Sample Category Title

Bitcoin Bulls Face Obstacles: Can They Reclaim $100K?

Key Highlights

- Bitcoin price found support at $90,000 and started a recovery wave.

- BTC cleared a declining channel with resistance at $94,800 on the 4-hour chart.

- Ethereum price is struggling to stay above the $3,000 support zone.

- Gold might continue to rise toward the $2,720 zone.

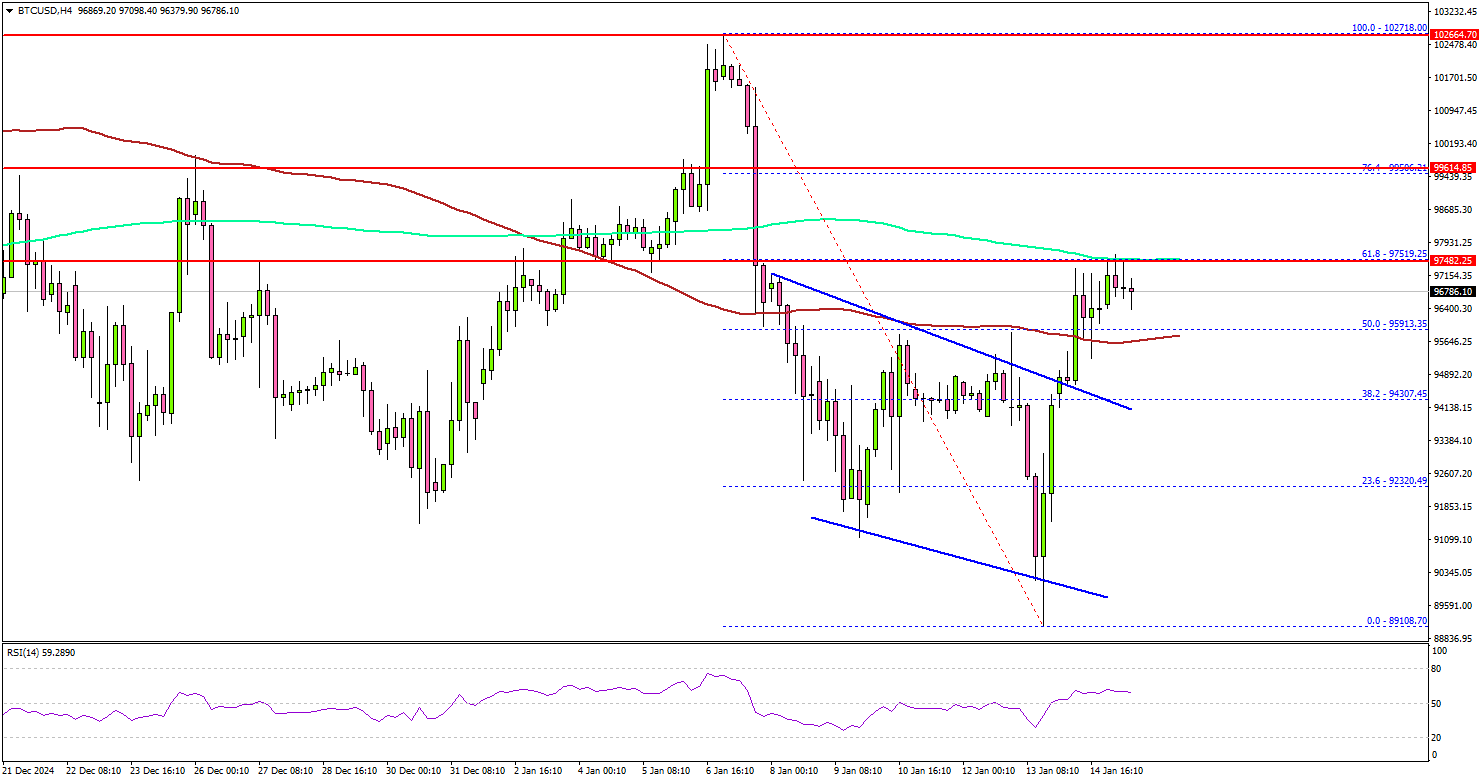

Bitcoin Price Technical Analysis

Bitcoin price found support and started a fresh recovery above $92,000. BTC/USD climbed above the $92,500 and $93,500 levels to move into a short-term bullish zone.

Looking at the 4-hour chart, the price cleared a declining channel with resistance at $94,800. There was a move above the 50% Fib retracement level of the downward move from the $102,718 swing high to the $89,108 low.

BTC even cleared the 100 simple moving average (red, 4-hour) and tested the 200 simple moving average (green, 4-hour). It faced hurdles near the $97,500 level.

The 61.8% Fib retracement level of the downward move from the $102,718 swing high to the $89,108 low acted as a resistance. On the upside, the price could face resistance near the $97,500 level. The next key resistance is $100,000.

A successful close above $100,000 might start another steady increase. In the stated case, the price may perhaps rise toward the $102,500 level.

Immediate support is near the $95,850 level. The next key support sits at $94,300. A downside break below $94,300 might send Bitcoin toward the $92,500 support. Any more losses might send the price toward the $90,000 support zone.

Looking at Ethereum, the bulls protected the $3,000 support zone and the price is now attempting a recovery wave above $3,120.

Today’s Economic Releases

- US Initial Jobless Claims - Forecast 210K, versus 201K previous.

