Sample Category Title

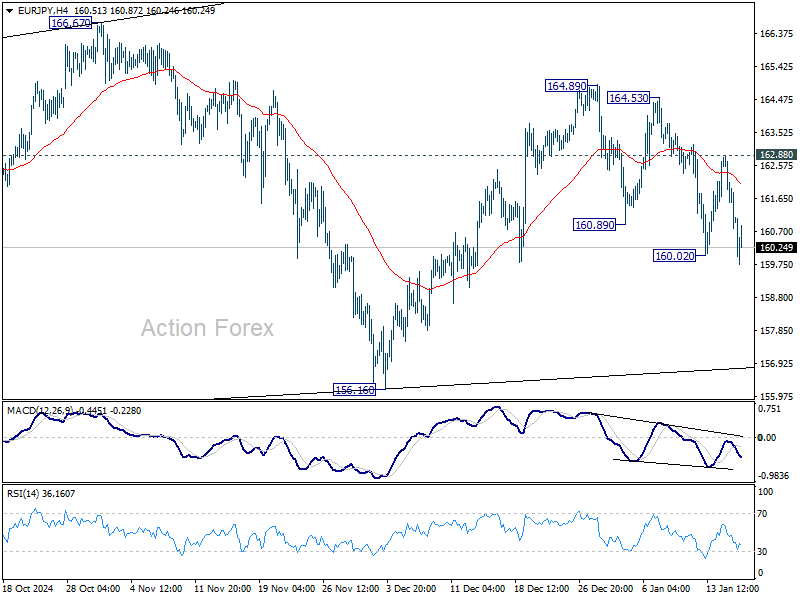

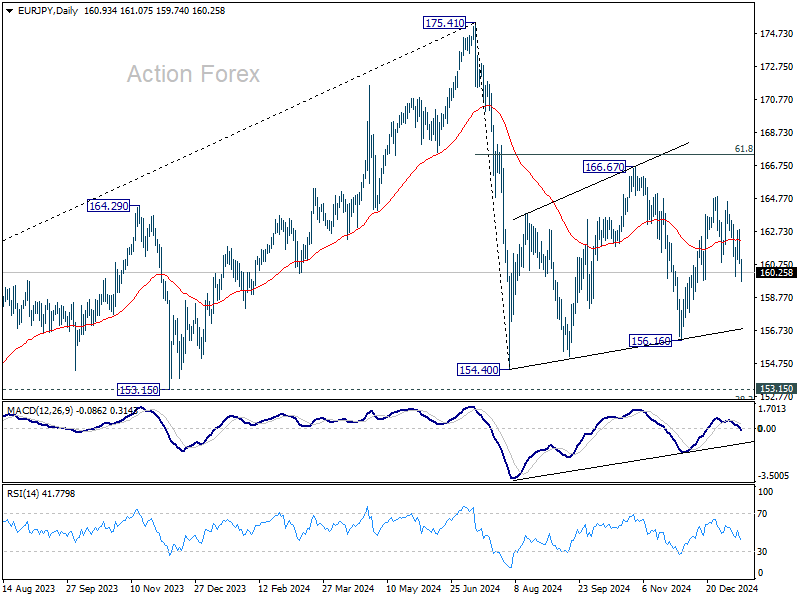

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.22; (P) 161.59; (R1) 162.38; More...

EUR/JPY's fall from 164.89 is resuming through 160.02 temporary low. Intraday bias is back on the downside for 156.16 support next. Firm break there will argue that corrective pattern from 154.40 has completed, and fall from 175.41 is ready to resume. For now, risk will stay on the downside as long as 162.88 resistance holds, in case of recovery.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

S&P 500 Index Rises to Psychological Level

The US stock market experienced an upswing following the release of inflation data yesterday. According to ForexFactory:

→ The annual Consumer Price Index (CPI) matched expectations at 2.9%.

→ The monthly Core CPI came in at 0.2%, below analysts' forecast of 0.3%.

Market participants interpreted this as a positive signal, leading to the S&P 500 index (US SPX 500 mini on FXOpen) gaining over 1% in the first 30 minutes after the data release.

