Sample Category Title

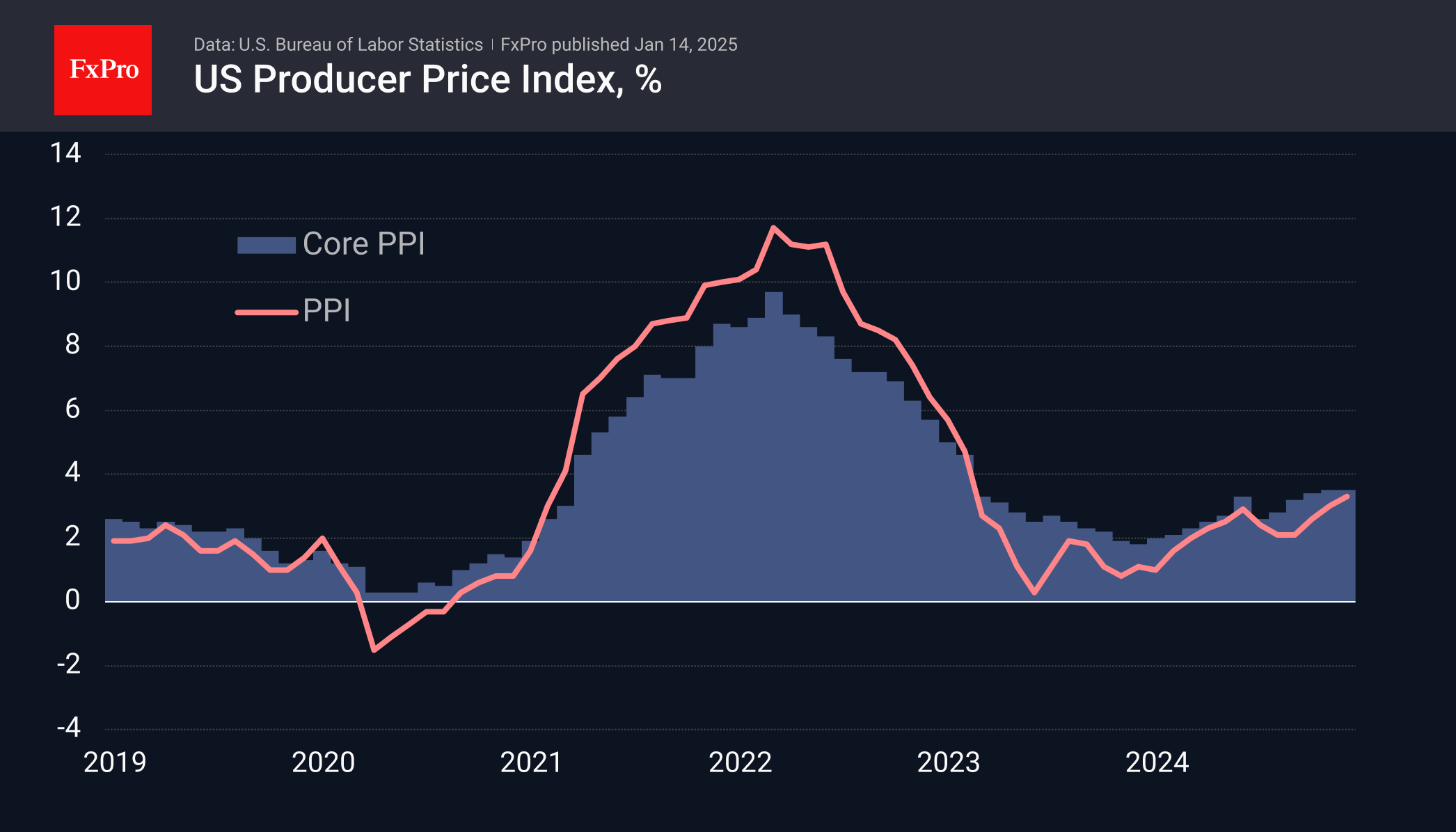

December PPI Eases Fears of Hawkish Fed

US producer prices rose at a slower-than-expected pace in December, easing fears of tighter monetary policy.

The PPI rose 0.2% in December, down from 0.4% in the previous month. And while price growth accelerated to 3.3% from 3.0% a year earlier, this was below the average forecast of 3.5%. Core PPI, which excludes volatile food and energy, was virtually unchanged over the month and maintained its year-over-year growth rate at 3.5% against the expected acceleration to 3.8%.