- US Retail Sales for Dec 2024 (MoM) – Forecast +0.6%, versus +0.7% previous.

Elliott Wave View: Oil (CL_F) Impulsive Rally in Progress

Short Term Elliott Wave view in Light Crude Oil (CL_F) suggests cycle from 12.6.2024 low is in progress as an impulse. Up from 12.6.2024 low, wave ((i)) ended at 71.44. Pullback in wave ((ii)) ended at 68.42 as the 1 hour chart below shows. The instrument extends higher in wave ((iii)) with subdivision of an impulse in lesser degree. Up from wave ((ii)), wave (i) ended at 69.94 and wave (ii) ended at 68.59.

Wave (iii) higher ended at 75.29 and pullback in wave (iv) ended at 72.84. Final leg wave (v) ended at 79.27 and this completed wave ((iii)) in higher degree. From there, the instrument pullback in wave ((iv)) which ended at 77.24. Wave ((v)) higher is in progress and wave (i) of ((v)) should end soon. It should then pullback in wave (ii) to correct the rally from 77.24 low before extending higher again. Near term, as far as pivot at 68.36 low stays intact, expect pullback to find support in 3, 7, 11 swing for further upside. Once wave ((v)) is complete, the instrument should correct cycle from 12.6.2024 low in 3, 7, or 11 swing before it turns higher again.

Oil (CL_F) 60 Minutes Elliott Wave Chart

CL_F Elliott Wave Video

https://www.youtube.com/watch?v=wKGzJoQRng8

Fed’s Williams highlights uncertainty tied to fiscal, trade, and regulatory Policies

New York Fed President John Williams said today that monetary policy remains "well-positioned" to balance Fed’s dual mandate of stable prices and maximum employment. He noted that the process of disinflation is expected to persist, though achieving the 2% target may take time, with a return to the goal likely “in the coming years.” The pace and direction of monetary policy, however, remain highly data-dependent

Williams highlighted significant uncertainties clouding the economic outlook, including risks related to fiscal policies, trade dynamics, immigration changes, and regulatory shifts.

Therefore, "our decisions on future monetary policy actions will continue to be based on the totality of the data, the evolution of the economic outlook, and the risks to achieving our dual mandate goals," he added.

Separately, Richmond Fed President Thomas Barkin commented on the December CPI report released today, acknowledging that it reinforces the narrative of inflation gradually declining toward Fed’s target. Barkin also downplayed the potential impact of rising 10-year Treasury yields on the Fed’s monetary policy stance.

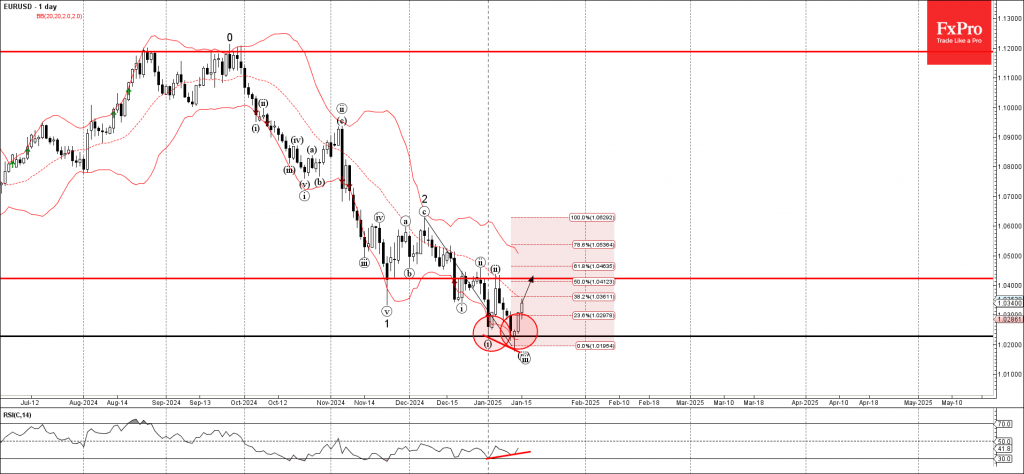

EURUSD Wave Analysis

- EURUSD reversed from key support level 1.0225

- Likely to rise to resistance level 1.0425

EURUSD currency pair recently reversed up with the daily Japanese candlesticks reversal pattern Morning Star (with the daily Hammer in its middle) from the key support level 1.0225, which stopped the previous impulse wave i at the end of December.

The upward reversal from the support level 1.0225 started the active short-term correction iv, which belongs to the downward impulse wave 3 from last month.

Given the bullish divergence on the daily RSI indicator, EURUSD currency pair can be expected to rise to the next resistance level 1.0425, which stopped the previous waves ii and (ii).

