Sample Category Title

All Eyes on US CPI Today

In focus today

From the US, we get the most important data release of the day: December CPI. We forecast headline CPI at +0.3% m/m SA (2.8% y/y) and Core CPI at +0.2% m/m SA (3.3% y/y), mostly in line with consensus. The PPI data released already yesterday pointed towards slightly lower-than-expected price pressures. In the evening, a range of Fed speakers will be on the wires, including Barkin, Kashkari, Williams and Goolsbee.

In the euro area, industrial production data for November is released, which is expected to show a small increase of 0.3% m/m by consensus. However, given data released on individual countries we expect production rose 0.7% m/m as Germany rose 1.5% m/m.

In the UK, December inflation data is released this morning at 8:00 CET. Consensus expects headline to remain put at 2.6% y/y but easing in core and services inflation. Focus will be on momentum in core services, which is key for the BoE in determining underlying inflation pressure. Considering the recent sell-off in Gilts and GBP FX, today's print is set to prove highly important for UK markets.

In Sweden, the final details of the December inflation print will be released at 8:00 CET. The flash estimates were below market and Riksbank forecasts. We expect no changes to preliminary outcomes (CPIF 1.5% y/y, CPIF ex Energy 2.1% y/y). Details may affect the January inflation outlook due to volatile price components. Riksbank speeches from Bunge at 9:10 CET and Thedéen at 15:30 CET may offer insights into the inflation print and potential timing of the next rate cut.

Economic and market news

What happened yesterday

In the US, the Core PPI came in lower than expected; keep in mind this (unusually) comes ahead of the CPI due for release tomorrow. EUR/USD edged higher, while UST yields declined. There has been a significant slowdown in the growth of services ex. transportation and core goods PPI. The NFIB survey indicates a continued rebound in US business confidence following the election. Looking at the survey components, it reveals that firms are considerably more optimistic about sales expectations and the general outlook for business expansion. Hiring plans have remained steady, although actual employment changes have slightly weakened. Firms' price plans (which often correlate well with the CPI), have also remained steady. Those firms reporting rising profits mainly attributed this to improving real volumes rather than increased selling prices, which is likely welcomed by the Fed.

In China, the credit and monetary growth data were released, showing slightly stronger than expected results. Year-to-date aggregate financing reached CNY 32260.0 bn (cons: CNY 31560.0bn). although details are not yet available, this overall trend suggest a pick-up in credit in December, supported by stimulus measures. M2 growth increased to 7.3% y/y (prior: 7.1% y/y) in line with consensus.

Equities: Global equities were higher yesterday, driven by cyclical stocks, small caps, and, notably, financials. We had yet another day of supportive macroeconomic figures from the US, but it is important to note that most gains occurred ahead of the key figure releases. When discussing cyclical outperformance over the past few years, it has largely been related to technology, consumer discretionary, and communication services. However, year to date, the best-performing sector is energy, with oil prices up by 7%, followed by materials. While it aligns with the business cycle to see energy and materials outperforming, we believe better data from China is necessary to support continued outperformance in these sectors. In the US yesterday, the Dow was up by 0.5%, the S&P 500 increased by 0.1%, the Nasdaq declined by 0.2%, and the Russell 2000 rose by 1.1%. Markets are mixed in Asia this morning, while both European and US futures are marginally higher.

FI: European government bond yields continued to rise yesterday and there was a modest bearish steepening of the various EGB curves. The Bund ASW-spread keeps testing the 0bp-level and we do expect to break through the level and go towards -10bp to -15bp given the supply as well as no QE. We discuss the outlook for the Bund ASW-spread as well as ECB and our top trades for 2025 in our special edition of RTM EUR. See RtM EUR - Outlook and top trades in 2025, 14 January.

FX: Yesterday proved another relatively soft session for the USD with EUR/USD moving back above the 1.03 level. Also, the JPY had a relatively weak session with USD/JPY moving sideways to marginally higher. In the Scandies, lower energy prices weighed on the NOK while the SEK remained close to unchanged. Finally, GBP had another volatile and nervous session ahead of today's CPI print.

