Sample Category Title

AUD/USD More Upside In View

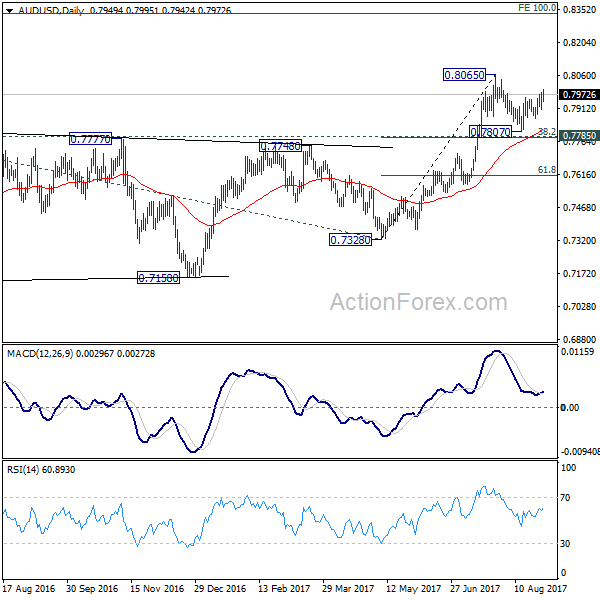

Price climbs higher aggressively as the USD was weakened seriously by the USDX’s drop. AUD/USD is strongly bullish on the Daily chart, should approach and reach the 0.8065 swing high, only a failure to do this will signal an exhaustion and a potential decrease.

The pair rallies and seems motivated to jump above the 0.8000 psychological level in the upcoming hours.

The USDX has managed to rebound in the US session and to stay above the 92.00 psychological level, now is trading in the red again, but we may have a bounce back on the short term after the yesterday’s spike. The dollar index plunged through the 91.91 long term horizontal support, but failed to stay there and closed the day at 92.35 level.

The Aussie rallied also because the Australian Building Approvals dropped only by 1.7% in the previous month, less versus the 5.4% estimate, while the Construction Work Done rose by 9.3% in the second quarter, beating the 0.9% estimate.

You should keep an eye on the economic calendar because the US is to release high impact data in the afternoon, which could shake the markets.

Price moves higher after the retest of the lower median line (LML) of the major ascending pitchfork, It is approaching the 0.8065 highest high, where he may find resistance again. The retreat towards the LML was natural after the failure to reach and retest the median line (ml) of the ascending pitchfork. A failure to reach the mentioned static resistance will signal and exhaustion and a potential reversal.

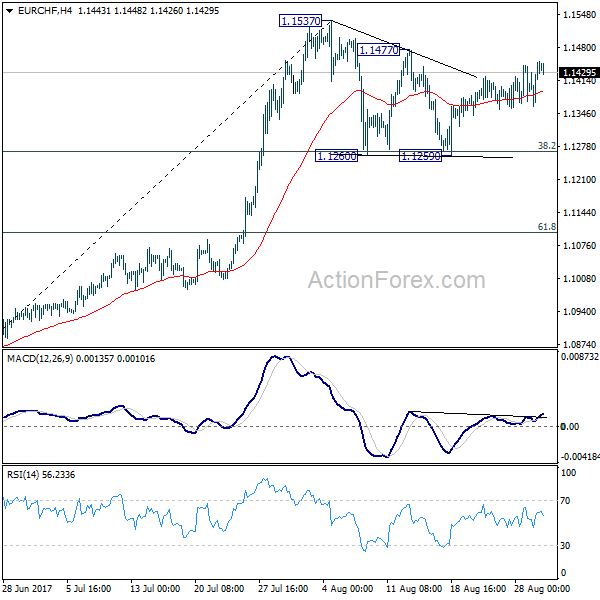

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1381; (P) 1.1416; (R1) 1.1472; More...

Intraday bias in EUR/CHF remains neural as consolidation from 1.1537 might extend. On the upside, break of 1.1477 resistance will argue that the consolidation from 1.1537 has completed and larger rise is resuming. Further break of 1.1537 will confirm and target 1.2 key resistance level next. On the downside, however, firm break of 38.2% retracement of 1.0830 to 1.1537 at 1.1267 will extend the correction to 61.8% retracement at 1.1100 before completion.

