Sample Category Title

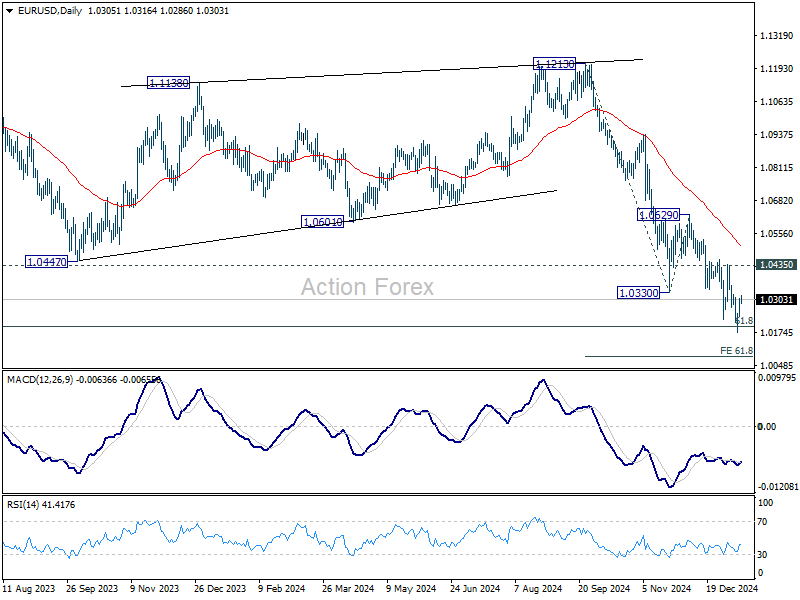

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0261; (P) 1.0286; (R1) 1.0333; More...

Intraday bias in EUR/USD remains neutral as consolidations continue above 1.0176. While stronger recovery cannot be ruled out, outlook will stay bearish as long as 1.0435 resistance holds. On the downside, break of 1.0176 will resume the fall from 1.1213 and target 61.8% projection of 1.1213 to 1.0330 from 1.0629 at 1.0083.

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.

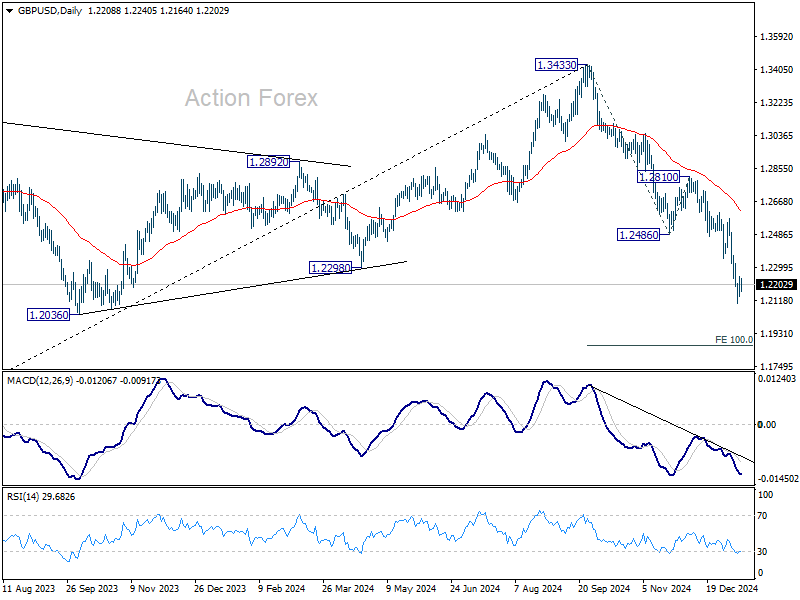

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2154; (P) 1.2202; (R1) 1.2264; More...

GBP/USD is staying in consolidation above 1.2099 and intraday bias remains neutral. While stronger recovery cannot be ruled out, outlook will stay bearish as long as 1.2486 support turned resistance holds. Break of 1.2099 will resume the decline from 1.3433 to 100% projection of 1.3433 to 1.2486 from 1.2810 at 1.1863.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433, and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move.