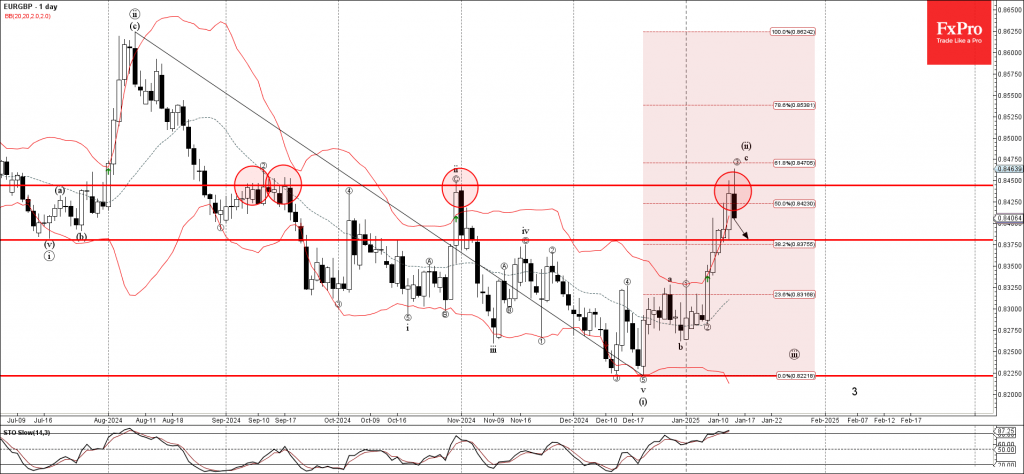

EURGBP Wave Analysis

- EURGBP reversed from multi-month resistance level 0.8445

- Likely to fall to support level 0.8380

EURGBP currency pair recently reversed down from the strong multi-month resistance level 0.8445, which has been steadily reversing the price from the start of September, as can be seen below.

The resistance level 0.8445 was further strengthened by the upper daily Bollinger Band and by the nearby 61.8% Fibonacci correction of the downtrend from the start of August.

Given the overbought daily Stochastic, EURGBP currency pair can be expected to fall to the next support level 0.8380.

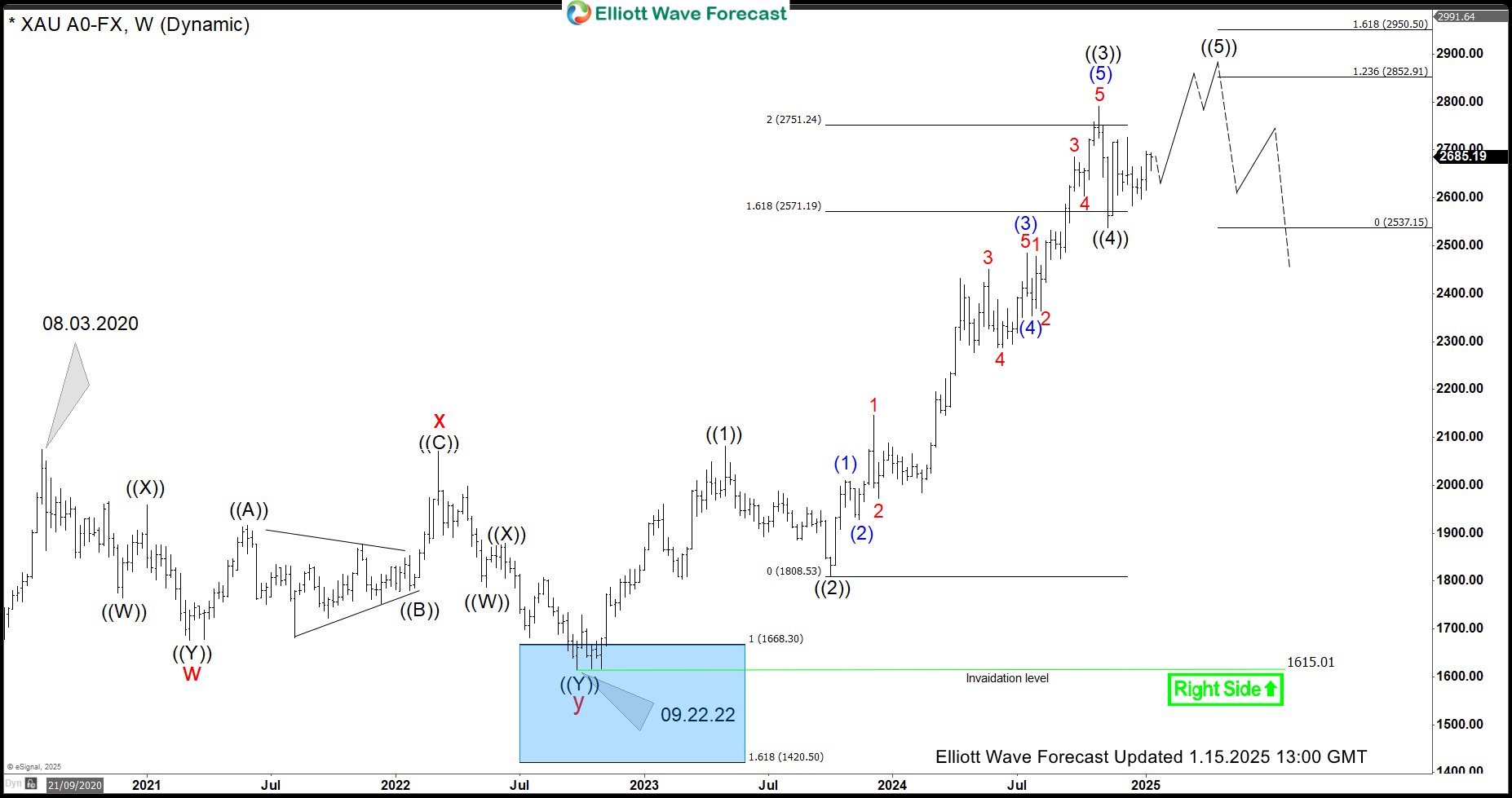

Gold Cycle Since September 2022 Low Calling For More Upside

More than two years back, we were calling Gold to end a Zigzag Elliott Wave correction in the blue box area and resume the rally. Zigzag is a 5-3-5 Elliott wave structure in which wave A and C are in 5 waves and wave B is in 3 waves. Blue Boxes are High-Frequency areas and are based in a relationship of sequences, cycles and calculated using Fibonacci extensions. We refer to them as High Frequency trading areas, mainly because at Blue Boxes majority of the times, both buyers and sellers agree in the direction of the next moves and, hence why they present high probability and low-risk opportunities to enter the market in the direction of the trend. Let’s take a look at the weekly Elliott wave chart of Gold from September 2022.