As reported by Reuters:

→ Concerns about inflation eased, reviving hopes for a potential Federal Reserve rate cut, buoyed by a strong start to the earnings season (which we will cover in more detail later);

→ However, the rally may be short-lived, as inflation in the US remains uncomfortably high and could increase further due to aggressive tariff and tax policies under the new Trump administration;

→ Analysts caution that the Federal Reserve's rate is likely to remain unchanged for some time.

Technical analysis of the S&P 500 index chart (US SPX 500 mini on FXOpen) shows that since early August—when the Japanese stock market crash triggered concerns of a global recession, dragging US equities lower—the price has been in an upward trend, marked by a blue channel. The January mid-month low has provided a more precise point to define the lower boundary of this channel.

From this perspective, traders should note that the current S&P 500 price has reached a resistance zone, which consists of:

→ The median line of the blue channel;

→ The psychological level of 6,000 points;

→ The upper red line, drawn through the local highs of December 2024 and January 2025, suggesting that the decline beginning on 18th December could be viewed as an intermediate correction within the blue ascending channel.

This resistance area may serve as a key test of the bulls' determination to complete the correction and resume the upward trend.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

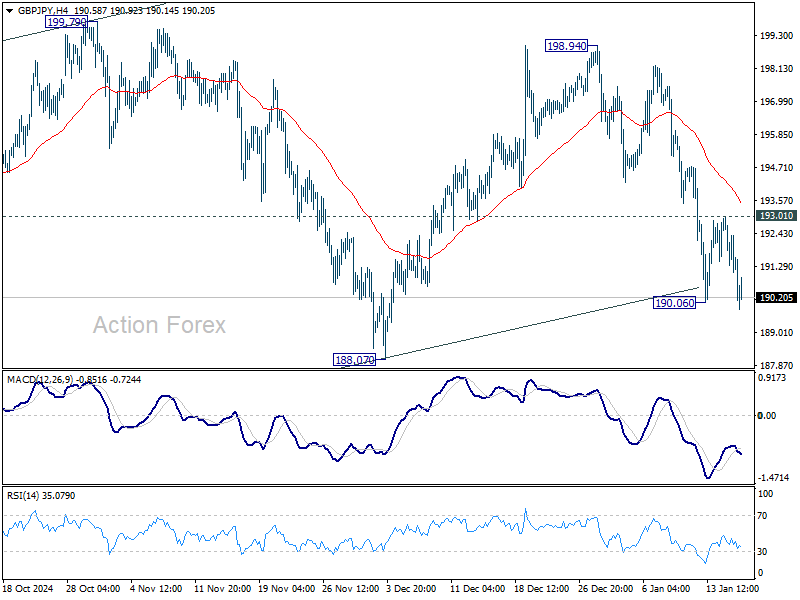

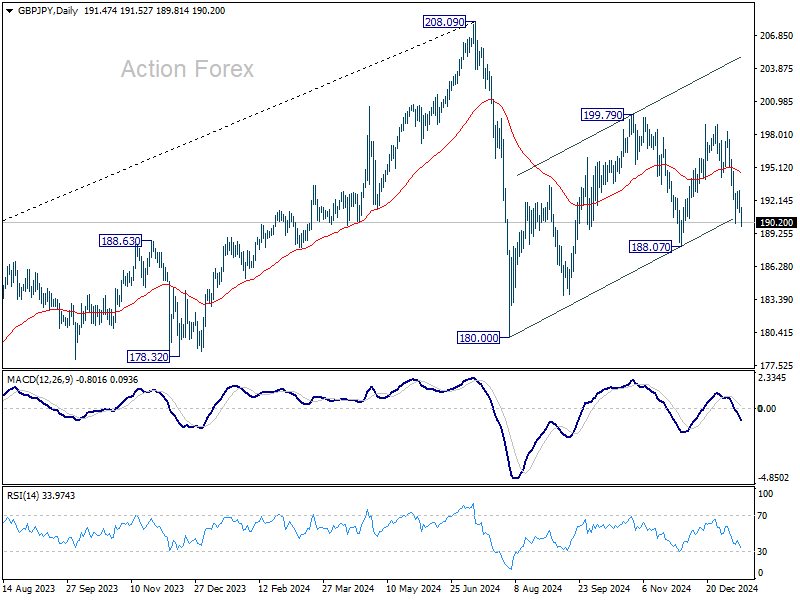

GBP/JPY Daily Outlook

Daily Pivots: (S1) 190.78; (P) 191.91; (R1) 192.72; More...

