Sample Category Title

GBPNZD: Expanding Wedge

GBPNZD, Daily

In the Daily timeframe, GBPNZD fell towards the lower trendline of the expanding channel. Price is testing support and has crossed the lower Bollinger line, indicating a possible rebound. However, the AO indicates that the bearish momentum is gaining strength.

- A trendline break below 2.1760 will drop GBPNZD to 2.1470;

- A rebound from the trendline will bring the price back to 2.2100;

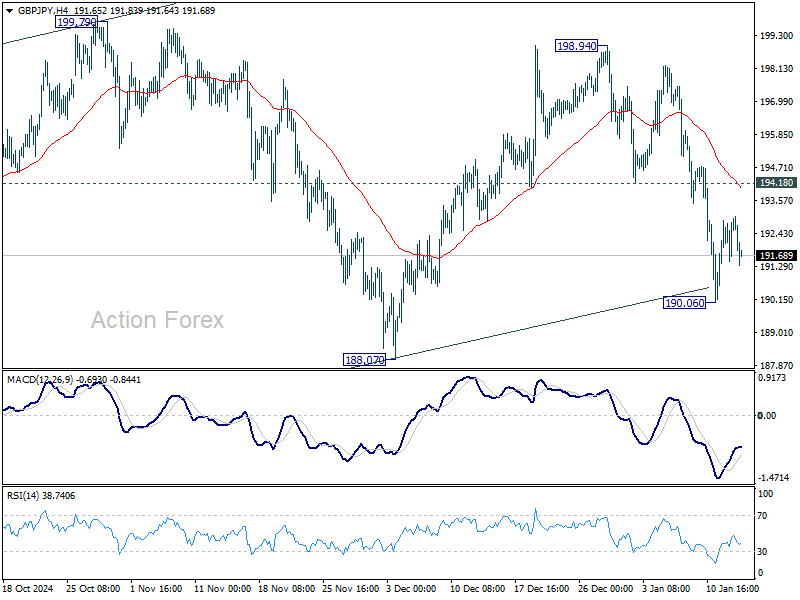

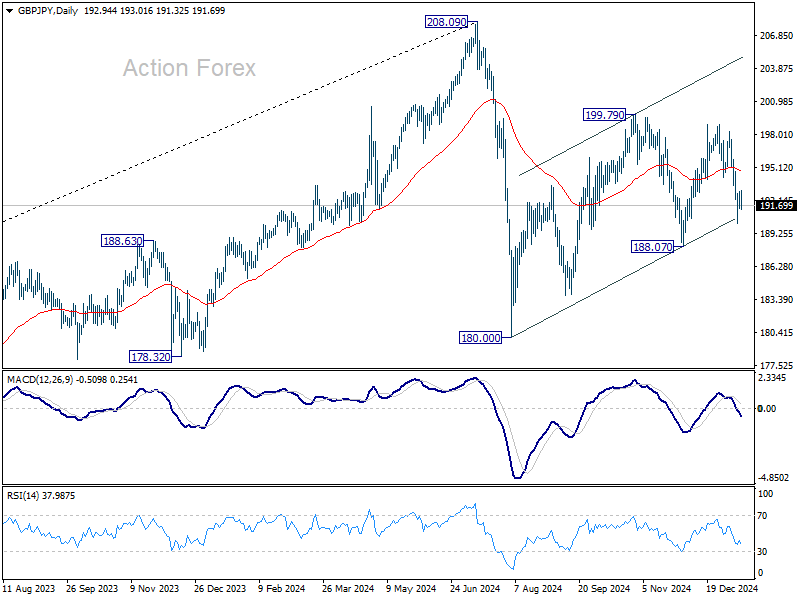

GBP/JPY Daily Outlook

Daily Pivots: (S1) 192.00; (P) 192.50; (R1) 193.51; More...

