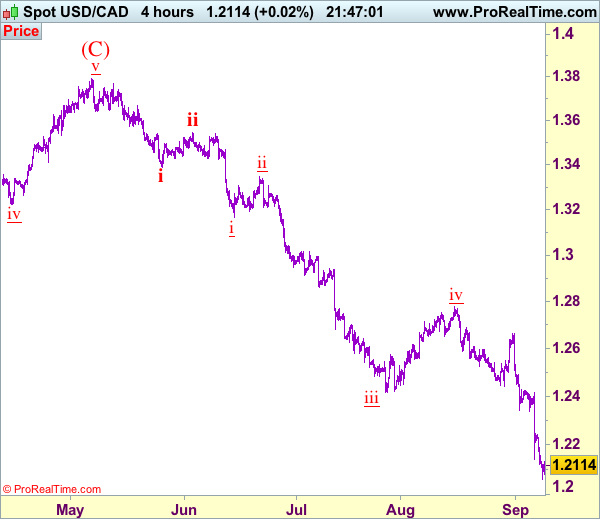

USD/CAD - 1.2145

Trend: Down

Original strategy :

Sell at 1.2285, Target: 1.2100, Stop: 1.2345

Position: -

Target: -

Stop: -

New strategy :

Sell at 1.2240, Target: 1.2080, Stop: 1.2300

Position: -

Target: -

Stop:-

As the greenback has recovered after falling to 1.2061, suggesting consolidation above this level would be seen and gain to 1.2200 cannot be ruled out, however, reckon resistance at 1.2245 would limit upside and bring another decline later, below said support at 1.2061 would signal recent decline is still in progress and may extend further weakness towards psychological support at 1.2000 but loss of downward momentum should prevent sharp fall below 1.1950-60, bring rebound later. We are keeping our count that wave v as well as wave (C) ended at 1.3794 and impulsive wave (i ii, i ii) is now unfolding with minor wave iii ended at 1.2414, followed by wave iv correction ended at 1.2778, wave v has reached our indicated downside target at 1.2100 and may extend to 1.2000.

In view o this, would not chase this fall here and would be prudent to sell on recovery as 1.2245 should limit upside. Above 1.2300 would would defer and risk a stronger rebound to 1.2335-40 but only break of resistance at 1.2429 would signal low is formed, bring retracement of recent decline to 1.2490-00.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

EUR/GBP Accelerated Lower

The pair accelerated lower on Friday and hit fresh marginally lower low at 0.9114, offsetting reversal signal that was formed by Wednesday's Doji and Thursday's bullish close and signaling further extension of pullback from 0.9306 (29 Aug high).

Fresh acceleration lower is eyeing next strong support at 0.9091 (Fibo 38.2% of 0.8744/0.9306), close below which would generate another strong bearish signal.

The price broke below 10/20SMA's which reinforces negative near-term outlook, as south-heading daily RSI is passing through neutrality territory and showing a plenty of room downside.

Firm break below Fibo 0.9091 support would trigger towards psychological 0.9000 level, reinforced by rising 55SMA).

South-turned 10SMA which capped upside action in past five days, offers solid resistance at 0.9184.

Res: 0.9184; 0.9210; 0.9237; 0.9268

Sup: 0.9114; 0.9091; 0.9062; 0.9024

EUR/GBP Resists Global Euro Rebound

- European stock markets trade mixed amid an empty eco calendar. US stock markets lose marginally ground in the opening. After heavy declines in USD and US rates, some calm returned today cross-markets.

- The UK's manufacturing sector (+0.5% M/M) started the third quarter on a stronger footing after falling into contraction earlier in the year, but overall growth in industrial output (+0.2%) remained sluggish despite consistently optimistic confidence surveys.

- Possibilities discussed by the ECB at yesterday's policy meeting on the future of APP included - but are not limited to - cutting monthly assets buys from €60 bn now to €40 bn or €20 bn from the start of next year, with extension options including 6 months or 9 months, said sources, who asked not to be named.

- China posted stronger-than-expected import growth in August, reinforcing views that the world's second-largest economy is still expanding at a healthy pace despite tighter policy. China's imports grew 13.3% Y/Y. Exports showed signs of softening, however, with growth cooling to 5.5% Y/Y.