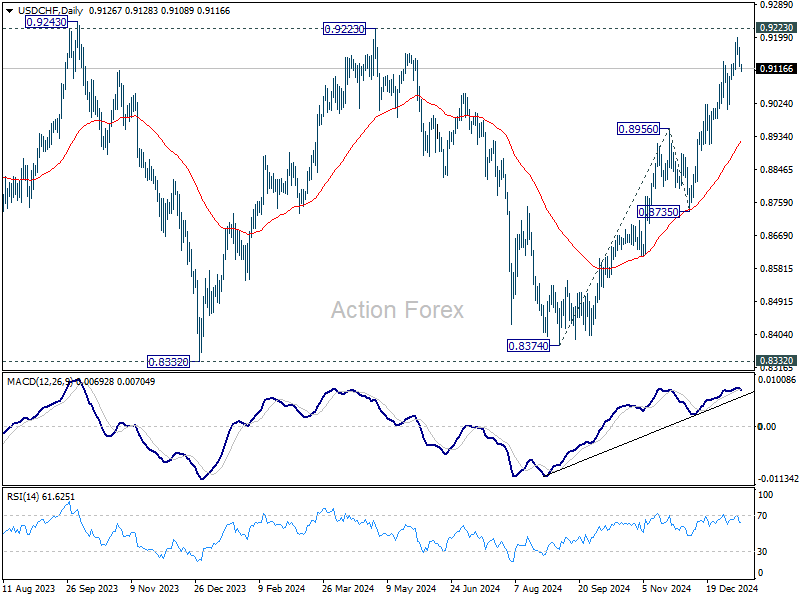

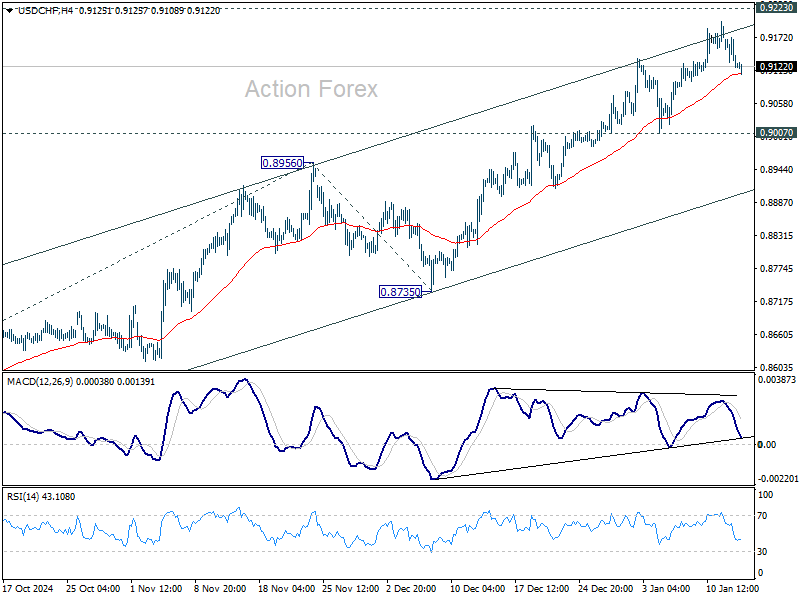

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9105; (P) 0.9141; (R1) 0.9159; More…

Intraday bias in USD/CHF stays neutral and outlook is unchanged. More consolidations could be seen and deeper pullback cannot be ruled out. But near term outlook will stay bullish as long as 0.9007 support holds, in case of deep retreat. On the upside, decisive break of 0.9223 will carry larger bullish implications.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes. However, decisive break of 0.9223 will be an important sign of bullish trend reversal.

Australian Dollar Gains, but Rate Uncertainty Limits Potential

The AUD/USD pair climbed to 0.6192 midweek, reflecting cautious optimism in the market. Traders remain vigilant ahead of key December inflation data from the US, which could influence expectations regarding the Federal Reserve’s potential interest rate cuts in 2025. Earlier, the Australian dollar recovered some of its losses as the US dollar reacted to Producer Price Index statistics.

