Sample Category Title

European Open Briefing: Asian Equity Markets Bounced Back On Thursday

Global Markets:

- Asian stock markets: Nikkei gained 0.19 %, Shanghai Composite down 0.06 %, Hang Seng rose 0.11 %, ASX 200 fell 0.06 %

- Commodities: Gold at $1340.68 (+0.13 %), Silver at $17.94 (+0.21 %), WTI Oil at $49.05 (-0.22 %), Brent Oil at $54.03 (-0.31%)

- Rates: US 10-year yield at 2.09, UK 10-year yield at 1.01, German 10-year yield at 0.35

News & Data:

- (AUD) Retail Sales m/m 0.0 % vs 0.2 % expected

- (AUD) Trade Balance 0.46 B vs 0.93 B expected

- (CAD) Trade Balance -3.0 B vs -3.2 B expected

- (CAD) Labor Productivity q/q -0.1 % vs 0.9 % expected

- (USD) Trade Balance -43.7 B vs -44.6 B expected

- (CAD) Overnight Rate 1.00 % vs 0.75 % expected

- (USD) ISM Non-Manufacturing PMI 55.3 vs 55.8 expected

- US seeks oil embargo on North Korea, according to a draft UN resolution- AFP

- Oil steady as U.S. refining demand rises but ample crude supplies weigh- RTRS

Markets Update:

Asian equity markets bounced back on Thursday, tracking overnight gains on the wall street. The US Markets gained as investors weighed a deal that ensures the funding of its government through mid-December against persistent geopolitical tensions.

USDJPY is currently seen trading around 109.030. Following a fall of around 0.4 percent against the US Dollar yesterday, the Japanese yen was slightly higher early on Thursday as the pair dropped under 108.90 very briefly before bouncing back to around 109.20.

AUDUSD dropped a few points, back under the round number 0.8 and is currently seen trading around 0.7990. Both the Australian Data came in negative with the Trade Balance dropping to 0.46 Billion from 0.89 Billion and the change in total value of Retail sales falling to 0.0% against the expected 0.2%

EURUSD stood almost flat currently seen trading at 1.1927 as the global investors remained on the side-lines ahead of the ECB's policy meeting. The Euro added a mere 0.1 percent against the US Dollar. The dollar index, which tracks the dollar against a basket of currencies, lost a little over 0.1% and is currently valued at 92.17.

Upcoming Events:

- 07:30 GMT – (GBP) Halifax HPI m/m

- 11:45 GMT – (EUR) Minimum Bid Rate

- 12:30 GMT – (CAD) Building Permits m/m

- 12:30 GMT – (EUR) ECB Press Conference

- 12:30 GMT – (USD) Unemployment Claims

- 14:00 GMT – (CAD) Ivey PMI

- 15:00 GMT – (USD) Crude Oil Inventories

- 23:00 GMT – (USD) FOMC Member Dudley Speaks

- 23:50 GMT – (JPY) Final GDP q/q

Market Update – Asian Session: US Temporary Debt Deal Provides Some Relief To The Markets

Asia Summary

Asian equity markets opened mostly higher with short term stability seen in US government on funding deal, gains overall remained muted as South Korea prepares for any action from the North. China was weaker, being dragged down by real estate names after S&P commented on the sector’s leverage.

US Senate reached a deal to keep the government funded to early December, after the US close a Republican congressional aide says in debt ceiling talks today there was no discussion of blocking the Treasury from using extraordinary measures.

Currencies were quiet for another session yen a little stronger, Aussie weaker after weaker than expected retail sales and trade surplus. PBOC again set the yuan mid-point rate stronger for the 9th consecutive setting and the longest run since 2011. It did skip OMO operations electing to use CNY298B in 1-yr medium-term lending facility, rate of 3.2% was left unchanged from prior. Mid-session financial press reported that there was a h.

Overnight Russia reiterated that tougher sanctions would not help the North Korea situation however today Japan PM Abe and South Korea President Moon held meeting and said they agree to seek maximum sanctions on North Korea. South Korea Vice Foreign Min Lim noted that the UN discussing banning North Korea exports of textiles and workers. South Korea confirmed it has set up four additional Thaad missile shields in addition to its regular two.