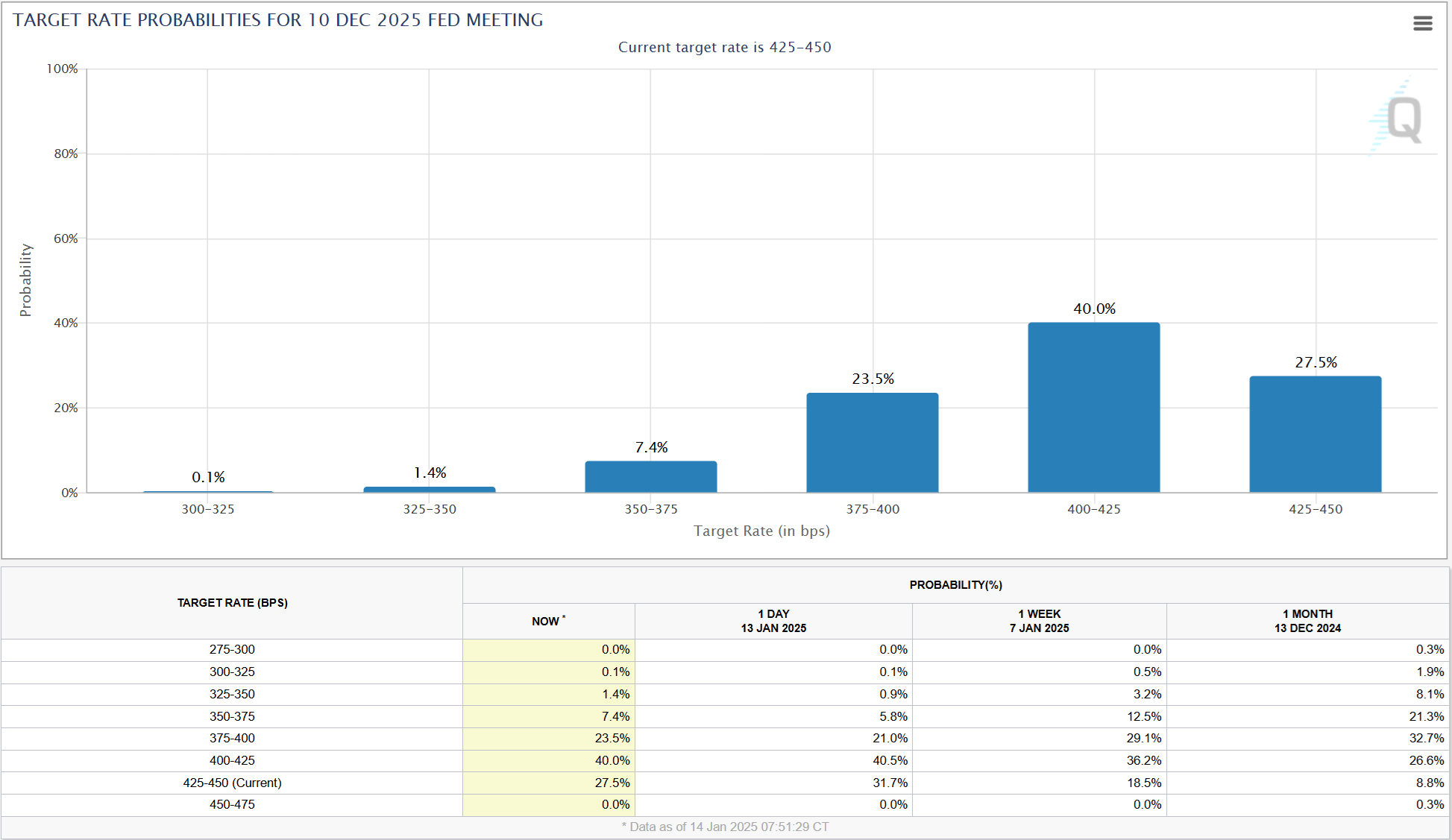

This is positive news for markets, where expectations of a more hawkish Fed in 2025 have gained momentum in recent weeks. The local high was reached on Monday morning when markets were pricing in a 32% probability of no change in the Fed Funds rate by the end of the year. The latest data shows that this estimate has fallen to 27.5%.

The softer report fuels tentative hopes that we may be seeing the start of a turnaround. This would be especially true if such a shift is confirmed in Wednesday’s consumer inflation report. Typically, these two publications miss expectations by about the same amount. However, the CPI has much greater potential to influence market prices, and it would be too presumptuous to rule out surprises altogether.