Key upcoming events for the AUD

Australia will release its employment report on Thursday, a critical data point for assessing the state of the labour market. These figures are crucial for adjusting forecasts concerning the Reserve Bank of Australia’s (RBA) interest rate trajectory.

Fresh Q4 2024 inflation data for Australia will also be published at the end of the month. These data will be pivotal in shaping expectations for the RBA’s upcoming meeting and its decisions on borrowing costs.

Investors currently assign a 70% probability of a rate cut at the RBA’s February meeting. If realised, the rate could decrease by 25 basis points from the current 4.35% per annum. Market prices have already factored in this potential decision.

However, lingering uncertainty about the RBA’s future policy direction and the terminal rate target for the year keeps investors cautious, limiting the AUD’s upside potential.

Technical analysis of AUD/USD

On the H4 chart, AUD/USD is developing an upward wave targeting 0.6211. This level is expected to be tested today, followed by a potential decline towards 0.6161. A consolidation range is likely to form around 0.6161. If the pair breaks upwards from this range, a correction to 0.6290 could materialise. Conversely, a downward breakout could trigger a new wave targeting 0.6116. The MACD indicator supports this scenario, with its signal line below the zero mark but pointing sharply upwards.

On the H1 chart, the pair is building a growth wave towards 0.6211, which is expected to be reached today. Following this, a corrective move to 0.6161 may occur. The Stochastic oscillator confirms this scenario, with its signal line above the 50 mark and trending upwards towards 80.

Conclusion

The Australian dollar’s recent recovery is tempered by uncertainty surrounding the RBA’s future policy decisions. Key domestic data, including employment figures and Q4 inflation, heavily influence market expectations. While technical indicators suggest short-term growth potential for AUD/USD, further gains will depend on clarity regarding the RBA’s policy trajectory and broader economic conditions.

Gold and WTI Crude Oil Prices Regain Momentum

Gold price started a fresh increase above the $2,665 resistance level. WTI Crude oil prices climbed higher above $77.00 and might extend gains.

Important Takeaways for Gold and WTI Crude Oil Prices Analysis Today

- Gold price started a steady increase from the $2,630 zone against the US Dollar.

- It cleared a key bearish trend line with resistance at $2,670 on the hourly chart of gold at FXOpen.

- WTI Crude oil prices extended gains above the $74.40 and $76.50 resistance levels.

- There is a short-term declining channel forming with support at $76.00 on the hourly chart of XTI/USD at FXOpen.

Gold Price Technical Analysis

On the hourly chart of Gold at FXOpen, the price formed a base near the $2,630 zone. The price started a steady increase above the $2,650 and $2,665 resistance levels.

There was a decent move above the 50-hour simple moving average and $2,680. The bulls pushed the price above the $2,690 resistance zone. Finally, the bears appeared near $2,700. A high was formed near $2,697 before there was a downside correction.

A low was formed at $2,656 and the price is again rising. There was a move above the 23.6% Fib retracement level of the downside correction from the $2,697 swing high to the $2,656 low.

Gold cleared a key bearish trend line with resistance at $2,670. The RSI is now above 50 and the price is now facing hurdles. Immediate resistance is near the $2,678 level or the 50% Fib retracement level of the downside correction from the $2,697 swing high to the $2,656 low.

The next major resistance is near the $2,688 level. An upside break above the $2,688 resistance could send Gold price toward $2,698. Any more gains may perhaps set the pace for an increase toward the $2,720 level.

On the downside, immediate support is near the $2,665 level. The next major support sits at $2,655, below which the price might test $2,645. Any more losses might send the price toward the $2,630 support zone.

Oil Price Technical Analysis

On the hourly chart of WTI Crude Oil at FXOpen, the price started a major upward move from $72.30 against the US Dollar. The price gained bullish momentum after it broke the $75.00 resistance and the 50-hour simple moving average.

The bulls pushed the price above the $76.50 and $77.00 resistance levels. The recent high was formed at $77.82 and the price started a downside correction. There was a minor move toward the 23.6% Fib retracement level of the upward move from the $72.32 swing low to the $77.82 high.