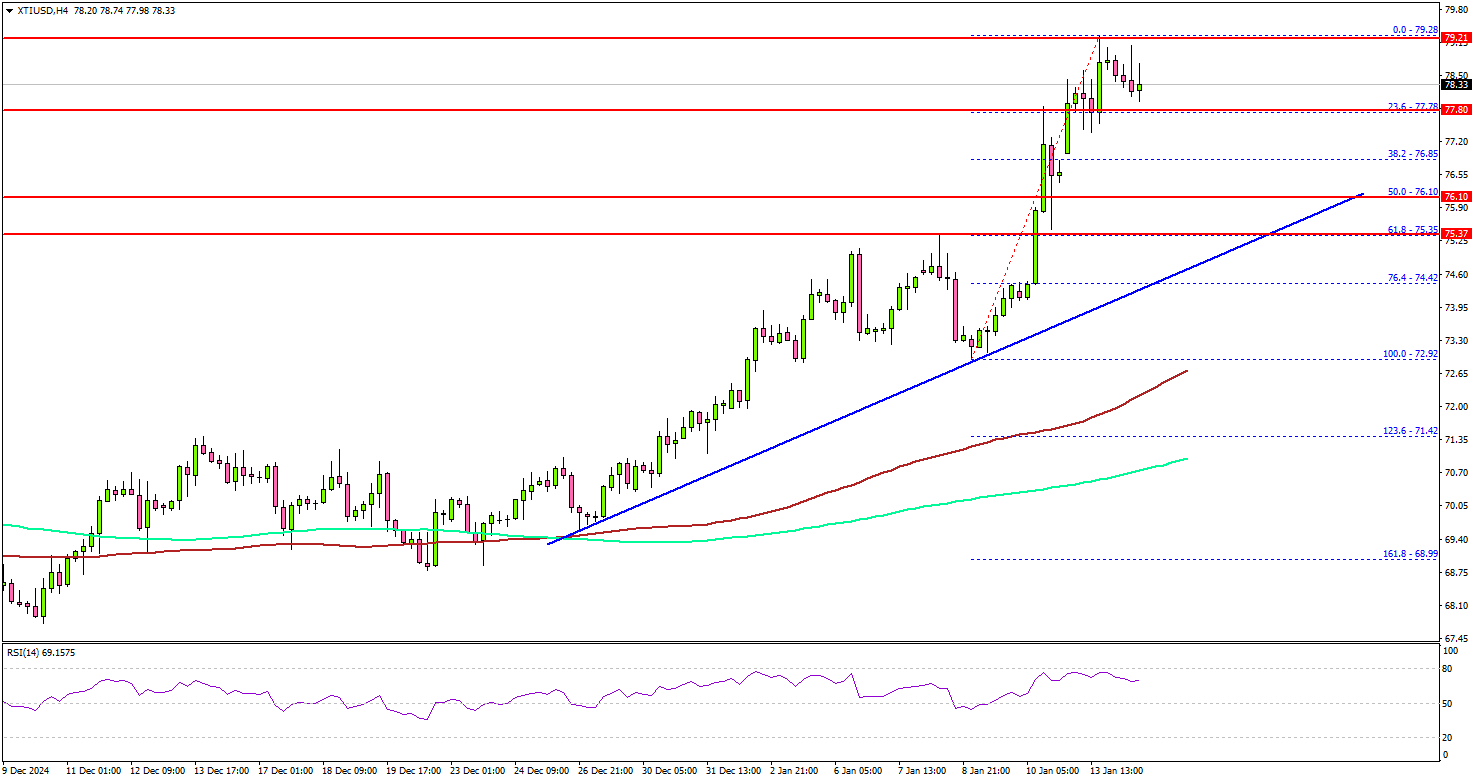

WTI Crude Oil Prices Surge: Bulls Drive the Rally, US CPI Next

Key Highlights

- WTI Crude Oil prices started a fresh increase above the $73.50 resistance zone.

- A connecting bullish trend line is forming with support at $75.35 on the 4-hour chart.

- Gold prices started a consolidation phase above the $2,635 support.

- The US CPI could increase by 2.9% in Dec 2024 (YoY).

WTI Crude Oil Price Technical Analysis

WTI Crude Oil price found support near the $72.00 zone. A base was formed and the price started a fresh increase above $75.00.

Looking at the 4-hour chart of XTI/USD, the price traded gained pace for a move above the $76.80 resistance zone, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour).

The bulls even pushed prices above the $78.00 level. A high was formed at $79.28 and the price is now consolidating gains. There was a minor decline toward the 23.6% Fib retracement level of the upward move from the $72.92 swing low to the $79.28 high.

On the upside, the price is facing hurdles near the $79.20 level. The main hurdle is now near the $80.00 zone, above which the price may perhaps accelerate higher.

In the stated case, it could even visit the $82.50 resistance. Any more gains might call for a test of the $85.00 resistance zone in the near term. On the downside, the first major support sits near the $76.85 zone.

A daily close below $76.85 could open the doors for a larger decline. The next major support is $75.35 and the trend line. Any more losses might send oil prices toward $72.00 in the coming days.

Looking at Gold, there was a steady increase above the $2,635 level and the price is now consolidating gains.

Economic Releases to Watch Today

- US Consumer Price Index for Dec 2024 (MoM) – Forecast +0.3%, versus +0.3% previous.

- US Consumer Price Index for Dec 2024 (YoY) – Forecast +2.9%, versus +2.7% previous.

US Consumer Price Index Ex Food & Energy for Dec 2024 (YoY) – Forecast +3.3%, versus +3.3% previous.