- Canada added more jobs than expected last month (+22.2k) and the country's unemployment rate fell to the lowest level since 2008 (6.2%) in the latest sign of the economic recovery. Details showed though that 88.1K full time jobs were lost, while 110.k part time jobs were created. The Canadian dollar didn't react.

Rates

Core bonds lose slightly ground in dull session

The Bund and US Treasuries lost slightly ground following strong gains on Thursday and a good opening today. Eco data were few and uneventful. A "sources" article on the ECB suggested that 4 specific options were presented to the ECB governors yesterday on the tapering of the APP programme. It suggests that the ECB discussion went further than Draghi admitted. While as such that isn't big news, it might have been the trigger for a mild profit taking, especially after the Bund (and the US T-Note future) set a new high at the start of trading. The Bund correction came in late morning session, while the T-Note's dive occurred when US traders got involved. The correction was too all standards minor.

At the time of writing, US yields rise by 0.5 to 1.5 bps. German yields are 0.1 bp to 2 bps higher. Spanish and Italian bonds underperformed, maybe due to the Catalonian problem or due to the "source" article.

Sources suggested that ECB-policymakers were presented four options for the APP programme in 2018 that kept the programme within the existing parameters (issue/issuer limits). The options included, but were not limited to reducing the monthly purchase target to 40 or 20 B euros with extension options including 6 and 9 months. This is more specific that the reference of Mario Draghi that discussions were about the length and size of the monthly flows. ECB Weidmann said that one reason why the council decided to wait for now is uncertainty over the path of inflation, but he warned that officials should not miss the right moment to act.

Currencies

EUR/USD rallies even as Draghi brings no news

FX investors are still searching for the right strategy to avoid event risk this weekend or in the near future. The dollar remains more sensitive t than the yen or the euro. EUR/USD set a new correction low in the high 1.20 area early this morning. The rally stalled, but there is no sign of any meaningful correction. EUR/USD trades near 1.2050. USD/JPY remains below the key 108.13 area (currently 107.75). So, the USD alerts are still flickering.

This morning, Asian equities traded mixed with China again outperforming. Japanese Q2 GDP growth was downgraded more than expected from 4.0% to 2.5% Q/Qa. However, it didn't stop the rise of the yen. USD/JPY already dropped below 108.13 support before the European market opening. EUR/USD filled offers in the 1.2090 area, but upward pressure eased slightly as European traders entered. EUR/USD settled near the 1.2070 recent top.

The euro rally took a breather during the European morning session. The pair settled in an 1.2035/75 consolidation pattern. However, there was no indication at all that a meaningful correction was imminent. Changes in interest rate differentials between the euro and the dollar were again limited. IF anything they developed in favour of the euro. Other major dollar cross rates also indicated an ongoing uphill battle for the US currency. Interesting, European equities hardly suffered from the latest euro strength/dollar decline.

There were no important data in the US. Investors didn't want to place any big directional bets and basically try to avoid potential event risk (North Korea, bickering in Washington, economic and market impact of the hurricanes). Core bond yields rose marginally off the recent lows and the dollar shows tentative signs of an intraday bottoming process. However, the broader picture hasn't change. Dollar sentiment remains fragile and any negative news (from whatever origin) might put the US currency again under pressure. EUR/USD trades in the 1.2050 area. USD/JPY is changing hands in the 107.75 area.

EUR/GBP resists global euro rebound

There were again plenty of headlines on the stalemate in the Brexit negotiations and the UK eco data calendar was well filled. However, those topics played no important role in sterling trading. The rise of the euro took a breather early in Europe. EUR/GBP also declined from the 0.92 area to the 0.9160 area. The UK production data printed strong than expected and the trade deficit was smaller than forecast. Construction output missed consensus. We didn't see a direct impact on sterling trading. Even so, sterling bulls might find some indications of sterling resilience in today's price action. Sterling evidently extended gains against a bleeding dollar. Even more, EUR/GBP also resisted the overall strong bid in the euro. The pair even returned back to yesterday's pre-Draghi low. The jury is still out, but for now, sterling shows good resilience in an overall very uncertain context.

Canadian Dollar Unchanged after Strong Jobs Data

- Canada Aug Jobless Rate 6.2%; Jul 6.3% vs. Aug Forecast At 6.3%

- Canada Aug Net Jobs +22,200 From Jul vs. Aug Net Jobs Forecast At +15,000

- Canada Aug Avg Hourly Wages +1.8% From Year Ago

- Canada Labor Force +2,000 In Aug From Jul

- Aug Participation Rate At 65.7% Vs 65.7% In Jul

Canada added jobs in August and its unemployment rate fell for a third-straight month to a fresh post-crisis low, even though full-time employment declined steeply in the month.

