Sample Category Title

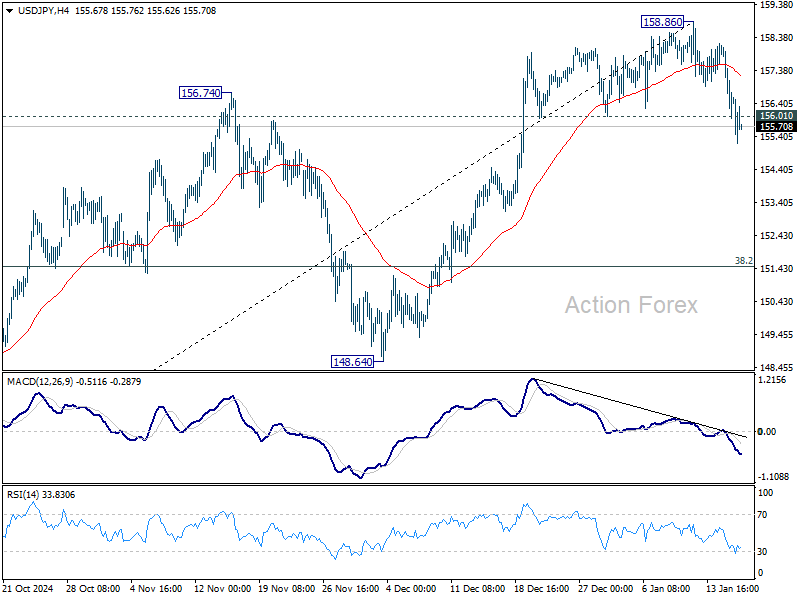

USD/JPY Hits One-Month Low

The USD/JPY pair fell to its lowest level in a month during today’s Asian session, dropping below 155.5 yen per US dollar for the first time since 19th December.

As Reuters reports:

→ The yen’s strengthening was driven by hawkish comments from Bank of Japan (BOJ) Governor Kazuo Ueda, which prompted markets to bet on a potential interest rate hike next week.

→ A significant majority of surveyed economists anticipate the BOJ will raise rates at one of its two meetings this quarter, with most favouring a January hike.

The BOJ’s decision on rates may depend on market stability following Donald Trump’s return to the White House next Monday. His inauguration speech will be closely watched by policymakers worldwide to gauge his likely political direction.

Technical analysis of the USD/JPY chart shows:

→ The price has struggled to hold above the 158 yen-per-dollar level, which can be considered a critical barrier where bulls are unwilling to take on the risk associated with potential rate hikes.

→ The 157 level has been broken, transitioning from support to resistance (as indicated by the arrows).

Bulls might find support at the lower boundary of the ascending channel (marked in blue), which has been in place since November last year. However, given strong fundamental factors, such as the US presidential inauguration and BOJ rate decisions, USD/JPY is likely to experience spikes in volatility that could significantly shift the supply-demand balance—not just in the short term.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