Gold Weekly Chart September 2022

Gold cycle from 2015 low ended at $2075.14 on 08.03.2020 high. Following this peak, $XAUUSD started a pullback which lasted more than two years. Back in September 2022 (as shown in the chart above), we expected the yellow metal pullback to complete in the blue box area between $1668.46 – $1420.66 and rally to resume for a new high above 08.03.2020 high or for a three waves reaction higher at least. $1420.66 being the 161.8% Fibonacci extension of (( A )) related to (( B )) was the invalidation level which we expected to hold.

Gold Weekly Chart January 2025

Gold buyers indeed appeared in the blue box as expected and it started a rally which has lasted 27 months but is still not over yet. Blue box low was seen on 09.22.2022 at $1615.01 and since then we see Gold rally to be in fifteen (15) swings. Gold made a new all-time high, rally is extended as third wave went past 161.8 Fibonacci extension of wave (( 1 )) related to wave ((2)) but we still expect more upside because fifteen (15) is part of a corrective sequence and we need at least 1 more high to make it seventeen (17) swings and hence complete the cycle since 09.22.2022 low. As dips hold above wave (( 4 )) low at $2536.89, we are expecting more upside in Gold toward $2852.91 – $2950.50 area to complete wave ((5)). Following this, there should be a larger 3 waves pull back to correct the cycle from 09.22.2022 low. In the unlikely event of a break below $2536.89, Gold should still be in wave ((4)) and can see a test of $2474.41 – $2318.80 area before it turns higher in wave ((5)).

Bitcoin (BTC/USD) vs. Nasdaq: Is the Correlation Affecting Crypto Outflows?

- Bitcoin has recovered from a sharp selloff earlier in the week, rising from around 89000 to nearly 98500 post CPI.

- ETF flow data shows three consecutive days of net outflows for Bitcoin as correlation with Nasdaq grows.

- Could a Trump Presidency lead to significant capital inflow into Bitcoin in 2025?

- Technically, Bitcoin is at a critical juncture breaking the 50-day moving average and eyeing the 100k handle.

Bitcoin has staged an impressive recovery since Monday afternoon lows around the 89000 mark. Cryptocurrencies were also affected by US jobs data ahead of the weekend and the stronger US Dollar early on Monday was in part responsible for the sharp selloff.

The recovery has been swift however with Bitcoin rising from a Monday low of around 89000 to end the day just shy of the 95000 handle. Yesterday the worlds largest Crypto by market cap edged above the key 95000 handle to trade at a high of 97339 (helped by softer than expected US PPI data) before facing some resistance by the 50-day MA.

Let us take a look at the performance of the Crypto market for the day.

Crypto Heatmap (post CPI), January 15, 2025

Source: TradingView (click to enlarge)

ETF Flow Data Shows 3 Successive Days of Outflows

Looking at ETF flow data courtesy of Farside investors, Bitcoin has recorded three consecutive days of net outflows with the largest being on Monday. Bitcoin started the week recording $284.1m of net outflows and followed that up with outflows totaling $209.8m yesterday.

It will be interesting to gauge whether ETF flows turn positive again ahead of the Trump inauguration next week.

Source: Farside Investors (click to enlarge)

There could be a host of reasons for this but one which has gained traction this week stems from a report showing the increase in correlation between US indices (particularly Nas100) and Bitcoin.

K33 Research Report – Nasdaq vs Bitcoin Correlation

K33 Research’s latest “Ahead of the Curve” report highlights that the crypto market is facing the same challenges affecting global markets. Over the past month, Bitcoin (BTC) and the Nasdaq have become more closely linked, with their current 30-day connection reaching its highest point in 2024.

According to K33’s analyst, Trump is expected to push for policies that grow the economy, extend the 2017 tax cuts, and provide more tax breaks for working-class Americans. These actions could be positive for riskier investments like crypto. The analyst also noted that Trump is likely to introduce crypto-friendly policies, which could benefit the crypto market.

Such data may be contributing to ETF outflows as institutional investors looked at Bitcoin as a sort of portfolio hedge providing diversification. However if the correlation with US stocks continues this could result in allocations for equities and Bitcoin being split rather than having their own allocations.

In an interview with Bloomberg on Tuesday, VanEck’s CEO, Jan van Eck stated that ‘it is disappointing to note the correlation between Bitcoin and Nasdaq over the past 6 months. Mr van Eck went further by saying that many people are looking at Bitcoin for the first time which is not what you want (referring to the growing correlation). If you look at the ten-year correlations, they are almost zero, which is really what diversification should be. We’ll have to see how Bitcoin performs going forward.’

Such comments tend to support the idea that the higher the correlation between the Nasdaq and Bitcoin, the greater the chance that outflows may increase due to portfolio diversification and positioning.