Wages also rose at the fastest pace in 10 months, although still below the 2% level.

The report indicated the economy shed -88,100 full-time jobs, but that was offset by a +110,400 increase in part-time employment.

The CAD is trading atop of C$1.2100 just north of this week's dollar low move (C$1.2037) after Wednesday surprise Bank of Canada (BoC) rate hike of +25 bps to +1%.

Bank of Canada (BoC)

Three things that Bank of Canada's (BoC) Poloz has done with this week's surprise rate hike:

- A gradual approach to rate rises is now a "myth,"

- The hike came at a decision-only meeting (without press conference)

- and most importantly throws into the doubt the markets view that Poloz preferred a weaker CAD.

The BoC is now in rate "hike" cycle, but data dependent - fixed income dealers are beginning to price in +1.75% by the end of 2018.

Intraday, CAD is very much overbought, but there is 'no' reason to want to sell it at the moment. C$1.2030 is very strong dollar support - the USD needs to break above C$1.2350 - C$1.25 with conviction to get any dollar traction. With another Fed rate hike being priced out this will be difficult to sustain.

In the medium term, any USD rallies will see CAD buying to target C$1.1950-1.20. However, the "elephant" in the room remains NAFTA negotiations.

Gold Rally Hits 13-Month High

Gold continues to move upwards on Friday. In the North American session, gold is trading at $1353.40, up 0.32% on the day. On the release front, there are no major events, but we'll hear from FOMC member Patrick Harker, as the markets look for clues about interest rate policy.

It's been a strong September for gold prices, as the metal has gained 2.4 percent. The rally continued on Friday, as unemployment claims jumped to 298 thousand last week, the highest level since April 2015. This follows weak readings in July for nonfarm payrolls and wage growth. However, the jump in jobless claims can be attributed to Hurricane Harvey, which led to thousands of displaced workers in Texas filing for unemployment benefits. Unemployment claims could remain high in upcoming weeks, until flooded areas are able to get on their feet and rebuilding efforts pick up steam.

As a traditional safe-haven asset, gold tends to rise during geopolitical tensions. The global hot spot in recent weeks has been the Korean peninsula. North Korea recently tested a hydrogen bomb, sending alarm bells off in the the US, Japan and South Korea. As the crisis has worsened, nervous investors have snapped up gold. If the situation worsens, it's a safe bet that gold prices will continue to move higher. On Friday, gold has touched a high of $1357.62, its highest level since August 2016.

Inflation has been the Achilles Hill in the US economy for months, and this was reiterated in the Federal Reserve Beige Book report on Wednesday. The survey found that wage pressure remains limited, despite the fact that many businesses cannot fill job openings. The lack of wage growth has been an important factor in ongoing weak inflation levels, despite moderate economic growth and a very strong labor market. Weak inflation has hampered the Fed's plans to raise interest rates a third time this year, and the odds of a December hike have dipped to just 31%, as the markets are increasingly doubtful that the Fed will make a move before next year.

USDCAD Consolidating Above Fresh Low at 1.2061

The USDCAD pair is consolidating above fresh low at 1.2061 posted earlier today (the lowest since mid-May 2015) after six straight days in red. The pair traded in a choppy mode around 1.2100 handle after release of Canada's jobs data for August. Unemployment dropped to 6.2% in August, hitting 9-year low, vs 6.3% forecast as economy added more jobs than expected. Employment change showed 22.2K new jobs created in August, against forecasted increase by 19K and well above 10.9K seen last month. Another upbeat figure came from part-time jobs which showed 110.4K part-time jobs added last month, but overall picture was soured by fall of 88.1K full-time jobs in August. Mixed jobs report kept Loonie in directionless near-term mode after it registered strong gains of over 2.5% against the dollar since the beginning of the week, but without firmer correction signal so far, despite strongly oversold daily studies. However, the pair may show stronger hesitation ahead of targets at 1.2046 (50% retracement of larger 0.9405/1.4688 rally) and psychological 1.2000 support. Bearish divergence on daily RSI and MACD supports scenario of corrective rally in the near term, but limited upside is seen as the greenback remains under strong pressure and may fall further if geopolitical situation over North Korea deteriorates during the weekend.