GBP/JPY's breach of 190.06 temporary low suggests that fall from 198.94 is resuming. Intraday bias is back on the downside for 188.07 support. Firm break there will argue that corrective pattern from 180.00 has finished too, and larger decline from 208.09 might be ready to resume. On the upside, above 193.01 resistance will delay the bearish case and turn intraday bias neutral again.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

BoJ’s Repeated Hawkish Signals Fuel Yen Rebound, Sterling Falters on Stagnant Growth Data

Yen's near term rebound gained momentum again today, supported by BOJ Governor Kazuo Ueda’s persistent messaging about a potential rate hike at next week’s policy meeting. Ueda’s repeated remarks are interpreted as laying the groundwork for markets to brace for a monetary policy shift. While recent polls as of last week indicated only a minority expectation of a January hike, the market are clearly undergoing recalibration. However, the current move in Yen against Dollar remains largely corrective, and a sustained reversal in the broader down trend trend would require further confirmation.

Meanwhile, Sterling continues to face mounting pressure after UK GDP data highlighted stagnation in economic activity. Monthly GDP rose just 0.1% in November, falling short of expectations. More importantly, growth over the three months to November was flat. The data has heightened fears of a contraction in Q4. Adding to Sterling’s challenges, new MPC member Alan Taylor struck a dovish tone in his first public speech, noting that while inflation is nearing its endgame, the weakening economy justifies a return to more “normal” interest rates.

For the week so far, Sterling remains the weakest performer among major currencies, with no signs of a sustainable rebound. Dollar is the second worst, as it continues to consolidate recent gains. . Yesterday’s softer-than-expected core CPI reading alleviated fears of a Fed policy reversal toward tightening, while a resurgence in risk appetite has kept the Dollar’s recovery momentum in check. Canadian Dollar rounds out the bottom three.

On the other hand, Australian Dollar, buoyed by risk-on sentiment. However, the Aussie’s inability to extend its rally following robust employment data raises questions about its underlying strength. Yen is the second-best performer, with the potential to advance further as expectations for a BoJ policy shift solidify. New Zealand Dollar rounds out the top three, while Euro and Swiss Franc are mixed in the middle.

Technically, the US stock markets are back into focus with yesterday's strong rebound. It might be too early to call for resumption of record run in S&P 500. But price actions from 6099.97 are still clearly corrective looking. Downside is also supported above 5669.67 resistance turned support. So, break of 6099.97 remains in favor at a later stage, probably after Trump's inauguration that clear out some uncertainties over his trade policies, as tariff could be raised just gradually to minimize the shocks to the economy.

UK GDP grows only 0.1% mom in Nov, with mixed sector performance

UK’s economy posted modest growth in November, with GDP increasing by 0.1% mom, but slightly missing market expectations of 0.2%. Nevertheless, this marked a positive turnaround from the -0.1% mom contraction in October.

Sectoral performance was mixed, with services, the largest contributor to the economy, inching up by 0.1% mom, while production fell by -0.4% mom. Construction activity, however, provided a brighter spot, rising 0.4% mom during the month.

Despite November’s modest gains, the broader economic picture remains subdued. Over the three months to November 2024, real GDP showed no growth compared to the three months to August. Services, which account for a significant portion of the UK’s output, stagnated over this period. Production output contracted by -0.7%, offsetting the 0.2% growth seen in construction.

BoJ’s Ueda reiterates rate hike debate for next week’s policy meeting

BoJ Governor Kazuo Ueda indicated today, for the second time this week, that the central bank will "debate whether to raise interest rates" at its upcoming January 23-24 policy meeting. This marks the second time in this week that Ueda has emphasized

Ueda’s comments come as BoJ prepares its new quarterly economic report, which will serve as the basis for its policy decision. While the Governor has not committed to a specific outcome, the repeated message signals that a rate hike is a plausible scenario, barring any significant market shocks tied to the January 20 inauguration of U.S. President-elect Donald Trump.