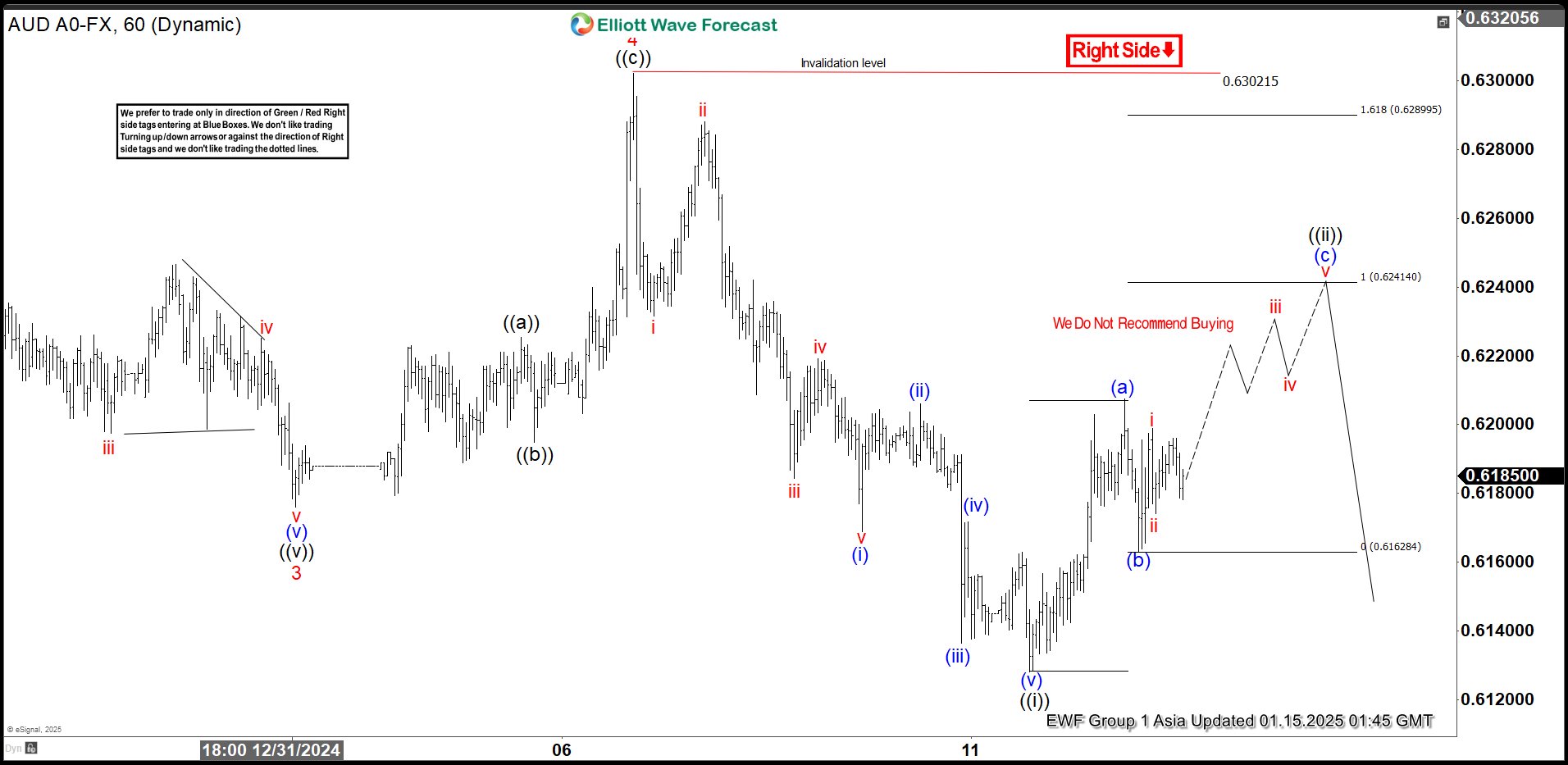

Elliott Wave View Looking for AUDUSD to Resume Lower

Short Term Elliott Wave view in AUDUSD suggests that cycle from 9.30.2024 high is in progress as an impulse. Down from 9.30.2024 high, wave 1 ended at 0.6434 and wave 2 rally ended at 0.6528. Pair resumed lower in wave 3 towards 0.6176 as the 1 hour chart below shows. Wave 4 rally ended at 0.63. Internal subdivision of wave 4 unfolded as a zigzag Elliott Wave structure.

Up from wave 3, wave ((a)) ended at 0.6225 and pullback in wave ((b)) ended at 0.6194. Wave ((c)) higher ended at 0.63 which completed wave 4 in higher degree. Pair has resumed lower in wave 5 which subdivides into another 5 waves. Down from wave 4, wave ((i)) ended at 0.6128. Wave ((ii)) rally is in progress as a zigzag with wave (a) ended at 0.6207 and wave (b) ended at 0.6162. Expect wave (c) higher to end at 0.624 – 0.629 area and this should complete wave ((ii)) in higher degree. As far as pivot at 0.6302 high stays intact, expect rally to fail in 3, 7, 11 swing for further downside.

AUDUSD 60 Minutes Elliott Wave Chart

AUDUSD Elliott Wave Video

https://www.youtube.com/watch?v=wsLrJqyGzFc

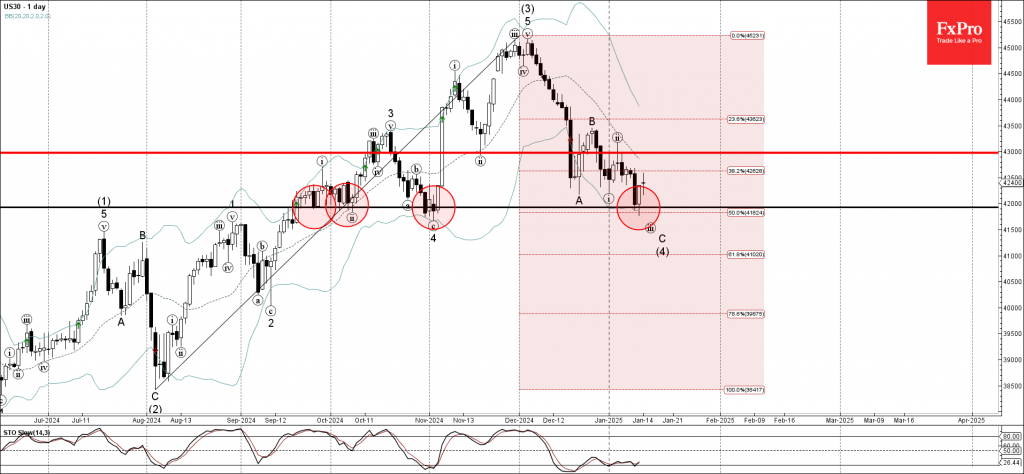

Down Jones Wave Analysis

- Down Jones reversed from support level 42000.00

- Likely to rise to resistance level 43000.00

Down Jones index recently reversed up with the daily Piercing Line reversal pattern from the pivotal support level 42000.00, which has been reversing the price from September.

The support level 42000.00 was strengthened by the lower daily Bollinger Band and the 50% Fibonacci correction of the upward impulse from August.

Given the strength of the support level 42000.00 and the improvement in investor sentiment as seen across the global equity markets, Down Jones index can be expected to rise to the next resistance level 43000.00.