In the bigger picture, firm break of 1.1198 key resistance confirms resumption of the long term rise from SNB spike low back in 2015. In this case, EUR/CHF would eventually head back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1087 resistance turned support holds.

Precious Metals Keep Their Feet On The Pedals

Precious metals gave back some gains to varying degrees as the dollar corrected, but overall still paint a rosy picture.

Gold

Gold gave back most of its gains overnight to finish unchanged at 1311.00 from the previous day. Having spiked to 1326.00 yesterday on the North Korean headlines in early Asia trading, gold fell victim to the general recovery in the U.S. dollar. New York unwinding the extreme short term positioning the headlines had generated earlier in the day.

Gold's pullback looks corrective in nature from a technical perspective. In the bigger picture the yellow metal consolidating its gains around the 1311.00 mark well above the previous high at 1301.00. An overbought RSI and some heavy data days from the U.S. into Friday's Non-Farm Payrolls may slow the charge for now, but overall the technical picture remains constructive.

Gold has resistance at the overnight highs of 1326.00 followed by 1337.00. Support rests at 1301.00 and 1296.00 followed by the ascending trend line, today at 1282.50.

Silver

Silver too, gave up its overnight gains to finish just above support at 17.3900. It has managed a small rally in Asia though, climbing back to 17.4510 in early trading to level the technical picture still positive.

Key resistance still lies at 17.7600 with only a break of the ascending trend line support at 16.8830 casting doubt on the technical picture.

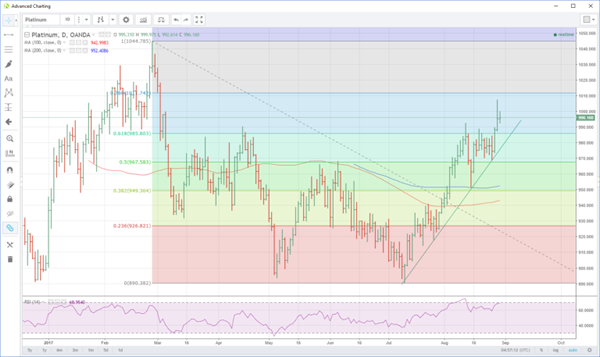

Platinum

Platinum carved through the psychological 1000.00 mark overnight and of the three metals, gave up the least of its gains, finishing comfortably above its opening to close at 995.00.

Platinum has continued to push higher in early Asia trading, up five dollars to 1000.00. Initial resistance is at the overnight high of 1007.00 followed by the more formidable 76.80% Fibonacci at 1012.00.

Supports appears initially at 989.00 followed by the rising trendline support today at 976.00.

Palladium

Shrugs of the dollar correction and marches higher, as has been its want for most of the year. Among the precious metals, Palladium hardly flinched yesterday, finishing at 945.00 just off its highs of 950.00 and first resistance level. support appears at 941.00 followed by the 919.00 breakout. Although the RSI is approaching overbought territory, any correction will likely be a shallow one looking at the technical picture.

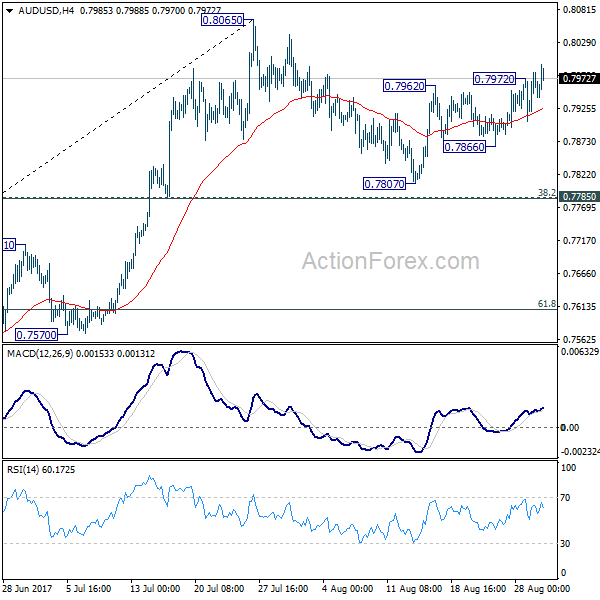

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7910; (P) 0.7947; (R1) 0.7988; More...