The RSI is now below the 50 level and there is a short-term declining channel forming with support at $76.00. Immediate support on the downside is near the $76.50 zone.

The next major support on the WTI crude oil chart is near the $76.00 zone, below which the price could test the $75.05 level and the 50% Fib retracement level of the upward move from the $72.32 swing low to the $77.82 high.

If there is a downside break, the price might decline toward $74.50. Any more losses may perhaps open the doors for a move toward the $72.30 support zone.

If the price climbs higher again, it could face resistance near $77.05. The next major resistance is near the $77.80 level. Any more gains might send the price toward the $78.50 level.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

GBP/USD Analysis: Bulls Find Renewed Hope

This morning, UK inflation data was released, as reported by ForexFactory:

- Consumer Price Index (CPI): actual = 2.5%, expected = 2.6%, previous = 2.6%;

- Core CPI: actual = 3.2%, expected = 3.4%, previous = 3.5%.

The foreign exchange market reacted with a surge in volatility as UK inflation showed a decline.

At the same time, a technical analysis of the GBP/USD chart offers some hope for bulls following a drop of more than 9% from the peaks of September 2024 (interestingly, on 10th September 2024, we noted that bulls were facing challenges).

When analysing today’s GBP/USD price movements, we observe that at the start of 2025, the price has approached a key support zone formed by:

- the lower boundary of the descending channel (drawn in red);

- the psychological level of 1.2000;

- the significant 2023 low around the 1.2040 level.

The long lower wicks on the 4-hour candles, including today’s (highlighted with an arrow), can be interpreted as a signal of increasing demand. This could be an early sign that the pound is gaining confidence to resist the building pressure from the dollar.

Traders’ attention today will be on the release of the US CPI report (at 16:30 GMT+3), which may further support the case for strengthening bulls.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Yen Gains BoJ Hike Speculations, Sterling Steady after Inflation Data, Dollar Awaits CPI

Yen's recovery gained some momentum today on as speculation over an imminent BoJ rate hike. Governor Kazuo Ueda reinforced Deputy Governor Ryozo Himino’s earlier comments, suggesting that next week’s policy meeting could bring a shift in monetary policy. The unified tone from BoJ’s leadership is seen a calculated effort to prime markets for potential action.

Overnight index swaps now indicate a 68% probability of a BoJ rate hike in January, rising to 86% by March. Positive observations by BoJ's regional branch managers on wages growth should have bolstered the confidence in BoJ’s readiness to act.

Despite this, uncertainty still lingers as BoJ policymakers await US President-elect Donald Trump’s inauguration speech early next week, which may provide more concrete insights into his trade and economic policies.

Meanwhile, Sterling is showing little reaction to inflation data released today. UK CPI reported revealed a marked slowdown in services inflation to 4.4%, its lowest level since March 2022. This has raised speculation of a BoE rate cut at its February meeting.

However, any optimism in the UK is tempered by lingering concerns over fiscal health and rising government borrowing costs. Market sentiment could deteriorate further if Thursday’s GDP data disappoints, compounding fears of a broader economic slowdown.

Overall in currency markets, Dollar has taken a step back, consolidating last week’s gains. Risk sentiment is somewhat buoyed by the absence of firm denial from Trump regarding proposals for gradual tariffs. Additionally, traders are awaiting today’s US CPI data, which could significantly impact expectations of Fed's monetary policy over the course of 2025. For now, Dollar is the worst-performing currency this week, followed by Sterling and Swiss Franc. Conversely, New Zealand Dollar leads gains, followed by Australian Dollar and Euro. Canadian Dollar and Yen are trading in middle positions.

Technically, as Dollar is retreating, there are some support levels to pay attention to. The levels include 1.0435 resistance in EUR/USD, 1.2486 resistance in GBP/USD, 0.6301 resistance in AUD/USD and 0.9007 support in USD/CHF. As long as these levels hold, Dollar's near term bullishness should be maintained in case of deeper pull back. As for USD/JPY, however, it's likely moving on its own course based on expectations on BoJ rate hike next week.