Market sentiment, nevertheless, remains divided on the timing of the anticipated hike. A recent poll conducted between January 8-15 shows that 59 out of 61 economists expect BoJ to raise rates to 0.50% by the end of March. Yet, only 20 foresee the move occurring at this month’s meeting.

Japan's PPI holds steady at 3.8% as import prices turn positive

Japan's PPI held steady at 3.8% yoy in December, meeting market expectations and maintaining the previous month’s pace. Key drivers included a sharp 31.8% yoy rise in agricultural goods prices, fueled by soaring rice costs.

Energy costs also contributed significantly, with electric power, gas, and water prices climbing 12.9% year-on-year. This uptick comes as the government phases out subsidies designed to mitigate rising utility and gasoline prices.

Yen-based import prices turned positive, rising 1.0% yoy after three months of declines. While modest, this reversal underscores the lingering effects of Yen depreciation, which was recorded at -0.1% mom.

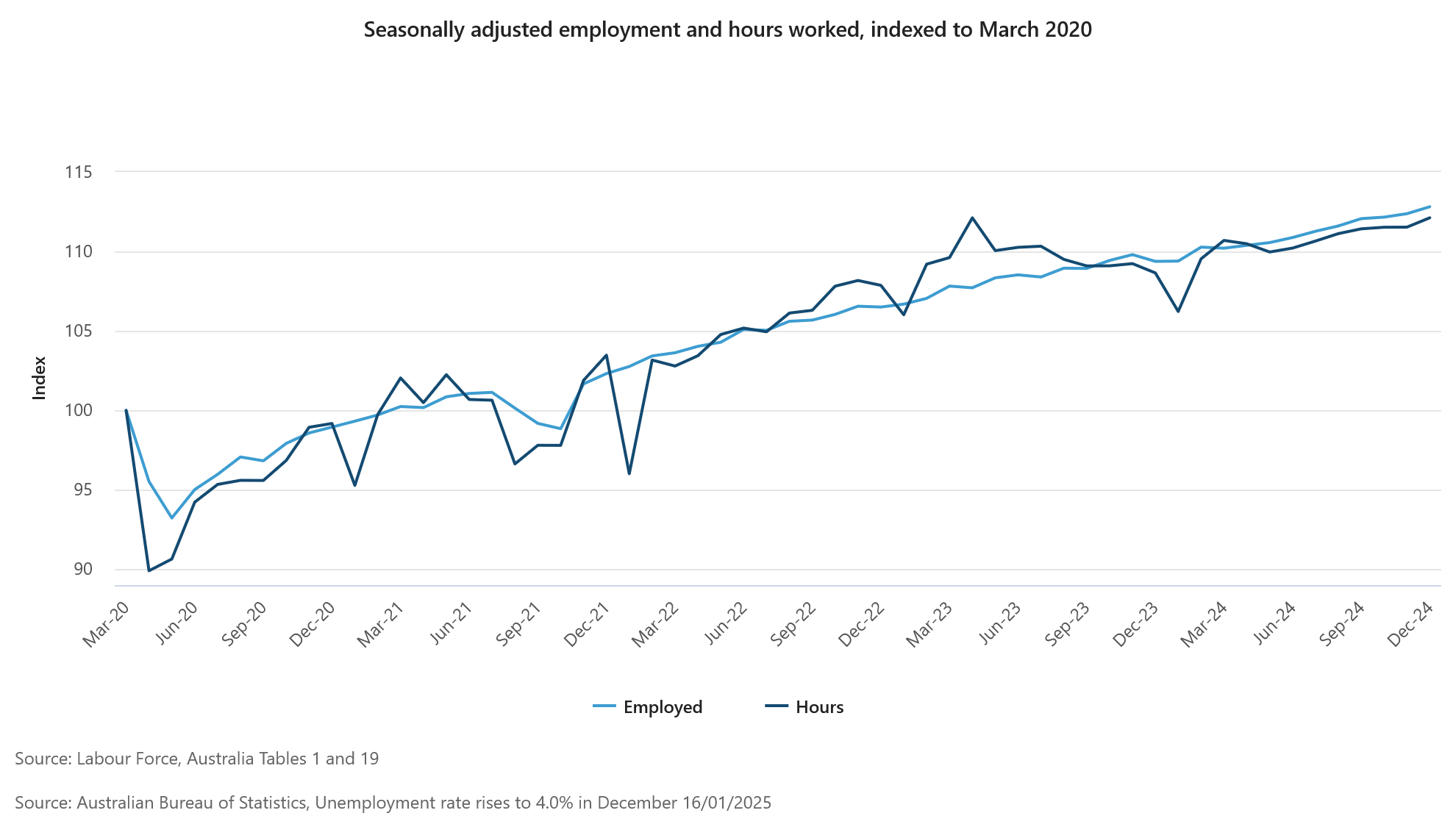

Australia’s employment grows 56.3k in Dec, showing continuous resilience

Australia’s labor market displayed resilience in December as employment surged by 56.3k, significantly exceeding expectations of a 15.0k increase. Number of unemployed people also rose by 10.3k, contributing to a slight uptick in the unemployment rate from 3.9% to 4.0%, in line with forecasts.

Participation rate climbed to a record high of 67.1%, up from 67.0%, reflecting an expanding labor force. Additionally, employment-to-population ratio rose by 0.1 percentage point to a new peak of 64.5%, showcasing the labor market’s capacity to absorb more workers. Monthly hours worked increased by 0.5% mom, equivalent to 10 million additional hours.

This data supports the view that the labor market’s earlier signs of easing have stabilized in the second half of 2024. Robust employment growth, consistent levels of average hours worked, and unchanged or lower levels of labor underutilization compared to a year ago affirm the ongoing strength of the job market.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 190.78; (P) 191.91; (R1) 192.72; More...