Break of 0.7927 suggests that rebound from 0.7807 has resumed. Intraday bias is turned back to the upside for 0.8065 high next. Firm break of 0.8065 will resume the medium term rise and target 100% projection of 0.6826 to 0.7833 from 0.7328 at 0.8335. On the downside, below 0.7866 will extend the correction from 0.8065. But downside should be contained by 0.7785 cluster support (38.2% retracement of 0.7328 to 0.8065 at 0.7783) to bring rebound.

In the bigger picture, rise from 0.6826 medium term bottom is still in progress. At this point, there is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, break of 55 month EMA (now at 0.8097) will target 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now in favor.

Market Update – Asian Session: Australia Building Approvals Better Than Expected

Asia Summary

Asian equity markets opened mixed but mostly higher, as action on North Korea so far has been restrained from the global community. KCNA reported that the missile launching drill is the first step of the military operation in the Pacific and a "meaningful prelude" to containing Guam. China Foreign Min Wang said China will 'fully and completely’ abide by UN Resolutions but was not in favor of unilateral sanctions against North Korea. In New Zealand, RBNZ Govt Wheeler comments that a lower NZD is needed to increase tradables inflation, sending the Kiwi down initially 0.2% to 0.7232 before reversing to 0.7260. Wheeler also noted that LVRS are not expected to be a permanent measure but their removal would require a degree of confidence that financial stability risks won’t deteriorate again. China yuan rose to a 14-month high to 6.5813, in its 4th consecutive day of gains, feeding off weaker USD, with risk off sentiment trickling back into the market. PBOC OMO drained a net CNY100B v injections the last several days.

Saw several comments out of China govt officials from the bimonthly session of the National People's Congress Standing Committee. China National Development and Reform Commission (NDRC) chief He Lifeng: China can meet its 2017 targets on GDP, employment, inflation, fiscal revenue and trade, it may struggle to achieve investment and foreign investment goals. China Fin Min Xiao Jie: China will contain the growth of hidden debt with active, prudent steps to defuse local debt risk. Australia July building approves continue to fall though much lower than expected. Q2 construction works done came in at 9.3% v the expected 1%. AUD/USD rose on the building data, then continued its momentum into the second part of the session.

Key economic data

(NZ) New Zealand Jul Building Permits m/m: -0.7% v -1.3% prior

(JP) JAPAN JUL RETAIL SALES M/M: 1.1% V 0.3%E; RETAIL TRADE Y/Y: 1.9% V 1.0%E

(AU) AUSTRALIA JUL BUILDING APPROVALS M/M: -1.7% V -5.0%E; Y/Y: -13.9% V -16.6%E

(AU) AUSTRALIA Q2 CONSTRUCTION WORK DONE Q/Q: 9.3% V 1.0%E

Speakers and Press

China/Hong Kong

(CN) Negotiable Certificate of Deposit (NCD) due to mature in Sept to have limited impact on liquidity in China - China Financial News

(CN) China rust-belt provinces are driving the rapid growth in shadow lending - financial press

(CN) China National Development and Reform Commission (NDRC) chief He Lifeng: China can meet its 2017 targets on GDP, employment, inflation, fiscal revenue and trade, it may struggle to achieve investment and foreign investment goals

Korea

(US) Reportedly will not call for U.N. Security Council to impose oil embargo on N. Korea today – press

(KR) North Korea test fired Hwasong-12 IRBM against US/South Korea drills, was guided by Kim – KCNA

Japan

(JP) Japan said to be considering reducing 2018 budget request to ¥98T - Nikkei

Other

(NZ) CoreLogic assessment of New Zealand housing market for August and September: Market activity gauge is -30% y/y

Asian Equity Indices/Futures (00:00ET)

Nikkei +0.6%, Hang Seng +0.8%; Shanghai Composite 0.0%, ASX200 -0.2%, Kospi +0.1%