Trump Inauguration to Fuel Crypto Rally?

As you can see from the K33 research report above, there is optimism that a Trump Presidency will provide a major boost to the crypto industry.

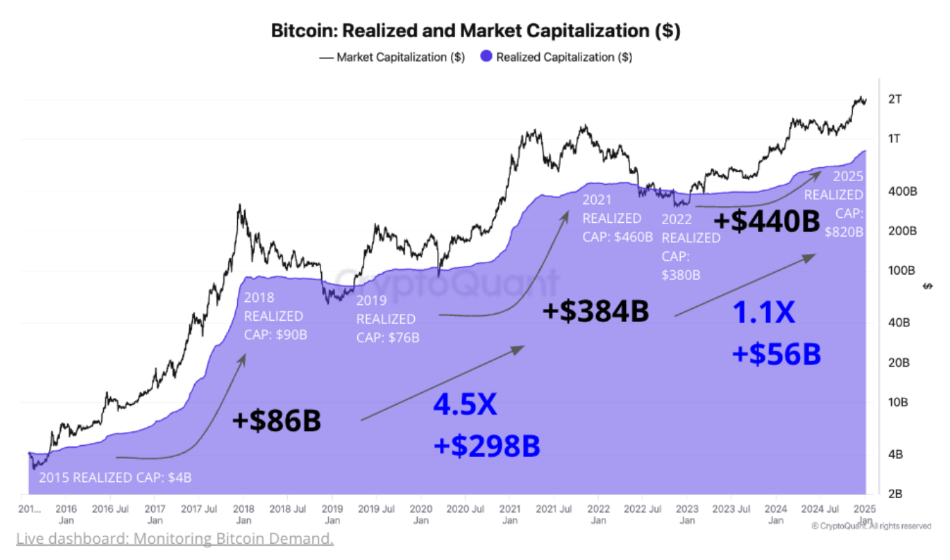

According to CryptoQuant, About $520 billion of fresh capital could flow into Bitcoin in 2025. In the context of favorable regulatory, monetary and cyclical conditions, it’s reasonable to expect capital to continue flowing into Bitcoin in 2025 the data and analytics provider added.

The idea of a bullish run in 2025 for crypto is further supported by Pantera Capital, who claims that the upcoming inauguration of Donald Trump should propel Bitcoin to new heights.

Another interesting one to keep an eye on as inauguration day draws closer.

Bitcoin realized cap data

Source: CryptoQuant (click to enlarge)

An accompanying chart (above) shows Bitcoin’s realized market cap with the combined value of the supply as it moves on chain since 2015. If the market follows historical patterns, CryptoQuant said, the $520 billion tally becomes attainable. Such a move would no doubt fuel rallies in price but leaves one with many questions.

US Data Could Temporarily Drive Bitcoins Price

US inflation data came out a short while ago with the Core inflation print YoY softer than expected. It will be interesting to see if this helps propel Bitcoin toward the 100000 mark and beyond.

Technical Analysis – BTC/USD Rests at Critical Juncture

Bitcoin (BTC/USD) from a technical standpoint on the daily timeframe the overall price action has been messy.

The reason for my observation stems from the lack of a convincing break of the previous swing low around 91800.

Though prices plunged below $90000 handle for a moment on Monday the swiftness with which prices rose suggest strong buying pressure remains in play.

As things stand, BTC/USD is a critical juncture as it tests 50-day MA which could serve to cap gains.

A failure to break back above and find acceptance could lead to a sharper selloff.

A rejection of this level brings the 95000 and 90000 into play, before attention turns to the 91804 and 90000 handle.

Bitcoin (BTC/USD) Daily Chart, January 15, 2025

Source: TradingView.com (click to enlarge)

