Sample Category Title

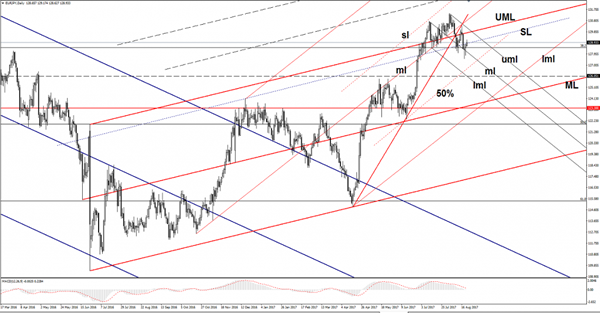

EUR/JPY Is The Retreat Completed

Price has found strong support right below the median line (ml) of the minor descending pitchfork and now has come back to retest some resistance levels. Right now is pressuring the inside sliding line (SL), could come to retest also the upper median line (UML) of the major ascending pitchfork. Actually, it could be attracted by the confluence area formed at the intersection between the UML with the upper median line (uml) of the minor descending pitchfork. The outlook is bearish as long as is trading within the descending pitchfork’s body.

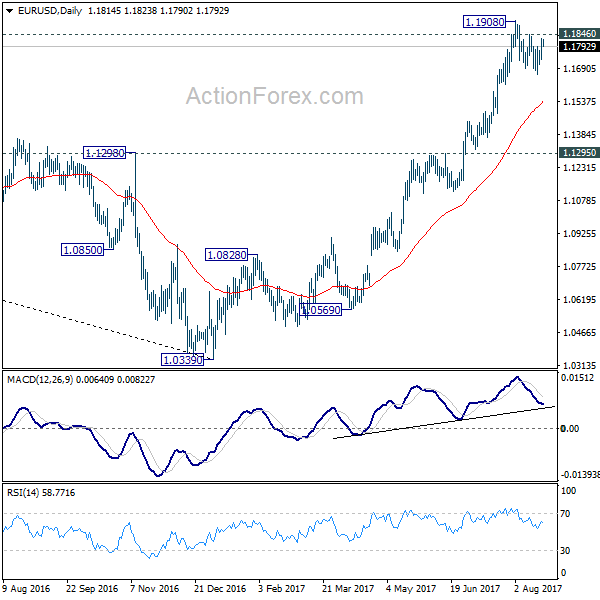

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1753; (P) 1.1790 (R1) 1.1851; More...

While EUR/USD recovered, it's limited below 1.1846 minor resistance so far. Intraday bias remains neutral as consolidation from 1.1908 might extend. In case of another fall, downside should be contained by 38.2% retracement of 1.1119 to 1.1908 at 1.1606 to bring up trend resumption. Break f 1.1846 minor resistance will argue that larger rise from 1.0339 is resuming for 1.2042 long term support turned resistance next.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained trading above 55 month EMA (now at 1.1768) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. But for now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

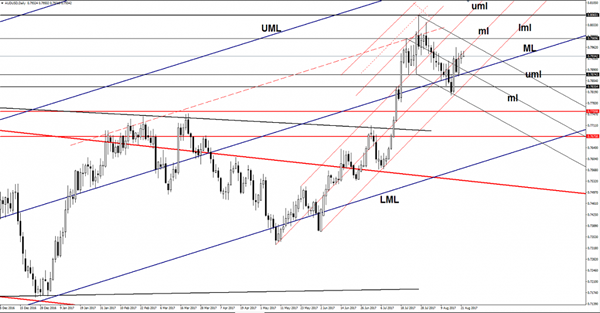

AUD/USD Seems Exhausted

Price is trading below the 0.7950 psychological level and looks a little overbought on the short term. Has retested a dynamic resistance and now could decrease if the dollar index will stay above the 92.94 previous low.

AUD/USD is still trading in the green on the short term, it maintains a bullish perspective as long as is located above a major dynamic support. Price is signaling an exhaustion and could come down to retest a support before will try to climb much higher.

Price is driven by the technical factors as we have a poor economic calendar. Technically could slip lower on the short term if will fail to close above the 0.7962 previous high. Right now is very important to see what will happen on the USDX, which is under bearish pressure on the Daily chart.