Equity Futures: S&P500 +0.1%; Nasdaq100 +0.1%, Dax +0.1%, FTSE100 -0.1%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1984-1.1963; JPY 109.92-109.54; AUD 0.7996-0.7948; NZD 0.7278-0.7232

Dec Gold -0.1% at $1,318/oz; Oct Crude Oil -0.3% at $46.31/brl; Sept Copper +0.2% at $3.11/lb

GLD SPDR Gold Trust ETF daily holdings higher by 2.07 tonnes to 816.43 tonnes

(AU) Australia sells A$900M in 2.25% 2028 bonds; avg yield 2.7060%; bid-to-cover 2.76x

(CN) China PBOC OMO injects CNY130B in 7-day and 14-day v injects CNY50B prior in 7-day reverse repo prior; Net drains CNY100B v injects CNY10B prior

USD/CNY *(CN) PBOC SETS YUAN REFERENCE RATE AT 6.6102 V 6.6293 PRIOR

Equities notable movers

Australia/New Zealand

TLS.AU Comments on NBN monetization: NBN noted its position is not protected by the proposed monetization; +4.2%

OMH.AU Reports H1 (A$) Net loss 21.3M v loss 82.2M y/y, Rev 263M v 183M y/y; +9%

RFX.AU Reports FY17 (A$) Net -12.9M, -9% y/y, Rev 1.4M, +14% y/y -12.5%

Hong Kong/China

813.HK Reports H1 (CNY) Net 3.88B v 3.50B y/y; Rev 35.8B v 30.0B y/y; +16%

1813.HK Issues clarification to certain press articles; Says comments made by general manager Yang Huan regarding 2018-2020 outlook were his own personal comments; +11.4%

Focus On Missile Launch Aftermath As North Korea Says More To Come

Market movers today

The first information about euro area inflation in August is due for release today with the German and Spanish figures. In both countries, inflation should be above 1.5% and not far from the ECB's 2% target . However, the French and Italian figures are closer to 1.0%, and the underlying price pressure remains weak across the euro area, meaning the ECB is likely to stay patient, particularly in light of the stronger euro.

The euro area economic confidence figures will also be in focus. Consumer sentiment has improved on the positive employment situation and on the past year's high real wage growth. Looking ahead, the stronger euro should be a headwind to industrial confidence over time.

In the US, ADP employment is due for release ahead of the employment report on Friday. The latest ADP report showed job growth of 178,000 while the employment report had stronger growth of 209,000. That said, main focus is on the unemployment rate and particularly wage growth as these are more important for the Fed. The second GDP estimate for Q2 is also due for release but we expect no significant revisions in the figure.

Norwegian retail sales data is the highlight in Scandi markets today. Please see the Scandi section on page 2 for further details.

Selected market news

Focus on missile launch aftermath as North Korea says more to come. The UN Security Council held an emergency meeting yesterday, condemning the four recent missile launches. It demanded that Pyongyang halt its weapons programme, but held back on any threat of new sanctions. Meanwhile, President Trump said that ‘all options are on the table' for dealing with North Korea. This morning, the North Korean state news agency quoted Kim Jong-un for saying that the launch on Tuesday was to counter the annual large-scale US and South Korean military exercises, which began earlier this month. Furthermore, Kim said the test firing of a missile over Japan was a ‘meaningful prelude' to containing Guam and that he would continue to watch the US response before deciding on further action. Furthermore, the North Korean leader said that more such launches with the Pacific as target were needed.

Asian equities higher as investors shrug off geopolitical concerns. Following losses on Tuesday, particularly in Japanese equities, Asian stocks are generally higher this morning as investors do not seem alarmed by the post -missile launch reactions from the UN, the US and North Korea.

UK seeks more negotiating rounds on divorce settlement . Yesterday, the EU's chief negotiat or Michel Barnier urged to UK to start ‘negotiating seriously', as the October deadline for securing the country's exitterms from the EU looks increasingly unattainable. According to Bloomberg, with only two more negotiating rounds left , the May administ ration is now seeking to squeeze in more sessions. Sterling was weaker and UK yields lower yesterday.