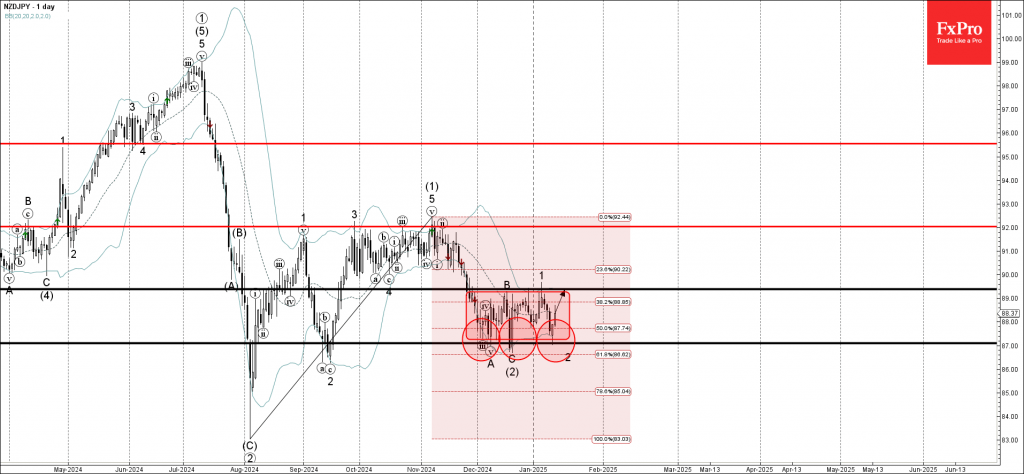

NZDJPY Wave Analysis

- NZDJPY reversed from key support level 87.00

- Likely to rise to resistance level 89.40

NZDJPY currency pair recently reversed up from the key support level 87.00, which is the lower border of the sideways price range inside which the pair has been moving for the last few weeks.

The support level 87.00 was also strengthened by the lower daily Bollinger Band and the 50% Fibonacci correction of the upward impulse from August.

NZDJPY currency pair can be expected to rise to the next resistance level 89.40 (upper border of the active sideways price range and the top of the previous waves B and 1).

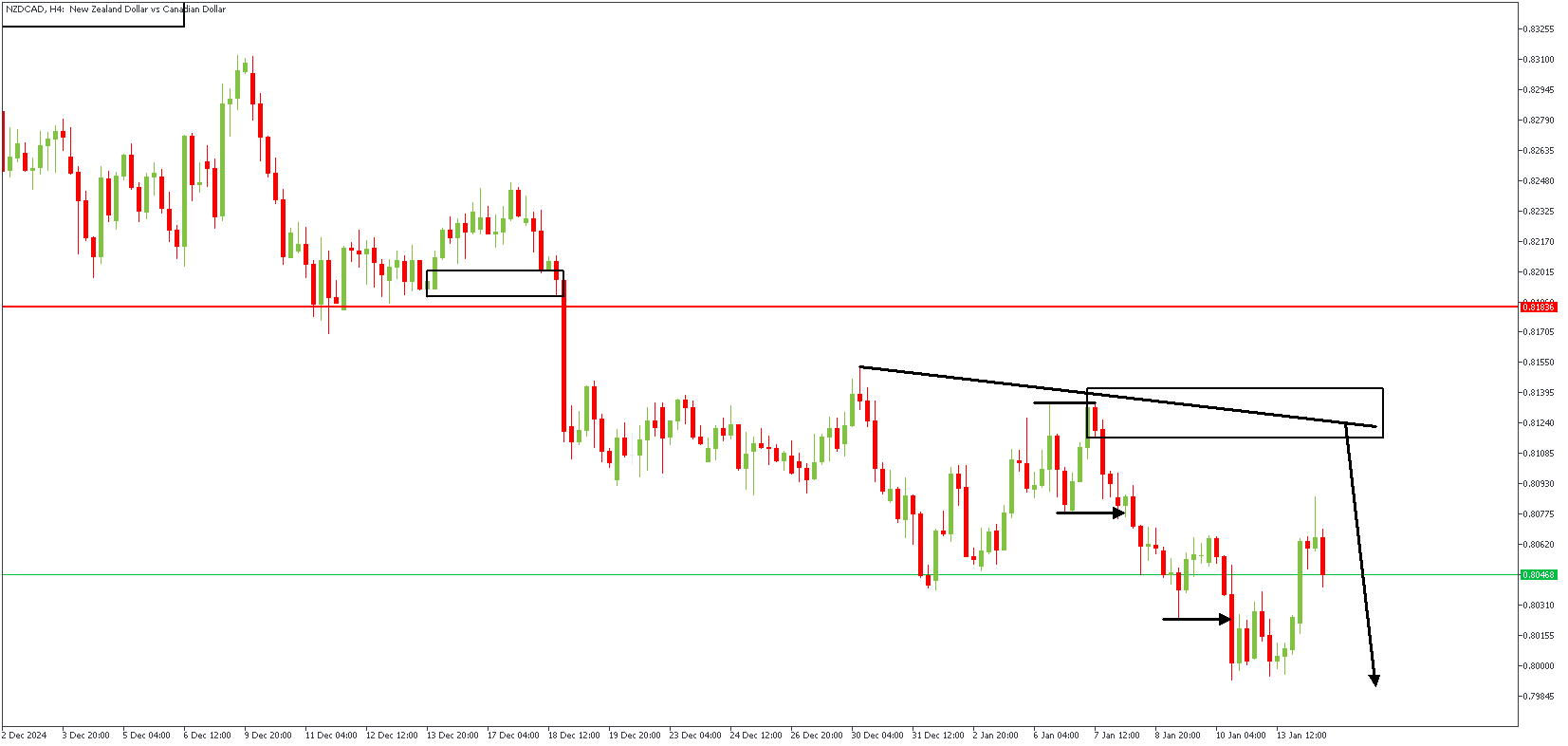

NZDCAD Bearish Sentiment Breakdown

The NZDUSD pair continues to rise for the second straight day, trading near 0.5610 on Tuesday morning. This boost is partly due to China's recent economic support measures, as New Zealand's close trade ties with China mean its economy heavily influences the New Zealand Dollar. China's central bank officials have announced plans to use tools like interest rate adjustments and increased fiscal spending to stabilize their economy and keep the Yuan exchange rate steady, which has fueled market optimism.

After reports from US President-elect Donald Trump's team considered a gradual approach to raising import tariffs and easing fears of sudden inflation, the New Zealand dollar also gained from positive risk sentiment. Meanwhile, the US Dollar has eased slightly after hitting a high last seen in November 2022, supported by strong US labor market data and rising Treasury yields. At the same time, traders are waiting for December's US Producer Price Index (PPI) data, which could further influence the US Dollar's movements. Overall, the Kiwi Dollar remains strong amid global economic developments.