It is pressuring the median line (ml) of the minor ascending pitchfork, a failure to close above stabilize above will send the rate tumbling on the short term. The rebound towards the median line (ml) was expected after the failure to retest the lower median line (lml), but the false breakout above it shows an overbought.

Could come down to retest the median line (ML) of the major ascending pitchfork and the lower median line (lml). The perspective will remain bullish as long as is trading above these levels, but a valid breakdown will confirm a major drop.

EUR/USD Stays in Consolidation as Markets Lack Direction

The forex markets are lacking clear direction so far this week. It feels there is a lack of interest among traders ahead of Jackson Hole symposium. Euro attempted to resume recent rally against Dollar. While EUR/USD takes out a near term channel resistance, it's staying below 1.1846 resistance. Thus, the consolidation from 1.1908 is likely still in progress. GBP/USD and USD/JPY are also staying in very tight range. Canadian dollar strengthens with very weak momentum but USD/CAD is still in progress for deeper decline. The economic calendar is relatively light today but Canadian retail sales could trigger firmer momentum in USD/CAD.

Trump revealed Afghanistan strategy, Mnuchin urge to raise debt ceiling

US President Donald Trump revealed his Afghanistan strategy and said "a core pillar of our new strategy is a shift from a time-based approach to one based on conditions." But there are criticisms that Trump's new strategy was essentially the same as his predecessors, which failed to get the US our of that war. At the same time Treasury Secretary Mnuchin indicated that the Congress has to lift the ceiling by the end of September in a "clean" debt-ceiling increase. This was echoed by Senate Majority Leader Mitch McConnell who noted that there is a "zero chance" the US government fails to raise the ceiling. Mnuchin has been urging to lift the debt ceiling before leaving Washington for the August recess. Indeed, the Treasury has been using "extraordinary measures" since this spring to avoid breaching the debt ceiling but the trick cannot be used indefinitely due to weaker tax collection.

Japan businesses not keen on additional BoJ easing

According to a survey of 548 firms conducted for Reuters Nikkei Research, businesses in Japan were not too optimistic that BoJ could hit the 2% inflation target. Yet, they are not keen on having additional easing from the central bank. The results showed that 31% of respondents believed it's "impossible" for BoJ to achieve the inflation target. 37% believed that BoJ could hit it after three years. 46% said that BoJ's future policy direction should be standing pat. 40% said BoJ should seek exit from monetary easing. And only 14% believed that BoJ should adopt further monetary easing. Inflation expectation was also quite clear with 75% said they don't play to raise prices of their main goods and services.

ECB to hit 33% bond purchase ceiling soon

A report by Financial Times revealed that the ECB is about to break its self-imposed limit of owning 33% of a country's government debt, leading the central bank to taper no matter how well (or bad) inflation goes. It is projected that the limits for German, Portuguese and Irish debts could be breached as early as in February. At the same time, it's believed to be unlikely for ECB to raise the ceiling considering continuous legal challenges from Germany. President Mario Draghi's speech at the Jackson Hole symposium this Thursday is closely awaited. He would likely discuss about the Eurozone's economic outlook and hinted about the central bank's policy stance.

On the data front

Swiss trade surplus widened to CHF 3.51b in July. German ZEW economic sentiment is the main feature in European session. UK will release public sector net borrowing. Canada retail sales will be a major focus in US session. US will release house price index.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1753; (P) 1.1790 (R1) 1.1851; More...

While EUR/USD recovered, it's limited below 1.1846 minor resistance so far. Intraday bias remains neutral as consolidation from 1.1908 might extend. In case of another fall, downside should be contained by 38.2% retracement of 1.1119 to 1.1908 at 1.1606 to bring up trend resumption. Break f 1.1846 minor resistance will argue that larger rise from 1.0339 is resuming for 1.2042 long term support turned resistance next.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained trading above 55 month EMA (now at 1.1768) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. But for now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 06:00 | CHF | Trade Balance (CHF) Jul | 2.88B | 2.81B | ||