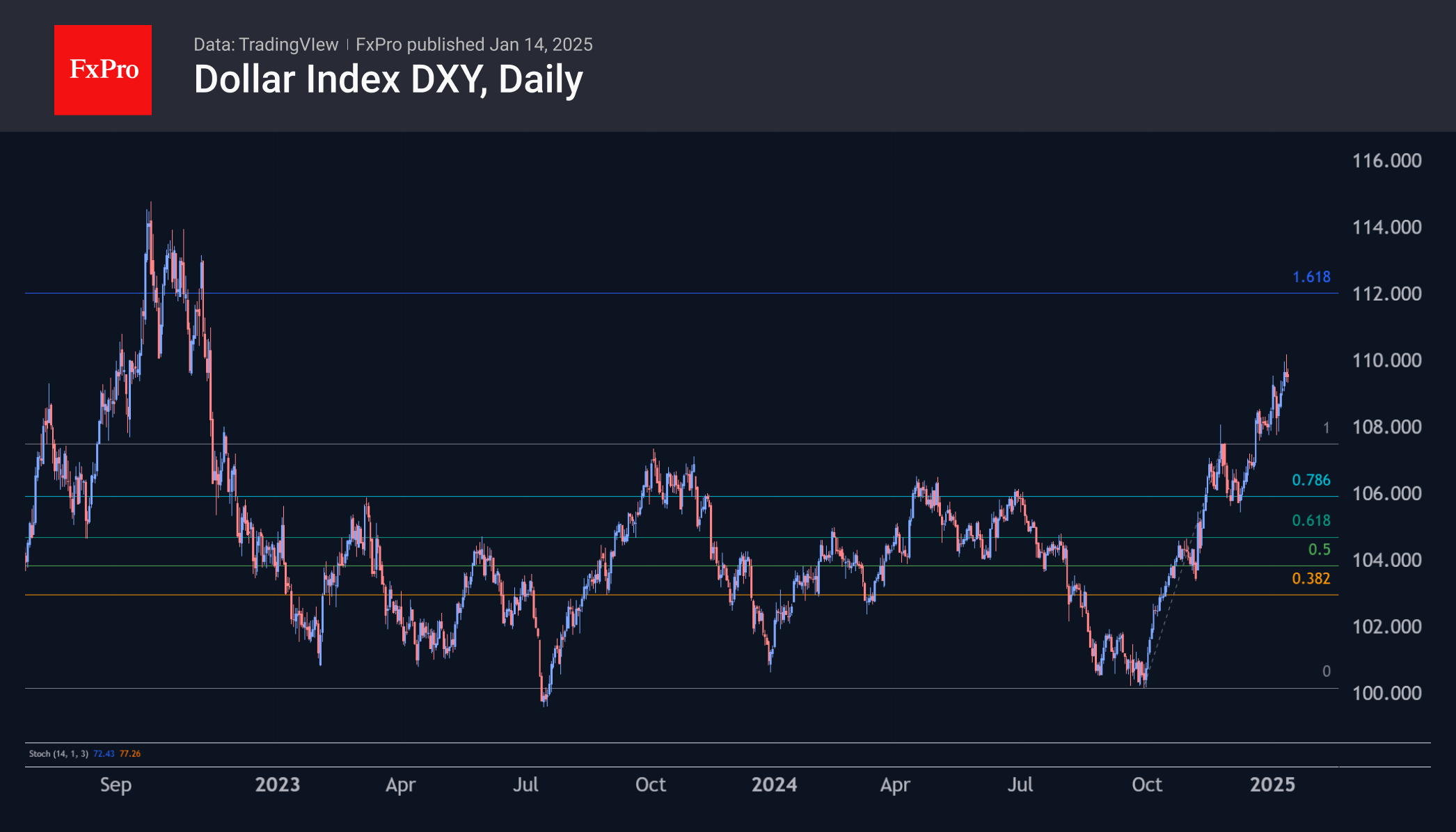

The Dollar Index fell 0.2% on release but quickly recovered its initial losses. In this case, the logic is clear: the dollar’s main competitors will have to ease policy by 50-100 points in the face of a significant cooling of the economy. This is the main factor in the tug-of-war over whether we will see 25 or 50 points of Fed easing within a year.

If confirmed on Wednesday, soft inflation could trigger profit-taking by dollar bulls, who took the DXY to 110 the previous afternoon. That said, a reversal for the dollar seems unlikely in the near future. It is more likely that the medium-term consolidation of positions will be followed by a new growth impulse towards the 112-113 area.

BoJ to Discuss Rate Hike, Yen Dips Lower

The yen remains calm and is lower on Tuesday. In the North American session, USD/JPY is trading at 157.98, up 0.34% on the day.

US inflation expected to rise

There are no tier-1 events out of Japan this week and the yen is having a relatively quiet week. That could change with the release of US inflation on Wednesday. Headline CPI is expected to rise to 2.9% y/y in December from 2.7% in November, while core CPI is expected to remain at 3.3% y/y for a third straight month. Inflation reports have had significant impact on rate expectations but the December inflation rate might not be all that significant, as expectations of a rate cut have fallen in recent weeks.

Since the December meeting, the Fed has tried to dampen rate-cut expectations and the market is not expecting a rate cut in the first quarter of 2025. The money markets have currently priced in a quarter-point cut at the Jan. 29 meeting at below 3% and at the March meeting at around 20%. With inflation largely under control and a solid labor market, there is little reason for the Fed to cut rates in the near term.

BoJ’s Himino: BoJ will discuss rate hike at Jan. 24 meeting

The Bank of Japan tends not to telegraph its rate plans, leaving investors in the dark and on the hunt for clues about the central bank’s rate plans. The uncertainty adds to the drama ahead of BoJ meetings and means that each meeting should be treated as a market-mover.