Support

- 97500

- 95000

- 91804

Resistance

- 100000

- 102261

- 103647

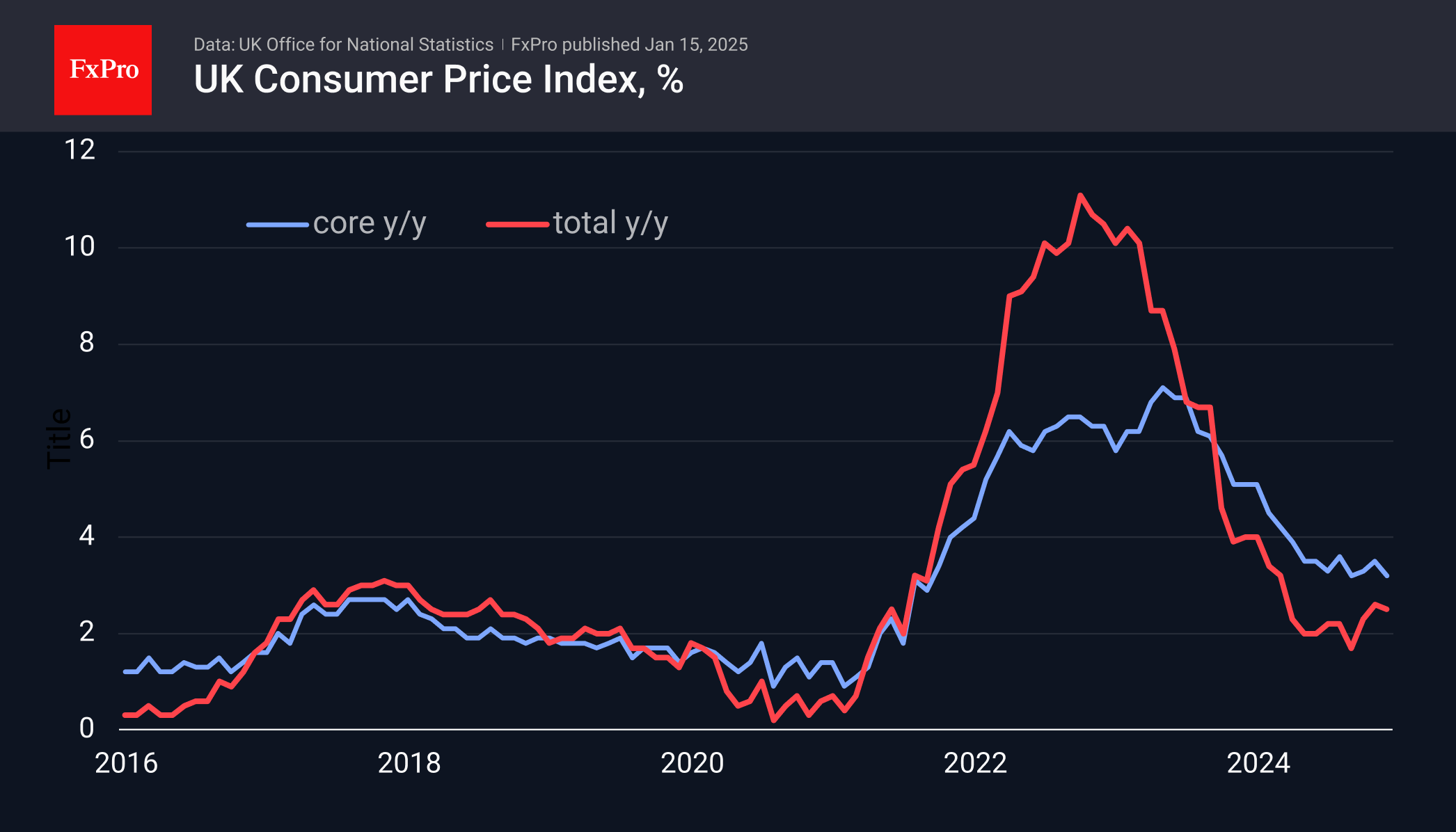

UK Inflation: Below Expectations But Above Target

The UK Consumer Price Index (CPI) added 0.3% m/m in December, slightly below the average expectation of 0.4%. Annual inflation eased to 2.5%, having remained mostly in the 2.0-2.5% range for the past nine months. This is quite a long period without a significant decline and with some upward bias.

Core consumer inflation was 3.2% y/y in December, having remained in the 3.2-3.5% range for the past eight months. This figure is well above the 2% target and without a clear downward trend. As a higher reading was expected, the report probably stirred the bears, but did not allow them to play up to their full potential due to US inflation expectations.