| 08:30 | GBP | Public Sector Net Borrowing (GBP) Jul | 0.3B | 6.3B | ||

| 09:00 | EUR | German ZEW (Economic Sentiment) Aug | 15 | 17.5 | ||

| 09:00 | EUR | German ZEW (Current Situation) Aug | 85.5 | 86.4 | ||

| 09:00 | EUR | Eurozone ZEW (Economic Sentiment) Aug | 34.2 | 35.6 | ||

| 10:00 | GBP | CBI Trends Total Orders Aug | 10 | 10 | ||

| 12:30 | CAD | Retail Sales M/M Jun | 0.30% | 0.60% | ||

| 12:30 | CAD | Retail Sales Less Autos M/M Jun | 0.30% | -0.10% | ||

| 13:00 | USD | House Price Index M/M Jun | 0.50% | 0.40% |

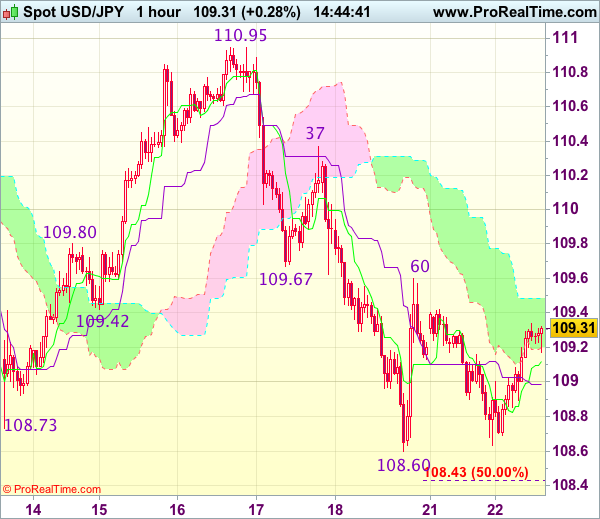

Trade Idea : USD/JPY – Stand aside

USD/JPY - 109.33

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 109.12

Kijun-Sen level : 108.99

Ichimoku cloud top : 109.49

Ichimoku cloud bottom : 109.20

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite yesterday’s all to 108.63, the subsequent rebound after holding above indicated support at 108.60 has retained our view that further consolidation would take place and another test of resistance at 109.60-67 cannot be ruled out, however, a firm break above there is needed to signal low has been formed at 108.60, bring a stronger rebound to 110.00 and later towards resistance at 110.37 which is likely to hold from here.

On the downside, below 108.80 would bring retest of 108.60 but only break there would signal recent decline has resumed and may extend further weakness to 108.30 (1.618 times projection of 110.95-109.67 measuring from 110.37), then towards 108.10-15 (61.8% projection of 110.95-108.60 measuring from 109.60), however, loss of downward momentum should prevent sharp fall below latter level and reckon 108.00 would hold from here, bring rebound later. As near term outlook is mixed, would be prudent to stand aside for now, then look to sell dollar on subsequent rebound.

Currencies: Dollar Holding Within Reach Of Recent Lows

Sunrise Market Commentary

- Rates: Positive bias core bonds ahead of Yellen/Draghi

We forecast trading to remain sentiment-driven ahead of speeches by ECB Draghi (tomorrow and Friday after close) and Yellen (Friday). Current market sentiment underpins core bonds as subdued inflation readings dealt a blow to tightening expectations while turmoil in Washington sparked some volatility on Wall Street. - Currencies: dollar holding within reach of recent lows

The dollar continues to trade soft, but nearby technical support levels are left intact as investors await CB speeches at the Jackson hole Fed symposium. Today's data won't change the global dollar picture. EUR/GBP extends its impressive rebound as investors look forward to the next round of Brexit negotiations

The Sunrise Headlines

- US equities ended little changed with energy (lower oil prices) and financials lagging and real estate outperforming. Asian equities started the day on a stronger footing (good corporate results) and US equity futures show gains too.

- Britain will be subject to the rulings of European courts after Brexit, the government has conceded, in an apparent climb-down from its promise of judicial independence, said the Guardian.

- President Trump made an open-ended commitment to Afghanistan that'll add as many as 4,000 more US troops into the country and keep American forces there as long as it takes to ensure a stable and enduring peace.