NZDCAD – H4 Timeframe

The price action on the 4-hour timeframe of NZDCAD already shows an initial break below the previous low. The price is currently inching toward the supply zone at the origin of the bearish impulse. The said supply zone is in confluence with the 88% Fibonacci retracement level and trendline resistance.

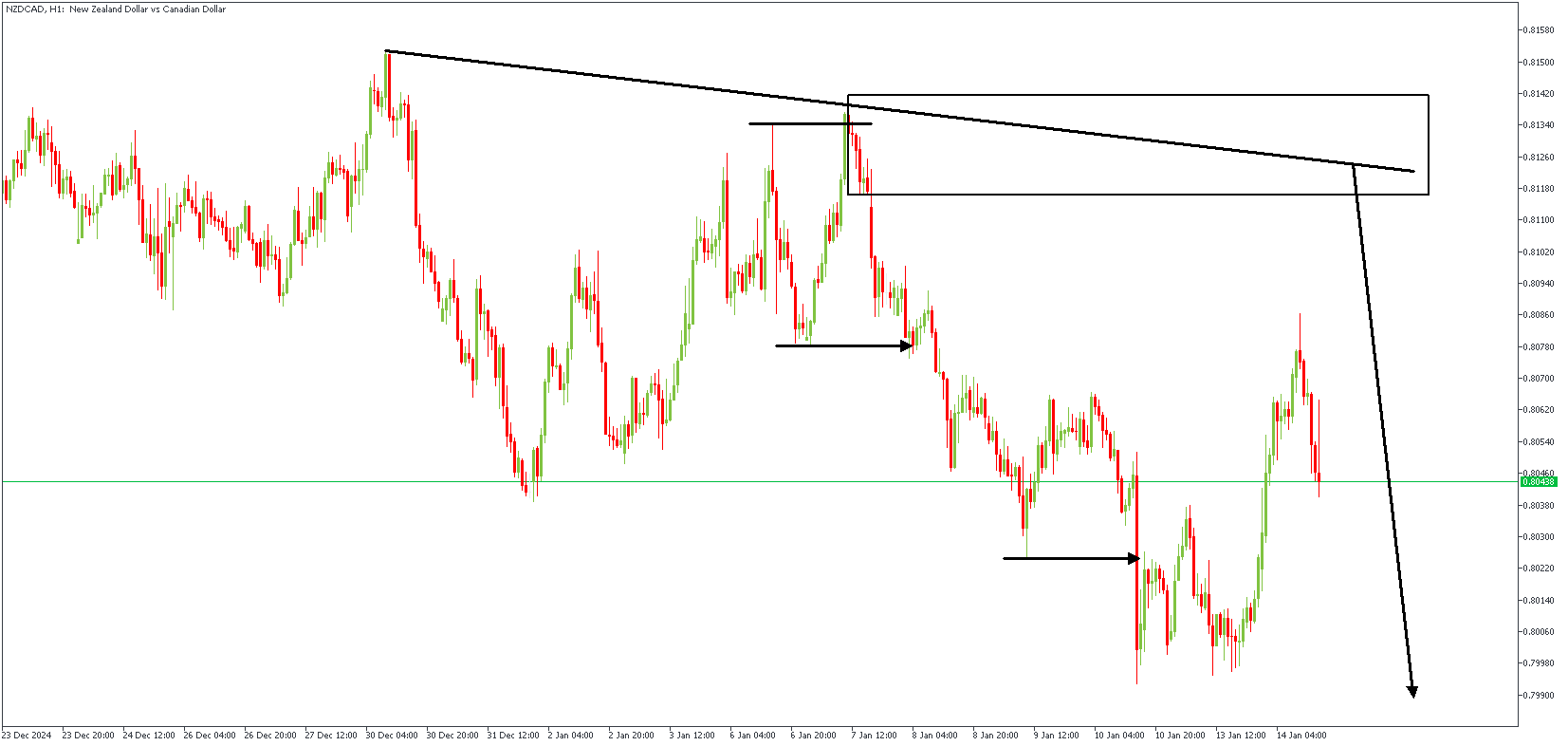

NZDCAD – H1 Timeframe

The SBR pattern on the H1 timeframe aligns perfectly with the sentiment from the 4-hour timeframe chart of NZDCAD. Here, we can see the sweep above the previous high, immediately followed by a bearish break of structure, further confirming the likelihood of a bearish continuation at the retest of the rally-base-drop supply zone.

Analyst's Expectations:

- Direction: Bearish

- Target: 0.80139

- Invalidation: 0.81525

GBPNZD Maintains Bullish Outlook

The GBPUSD pair has fallen sharply for five days, reaching its lowest point since November 2023, around 1.2120. The British Pound has been struggling due to concerns about "stagflation," which combines high inflation with weak economic growth. Adding to the pressure, rising UK government bond yields after the Labour government's budget plan in October have raised fears that borrowing targets may not be met. Meanwhile, a strong US Dollar, backed by expectations that the Federal Reserve will pause rate cuts soon, is further weighing on the Pound.

The US Dollar remains strong after better-than-expected job numbers for December, which showed 256K jobs added and a slight drop in the unemployment rate to 4.1%. Ongoing global risks, like the Russia-Ukraine conflict and Middle East tensions, are boosting demand for safer assets like the Dollar. Even though the Pound has recovered slightly from its daily low, the overall market outlook suggests it could face more downward pressure. Investors remain cautious, and any bounce-back for GBPUSD might not last long.