BoJ’s Deputy Governor Ryozo Himino said on Tuesday that the BoJ would discuss a rate hike at the Jan. 24 meeting. Himino didn’t say what decision he expected the BoJ to make but reiterated Governor’s Ueda recent comments that wage growth was solid and that there was a lot of uncertainty surrounding Donald Trump’s trade policies.

USD/JPY Technical

- USD/JPY tested resistance at 158.13 earlier. Above, there is resistance at 158.49

- There is support at 157.78 and 157.42

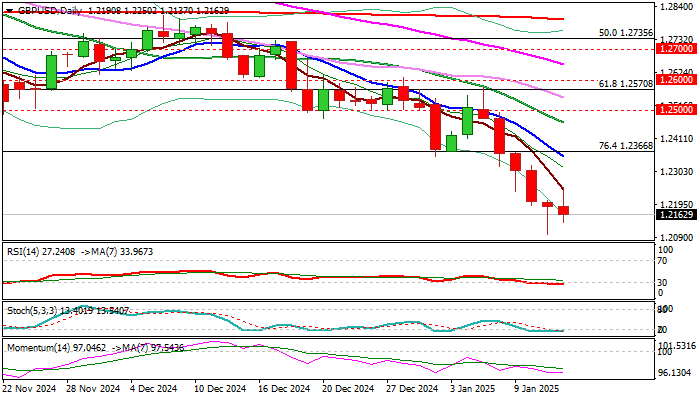

GBP/USD: Holds Near New Multi-Month Low, UK and US CPI Reports in Focus

Cable came under fresh pressure on Tuesday and looks for retest of new multi-month low (1.2099) after recovery from Monday’s strong downside rejection failed repeatedly at 1.2250 zone.

Bears regained control after a mild correction, with loss of 1.2099 low (also monthly cloud base) to open way for test of 1.2037/00 targets (4 Oct 2023 low / psychological).

Daily studies remain in full bearish setup, though oversold conditions may keep near term action on hold for some time.

Upticks are likely to be limited and ideally capped under 1.2350/60 zone falling 10DMA / broken Fibo 76.4% support) as fundamentals are dollar positive.

US Dec PPI missed expectations but came above previous month’s figure (y/y), which signals that inflation remains elevated and to further soften Fed’s rate cut outlook for 2025.

Markets focus on UK and US December inflation reports (due on Wednesday) which would further pressure pound, as price pressure is expected to rise, and UK economy remains on fragile legs.

The dollar would benefit more from the anticipated implementation of tariffs, proposed by Trump’s administration, even on the latest comments that tariff implementation might be gradual at the beginning.

Res: 1.2250; 1.2299; 1.2360; 1.2400.

Sup: 1.2099; 1.2069; 1.2037; 1.2000.

Sunset Market Commentary

Markets

Yesterday’s Bloomberg story brought some relief to markets. The news company citing people familiar reported that president-elect Trump’s team is working on a phased introduction of import tariffs. Raising levies 2%-5% each month instead of everything all at once reduces its shock effect both on US inflation and exporting areas, including the EU. The article shouldn’t be taken by face value though. A previous report by the Washington Post about a targeted tariff approach on a product level was quickly rebuffed by the present-to-be. Lacking such denial for the time being, however, and helped somewhat by lower-than-expected US PPIs, that eased the upward pressure on (US) bond yields, Euro area stocks rise about 1%, Wall Street between 0.4-0.9%. Producer prices were flat to +0.2% higher in December, depending on the gauge. This compared to a consensus estimate varying between +0.3-0.4%. With tomorrow’s more important consumer price inflation on the agenda, it triggered a kneejerk reaction lower in short-term US bond yields. Net daily changes vary between -1.4 (2-yr) to +1.4 bps (30-yr). European yields overcame morning weakness to trade slightly higher in a bear steepener. Long-end underperformance remains the name of the game since the short end is more or less locked in. A reasonable 100 bps of additional ECB easing is discounted. Swap yields add up to 5 bps. Maturities from 10-yr on hit new multi-month highs. The beginning-of-the-year bond market taps continue to be in high demand. A dual tranche European offering consisting of a new €6bn 3-yr benchmark and a €5bn Oct2054 tap attracted a combined €170bn. Books for Greece’s €4bn 10-yr syndicated sale ran above $40bn. Oil prices fluctuated near their 5-month highs (Brent +$80 per barrel) amid cease fire talks between Israel and Hamas reported to be in their final stages. Currency markets trade mixed with sterling the noticeable underperformer. Chancellor Reeves sought to reassure markets by repeating a pledge to stick by her own fiscal rules “at all times”. GBP investors send the currency nevertheless lower against the euro (EUR/GBP >0.84) and the dollar (GBP/USD 1.215, on track for its lowest close since October 2023). EUR/USD trades around the recent lows of 1.025.