Key economic data

(AU) Australia Aug AiG Performance of Construction Index: 55.3 v 60.5 prior

(JP) Foreign investors net bought ¥1.35T in Japan bonds v bought ¥500.2B prior (3rd largest buy on record)

(AU) AUSTRALIA JULY RETAIL SALES M/M: 0.0% V 0.2%E

(AU) AUSTRALIA JULY TRADE BALANCE (A$): 460M V 1.0BE

Speakers and Press

China

(CN) S&P: China property developer margins are up, leverage unchanged but will moderately improve

(CN) China increases financial regulation to address risks (reference to ban on Initial Coin Offerings) - Xinhua

Korea

(KR) Moody's: If there was a short contained military conflict, the credit implications would be limited; Damage to sovereign credit profile would depend on length and intensity of any conflict

(KR) South Korea PM Lee: North Korea may launch missile on Sept 9th (reiteration)

(KR) Full artillery of the Thaad missile shield in South Korea will be ready for operation as soon as an internal process ends, this is 4 additional launches on top of the 2 already

(KR) US White House Official: Confirms to set aside for now consideration of terminating free trade agreement with South Korea

Other

USD/PHP (PH) Philippines Central Bank Gov Espenilla: Philippines to ease FX rules further this year, to streamline FX requirements

Asian Equity Indices/Futures (00:00ET)

Nikkei +0.1%, Hang Seng +0.1%; Shanghai Composite -0.1%, ASX200 +0.1%, Kospi +1.1%

Equity Futures: S&P500 -0.1%; Nasdaq100 -0.1%, Dax +0.1%, FTSE100 +0.1%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1935-1.1919; JPY 109.26-108.89; AUD 0.8018-0.7984; NZD 0.7218-0.7195

Dec Gold +0.1% at $1,340/oz; Oct Crude Oil -0.2% at $49.06/brl; Sept Copper -0.3% at $3.15/lb

(CN) China PBOC skips OMO v CNY180B in 7 and 14-day reverse reports prior: net drains CNY100B v drains CNY40B prior

GLD SPDR Gold Trust ETF daily holdings -0.4% to 837.1 metric tonnes

(US) Weekly API Oil Inventories: Crude: +2.8M v -5.8M prior

USD/CNY *(CN) PBOC SETS YUAN REFERENCE RATE AT: 6.5269 V 6.5311 PRIOR (9th consecutive stronger setting, longest run since 2011)

(CN) China PBoC skips OMO v injects CNY40B prior in 7-day and 28-day reverse repos

(CN) PBOC conducts CNY298B v CNY360B prior in 1-yr MLF 3.2% v 3.2% prior in medium term lending facility (MLF) operations

(JP) Japan MoF sells ¥3.622T in 3-month bills; avg yield -0.2040% v -0.1463% prior; bid-to-cover 3.19x

JGB (JP) Japan MoF sells ¥658.3B in 0.8% (0.8% prior) 30-yr bonds; Avg yield: 0.8320% v 0.8760% prior; Bid to cover: 3.67x v 3.90x prior

Equities notable movers

Australia/New Zealand

MBE.AU Launches AddGlu for Marketers a Predictive Customer Acquisition Platform for Digital Performance Marketing; +8.6%

Hong Kong/China

3383.HK Agile Property Holdings, +6.4%; 2007.HK Country Garden Holdings, +3.8% Both names move on broader real estate sector move

2313.HK Prices 52.1M shares at HK$58.60 v 58.50-60.50 expected range; -6.4%

Australia’s Construction Sector Growth Cooled In August, Trade Surplus Unexpectedly Contracted In July

For the 24 hours to 23:00 GMT, the AUD marginally rose against the USD and closed at 0.8007.

LME Copper prices declined 0.6% or $40.0/MT to $6864.0/MT. Aluminium prices declined 0.6% or $12.5/MT to $2069.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7989, with the AUD trading 0.22% lower against the USD from yesterday's close, following the release of dismal economic data from Australia.

Data indicated that Australia's AiG performance of construction index dropped to a level of 55.3 in August, following a reading of 60.5 in the previous month. Additionally, the nation's seasonally adjusted trade surplus surprisingly narrowed to A$460.0 million in July, from a revised surplus of A$888.0 million in the prior month. Market participants had anticipated for the country's trade surplus to widen to A$1000.0 million.

Moreover, the nation's seasonally adjusted retail sales surprisingly remained flat on a monthly basis in July, compared to market consensus for a gain of 0.2%. Retail sales had registered a revised rise of 0.2% in the previous month.