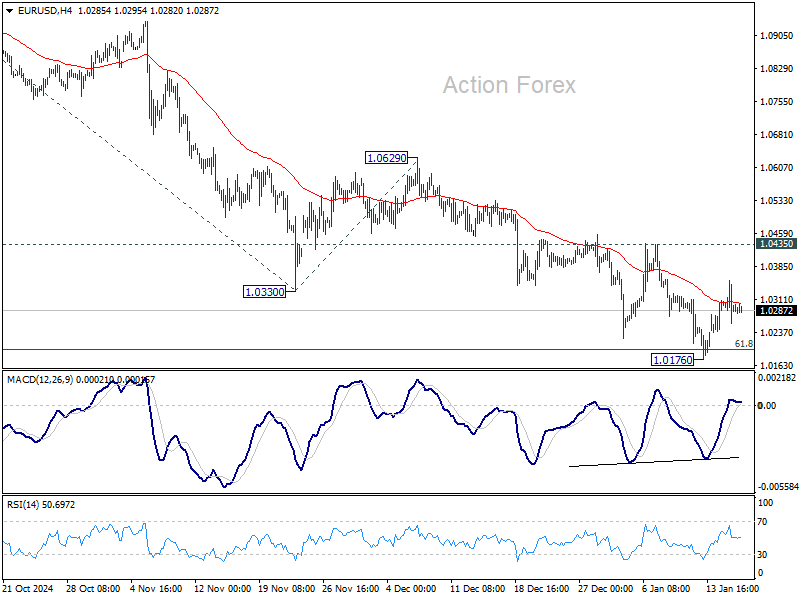

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0248; (P) 1.0302; (R1) 1.0344; More...

Intraday bias in EUR/USD remains neutral as consolidation continues above 1.0176. Further decline is still expected with 1.0435 resistance intact. On the downside, break of 1.0176 will resume the fall from 1.1213 and target 61.8% projection of 1.1213 to 1.0330 from 1.0629 at 1.0083. However, considering bullish convergence condition in 4H MACD, firm break of 1.0435 will confirm short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.

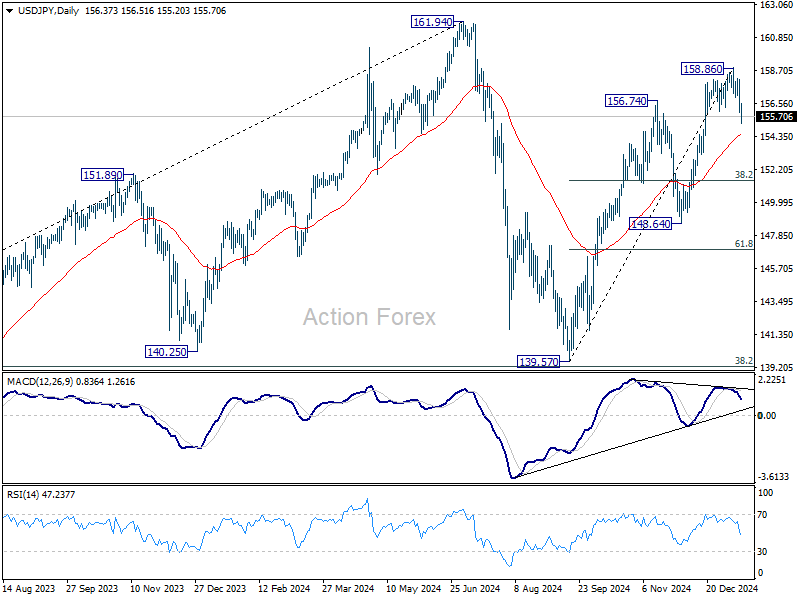

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.56; (P) 156.85; (R1) 157.75; More...

USD/JPY's break of 156.01 support indicates short term topping at 158.86, on bearish divergence condition in 4H MACD. Intraday bias is back on the downside for 55 D EMA (now at 154.44). Firm break there will target 38.2% retracement of 139.57 to 158.86 at 151.49 next. For now, risk will stay on the downside as long as 158.86 resistance holds, in case of recovery.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