GBP/JPY's breach of 190.06 temporary low suggests that fall from 198.94 is resuming. Intraday bias is back on the downside for 188.07 support. Firm break there will argue that corrective pattern from 180.00 has finished too, and larger decline from 208.09 might be ready to resume. On the upside, above 193.01 resistance will delay the bearish case and turn intraday bias neutral again.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

UK GDP grows only 0.1% mom in Nov, with mixed sector performance

UK’s economy posted modest growth in November, with GDP increasing by 0.1% mom, but slightly missing market expectations of 0.2%. Nevertheless, this marked a positive turnaround from the -0.1% mom contraction in October.

Sectoral performance was mixed, with services, the largest contributor to the economy, inching up by 0.1% mom, while production fell by -0.4% mom. Construction activity, however, provided a brighter spot, rising 0.4% mom during the month.

Despite November’s modest gains, the broader economic picture remains subdued. Over the three months to November 2024, real GDP showed no growth compared to the three months to August. Services, which account for a significant portion of the UK’s output, stagnated over this period. Production output contracted by -0.7%, offsetting the 0.2% growth seen in construction.

Australia’s employment grows 56.3k in Dec, showing continuous resilience

Australia’s labor market displayed resilience in December as employment surged by 56.3k, significantly exceeding expectations of a 15.0k increase. Number of unemployed people also rose by 10.3k, contributing to a slight uptick in the unemployment rate from 3.9% to 4.0%, in line with forecasts.

Participation rate climbed to a record high of 67.1%, up from 67.0%, reflecting an expanding labor force. Additionally, employment-to-population ratio rose by 0.1 percentage point to a new peak of 64.5%, showcasing the labor market’s capacity to absorb more workers. Monthly hours worked increased by 0.5% mom, equivalent to 10 million additional hours.

This data supports the view that the labor market’s earlier signs of easing have stabilized in the second half of 2024. Robust employment growth, consistent levels of average hours worked, and unchanged or lower levels of labor underutilization compared to a year ago affirm the ongoing strength of the job market.