The pair is expected to find support at 0.7962, and a fall through could take it to the next support level of 0.7936. The pair is expected to find its first resistance at 0.8017, and a rise through could take it to the next resistance level of 0.8046.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

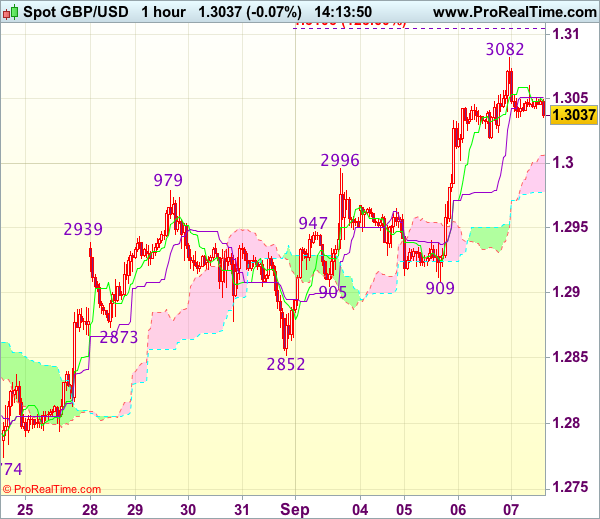

Trade Idea : GBP/USD – Buy at 1.2980

GBP/USD - 1.3043

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3048

Kijun-Sen level : 1.3051

Ichimoku cloud top : 1.3006

Ichimoku cloud bottom : 1.2977

Original strategy :

Buy at 1.2970, Target: 1.3070, Stop: 1.2935

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2980, Target: 1.3080, Stop: 1.2945

Position : -

Target : -

Stop : -

As cable has retreated after rising to 1.3082 yesterday, suggesting minor consolidation below this level would be seen and pullback to 1.3005-10 cannot be ruled out, however, reckon downside would be limited to previous resistance at 1.2996 and the lower Kumo (now at 1.2977) should hold, bring another rise later, above said resistance at 1.3082 would signal recent rise from 1.2774 is still in progress and may extend gain to 1.3100, however, loss of near term upward momentum should prevent sharp move beyond 1.3140-50, risk from there is seen for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy cable on pullback as previous resistance at 1.2996 should limit downside and bring another rise. Below the Ichimoku cloud bottom (now at 1.2977) would defer and risk weakness to 1.2950 and possibly 1.2930 but only break of support at 1.2905-09 would signal top is formed.

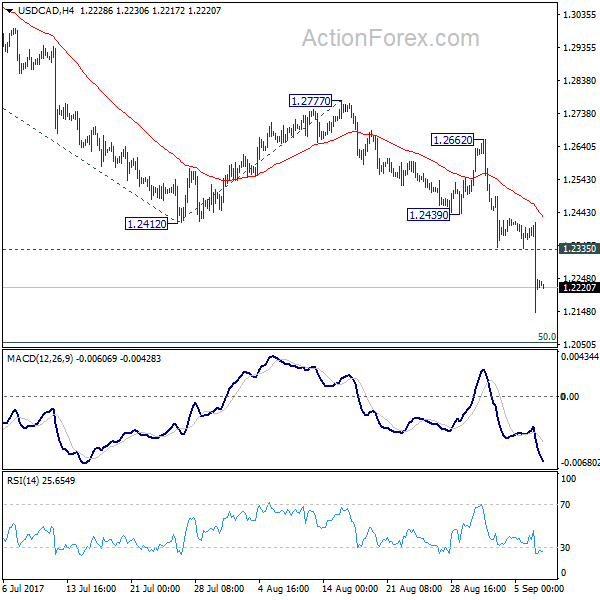

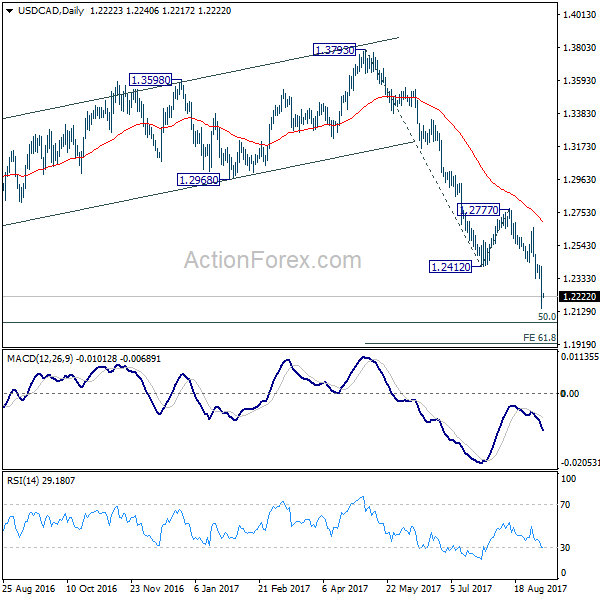

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2096; (P) 1.2255; (R1) 1.2385; More....