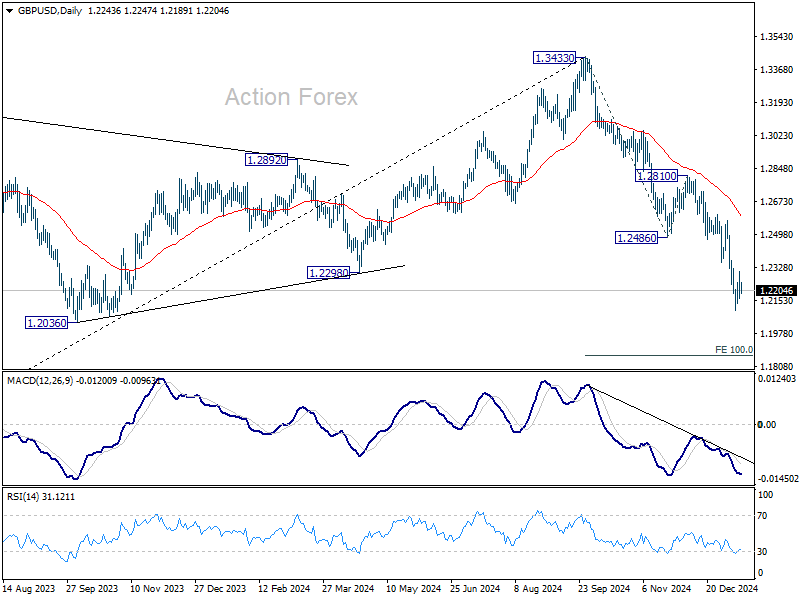

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2176; (P) 1.2242; (R1) 1.2310; More...

GBP/USD is staying in consolidation above 1.2099 and intraday bias remains neutral. Outlook remains bearish with 1.2486 support turned resistance intact. Larger fall from 1.3433 is still expected to continue. On the downside, break of 1.2099 will resume the decline to 100% projection of 1.3433 to 1.2486 from 1.2810 at 1.1863.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433, and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move.