BoJ’s Ueda reiterates rate hike debate for next week’s policy meeting

BoJ Governor Kazuo Ueda indicated today, for the second time this week, that the central bank will "debate whether to raise interest rates" at its upcoming January 23-24 policy meeting. This marks the second time in this week that Ueda has emphasized

Ueda’s comments come as BoJ prepares its new quarterly economic report, which will serve as the basis for its policy decision. While the Governor has not committed to a specific outcome, the repeated message signals that a rate hike is a plausible scenario, barring any significant market shocks tied to the January 20 inauguration of U.S. President-elect Donald Trump.

Market sentiment, nevertheless, remains divided on the timing of the anticipated hike. A recent poll conducted between January 8-15 shows that 59 out of 61 economists expect BoJ to raise rates to 0.50% by the end of March. Yet, only 20 foresee the move occurring at this month’s meeting.

Japan’s PPI holds steady at 3.8% as import prices turn positive

Japan's PPI held steady at 3.8% yoy in December, meeting market expectations and maintaining the previous month’s pace. Key drivers included a sharp 31.8% yoy rise in agricultural goods prices, fueled by soaring rice costs.

Energy costs also contributed significantly, with electric power, gas, and water prices climbing 12.9% year-on-year. This uptick comes as the government phases out subsidies designed to mitigate rising utility and gasoline prices.

Yen-based import prices turned positive, rising 1.0% yoy after three months of declines. While modest, this reversal underscores the lingering effects of Yen depreciation, which was recorded at -0.1% mom.

EUR/USD Stabilises as US Inflation Cools Without Major Surprises

Following a nervous session last night, the EUR/USD pair is trading near 1.0285 on Thursday morning. The market is now stabilising.

Key developments influencing EUR/USD

US inflation data showed moderate growth, aligning with expectations. As forecast, the Consumer Price Index (CPI) rose by 0.4% m/m in December, maintaining an annualised rate of 2.9% y/y. Core CPI, excluding volatile goods, offered a slight surprise with a ‘cooling’ effect. It increased by 0.2% m/m (3.2% y/y), below the forecasted 0.3% m/m (3.3% y/y).

US Treasury yields declined, negatively impacting the USD. However, the currency market’s reaction remained subdued.

The release of inflation statistics prompted investors to modestly revise their expectations for Federal Reserve interest rate cuts in 2025. Lending costs are now expected to drop by an average of 37 basis points throughout the year.

The USD demonstrated resilience in January and performed better than in December. If this trend continues, the current week will mark the fourth consecutive week of USD strengthening.

In contrast, European statistics provided little support for the euro. Industrial production in the Eurozone rose by 0.2% m/m in November, following stagnation in October. However, year-on-year figures revealed a deeper contraction, with production falling by 1.9%.

Investors now await key US economic data, including December retail sales and weekly jobless claims, which could further influence the pair.

Technical analysis of EUR/USD

On the H4 chart, EUR/USD completed a corrective wave to 1.0350 before forming a new downward impulse to 1.0258. The current outlook suggests the potential development of a new downward wave targeting 1.0160. After reaching this level, a corrective move towards 1.0250 is likely, with a possible further decline to 1.0050. This scenario is supported by the MACD indicator, with its signal line below zero and trending downwards, indicating the likelihood of renewed lows.

On the H1 chart, the pair formed a downward impulse to 1.0258, with a correction expected to target 1.0300. Once this level is reached, the downward wave may resume, aiming for 1.0210 and potentially extending to 1.0160. The Stochastic oscillator supports this outlook, with its signal line below the 50 mark and heading towards 20, suggesting continued downward momentum.

Conclusion

EUR/USD remains under pressure as US inflation data bolstered the dollar’s resilience. While technical indicators point to further downside potential, the pair’s movements will largely depend on upcoming US retail sales and jobless claims data, as well as the overall strength of the USD. On the euro’s side, weak industrial production data highlights ongoing challenges in the eurozone, adding further weight to the bearish outlook.