News & Views

Inflation in Hungary accelerated more than expected in December, surpassing the upper limit of its 3.0% +/- 1.0% MNB tolerance band. Price rose 0.5% M/M and 4.6% Y/Y, up from 3.7% in November. The rise was mainly due to higher prices for food (0.4% M/M), gas and electricity (1.7% M/M) and durable goods (0.6% M/M). Services prices stay elevated at 0.4% M/M and 6.8% Y/Y. The National Bank of Hungary’s core inflation measures all rose on a Y/Y year basis compared to November to between 4.7% and 5.4%. The NMB in its December inflation update indicated that inflation could rise to 4.6% Y/Y in January. With this level already reached in December, the risk is the hoped-for 2025 disinflation process will start from a higher level. The MNB in December also raised its 2025 inflation estimate to 3.3%-4.1% before returning sustainably to 3.0% in 2026. The MNB since end-September kept the policy rate unchanged at 6.50%. Current inflation data and the still-weak forint suggests that there is no room to restart easing anytime soon. The 2-y swap adds 5.0 bps (6.67%) and the 10-y also moves further north (+6.0 bps at 7.16%). The forint gains modestly from the EUR/HUF 413 area to currently 411.9, but this is rather due to global sentiment.

The National Federation of Independent Business (NFIB) sentiment indicator among small US business improved further in December. The index rose 3.4 points to 105.1 after already having jumped at the fastest pace on record in November. It’s the highest reading since October 2018. “Optimism on Main Street continues to grow with the improved economic outlook following the election,” NFIB Chief Economist Bill Dunkelberg was quoted. “Small business owners feel more certain and hopeful about the economic agenda of the new administration. Expectations for economic growth, lower inflation, and positive business conditions have increased in anticipation of pro-business policies and legislation in the new year.” Of the 10 index components, seven increased. The uncertainty index declined substantially for the second consecutive month. Amongst others, the net percent of owners expecting the economy to improve rose 16 points to a net 52%, the highest since Q4 of 1983. Both the percentage of owners expecting higher real sales to rise and believing it is a good time to expand business rose to the highest level since early 2020. 20% reports inflation is their single most import problem, unchanged from November.

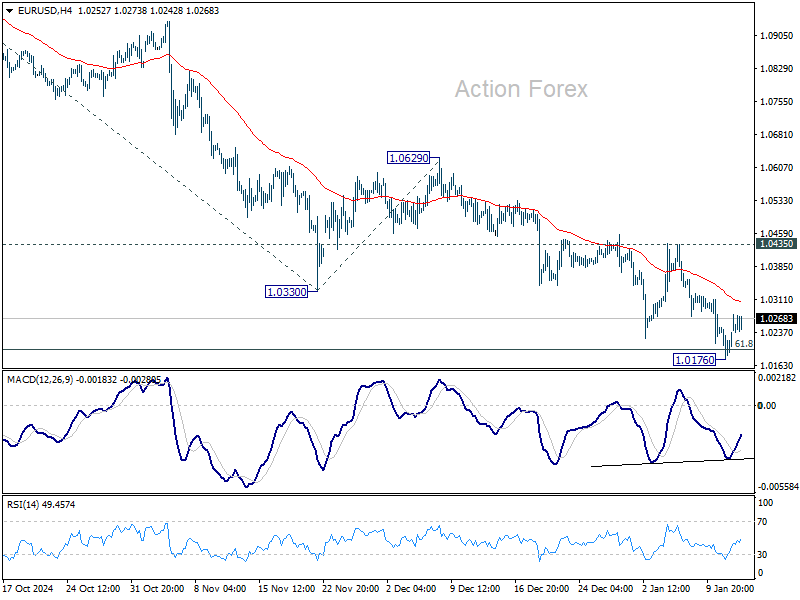

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0198; (P) 1.0224; (R1) 1.0270; More...

EUR/USD is staying in consolidations above 1.0176 temporary low and intraday bias stays neutral for now. While stronger recovery cannot be ruled out, outlook will stay bearish as long as 1.0435 resistance holds. On the downside, break of 1.0176 will resume the fall from 1.1213 and target 61.8% projection of 1.1213 to 1.0330 from 1.0629 at 1.0083.

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.