UK CPI slows to 2.5% in Dec, services inflation down to 4.4%

UK CPI slowed from 2.6% yoy to 2.5% yoy in December, below expectation of 2.7% yoy. Core CPI slowed from 3.5% yoy to 3.2% yoy, below expectation of 3.4% yoy.

CPI goods annual rate rose from 0.4% yoy to 0.7% yoy, while CPI services annual rate fell from 5.0% yoy to 4.4% yoy.

On a monthly basis, CPI rose by 0.3% mom, below expectation of 0.4% mom.

ECB’s Lane expects service inflation to ease

ECB Chief Economist Philip Lane noted during an event today that services inflation will "come down quite a bit" in the coming months. He attributed much of the anticipated moderation to a slowdown in wage growth. Additionally, firms are reportedly experiencing reduced cost pressures, which should also contribute to easing price increases.

Lane highlighted the challenges of providing a definitive future path for interest rates, citing significant uncertainties in the global economic environment, including escalating trade tensions.

"From our point of view, saying here's where we think the future rate path is going to be conveys a sense of certainty that we don't feel," Lane said, reinforcing the ECB's cautious stance.

On the topic of exchange rates and their influence on prices, Lane pointed out that while movements in the euro-dollar exchange rate can impact European prices over time, the short-term relationship is less predictable. He noted that in the early stages of a significant currency shift, much of the impact is "absorbed by firms.

“The exchange rate, I think, over time plays a role,” Lane said. “But in terms of the month-by-month, quarter-by-quarter correlation between the exchange rate and import prices is not that stable.”

BoJ’s Ueda signals rate hike on the table next week

BoJ Governor Kazuo Ueda today provided further hints that the central bank may be considering a rate hike at its upcoming policy meeting.

Ueda noted, “We are currently analyzing data thoroughly and will compile the findings in our quarterly outlook report. Based on that, we will discuss whether to raise interest rates at next week's policy meeting and would like to reach a decision.”

Ueda emphasized the significance of Japan's wage outlook, which has recently been a key focus for policymakers. He pointed to encouraging signals from wage negotiations, which could bolster consumer spending and support BoJ's inflation target.

Additionally, Ueda remarked that the economic policies of the incoming US administration, coupled with domestic wage trends, would play a pivotal role in determining the timing of any rate adjustment.

The governor's remarks align closely with those of BoJ Deputy Governor Ryozo Himino, who earlier this week suggested that a rate hike was on the table.