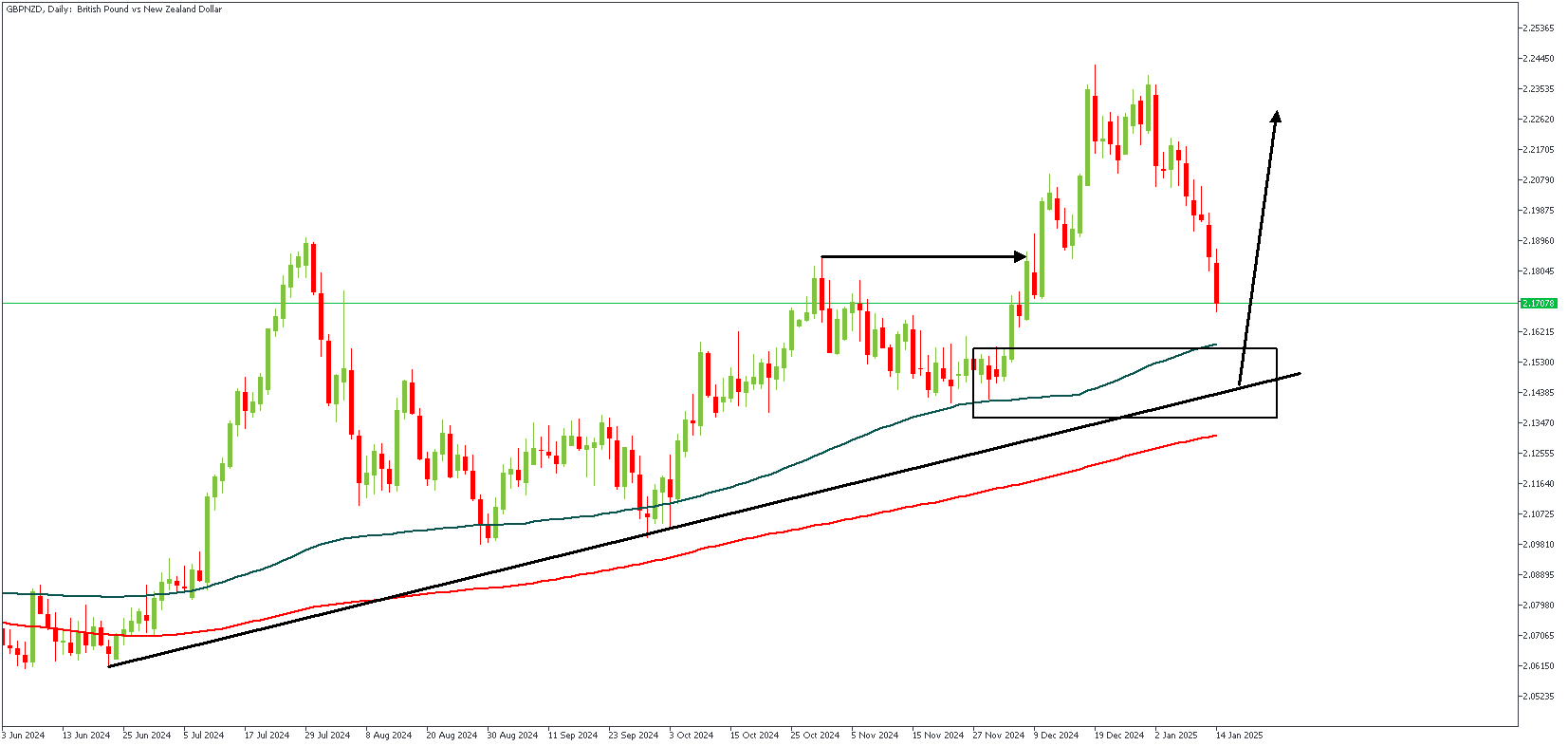

GBPNZD – D1 Timeframe

Following the bullish break of structure on the daily timeframe chart of GBPNZD, we see a steady downward glide as the price aims for the demand zone at the origin of the bullish break. Interestingly, the 100-day moving average and a trendline support the drop-base-rally demand at the base of the impulse.