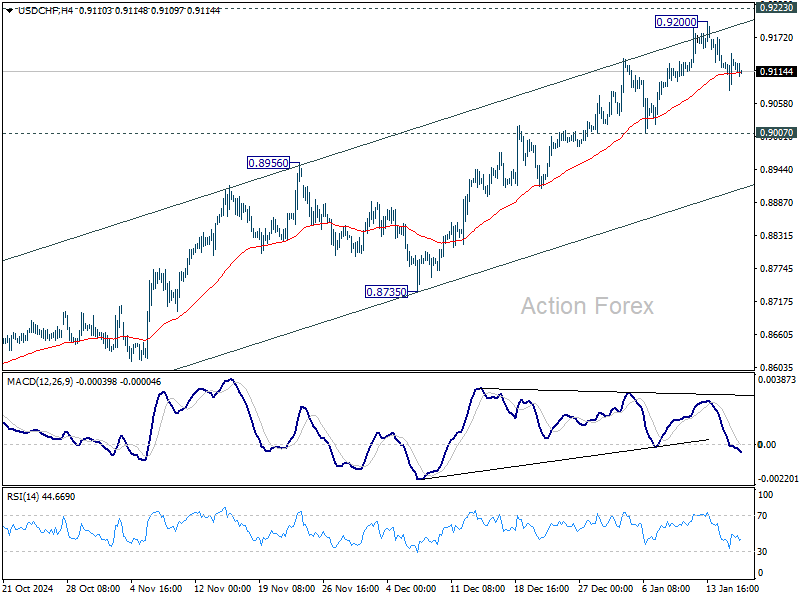

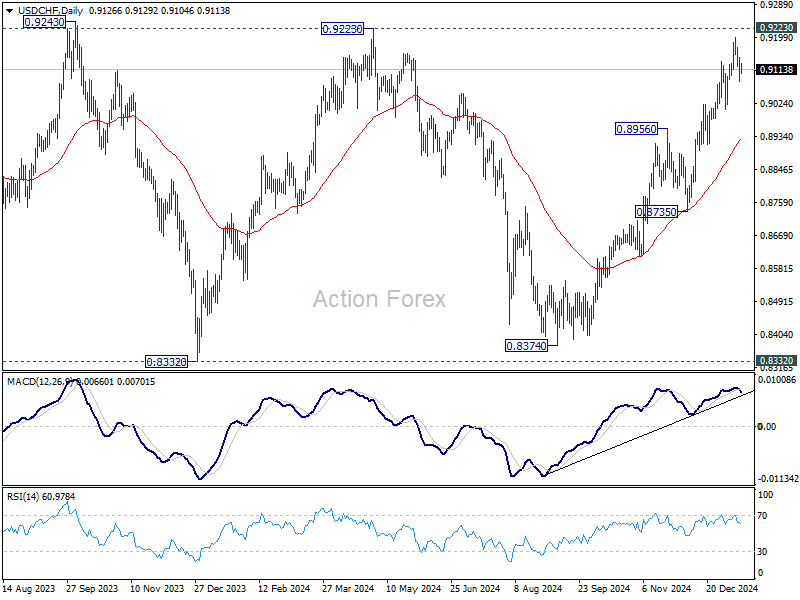

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9090; (P) 0.9122; (R1) 0.9158; More…

USD/CHF is staying in consolidation below 0.9200 and intraday bias stays neutral. As long as 0.9007 support holds, near term outlook remains bullish. On the upside, decisive break of 0.9223 will carry larger bullish implications. However, break of 0.9007 will confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 0.8930).

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes. However, decisive break of 0.9223 will be an important sign of bullish trend reversal.

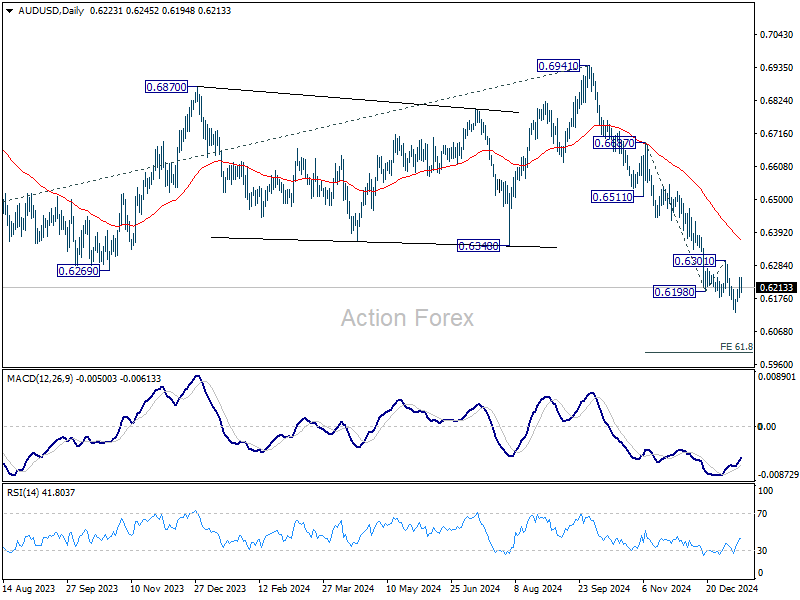

AUD/USD Daily Report

Daily Pivots: (S1) 0.6190; (P) 0.6218; (R1) 0.6256; More...

AUD/USD is staying in consolidation above 0.6130 and intraday bias remains neutral. Further decline is expected as long as 0.6310 resistance holds. Break of 0.6130 will resume the fall from 0.6941 to 61.8% projection of 0.6687 to 0.6198 from 0.6301 at 0.5999. However, considering bullish convergence condition in 4H MACD, break of 0.6310 will indicate short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, down trend from 0.8006 (2021 high) is resuming with break of 0.6169 (2022 low). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806, In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6587) holds.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4306; (P) 1.4336; (R1) 1.4371; More...

No change in USD/CAD's outlook as consolidation continues below 1.4466. Intraday bias remains neutral for the moment. Break of 1.4279 support will bring deeper correction. But downside should be contained by 55 D EMA (now at 1.4179) to bring rebound. On the upside, break of 1.4466 will resume larger up trend to 1.4667/89 long term resistance zone.

In the bigger picture, up trend from 1.2005 (2021) is in progress for retesting 1.4667/89 key resistance zone (2020/2015 highs). Medium term outlook will remain bullish as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.