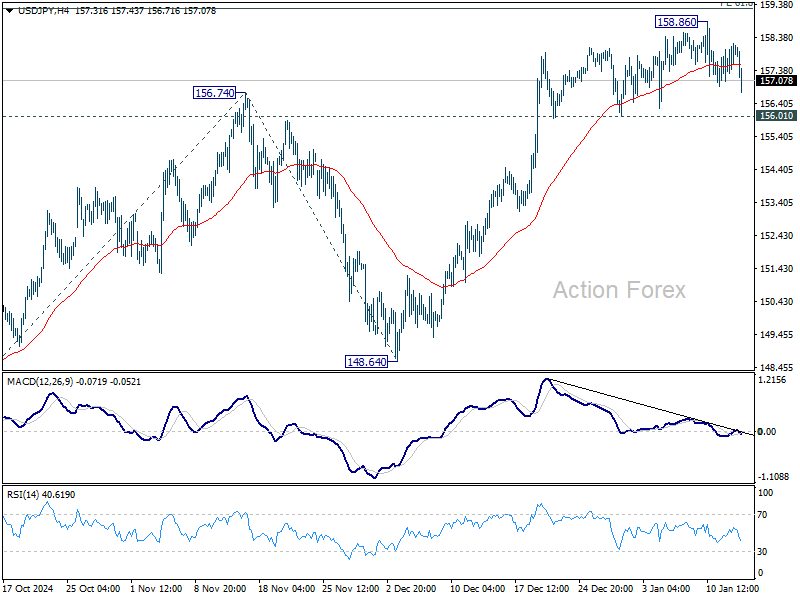

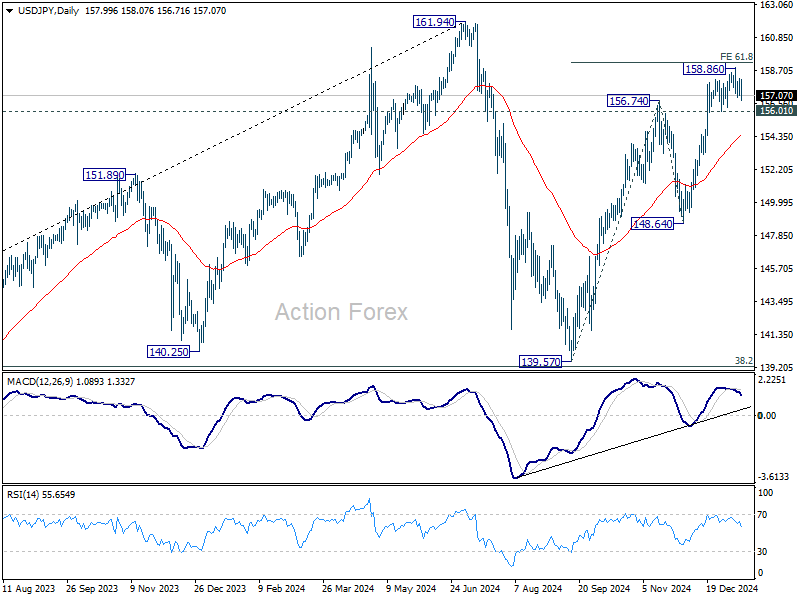

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.33; (P) 157.76; (R1) 158.41; More...

Intraday bias in USD/JPY remains neutral for the moment as sideway trading continues. Further rally is in favor as long as 156.0 support holds. On the upside, decisive break of 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25 will extend the rally from 139.57 to retest 161.94 high. However, considering bearish divergence condition in 4H MACD, firm break of 156.01 support will confirm short term topping. Intraday bias will then be back on the downside for 55 D EMA (now at 154.46) instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.33; (P) 157.76; (R1) 158.41; More...

Intraday bias in USD/JPY remains neutral for the moment as sideway trading continues. Further rally is in favor as long as 156.0 support holds. On the upside, decisive break of 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25 will extend the rally from 139.57 to retest 161.94 high. However, considering bearish divergence condition in 4H MACD, firm break of 156.01 support will confirm short term topping. Intraday bias will then be back on the downside for 55 D EMA (now at 154.46) instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

UK CPI slows to 2.5% in Dec, services inflation down to 4.4%

UK CPI slowed from 2.6% yoy to 2.5% yoy in December, below expectation of 2.7% yoy. Core CPI slowed from 3.5% yoy to 3.2% yoy, below expectation of 3.4% yoy.

CPI goods annual rate rose from 0.4% yoy to 0.7% yoy, while CPI services annual rate fell from 5.0% yoy to 4.4% yoy.

On a monthly basis, CPI rose by 0.3% mom, below expectation of 0.4% mom.

BoJ’s Ueda signals rate hike on the table next week

BoJ Governor Kazuo Ueda today provided further hints that the central bank may be considering a rate hike at its upcoming policy meeting.

Ueda noted, “We are currently analyzing data thoroughly and will compile the findings in our quarterly outlook report. Based on that, we will discuss whether to raise interest rates at next week's policy meeting and would like to reach a decision.”

Ueda emphasized the significance of Japan's wage outlook, which has recently been a key focus for policymakers. He pointed to encouraging signals from wage negotiations, which could bolster consumer spending and support BoJ's inflation target.

Additionally, Ueda remarked that the economic policies of the incoming US administration, coupled with domestic wage trends, would play a pivotal role in determining the timing of any rate adjustment.

The governor's remarks align closely with those of BoJ Deputy Governor Ryozo Himino, who earlier this week suggested that a rate hike was on the table.