Intraday bias in GBP/JPY remains neutral for the moment and outlook is unchanged. Rebound from 188.07 could have completed at 198.94 already. Risk will stay on the downside as long as 194.18 support turned resistance holds. Below 190.06 will target 188.07 support. Firm break there will argue that corrective pattern from 180.00 has finished too, and larger decline from 208.09 might be ready to resume.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

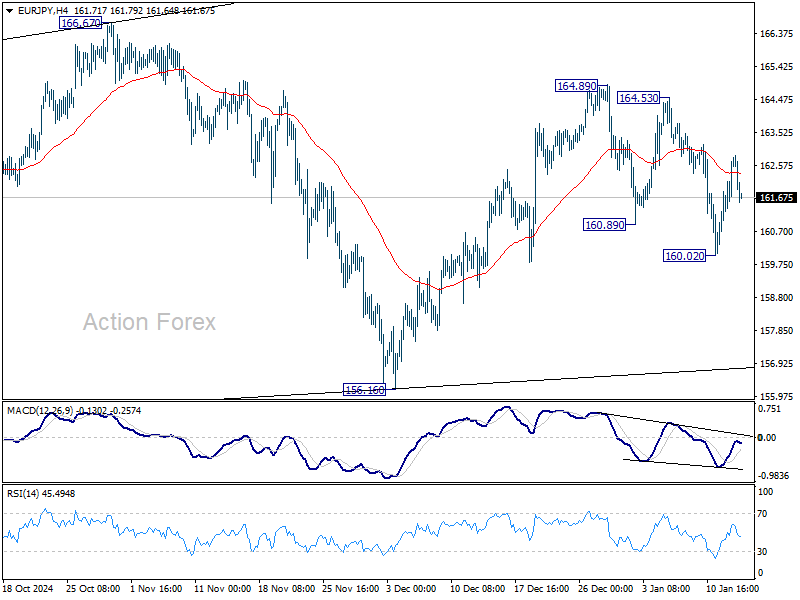

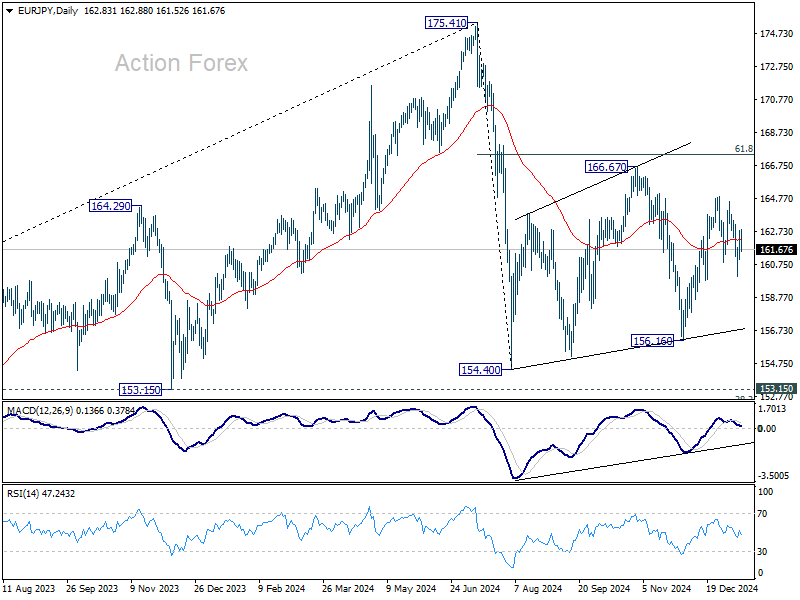

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.64; (P) 162.25; (R1) 163.45; More...

Intraday bias in EUR/JPY remains neutral and outlook is unchanged. Rebound from 156.16 might have completed at 164.89 already. Risk will stay on the downside as long as 164.53 resistance holds. Below 160.02 will bring deeper fall to 156.16 support next. Firm break there will argue that corrective pattern from 154.40 has completed, and fall from 175.41 is ready to resume.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