Intraday bias in USD/CAD remains on the downside for next long term fibonacci level at 1.2048. Downside momentum as seen in daily MACD is picking up again. Firm break of 1.2048 will carry larger bearish implication and target 61.8% projection of 1.3793 to 1.2412 from 1.2777 at 1.1924 next. On the upside, above 1.2335 minor resistance will turn intraday bias neutral first. But outlook will remain bearish as long as 1.2662 resistance holds.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. Such corrective fall is expected to extend to 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. Break of 1.2777 resistance will indicate reversal and turn outlook bullish for 1.3793 key resistance. However, sustained break of 1.2048 will dampen this view and carry larger bearish implications and bring deeper decline to 61.8% retracement at 1.1424 and below.

Germany’s Factory Orders Fell For The First Time In Three Months In July

For the 24 hours to 23:00 GMT, the EUR marginally rose against the USD and closed at 1.1925.

On the data front, Germany's seasonally adjusted factory orders unexpectedly dropped 0.7% on a monthly basis in July, defying market expectations for an advance of 0.2%. In the previous month, factory orders had gained by a revised 0.9%. Additionally, the nation's Markit construction PMI dropped to a level of 54.9 in August, after recording a level of 55.8 in the prior month.

The US Dollar declined against a basket of currencies, after the Federal Reserve (Fed) Vice Chairman, Stanley Fischer, surprisingly announced his resignation months before his term was due to end.

However, losses in the greenback were trimmed, after the US President, Donald Trump and top Democrats forged a deal to pass an extension of the debt limit for around three months.

Separately, macroeconomic data indicated that the US ISM non-manufacturing PMI advanced less-than-expected to a level of 55.3 in August, compared to a reading of 53.9 in the previous month, while markets were anticipating for a rise to a level of 55.5. Moreover, the nation's trade deficit advanced to $43.7 billion in July, while investors had envisaged the nation's trade deficit to rise to a level $44.7 billion. In the previous month, the nation had posted a revised deficit of $43.5 billion.

Other economic data showed that the US final Markit services PMI climbed less than initially estimated to a level of 56.0 in August, while the preliminary figures had indicated an increase to a level of 56.9. In the previous month, the PMI had registered a level of 54.7. Also, the nation's mortgage applications rebounded 3.3% in the week ended 01 September, after recording a drop of 2.3% in the prior week.

Meanwhile, the Fed's Beige Book report showed that the US economic activity expanded at a modest to moderate pace in July through mid-August, but signs of an acceleration in inflation remained slight. Also, it reported scant wage pressures, modest to moderate wage growth and worker shortages in numerous industries. Also, business contacts raised concerns about a prolonged slowdown in the auto industry.

In the Asian session, at GMT0300, the pair is trading at 1.1925, with the EUR trading flat against the USD from yesterday's close.

The pair is expected to find support at 1.1904, and a fall through could take it to the next support level of 1.1883. The pair is expected to find its first resistance at 1.1948, and a rise through could take it to the next resistance level of 1.1971.

Moving ahead, traders will eye the European Central Bank's (ECB) monetary policy meeting, scheduled later in the day, to get clarity on the central bank's plans of tapering its bond-purchasing programme. Moreover, final reading on the Euro-zone's 2Q GDP as well as Germany's industrial production data for July, will be on investors' radar. Separately, the US initial jobless claims data, set to release later in the day, will also attract market attention.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Pound Trading A Tad Lower In The Morning Session

For the 24 hours to 23:00 GMT, the GBP marginally rose against the USD and closed at 1.3048.

In the Asian session, at GMT0300, the pair is trading at 1.3043, with the GBP trading slightly lower against the USD from yesterday’s close.