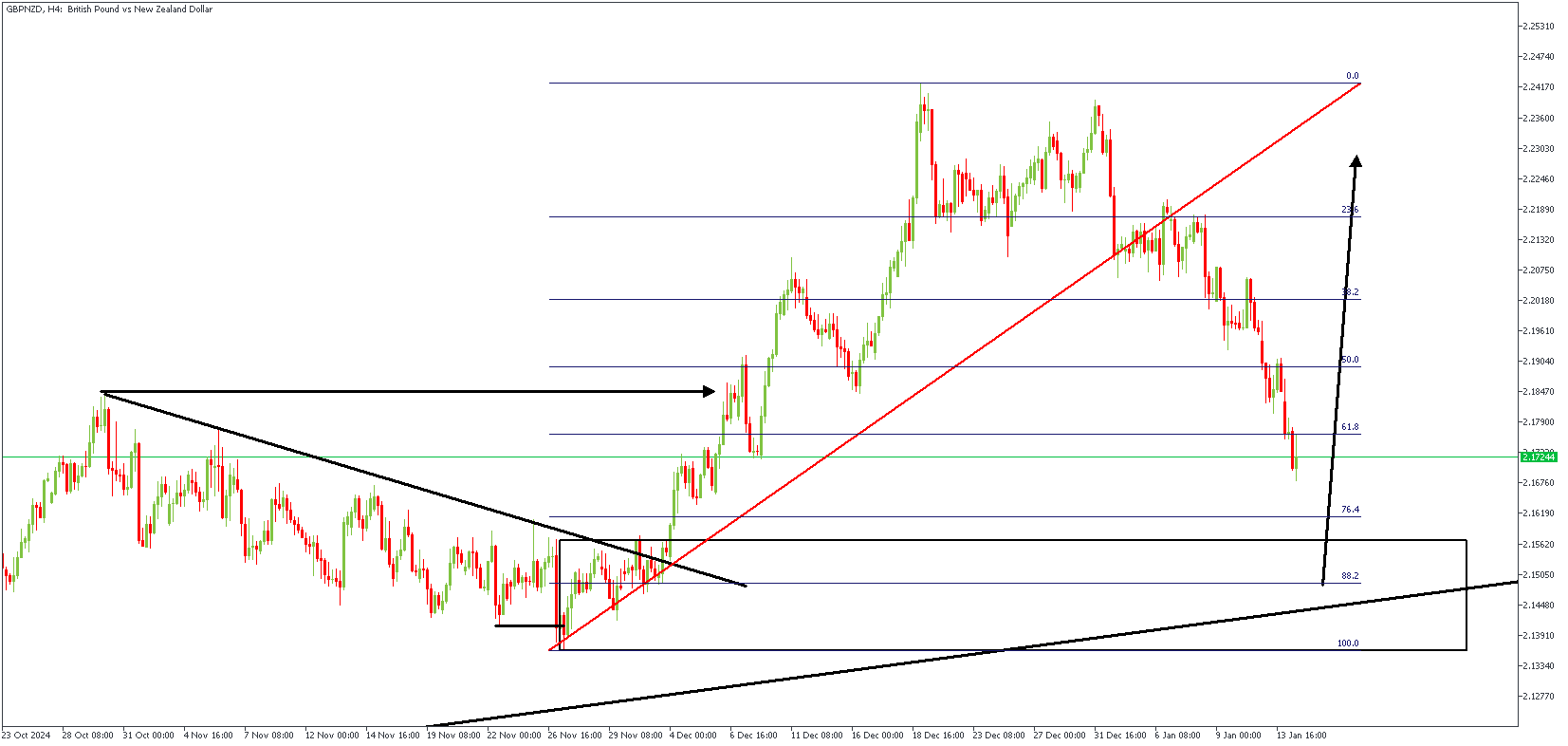

GBPNZD – H4 Timeframe

On the 4-hour timeframe of GBPNZD, we can see that price had a sweep of liquidity just before the onset of the bullish momentum. In this light, and with the other confluences observed on the daily timeframe, it is safe to conclude in favor of a bullish outcome.

Analyst's Expectations:

- Direction: Bullish

- Target: 2.21677

- Invalidation: 2.13569

Eurozone’s Uneven Economic Recovery Means More Monetary Easing

Summary

- The Eurozone economy is entering 2025 on an unsteady and uncertain footing. While household fundamentals are still favorable overall, they may become less supportive as 2025 progresses, suggesting the pace of consumer spending could slow. The outlook for the corporate sector remains challenging, and a further decline in investment spending cannot be ruled out.

- In addition to mixed fundamentals, sentiment has slipped through the latter part of 2024. Political uncertainties in France and Germany, and concerns surrounding the threat of U.S. tariffs on imports from Europe, are factors that have weighed on sentiment. Given the mixed fundamental backdrop and softening sentiment, our Eurozone GDP outlook for 2025 is for growth of just 0.9%. However, considering the prevailing uncertainties, we view the risks to even this modest outlook as to the downside.

- Considering the underwhelming Eurozone economic outlook, and even with some lingering inflation pressures, we expect the European Central Bank (ECB) to continue steadily along its monetary easing path through much of 2025. We maintain our outlook for 25 bps ECB rate cuts at the January, March, April and June meetings, with a final 25 bps rate cut in September, for a terminal ECB policy rate of 1.75%. The growing wedge between European Central Bank and Federal Reserve policy interest rates is likely, in our view, to keep the euro on the defensive versus the greenback over the medium term.

Eurozone Outlook Remains Uncertain And Unsteady

The Eurozone economy stagnated in 2023, in response to a spike in energy prices and inflation, and as European Central Bank monetary policy moved into restrictive territory. The region's economy has since experienced a recovery starting from early 2024, although that rebound has been uneven—a trend we think is likely to continue in 2025 given distinctly mixed fundamentals and as sentiment surveys remain downbeat.

Among the brighter pieces of recent economic news, Eurozone Q3 GDP grew 0.4% quarter-over-quarter, lead by a 0.7% gain in consumer spending. There are also indications that consumer activity may have continued expanding during the fourth quarter, with real retail sales for the October-November period up 0.4% compared to their third quarter average. However, while consumer fundamentals remain favorable overall (and certainly more so than for the corporate sector), there are signs they may become less supportive as 2025 progresses.

For the latest available figures (Q3-2024), growth in real employee compensation (3.1% year-over-year) and household disposable income (2.3%) outpaced growth in consumer spending (1.0%). While those favorable income trends would usually be considered supportive for the consumer outlook, the European Central Bank argued in a recent Economic Bulletin article that household savings could remain high, as households aim to rebuild their “real” net wealth that has been eroded by inflation in recent years. That is consistent with the Q3 household saving rate, which fell slightly to 15.3% of disposable income, but remains noticeably above the average of 13% in the year prior to the pandemic. Finally, while employment growth has held up to date, survey data suggest a slowdown in job gains may be ahead. The European Commission's Employment Expectations Indicator fell to 97.3 in December, a level that is historically consistent with job growth well below its current pace of 1.0% year-over-year in Q3-2024. Thus, while household fundamentals are favorable overall, they may become less supportive as 2025 progresses. Overall, we expect consumer spending will continue to advance this year. However, the combination of the potential for slower employment (and thus income) growth and continued consumer caution suggests gains in consumer expenditures may struggle to match the pace seen during the second half of 2024.

In contrast to the household sector, the outlook for the corporate sector remains more challenging. In Q3-2024, fixed investment spending rose 2.0% quarter-over-quarter, however much of that rise reflected a jump in the volatile intellectual property products component. We estimate that our measure of core ex-housing investment (which excludes both residential investment and intellectual property products) fell 1.6% quarter-over-quarter and 2.4% year-over-year. Moreover, we see reasons for investment spending to remain restrained in the quarters ahead. Net entrepreneurial income, a proxy for corporate profits, fell 4.6% year-over-year in Q3, a lack of profitability that may crimp investment spending. With manufacturing capacity utilization also at its lowest level since the pandemic, a further decline in investment spending cannot be ruled out.

Sentiment Slips Amid Rising Risks

In addition to these mixed fundamental factors, sentiment has slipped through the latter part of 2024, suggesting some downside risk to business investment in particular, and consumer spending to a lesser extent. Eurozone sentiment was at its most upbeat earlier in 2024, with the services PMI peaking at 53.3 in April and the manufacturing PMI peaking at 47.3 in May. Since then, however, Eurozone sentiment has followed a softening overall trend. By December the manufacturing PMI fell further into contraction territory at 45.1, while the services PMI was consistent with only modestly positive expansion at 51.6. As result, the composite (or economy-wide) PMI printed at 49.6, a level historically consistent with a stagnating economy.