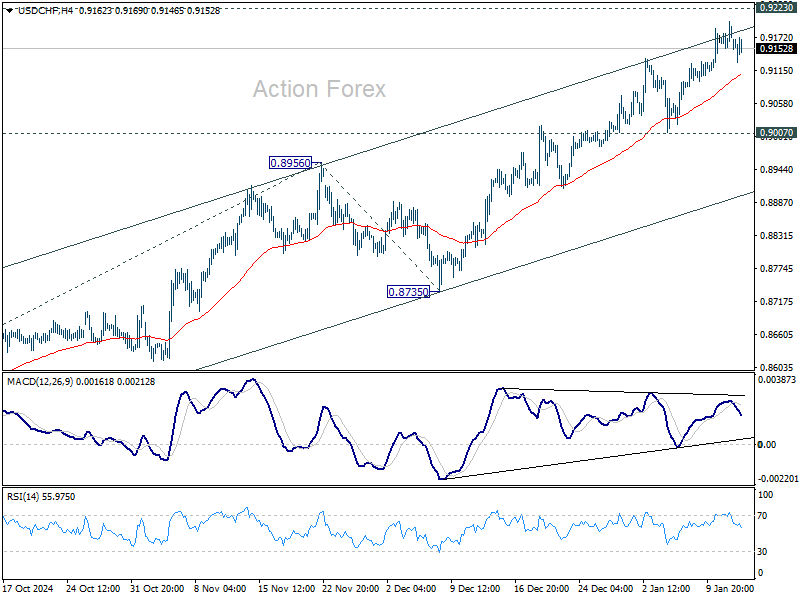

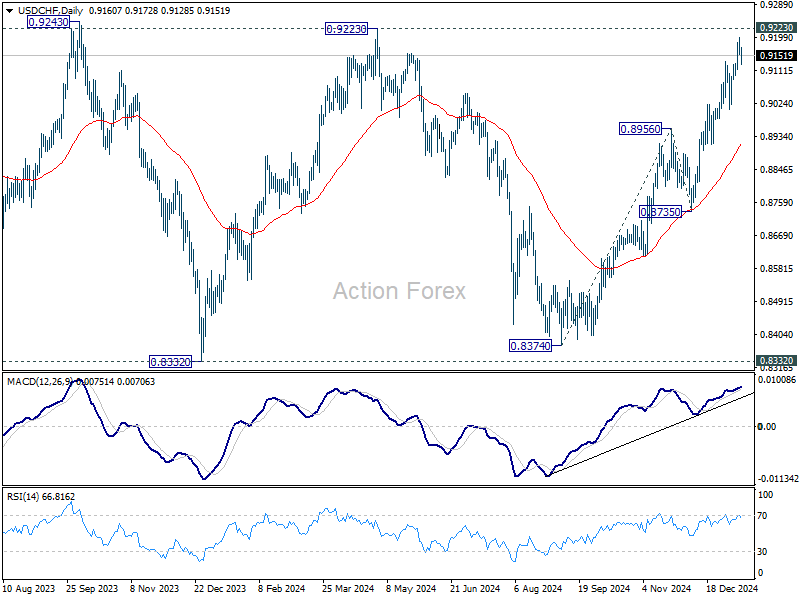

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9150; (P) 0.9176; (R1) 0.9196; More…

Intraday bias in USD/CHF remains neutral for the moment. More consolidations could be seen and deeper pullback cannot be ruled out. But near term outlook will stay bullish as long as 0.9007 support holds, in case of deep retreat. On the upside, decisive break of 0.9223 will carry larger bullish implications.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes. However, decisive break of 0.9223 will be an important sign of bullish trend reversal.

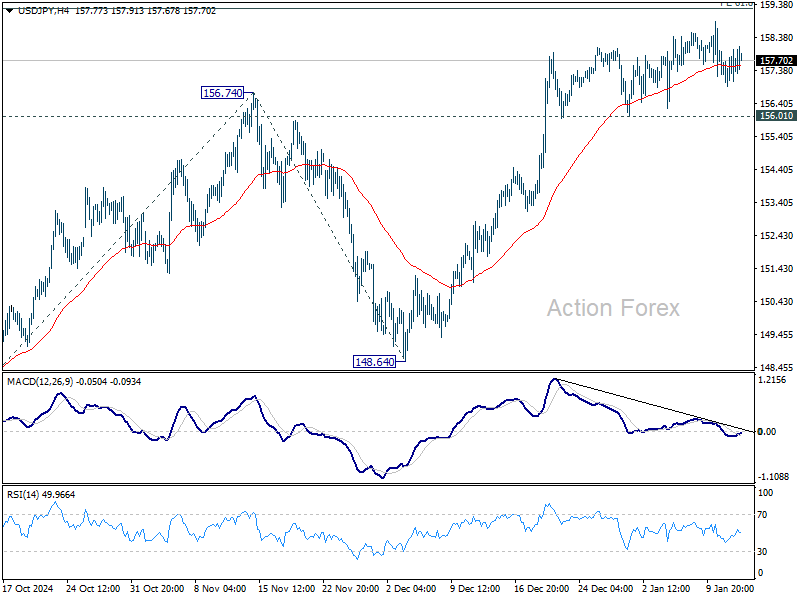

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.94; (P) 157.46; (R1) 157.99; More...