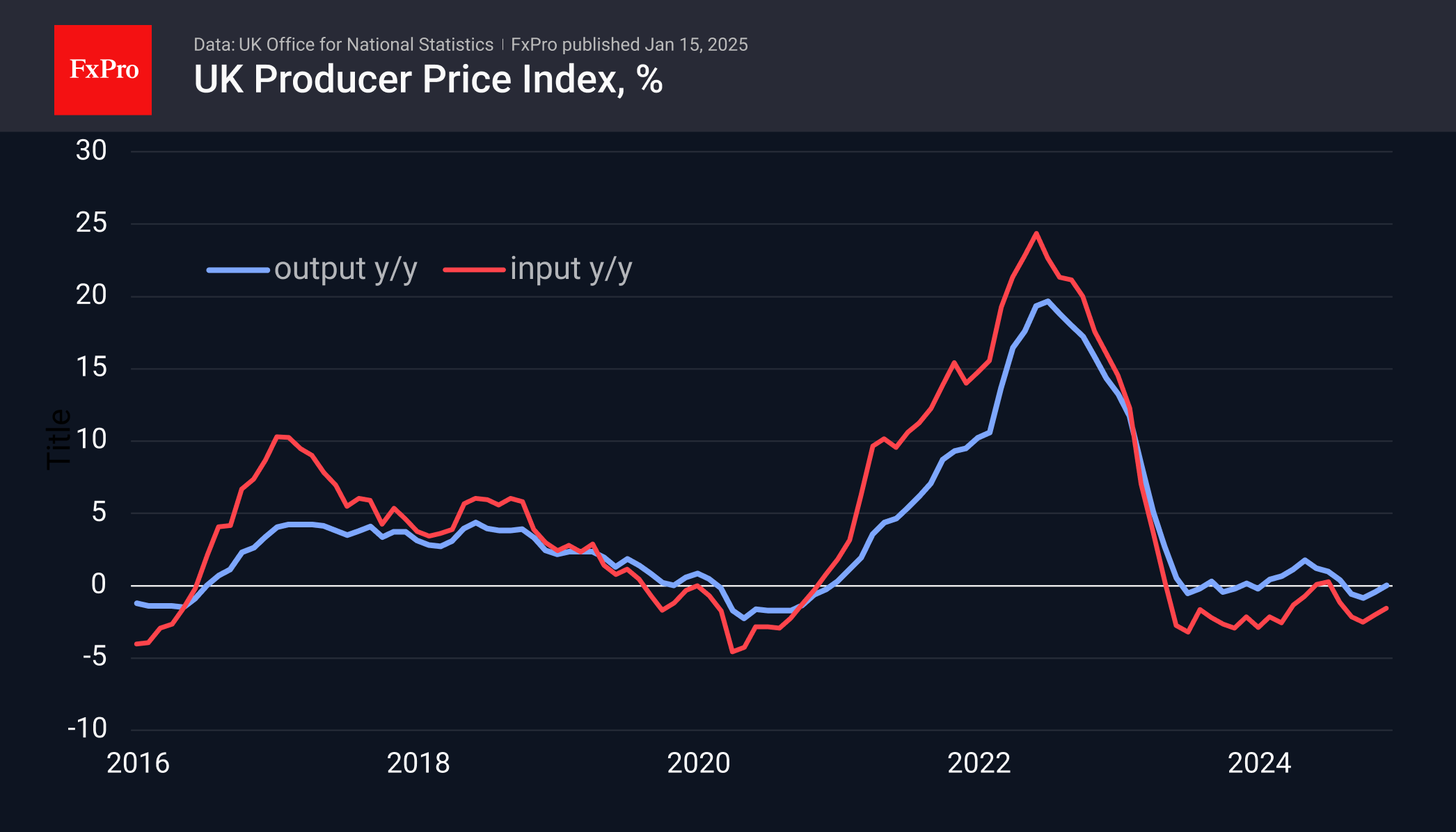

Input producer prices have barely been out of negative territory for the past year and a half, recording the latest data at -1.5% y/y. Producer prices ‘on the way out’ have shown near-zero momentum for the past 18 months, hitting 0.0% y/y in December.

Producer prices work to suppress inflation, while the rising cost of services raises the final price tag for consumers, suppressing their activity. The Bank of England is likely to use the weakness in producer prices and low economic activity as an excuse to cut rates. However, this support for the economy has its own negative effect in the form of higher inflation expectations. If inflation picks up again, rates will need to be raised for longer and more aggressively than they were when expectations were anchored at 2.0%.