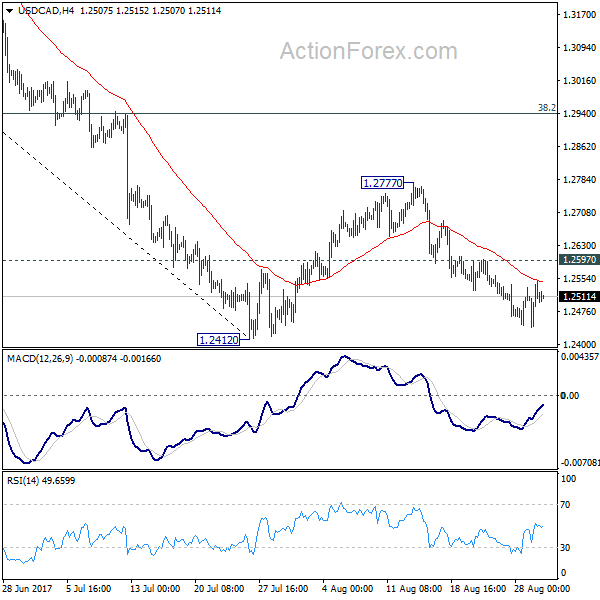

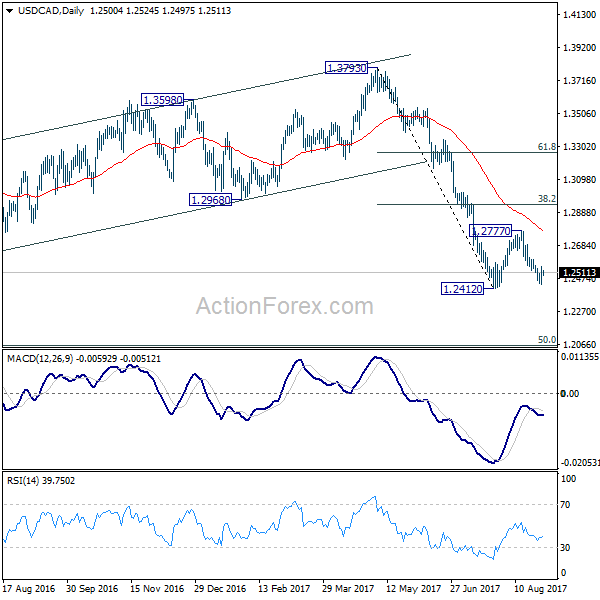

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2449; (P) 1.2500; (R1) 1.2559; More....

Intraday bias in USD/CAD stays neutral for the moment. On the downside, break of 1.2412 will resume recent fall from 1.3793 and target next long term fibonacci level at 1.2048. On the upside, above 1.2597 minor resistance will extend the consolidation from 1.2412 with another rise. But we'd expect upside to be limited by 38.2% retracement of 1.3793 to 1.2412 at 1.2940 to bring fall resumption eventually.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. Such corrective fall is still expected to extend to 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. Nonetheless, on the upside, sustained break of 1.2968, 38.2% retracement of 1.3793 to 1.2412 at 1.2940 will be the first sign of completion of the correction and will turn focus back to 1.3793 key resistance.