The pair is expected to find support at 1.3014, and a fall through could take it to the next support level of 1.2985. The pair is expected to find its first resistance at 1.3077, and a rise through could take it to the next resistance level of 1.3111.

Looking forward, investors will focus on UK’s Halifax house prices data for August, slated to release in a few hours.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average

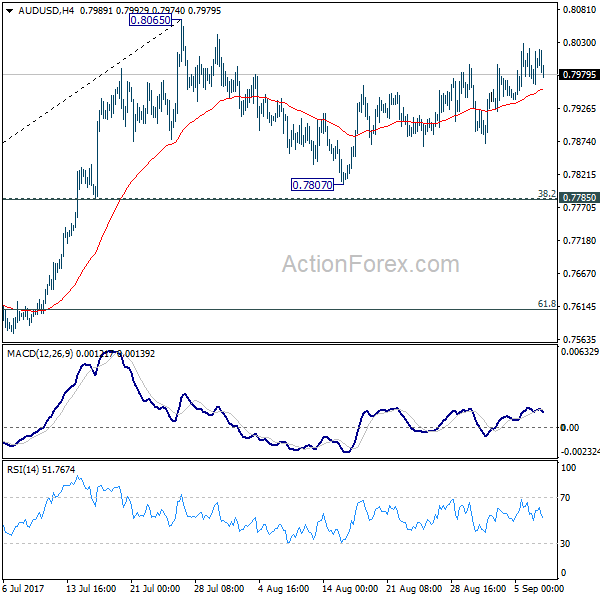

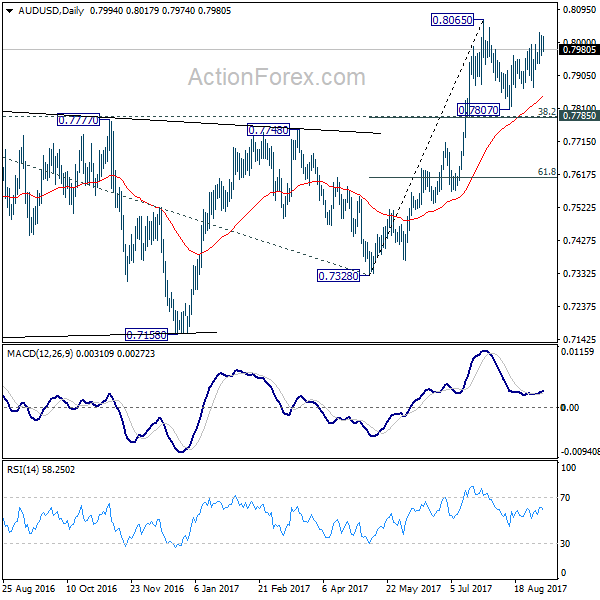

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7969; (P) 0.7994; (R1) 0.8026; More...

AUD/USD is still bounded in consolidation from 0.8065 and intraday bias stays neutral first. In case of another fall, downside should be contained by 0.7785 cluster support (38.2% retracement of 0.7328 to 0.8065 at 0.7783) to bring rebound. On the upside, break of 0.8065 will resume the medium term rise and target 100% projection of 0.6826 to 0.7833 from 0.7328 at 0.8335.

In the bigger picture, rise from 0.6826 medium term bottom is still in progress. At this point, there is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, break of 55 month EMA (now at 0.8087) will target 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now in favor.

Japanese Yen Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the USD rose 0.53% against the JPY and closed at 109.20.

In the Asian session, at GMT0300, the pair is trading at 109.10, with the USD trading 0.09% lower against the USD from yesterday’s close.

The pair is expected to find support at 108.57, and a fall through could take it to the next support level of 108.03. The pair is expected to find its first resistance at 109.52, and a rise through could take it to the next resistance level of 109.93.

Going ahead, market participants will look forward to Japan’s final GDP numbers for 2Q 2017 and trade balance (BOP basis) data for July, slated to release overnight.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Swiss Franc Trading Marginally Lower In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.22% against the CHF and closed at 0.9560.

In the Asian session, at GMT0300, the pair is trading at 0.9563, with the USD trading a tad higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9529, and a fall through could take it to the next support level of 0.9496. The pair is expected to find its first resistance at 0.9595, and a rise through could take it to the next resistance level of 0.9628.

With no macroeconomic releases in Switzerland today, investor sentiment will be governed by global macroeconomic events.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.