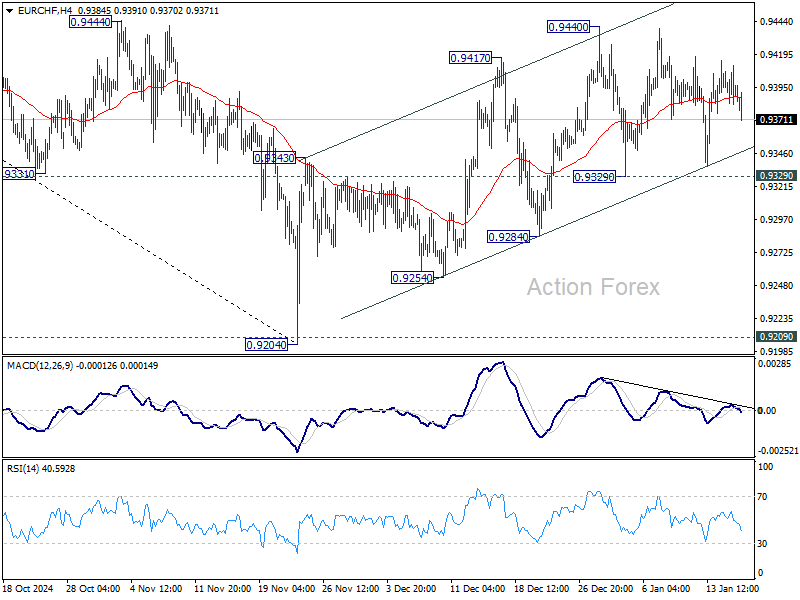

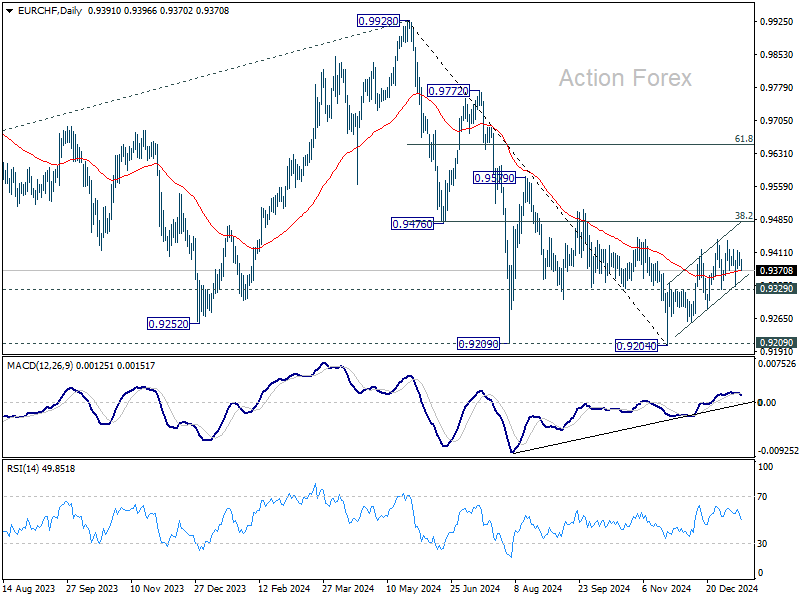

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9377; (P) 0.9398; (R1) 0.9412; More....

Intraday bias in EUR/CHF remains neutral and range trading continues. Corrective rebound from 0.9204 could still extend higher. But upside should be limited by 0.9481 fibonacci resistance. On the downside, firm break of 0.9329 support will argue that the correction has completed, and turn bias back to the downside for 0.9284 support first.

In the bigger picture, while corrective rebound from 0.9204 might extend higher, strong resistance could be seen from 38.2% retracement of 0.9928 to 0.9204 at 0.9481 to limit upside. Down trend from 0.9928 (2024 high) is still in favor to resume through 0.9204/9 support zone at a later stage.