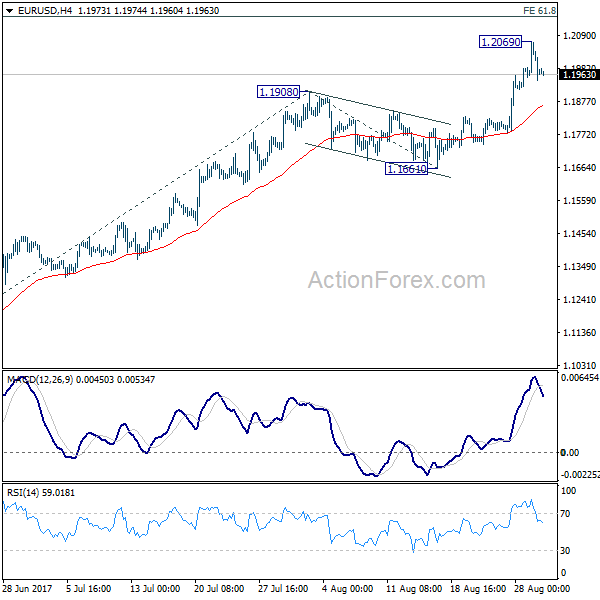

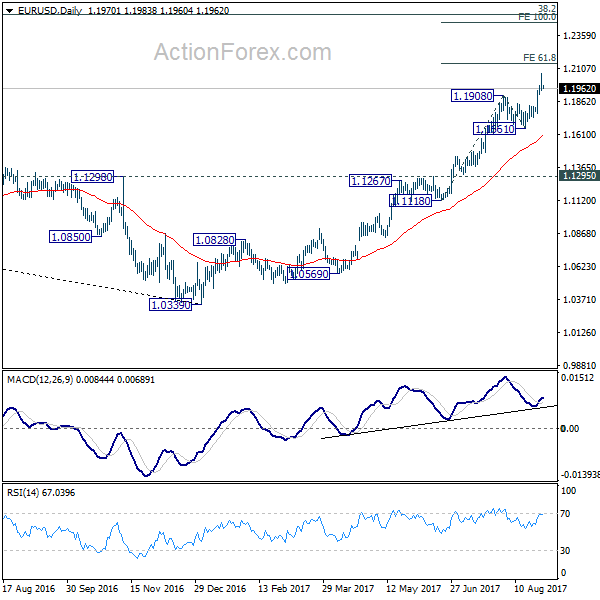

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1921; (P) 1.1996 (R1) 1.2046; More...

A temporary top is in place at 1.2069 and intraday bias is turned neutral first. Some consolidations would be seen but downside should be contained well above 1.1661 support to bring rise resumption. Above 1.2069 will extend the whole rally from 1.0339 to 61.8% projection of 1.1118 to 1.1908 from 1.1661 at 1.2149 first. Break there will target 100% projection at 1.2451 next.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained trading above 55 month EMA (now at 1.1768) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. For now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

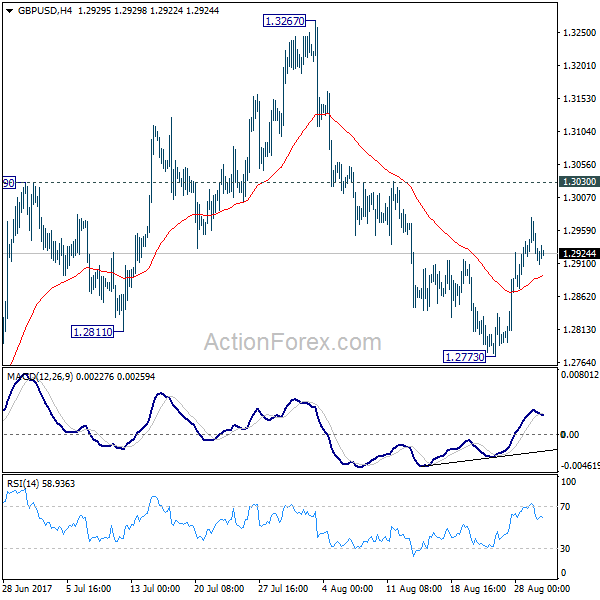

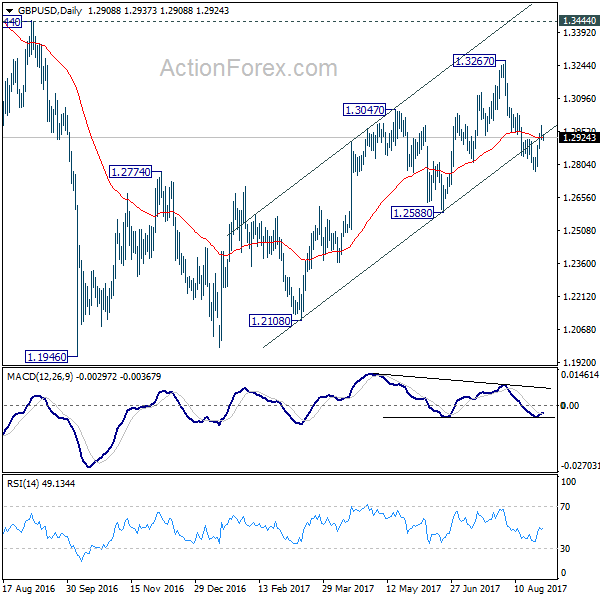

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2895; (P) 1.2937; (R1) 1.2959; More...