Res: 1.2141; 1.2200; 1.2240; 1.2300

Sup: 1.2061; 1.2046; 1.2000; 1.1910

Canada Notches Up a Ninth Straight Month of Job Gains

Canada saw another month of job gains, as 22.2k net positions were added in August. This was sufficient to bring the unemployment rate a tick lower, to 6.2%, close to pre-crisis lows.

The mix of jobs was somewhat unfavourable, as part-time work rose dramatically (+110.4k) and full-time positions declined by 88.1k. Both public sector (-8.3k) and the private sector (-2.1k) saw modest net employment declines, leaving self-employment (+32.7k) to fill the void.

Across industries, the goods-producers saw an overall decline (-13.7k), driven by manufacturing (-11.1k), and natural resources (-7.7k). It was a more positive story for services (+35.9k in aggregate) as net employment gains were recorded across most of the major industry groups.

Regionally, Ontario again drove the gain, adding 31.1k net positions, sufficient to reduce the provincial unemployment rate to 5.7%, a level last seen around the turn of the millennium. Employment was flat to slightly down across the remaining provinces.

The hours worked and wage rate figures were fairly encouraging: hours worked rose 2.2% year-on-year despite the climb in part-time work, helped by a drop recorded at this time last year (on a month-on-month basis, aggregate hours worked fell a tick). Similarly, the hourly wage rate ticked up 0.5%-pts to 1.8% year-on-year, continuing the acceleration seen last month.

Key Implications

August saw another month of job gains, and yet another month with mixed details. Part-time job growth, and self-employment drove the gains, resulting in a slight tick-back in aggregate hours worked. Indeed, the 88k drop in full-time work was enough to erase the better part of the previous three months' gains in this category.

Still, details can't be mixed if they're all bad, and the tick up in the hourly wage rate to 1.8% year-on-year is encouraging to see, particularly when compared with the soft growth seen earlier in the year.

Overall, while the August job figures hardly paint a picture of robustness, this is a noisy series, and the trend this year remains a healthy one (let's not forget the 105k full-time jobs added in February, or the 77k added in May). The further rise in wages is likely to provide more assurance to the Bank of Canada that overall price pressures are beginning to turn the corner, further supporting their decision to hike this week, and consistent with additional tightening before the year ends.

Employment in Canada Continued to Rise in August

Highlights:

- Employment rose 22.2k in August following a 10.9k rise in July.

- The unemployment rate in August dropped to 6.2% from 6.3% in July.

- The employment gain was significantly skewed towards part-time employment which soared 110.4k with full-time employment plummeting 88.1k. Despite this weakness in August, earlier strong gains contributed to full-time employment averaging a solid monthly increase of 17.8k over the past year.

- Manufacturing jobs fell 11.1k in August though it was offset by relatively widespread gains in service producing jobs which increased in aggregate by 35.9k.

Our Take:

The Canadian economy continues to generate jobs with hiring in August rising to 22.2K from the 10.9k gain recorded in July. This sent the unemployment rate down to 6.2% from July's rate of 6.3%. The employment increase over the last two months does represent a moderation from the very robust 29K average monthly increase evident over the prior twelve months. This strength in labour markets has been consistent with GDP growth rising by more than double the economy's long-run average or potential, rate over the last four quarters ending in 2017Q2. Despite rapid tightening in both labour and product markets, inflation pressures have been largely absent with consumer price inflation remaining well below the central bank's 2% mid-range target. However, today's employment report is providing tentative evidence of wage pressures starting to build with the year-over-year increase in average hourly earnings rising to 1.7% in August relative to 1.2% in July and a low in April of 0.5%. This wage measure is starting to mirror the upward trend evident in Canada's SEPH payroll employment survey where the fixed weighted wage measure was up 2.7% in June relative to a recent low at the start of the year of 1.5%. Indications of rising wage pressure provides validation of the Bank of Canada 25 basis point hike in the overnight rate to 1.00% which followed a similar increase at the policy meeting in July. Assuming continued above-potential growth and consumer price inflation starting to trend closer to the 2% target, the Bank of Canada is expected to continue to tighten with the overnight rate projected to rise to 2.00% by the end of 2018.