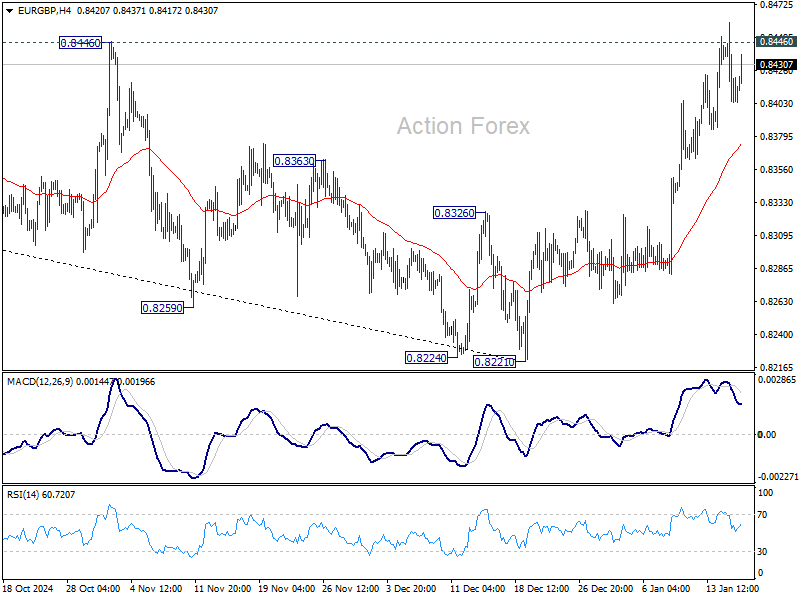

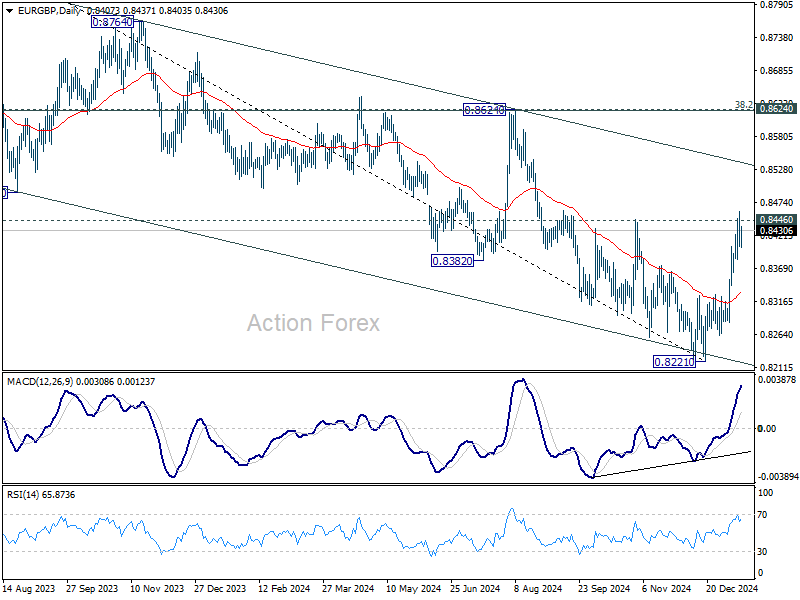

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8388; (P) 0.8420; (R1) 0.8436; More...

Intraday bias in EUR/GBP is turned neutral first with the current retreat and with 4H MACD crossed below signal line. Some consolidations would be seen, but further rally is expected as long as 55 4H EMA (now at 0.8374) holds. Firm break of 0.8446 resistance will target 0.8624 cluster resistance zone, even as a corrective move.

In the bigger picture, considering bullish convergence condition in D MACD, decisive break of 0.8446 resistance and 55 D EMA (now at 0.8446) should confirm medium term bottoming at 0.8221, just ahead of 0.8201 key support (2022 low). Further rally should be seen towards 0.8624 key resistance, even as a correction to the down trend from 0.9267 (2022 high). Overall, however, medium term outlook will be neutral at best until decisive break of 0.8624 cluster zone (38.2% retracement of 0.9267 to 0.8221 at 0.8621). Risk will stay on the downside even in case of strong rebound.