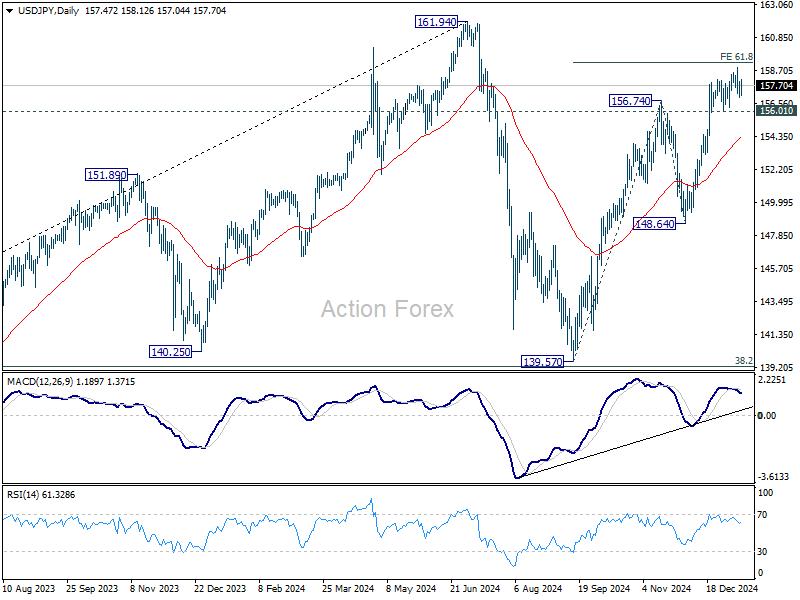

No change in USD/JPY's outlook as sideway trading continues. Intraday bias remains neutral for now. Further rally is in favor as long as 156.0 support holds. On the upside, decisive break of 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25 will extend the rally from 139.57 to retest 161.94 high. However, considering bearish divergence condition in 4H MACD, firm break of 156.01 support will indicate short term topping. Intraday bias will then be back on the downside for 55 D EMA (now at 154.37) instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

US: Small Business Optimism Index Rose to Six-Year High in December as Uncertainty Subsided

The NFIB's Small Business Optimism Index rose 3.4 points to 105.1 in December, beating market expectations for a mild decline. The uncertainty subindex continued to retreat, falling another 12 points in December to 86.

Seven out of ten main subcomponents improved on the month, two fell and one remained unchanged. The largest increase was in the share of owners expecting the economy to improve, which rose 16 points to 52% – the highest level since 2002. Notable gains were also recorded in the share of owners believing that now is a good time to expand (up 6 points to 20%) and expectations about higher real sales (up 8 points to 22%).

The net share of businesses planning to increase employment rose 1 point to 19%, reaching its highest level since spring 2023. The share of firms with unfilled job openings fell one point to 35%. Quality of labor concerns held steady, with 19% of business owners identifying this as their top business problem, second behind inflation concerns. The latter remained unchanged at 20%.

The share of firms increasing employee compensation fell 3 points to 29%, while the share of firms planning to do so over the next three months fell 4 points to 24% – reversing much of the outsized increase in the month prior.

Key Implications

Post-election optimism continues to reverberate across the small business community as uncertainty continues to subside. The improvement is visible in the headline NFIB confidence measure, which rose to its highest level in six years and is echoed across several sub-indicators. For instance, the belief that 'now is a good time to expand', and expectations about 'an improvement in the economy' and 'higher real sales' all surged higher at the tail end of 2024.

As last week's payrolls report showed us, the labor market continues to chug along at a healthy clip, and small businesses appear to echo this theme with plans to increase employment trending up recently. That said, it remains to be seen if this will lead to a major improvement in job growth over the near-term as not all indicators are singing to the same tune. Small business job openings have failed to mimic the improvement in employment plans, instead holding flat at a level that's roughly in line with the pre-pandemic period. Additionally, the fact that compensation trends retreated in December suggests that businesses may not be in a major hurry to fill their open positions.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2131; (P) 1.2172; (R1) 1.2244; More...

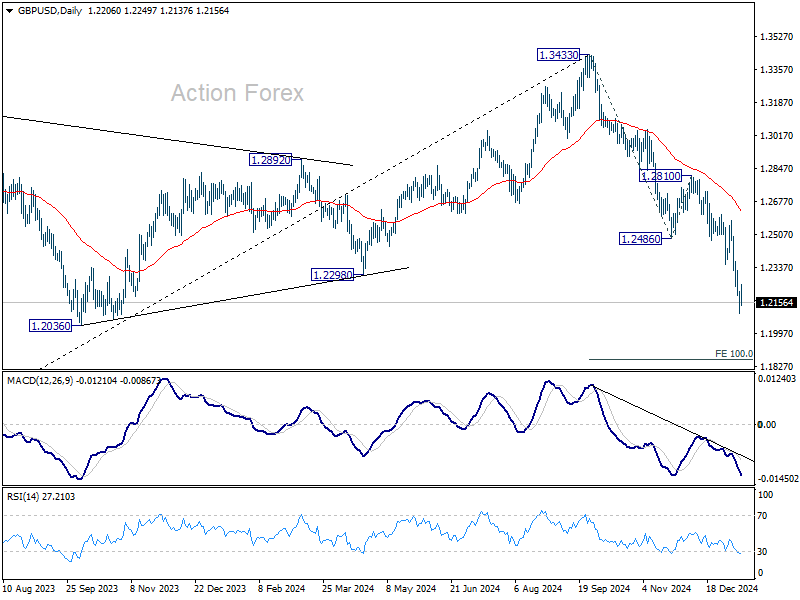

Intraday bias in GBP/USD remains neutral as consolidations continue above 1.2099 temporary low. While stronger recovery cannot be ruled out, outlook will stay bearish as long as 1.2486 support turned resistance holds. Break of 1.2099 will resume the decline from 1.3433 to 100% projection of 1.3433 to 1.2486 from 1.2810 at 1.1863.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433, and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move.