Intraday bias in GBP/USD remains neural for the moment as it's staying in consolidative trading in range of 1.2773/3030. We're favoring the case that correction from 1.1946 is completed at 1.3267. Below 1.2773 will target 1.2588 key near term support first. Decisive break of 1.2588 will confirm our view and target a test on 1.1946 low. Though, break of 1.3030 will dampen this bearish view and turn bias back to the upside for retesting 1.3267.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern. While further rise cannot be ruled out, larger outlook remains bearish as long as 1.3444 key resistance holds. Down trend from 1.7190 (2014 high) is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

European Open Briefing: Asia-Pacific Equity Markets Rebounded

Global Markets:

- Asian stock markets: Nikkei up 0.70 %, Shanghai Composite rose 0.02 %, Hang Seng climbed 0.92 %, ASX 200 up 0.02 %

- Commodities: Gold at $1317.33 (-0.10 %), Silver at $17.42 (+0.07 %), WTI Oil at $46.31 (-0.28 %), Brent Oil at $51.45 (-0.41 %)

- Rates: US 10-year yield at 2.14, UK 10-year yield at 1.00, German 10-year yield at 0.34

News & Data:

- AUD Building Approvals m/m -1.7 % vs -5.4 % expected

- AUD Construction Work Done q/q 9.3 % vs 0.9 % expected

- USD CB Consumer Confidence 122.9 vs 120.9 expected

- EUR GfK German Consumer Climate 10.9 vs 10.8 expected

- GBP Nationwide HPI -0.1 % vs 0.0 % expected

- EUR French GDP (QoQ) 0.5 % vs 0.5 % expected

- CAD RMPI m/m -0.6 % vs -0.2 % expected

- NZD Building Consents (MoM) -0.7 % vs -1.3% previous

- U.S. consumer confidence hits five-month high; house prices rise- RTRS

- Crude dips, gasoline spikes as floods knock out one-fifth of U.S. refineries- RTRS

Markets Update:

Asia-Pacific equity markets rebounded after selling off a day earlier following North Korea's latest missile launch. The Global investors returned to investing in risk assets as fear of further escalation receded after President Donald Trump's measured response.

USDJPY is currently seen trading around 109.90 as the dollar rose 0.1 percent against the Yen today, making the overall rise to 0.5 percent against the Yen. The pair after having spent the early hours of Wednesday under 109.60 from its late US high, started its steady march back up again as Tokyo got active.

EURUSD continued to be steady albeit not much changed in the Asian session on Wednesday. The Euro is currently trading around 1.1980 against the US Dollar after reaching highs of over 1.2060 after almost 3 years. The dollar index. DXY, which tracks the greenback against a basket of six major peers, edged up 0.1 percent to 92.317.

AUDUSD jumped 0.5 percent to 0.7996 early on Wednesday with building approvals numbers coming in better than expected and most importantly the Q2 construction work data showing a huge improvement to 9.3 % on the quarter, quite the surge from the expected 0.9 %. On the other hand, Reserve Bank of New Zealand Governor Wheeler's speech made the NZD drop from above 0.7260 to around 0.7230 very quickly and then bouncing back to around 0.7260 where the kiwi is currently seen trading

Upcoming Events:

- (EUR) German Prelim CPI m/m

- 07:00 GMT – (CHF) KOF Economic Barometer

- 07:00 GMT – (EUR) Spanish Flash CPI y/y

- 08:30 GMT – (GBP) Net Lending to Individuals m/m

- 12:15 GMT – (USD) ADP Non-Farm Employment Change

- 12:30 GMT – (CAD) Current Account

- 12:30 GMT – (USD) Prelim GDP q/q

- 13:15 GMT – (USD) FOMC Member Powell Speaks

- 14:30 GMT – (USD) Crude Oil Inventories