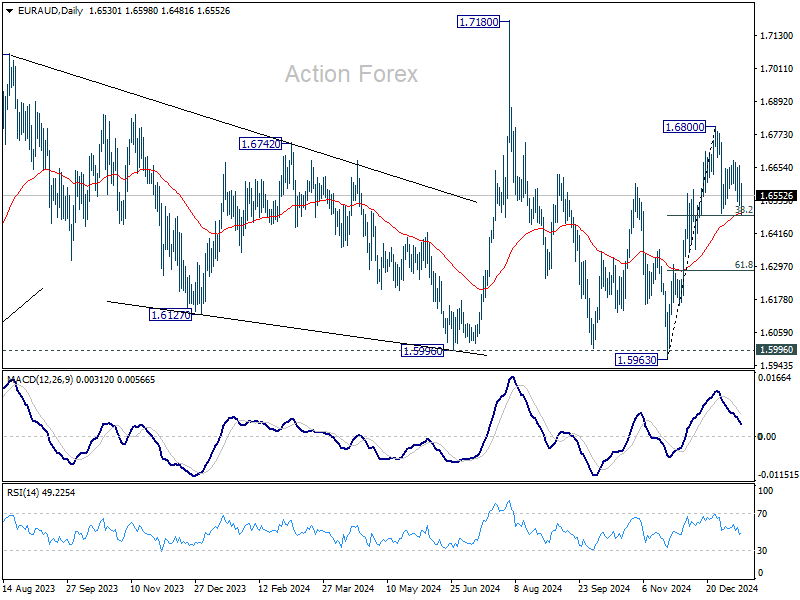

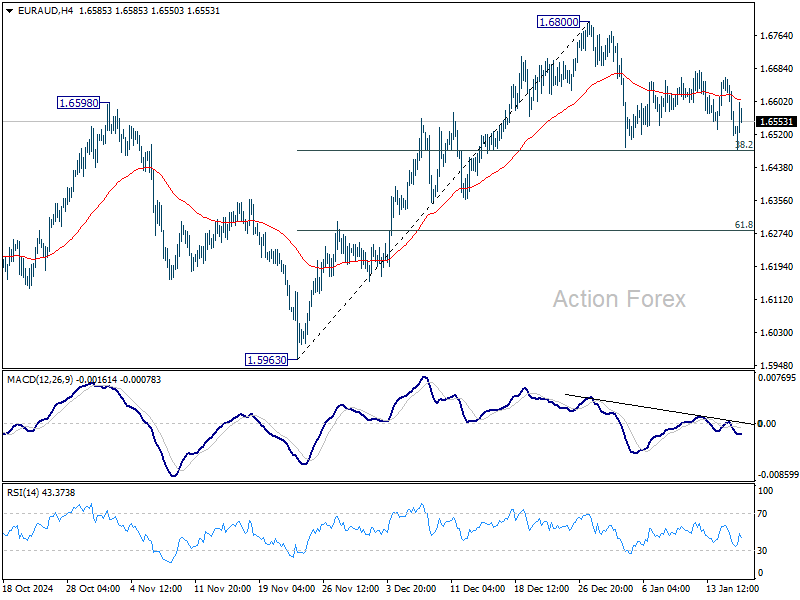

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6475; (P) 1.6570; (R1) 1.6620; More...

No change in EUR/AUD's outlook as consolidation continues below 1.6800. Strong support is still expected from 38.2% retracement of 1.5963 to 1.6800 at 1.6480 to contain downside. Firm break of 1.6800 will resume the rally from 1.5963. However, sustained break of 1.6480 will bring deeper correction 61.8% retracement at 1.6283.

In the bigger picture, EUR/AUD is holding on to 1.5996 key support despite brief breach. Larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5995 will indicate that such up trend has completed and deeper decline would be seen.