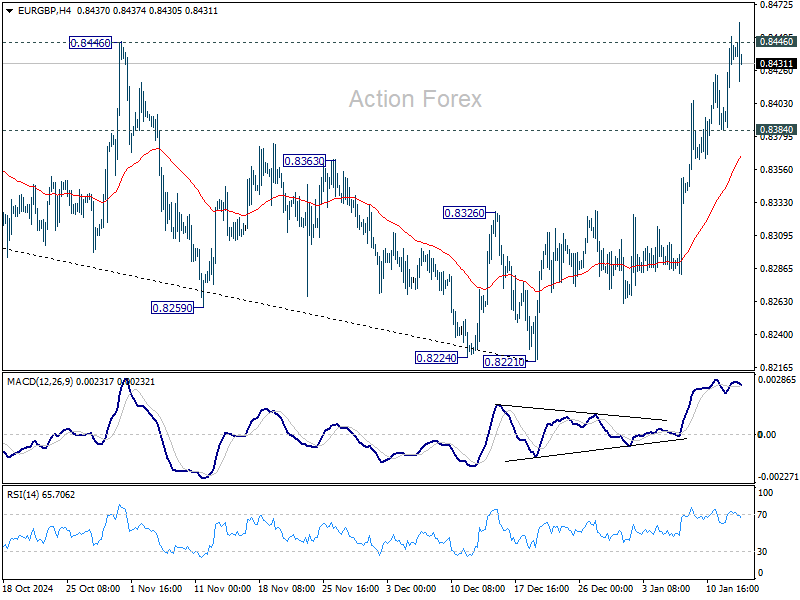

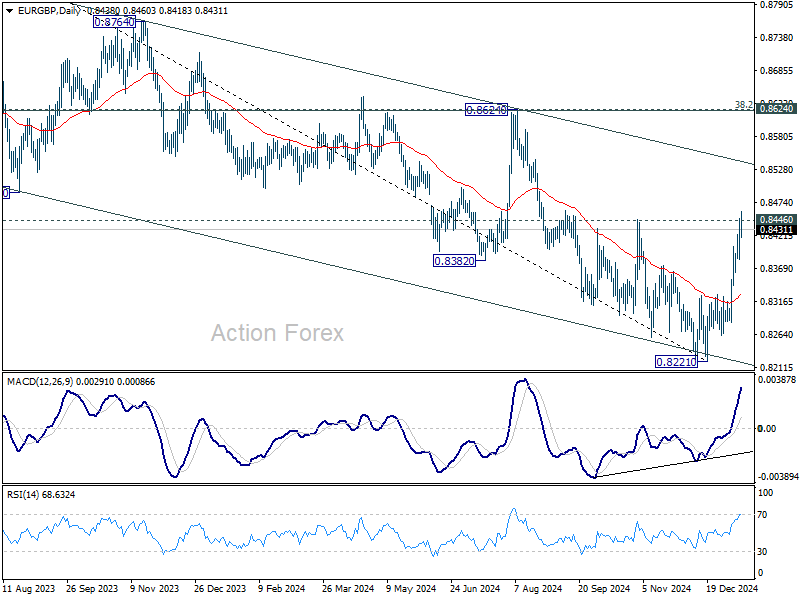

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8399; (P) 0.8425; (R1) 0.8465; More...

Intraday bias in EUR/GBP remains on the upside for the moment, with focus on 0.8446 resistance. Firm break there will target 0.8624 cluster resistance zone, even as a corrective move. On the downside, below 0.8384 minor support will turn intraday bias neutral first.

In the bigger picture, considering bullish convergence condition in D MACD, decisive break of 0.8446 resistance and 55 D EMA (now at 0.8446) should confirm medium term bottoming at 0.8221, just ahead of 0.8201 key support (2022 low). Further rally should be seen towards 0.8624 key resistance, even as a correction to the down trend from 0.9267 (2022 high). Overall, however, medium term outlook will be neutral at best until decisive break of 0.8624 cluster zone (38.2% retracement of 0.9267 to 0.8221 at 0.8621). Risk will stay on the downside even in case of strong rebound.

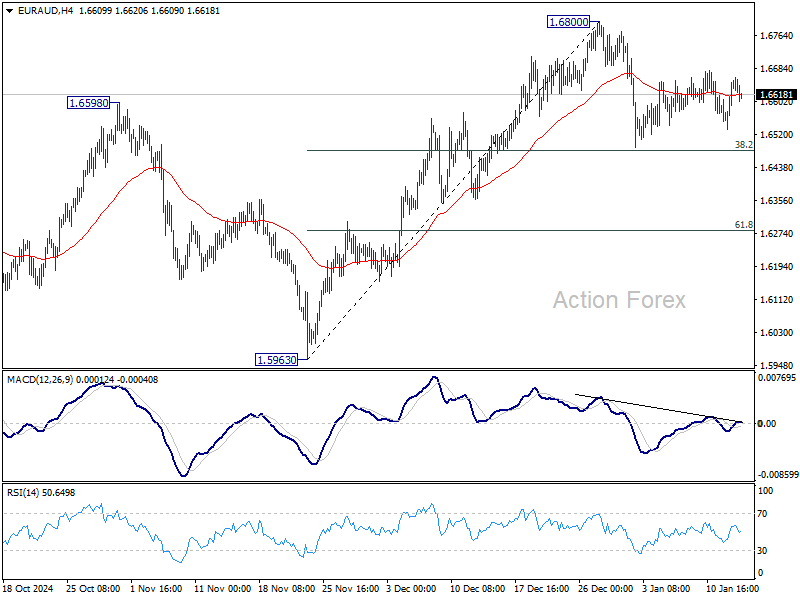

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6565; (P) 1.6610; (R1) 1.6685; More...