BoE Taylor Stroke a Dovish Tone in His First Public Speech

Markets

US December CPI numbers avoided a feared acceleration and triggered a cross-asset relief move. The big reaction was more about repositioning rather than the actual data. Headline CPI (0.4% M/M, 2.9% Y/Y) was in line with consensus while core CPI (0.2% M/M, 3.2% Y/Y) was only just below expectations. US yields lost 9.6 bps (30-yr) to 15.2 bps (7-yr) with the belly of the curve outperforming the wings. US money markets moved back to two rather than one more 25 bps Fed rate cut this year, with a first one discounted by June. NY Fed Williams, Richmond Fed Barkin and Chicago Fed Goolsbee all welcomed the monthly price report, but added that this doesn’t alter the story line set out back in December. It will take more time to bring inflation on a sustainable path to 2%, meaning restrictive policies are still necessary. The goldilocks combo of (strong) payrolls, (slightly) lower CPI, lower real rates and strong Q4 (US banks) earnings propelled US stock markets 1.65% (Dow) to 2.45% (Nasdaq) higher. US retail sales can today extend those positive market vibes. The US dollar was the odd one out, holding strong despite an initial move lower. EUR/USD closed at 1.0289 from 1.0308 and with an intraday top at 1.0354. Two elements are at play. First, European bond yields followed the US move with EU swap rates shedding up to 12 bps (belly). Second, event risk looms large with US markets enjoying a long weekend (MLK Day on Monday Jan 20) during which president-elect Trump will be inaugurated. The Japanese yen continues outperforming on more talk that the BoJ will effectively hike policy rates next week. USD/JPY approached 155 for the first time since mid-December.

Bank of England rate-setter Alan Taylor stroke a dovish tone in his first public speech since joining the central bank in September of last year. He sides with the more benign inflation cases made by the BoE in which price pressures fade relatively quickly. Under this view, the economy might face adverse demand pressures potentially on many fronts while supply is less perturbed. The BoE’s reaction function should then be one of lowering policy rates rather quickly to neutral, which Taylor estimates at around 2.75% in this scenario: “we are in the last half mile on inflation, but with the economy weakening it’s time to get interest rates back toward normal to sustain a soft landing”. Accelerated rate cuts means perhaps 125 bps to 150 bps in the coming year. This view contrasts sharply with UK money markets currently discounting a cumulative 50 bps of rate cuts by the end of the year. A first one could be implemented as soon as February given the 6-3 split vote in December and in the wake of yesterday’s below-consensus inflation numbers. BoE Taylor was one of the dissenters at that December policy meeting together with his colleagues Ramsden and Dhingra. They voted in favour of a 25 bps rate cut rather than sticking with unchanged policy rates. UK Gilts yesterday outperformed with UK yields losing 14 to 16 bps across the curve. EUR/GBP tested first resistance at 0.8448, but a break didn’t happen, at least not for now. GBP/USD holds near the sell-off lows (1.22) with support lingering around 1.2037 (Oct 2023 low). We stick to our bearish view against sterling.

News & Views

Canada set up a draft list of some C$150 bn of US-manufactured products eligible for import tariffs in case President-elect Trump decides to impose levies on Canadian goods, Bloomberg reported citing an official familiar to the matter. The exact items on this initial list are not disclosed yet and it would only come into force if the next US administration moves first. But its scope is in any case much bigger than during Trump’s previous term, when Canada slapped tariffs on some C$17bn of US exports to the country. Canadian imports from the US in the 12 months to November amounted to C$487bn, meaning the draft list covers nearly a third of the products’ value.

The central bank of South Korea unexpectedly kept its policy rate unchanged at 3% this morning in a 6-1 vote. Governor Rhee said that based on growth alone, the central bank would have cut rates. Inflation at 1.9% is also close to the BoK’s 2% target. All members except Rhee kept the door open for reductions in the next couple of months. But in considering all variables including financial stability risks the BoK today decided otherwise. Rhee was referring to the dramatic slide in the South Korean currency to the lowest level against since 2009 in the wake of president Yoon Suk Yeal’s failed martial law attempt early December. The economic fallout of the political crisis is probably bigger than expected, the governor said, and downside risks to the 2025 outlook have increased. Today’s status quo was also underpinned by uncertainty surrounding Trump’s first policy measures after his inauguration next week. USD/KRW trades little changed around 1456.7. The multi-year high end-December stood at 1486.85.