- Oil prices dropped sharply yesterday to €51.66/barrel, reversing Friday's gains. OPEC's Vienna meeting ended quietly without decision on the future of supply cuts. The cartel will discuss whether to extend or end the deal in November.

- The Hungarian central bank meets, but consensus unanimously expect an unchanged decision (base rate of 0.9%). The forint performed well recently and approaches the EUR/HUF 300 threshold (now 303.29).

- Today's calendar remains light with the August German ZEW economic sentiment and the US Richmond Fed manufacturing surveys. In the UK, public finances (July) and the CBI trends report are up for release. ECB Constancio speaks.

Currencies: Dollar Holding Within Reach Of Recent Lows

Dollar holding near the recent lows

EUR/USD held within reach of the early August top in recent weeks, but no new test occurred. This indecisive pattern continued yesterday. The dollar traded with a slightly negative intraday bias, partially due to a negative risk sentiment. EUR/USD drifted back north of 1.18 and closed the session at 1.1815. Investors awaited speeches of Fed's Yellen and ECB's Draghi at the Jackson Hole Fed symposium on Friday. USD/JPY drifted temporary below 109, but rebounded to the 109 area as risk sentiment improved later in US dealing.

Overnight, Asian equities show moderate gains, but volumes are low as there is no high profile (economic) news. The yen eases slightly. USD/JPY tries to find a bottom after a protracted decline throughout August. EUR/USD hovers near 1.18.

In EMU, the German August ZEW economic sentiment is expected to decline slightly. The current situation sub-index peaked in June (88). The expectations' component hovered sideways of late . A strong decline of the expectations would signal that the economy is rolling over, which we don't expect. The August Richmond Fed manufacturing index is expected to have declined to 10 from 14. Other recent surveys suggested that manufacturing is doing well. With a weaker dollar and signs of better domestic demand, we count on a stabilization of the Richmond Fed. The index is volatile and sharply surprised on the upside in July. The impact on USD trading should be limited. At the margin, the data might be slightly USD supportive, or at least slow the USD decline. The global equity performance remains a wildcard for USD trading. An easing of recent equity softness might be marginally USD supportive. Focus remains on the speeches of Yellen and Draghi later this week.

Broader context and technical picture. Late June, EUR/USD started a new upleg as investors anticipated a reduction of ECB bond buying to be announced in autumn. The Fed was expected to remove policy stimulation only in a very gradual way as US inflation remained soft. Uncertainty on the policy of the Trump administration was an secondary negative factor for the dollar. EUR/USD set a new correction top north of 1.19 before consolidating in a narrow 1.1662/1.1910 trading range. We expect this range will hold going into the Jackson Hole symposium. If US data remain ok (as most were this month) and if Draghi gives little information on next ECB steps, there might be room for a modest USD comeback. A return of EUR/USD to the 1.15/16 area is possible. Pockets of US political risk are a (negative) wildcard for the dollar.

A downward correction in core (US and European) yields supported the yen in August. USD/JPY declined from the mid 114 area mid-July to 108.60 last Friday. The April correction low (108.13) remains the key line in the sand. For now, this level won't be easy to break as quite some USD bad news is discounted after the recent protracted setback. A cautious buy-on-dips approach (with stop-loss protection below 108) may be considered

EUR/USD correction top stays within reach

EUR/GBP

EUR/GBP extends protracted uptrend

Yesterday, the gradual, but protracted EUR/GBP uptrend continued. Investors awaited new info on the Brexit negotiations going into a next round of formal talks next week. There were no UK eco data. In technical trading, EUR/GBP closed the session at 0.9162. Cable held an extremely tight sideways range in the upper half of 1.28/low 1.29. USD softness helped sterling.

Today, the UK monthly public finance data and the CBI trends orders data will be published. The data are usually only of second tier importance for sterling trading. The CBI orders are expected marginally softer at 8 from 10. Recent UK eco data were not too bad even as higher inflation is eroding Britons capacity to spend. The difficult Brexit talks remain a negative sterling factor MT. However, the recent rise of EUR/GBP has gone quite far and the pair is moving into overbought territory. So, we look for a correction, for whatever reason (correction in EUR/USD, decent UK eco data, improving global risk sentiment…).