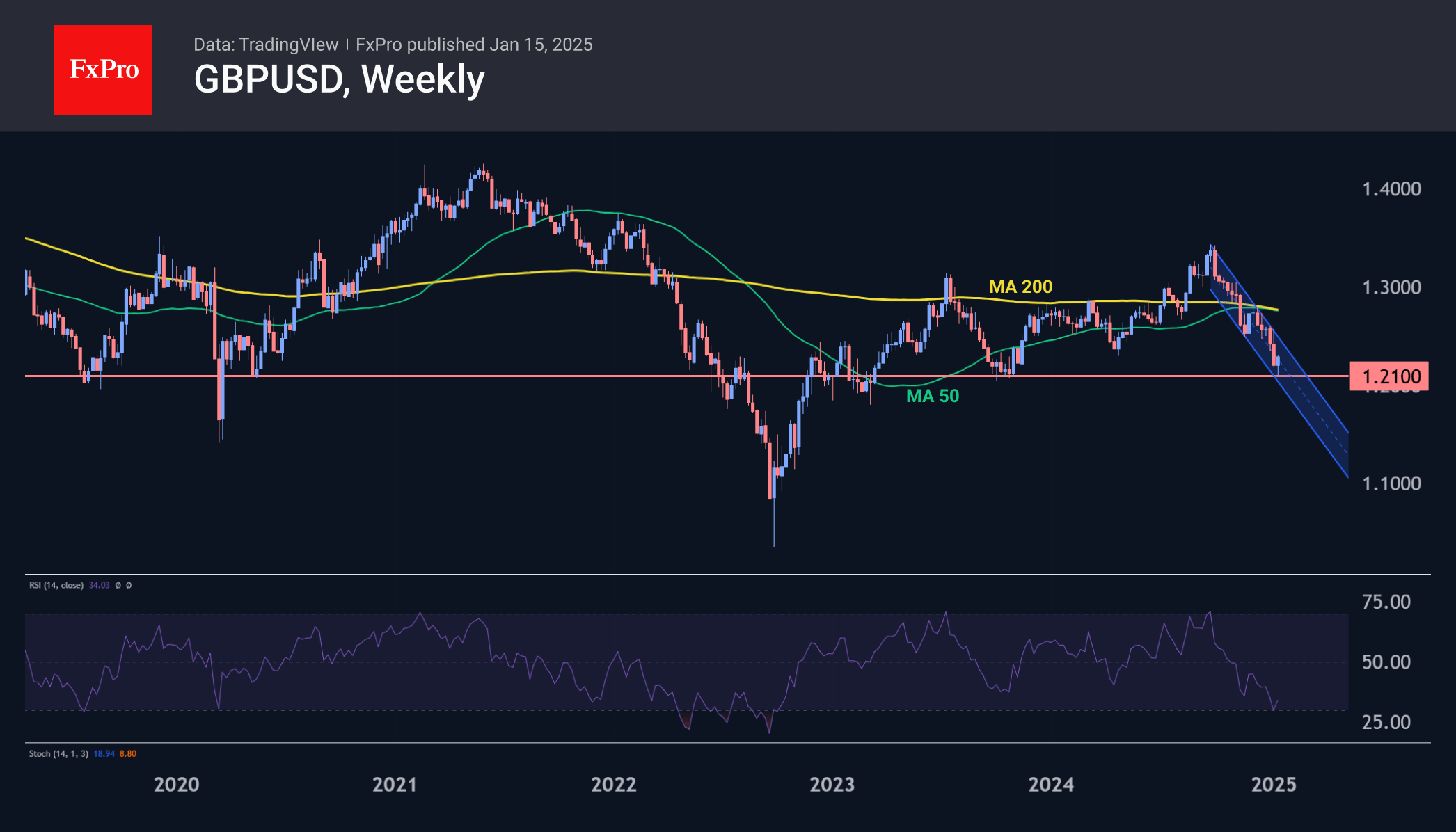

GBPUSD has been hovering around the 1.22 level for the fifth trading session, finding solid buying on dips towards 1.21. This local bottom roughly coincides with the 2023 year-end pivot area, which further fuels bullish hopes. Short-term, they have the accumulated oversold pound on their side after a 5.5% failure in the last five weeks. The start of growth of GBP/USD is well within the framework of technical correction with the potential of increase up to the area of 1.24-1.26. And only a confident exit to higher levels will allow us to speak about a global reversal in this pair.

December CPI: Hotter Headline, But Healthier Core

Summary

Consumer price inflation was hot in December, rising 0.4% in the month on the back of higher food and energy prices. Excluding food and energy, the inflation picture looked better. The core CPI rose 0.23%, in line with economist forecasts and marking a slowdown from the pace that had prevailed over the previous few months. Fairly flat prices for core goods and slower inflation for items like medical care helped to push core CPI down to 0.2% from its recent run rate of 0.3%.

That said, when looking through the month-to-month noise, the inflation data have been fairly stubborn in recent months, neither gathering nor losing speed. The 12-month change in the core CPI (+3.2%) is more or less the same as the three-month annualized rate (3.3%). The picture looks a bit better for the Fed's preferred inflation metric, the core PCE deflator, where we project December inflation to be 0.2% month-over-month and 2.8% year-over-year. But, this marks only a modest slowdown relative to the 3.0% core PCE inflation registered in December 2023, and it is still well above the central bank's 2% inflation target.

Accordingly, and given the more resilient labor market data seen over the past couple months, we have revised our expectations for the federal funds rate outlook. We now expect two 25 bps rate cuts by the FOMC this year, in September and December, down from the three cuts we anticipated coming into the year. If realized, the target range for the federal funds rate would be 3.75%-4.00% at year-end 2025. We will publish additional details and a full economic forecast update tomorrow in our flagship Monthly Economic Outlook publication.

More Work To Do in 2025

The Consumer Price Index finished 2024 in hot territory, rising 0.4% in December and roughly matching the largest monthly increase of the year. Higher gasoline prices (+4.4%) and food prices (+0.3%) contributed to the robust gain in the headline index. Despite the strong reading for food and energy prices in December, inflation in these categories was relatively subdued over the entirety of 2024 (chart). Gasoline prices were 3.4% lower in December 2024 compared to 2023, while food prices were up 2.5%, a smaller gain the 3.9% increase in average hourly earnings. Note that this masks some divergences beneath the surface for individual categories. As an example, prices for eggs at the grocery store rose 3.2% in December and 37% over the past year amid a bird flu epidemic outbreak that has constrained supply. Total CPI inflation was 2.9% in the 12-months ending in December, a modest improvement from the 3.4% rate registered in December 2023 and consistent with a moderate pace of real wage gains.

Excluding food and energy, there was slightly better news on the price front. After advancing 0.3% in each of the prior four months, the core index rose 0.23%. As expected, the tamer reading was driven by a more modest rise in core goods prices, which were up 0.1%. New and used vehicle prices continued to rise in December, but at a slower rate than in November, while prices for the remainder of the core goods index fell 0.2%.

Core services prices increased 0.3%—in line with November. Primary rent growth (owners' equivalent rent and primary rent) reverted to its recent trend of 0.3% after slowing sharply in November. But excluding housing, core services advanced 0.2% amid more modest gains in medical care and other services like recreation, tuition and personal care.

Today's CPI report along with yesterday's December Producer Price Index suggest the core PCE deflator, the Fed's preferred measure to gauge the current trend in inflation, rose 0.21% in the final month of the year. That would leave the year-over-year rate at 2.8%, only marginally better than the 3.0% change registered in December 2023. The core CPI, however, has seen more improvement, moving from 3.9% to 3.2%, thanks to the moderation in primary shelter and auto inflation. Similarly, the market-based measure of core PCE also has pointed to a more meaningful slowdown in price growth over the past year (chart). This measure excludes categories where prices are imputed and not directly observed, and has been mentioned by Fed officials including Chair Powell with increasing frequency.

Nevertheless, progress in the fight against inflation has seemed to effectively stall in recent months. Over the past three months, the core CPI has risen at an annualized rate of 3.3%, little different than the 6-month and 12-month rates of 3.2%. The sideways move in core inflation in recent months comes as deflation in core goods has faded since the summer and offset the frustratingly slow pace of services disinflation (chart).

The stubborn inflation readings over the past few months, alongside the stabilization in the labor market data, have led us to revise our expectations for the federal funds rate this year. We now expect two 25 bps rate cuts this year, in September and December, down from the three cuts we anticipated coming into this year. If realized, the target range for the federal funds rate would be 3.75%-4.00% at year-end 2025. We will publish additional details and a full economic forecast update tomorrow in our flagship Monthly Economic Outlook publication.