Greenback Holds Ground After Slight PPI Miss, Sterling Weakens Again as Gilt Yields Eye 5%

Dollar is holding steady against its peers in early U.S. trading, with softer-than-expected PPI report failing to trigger significant selling pressure. Market sentiment continues to shift toward the possibility that the Fed might refrain from additional rate cuts in 2025. Fed funds futures are currently pricing in less than 60% probability of a 25bps rate reduction in the first half of the year.

Attention now turns to Tuesday’s U.S. Consumer Price Index (CPI) data, which is anticipated to be a more significant indicator of inflationary trends and policy direction. Currently, the market expects a significant interest rate differential of 200-300 basis points between Fed and ECB by the terminal point of the currency easing cycle. Should domestic inflationary pressures in the US show any signs of resurgence, this differential could skew further toward the higher end of the range, solidifying Dollar strength.

Meanwhile, the Pound continues to bear the brunt of market concerns over the UK's fiscal health. The relentless selloff in UK government bonds drove 10-year Gilt yield to above 4.9%, with a break above 5% psychological barrier appearing increasingly imminent. Such a move could intensify the downward pressure on Sterling, which is already grappling with domestic economic challenges. The UK is bracing for a pivotal week, with CPI data scheduled for Wednesday and GDP figures following on Thursday. These releases could determine whether the Pound can stabilize or face further deterioration.

On the weekly leaderboard, Sterling is the worst performer so far, followed by Yen and Dollar. Kiwi leads the pack with Aussie and Loonie close behind. Euro and Swiss Franc remain in middle positions.

In Europe, at the time of writing, FTSE is down -0.13%. DAX is up 0.83%. CAC is up 0.86%. UK 10-year yield is down -0.004 at 4.887. Germany 10-year yield is up 0022 at 2.617. Earlier in Asia, Nikkei fell -1.83%. Hong Kong HSI rose 1.83%. China Shanghai SSE rose 2.54%. Singapore Strait Times fell -0.08%. Japan 10-year JGB yield rose 0.0319 to 1.244.

US PPI rises 0.2% mom, 3.3% yoy in Dec, miss expectations

US producer prices rose modestly in December, with PPI for final demand increasing by 0.2% mom, falling short of market expectations of 0.3%. The gain was driven primarily by 0.6% mom increase in goods prices, which included a sharp 3.5% rise in energy costs.

In contrast, prices for services remained flat. Excluding the more volatile components of food and energy, core PPI was unchanged for the month, missing the anticipated 0.2% mom increase.

On an annual basis, headline PPI edged higher from 3.0% to 3.3% yoy, narrowly below the forecast of 3.4% yoy. Core PPI, excluding food and energy, rose from 3.4% to 3.5% yoy, also underwhelming expectations of 3.8% yoy.

BoJ’s Himino signals rate hike possible in upcoming meeting

In remarks today, BoJ Deputy Governor Ryozo Himino signaled that a rate hike remains a tangible possibility at the upcoming policy meeting. He said the board "will discuss whether to raise interest rates next week, base its decision on thee projections detailed in the quarterly outlook report.

Himino stated, “When the appropriate timing comes, we must shift policy without delay, as the effect of monetary policy is said to show up with a lag of one to one-and-a-half years.”

The Deputy Governor clarified that BoJ does not rely on a predefined "checklist" for rate decisions. Instead, the board intends to thoroughly analyze the economic outlook and inflation expectations to determine the next steps.

Australian Westpac consumer sentiment dips again, RBA easing unlikely before May

Australia’s Westpac Consumer Sentiment fell -0.7% mom in January, settling at 92.1, reflecting a second consecutive decline. However, Westpac noted a divergence within the data: current conditions sub-indexes weakened, while forward-looking measures were flat or showed slight gains.

RBA faces a mixed picture as it prepares for its next policy meeting on February 17–18. While the central bank appears increasingly confident about bringing inflation back within its 2–3% target range, labor market “stopped easing” in the latter half of 2024 and subdued consumer surveys highlighted “mixed signals”.

According to Westpac, RBA is likely to keep interest rates unchanged in February, with an easing cycle more probable to commence in May.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2131; (P) 1.2172; (R1) 1.2244; More...

Intraday bias in GBP/USD remains neutral as consolidations continue above 1.2099 temporary low. While stronger recovery cannot be ruled out, outlook will stay bearish as long as 1.2486 support turned resistance holds. Break of 1.2099 will resume the decline from 1.3433 to 100% projection of 1.3433 to 1.2486 from 1.2810 at 1.1863.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433, and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move.