From a technical point of view, EUR/GBP cleared the 0.8854/80 resistance (top end June), opening the way for further gains The move was the result of euro strength (ongoing strong EMU growth and expectations of the ECB reducing policy stimulation later this year). At the same time, UK price data remain soft enough for the BoE to keep a wait-and-see modus as the Brexit negotiations continue. MT, we maintain a buy EUR/GBP on dips approach as we expect the constellation of relative euro strength and sterling softness to continue. The 0.9415 flash-crash spike is the next MT target on the charts. However, we don't jump on the trend anymore after recent protracted EUR/GBP rally and wait for a correction, e.g to the technical support in the 0.88/89 area.

EUR/GBP: consolidation near recent top

Market Update – Asian Session: Markets Shrug Of Latest N. Korea Threat

Asia Summary

Asian equity markets opened mixed, trade was quiet with the Hang Seng being the stand out. It was again a quiet economic data day, giving little direction to the currencies, though a stronger dollar trend has emerged as the session entered its second half. The offshore yuan is poised for the highest close since September (5th day of gains), boosted by a stronger central bank reference rate after a dollar weakness overnight. According to an un-named senior PBOC adviser, the yuan advance may continue this year. Markets continue to shrug off North Korea threats, KCNA said that the US will face revenge for ignoring North Korea warning.

Key economic data

(AU) Australia ANZ Roy Morgan Weekly Consumer Confidence Index: 109.2 v 111.7 prior

Speakers and Press

China/Hong Kong

(CN) China should shift more financial resources to high-tech and emerging industries and away from loss-making or highly leveraged ‘zombie’ firms – People’s Daily Commentary

Korea

(KR) North Korea KCNA reiterates South Korea and US drill heighten tensions; US will face revenge for ignoring North Korea warning

(KR) South Korea Fin Min Kim: Govt debt to be managed at lower than KRW700T; Hard to increase Govt spending by 7%/yr

Japan

(JP) Japan to seek ¥5.25T defense budget for FY18 - Japanese Press

Australia

(AU) Analysts comment that China restrictions on overseas property development will hurt Australia's land sales and residential property development - AFR

(AU) S&P: Australia And New Zealand ABS Performed Well In Q2 2017

Other

(PH) Philippines Finance Chief Dominguez: Rate of change in dollar/Peso (PHP) is of 'concern', but we are 'not uncomfortable' with it

(US) US House Majority Leader Ryan: Reiterates committed to tax overhaul in 2017

(US) President Trump: Announces will make drastic changes to strategy in Afghanistan as he believed withdrawing troops from the country would have unacceptable effects on the region; "wont say when we will attack but attack we will "

Asian Equity Indices/Futures (00:00ET)

Nikkei 0.0%, Hang Seng +1.1%, Shanghai Composite +0.1%, ASX200 +0.3%, Kospi +0.4%

Equity Futures: S&P500 +0.2%; Nasdaq100 +0.4%, Dax +0.1%, FTSE100 +0.2%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1824-1.1803; JPY 109.33-108.89; AUD 0.7951-0.7932; NZD 0.7335-0.7318

Dec Gold -0.2% at $1,294/oz; Oct Crude Oil +0.4% at $47.73/brl; Sept Copper +0.2% at $2.98/lb

(CN) China PBOC OMO injects CNY60B v CNY180B in 7 and 14-day reverse reports prior: net drains CNY10B v drains CNY50B prior

USD/CNY (CN) PBOC SETS YUAN REFERENCE RATE AT 6.6597 V 6.6709 PRIOR

(TH) Thailand sells combined THB60B in 3-month and 6-month bonds

(JP) Japan MoF sells ¥813.3B v ¥1.0T indicated in 0.60% (0.60% prior) 20-yr JGBS; avg yield 0.5500%; bid-to-cover 4.51x (strongest demand since Jan 2014)