Political uncertainty has weighed on sentiment to some extent, with French President Macron's centrist ruling coalition losing legislative elections in July, and the new French Prime Minister (and government) subsequently losing a vote of no-confidence in December. German Chancellor Scholz also lost a confidence vote late last year, with an election now scheduled for 23 February. Another factor likely weighing on sentiment is the threat of U.S. tariffs on imports from Europe. While the economic impact may be moderate—with Eurozone merchandise exports to the United States accounting for a little more than 3% of the region's GDP—the uncertainty surrounding tariffs could certainly weigh on investment spending and employment decisions.

Given the mixed fundamental backdrop and softening sentiment, our Eurozone GDP outlook for 2025 is for growth of just 0.9%. However, considering the prevailing uncertainties, we view the risks to even this modest outlook as to the downside.

European Central Bank Easing to Continue At a Steady Pace

Considering the underwhelming Eurozone economic outlook, and even with some lingering inflation pressures, we expect the European Central Bank (ECB) to continue steadily along its monetary easing path through much of 2025. Eurozone headline and core inflation are running moderately above the central bank's 2% inflation target, with January readings of 2.4% year-over-year and 2.7% year-over-year respectively. Services inflation is proving somewhat more stubborn at 4.0%. Still, with ECB policymakers expecting wage growth to slow and services inflation to ease, overall inflation is expected to converge more sustainably toward the 2% target by later in 2025. Moreover, we expect the European Central Bank to lower its policy interest rate largely independent of how fast, or how far, the Federal Reserve eases monetary policy. ECB policymakers have said as much in recent days. Governing Council member Olli Rehn said against “the backdrop of disinflation being on track and the growth outlook having weakened it makes sense to continue rate cuts” adding the ECB “is not the 13th federal district of the Federal Reserve System, we take decisions on the basis of our mandate, which is price stability in the euro area.” Croatia's Boris Vujcic said “we are not dependent on the Fed or any other central bank,” while Chief Economist Philip Lane said the ECB is likely to reduce rates further in order to ensure price stability and growth. Considering the economic environment and central bank signals, we maintain our outlook for 25 bps ECB rate cuts at the January, March, April and June meetings, with a final 25 bps rate cut in September, for a terminal ECB policy rate of 1.75%. Moreover, given a growing wedge between European Central Bank and Federal Reserve policy interest rates, we expect the euro to remain on the defensive versus the greenback over the medium term. As of now, we target a long-term EUR/USD exchange rate of $0.9700.

Gold (XAU/USD) Price Tug-of-War Continues. Breakout Incoming?

- Gold prices are currently in flux thanks to the US Dollar, global trade uncertainties, and geopolitics.

- A softer-than-expected US PPI release caused a temporary jump in Gold prices.

- The upcoming US CPI release is a key event that could trigger a significant move in Gold prices.

Gold prices continue to sway back and forth as markets weigh a strong US Dollar and growing uncertainties around global trade and geopolitics. On the other end we had a strong U.S. jobs report last week which boosted the dollar, and thus weighed on Gold prices.

A softer than expected US PPI release today helped Gold jump back toward the 2670/oz handle after hovering in the 2660’s for the majority of the European session. However the print has not really moved the needle when it comes to rate cut expectations, with markets still pricing in a more hawkish Fed in 2025.

Tomorrow we do have the US CPI release which could prove to be a catalyst for a bigger move. However this will rest on the data with a big deviation from expectations required in order for a major move to occur.

Markets are expecting a CPI headline print to come in at 2.9% and the MoM to come in at 0.4%. A significant beat of the forecast would likely see US treasury yields surge and thus drag Gold prices lower. There have however been occasions of late where Gold prices have remained resilient in the face of a stronger US Dollar and US data. Any moves after data releases have proved short-lived as we saw today following the PPI print.

Yesterday news filtered through that Donald Trump’s administration is considering gradually increasing tariffs to avoid causing a sharp rise in inflation, according to sources. I covered the implications of this on the US Dollar as well as an outlook on the US CPI release tomorrow: US Inflation: PPI, CPI Release Dates, DXY Analysis & Market Impact

Technical Analysis Gold (XAU/USD)

From a technical analysis standpoint, this analysis is a follow up from the technicals last week. Read: Gold (XAU/USD) Price Analysis: Will Prices Continue to Soar in 2025?

Gold appears poised for another leg higher looking at basic price action on a daily timeframe.

The precious metal saw a significant pullback yesterday printing a bearish engulfing candle on the daily timeframe. Today however has not resulted in any follow through with the precious metal now on course for a bullish inside bar candle close.

This would hint at further upside tomorrow with US CPI waiting in the wings. Gold does appear to have found support at the previous swing high around the 2658 handle and this is why from a price action perspective on the daily timeframe I am inclined to believe that we could be set for another push to the upside.

The 14-period RSI also supports this as the 50 level on the RSI has held firm indicating that bullish momentum remains in play.

The question will be whether the precious metal will have enough to break above the psychological 2700/oz handle.

Gold (XAU/USD) Daily Chart, January 14, 2025

Source: TradingView (click to enlarge)

Dropping down to a H1 chart and as you can see below, the red block has been holding prices in a tight $16-$17 range between the 2674 and 2658 handles respectively.

A one-hour candle close outside of the red block may lead to a breakout in that direction. I would however urge caution especially if the breakout occurs during the CPI release tomorrow.

What we have seen from recent price action is that such moves have failed to gain traction of late, usually reversing in the hours after the news or data release.

Gold (XAU/USD) One-Hour H1 Chart, January 14, 2025

Source: TradingView (click to enlarge)

Support

- 2664

- 2658

- 2650

Resistance

- 2674

- 2685

- 2700