Equities notable movers

Hong Kong/China

207.HK COFCO Property Group to acquire stake in Joy City; +19%

Australia/New Zealand

BHP.AU Reports FY17 underlying Net $6.73B v $7.3Be; Rev $38.3B v $38.3Be; to exit US onshore assets; Announces US and Euro bond buyback plan, subject to a $2.5B cap; +1.3%

ACX.AU Reports FY17 Net loss A$9.97M v profit A$5.7M y/y; Rev A$161.2M v A$123.4M y/y; -10%

CVT.NZ Reports FY17 (NZ$) NPAT 9.8M v 18.1M y/y, EBITDA 19.8M v 37.0M y/y, Rev 156M v 192M y/y; +11%

Taiwan

2498.TW Cuts price of Vive VR headset by $200 to $599; +8.8%

Trump Can Get Focus Back On The Policy Agenda

Market movers today

German ZEW expectations are due out today and we look for a slight further decline. Sentiment has been a bit in retreat recently (albeit from high levels) and we expect the stronger euro to put a further dent on ZEW expectations.

In the US, FHFA house prices are expected to show an unchanged rate of around 0.5% m/m corresponding to a 6% annualised rate. Rising housing wealth is one of the factors supporting US consumers on top of robust job growth and a rebound in real wage growth due to lower inflation.

Otherwise, focus continues to be on Jackson Hole later this week and whether Trump can get focus back on the policy agenda and his apparent new push for tax reform, which was reported by several media out lets yesterday.

Selected market news

According to a Fed survey published yesterday, US workers have low hopes for higher paychecks. When asked what the lowest annual salary was that they would accept in a new job the respondents replied USD57,960 on average in July down form USD59,660 four months earlier. When asked what salary they would expect in job offers over the next four months, the respondents on average replied USD50,790 , down from USD54,590 four months earlier.

In our view, the tightness of the US labour market is not the only factor determining wage growth, as second-round effects following many years of low inflation have hit wage growth. When employees expect inflation to remain low, they can live with low wage growth, as real wage growth may still be solid, making it less likely that inflation will reach the target (see Flash Comment US: Fed likely to continue tightening on strong jobs report, 7 August 2017).

With Steve Bannon leaving his role as Donald Trumps' Chief Strategist last week, focus is turning to whether this will pave the way for pushing forward a policy agenda that could gain support from Republicans. According to the Financial Times, the new Chief of Staff, John Kelly, is leading efforts to restore order to the White House and the tax cut agenda has been chosen as the best candidate to score a legislative gain and repair relations with the business community.

UK Prime Minister Theresa May's government is due to publish more details of UK's Brexit plans today with focus on civil judicial cooperation ahead of a document on the role of the EU Court of Justice on Wednesday.

Cable Retains Bearishness Ahead Of Jackson Hole

Key Points:

- Cable retains a bearish directional bias.

- Price action remains trapped below 50 and 100 Day EMA’s.

- Pair likely to remain under pressure in the week ahead.

The Cable continued to move lower last week as the pair was caught on the wrong side of the wave of sentiment swinging towards the greenback. Subsequently, early in the week saw a relatively rapid fall for the Cable, as the pair was dealt a blow from a -0.1% UK CPI result, and this commenced a slide which saw it close the week around 130 pips lower at 1.2870. Subsequently, there is plenty of evidence that the Cable could be in for a further fall ahead in the coming week.

The Cable never really had a chance to pick itself up last week and trading started off with some sharp declines following a stark miss in the UK CPI results. The key metric was forecast to come in flat at 0% but instead slipped to -0.1% m/m which kicked off some sharp selling. This was compounded when the U.S. Retail Sales data climbed strongly to 0.6% which set off a sentiment swing which the pair never recovered from. In addition, the U.S. Initial Jobless Claims, and U.S. Philly Fed Business Outlook Index also proved relatively robust at 232k, and 18.9, respectively. Subsequently, the Cable fell around 130 pips, over the course of the week, to close trading out at 1.2870.

Looking ahead, the pending week should be relatively interesting for the Cable given the large slew of economic data due for release. In particular, the UK GDP numbers are likely to be closely watched by the market given their relative importance and forecast of 0.3% q/q. The much awaited U.S. Core Durable Goods Order figures are also due to print and, given the recent U.S. economic strength, could provide a surprise to the upside. Finally, we could see plenty of volatility as the Jackson Hole Summit fires up late in the week and many of the major actors in fiscal and monetary policy get together to mull over the economy. Typically, there is always some interesting comments emanating from the forum which means it is often worthwhile monitoring.

From a technical perspective, the Cable’s recent decline from 1.3267 appears to have extended over the past week. Price action remains below the critical 100 Day MA whilst the RSI Oscillator is presently within neutral territory. Subsequently, our initial bias remains on the downside for the week ahead with a further breakdown highly likely. Support is currently in place for the pair at 1.2862, 1.2810, and 1.2774. Resistance exists on the upside at 1.2918, 1.3029, and 1.3267, and 1.3480.

Ultimately, the Cable is likely to have a relatively rough week ahead as long as price action remains trapped under the 50 and 100 Day MA. At this stage, an upside breakout looks unlikely unless both the fundamental and technical trends change in the week ahead. Regardless, keep a watch on the key 1.30 handle because if a breakout does occur this could be the critical inflection point.

Daily Technical Analysis: EUR/USD First Signs Of Bullish Break Above 1.18 Bull Flag

Currency pair EUR/USD

The EUR/USD is breaking above resistance trend lines (dotted reds) of a bull flag continuation chart pattern of a wave 4 (green) correction. This bullish break above resistance (red) could confirm the end of wave 4 and start of wave 5.

The EUR/USD seems to be building a 5 wave extension within wave 3 (purple). The wave 4 (brown) pullback should not retrace deeper than the 50% at 1.1780 otherwise the wave 4 is invalidated. A break above the bull flag chart pattern confirms the continuation of the wave 3 (purple) towards the Fib targets of wave 3 vs 1.

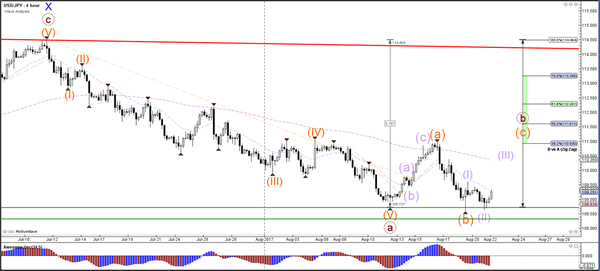

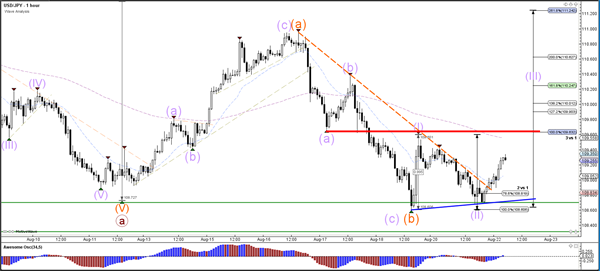

Currency pair USD/JPY

The USD/JPY has bounced again at the key support zone (green lines). The bullish bounce could see price expand a wave B (brown) correction via an ABC (orange) flat.

The USD/JPY broke above the resistance trend line (dotted orange) of the downtrend and is now showing a potential bounce. A bullish break above resistance (red) would confirm the potential wave 3 (purple) whereas a bearish break below support (green) would invalidate it.

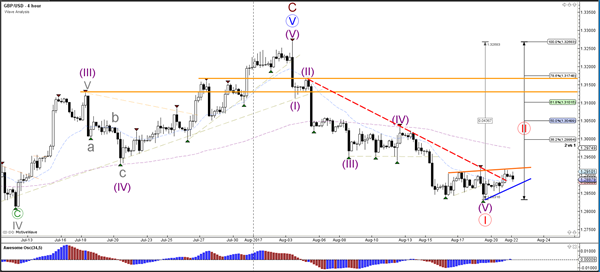

Currency pair GBP/USD

The GBP/USD could have completed a 5th wave (purple) within wave 1 (red). A bullish bounce at the support trend line (blue) could see price move higher towards the Fibonacci retracement levels of wave 2 (red).

A GBP/USD seems to be building a large correction via WXY (purple).