EUR/AUD is still bounded in consolidation from 1.6800 and intraday bias stays neutral. Downside should be contained by 38.2% retracement of 1.5963 to 1.6800 at 1.6480 in case of another fall. Firm break of 1.6800 will resume the rally from 1.5963. However, firm break of 1.6480 will bring deeper correction 61.8% retracement at 1.6283.

In the bigger picture, EUR/AUD is holding on to 1.5996 key support despite brief breach. Larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5995 will indicate that such up trend has completed and deeper decline would be seen.

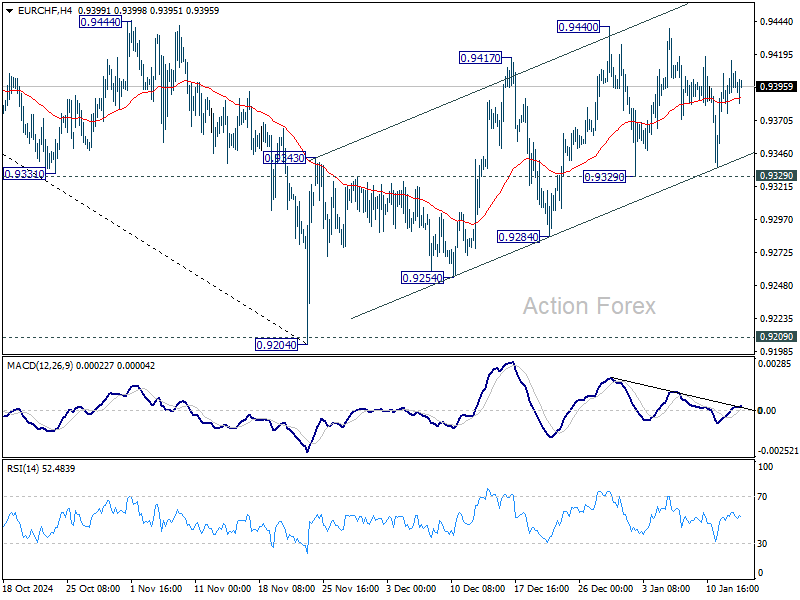

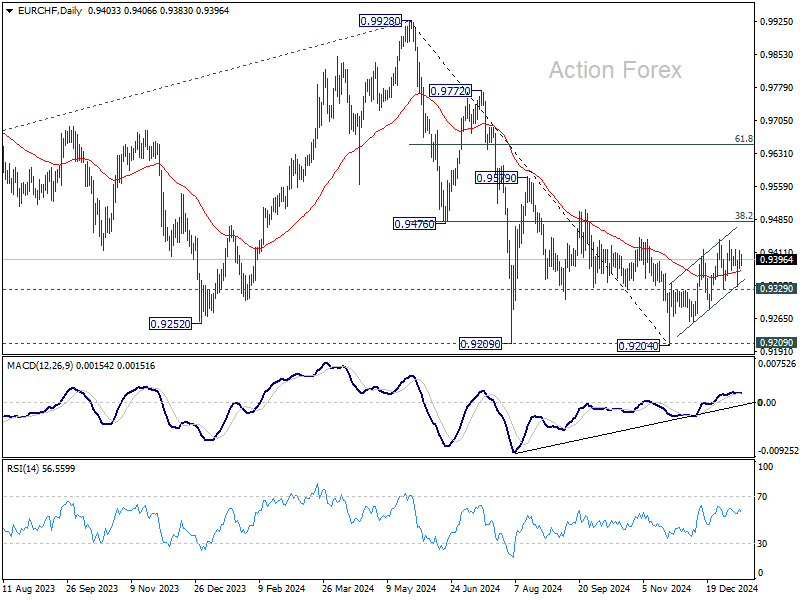

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9383; (P) 0.9399; (R1) 0.9422; More....

No change in EUR/CHF's outlook as consolidation continues and intraday bias remains neutral. Corrective rebound from 0.9204 could still extend higher. But upside should be limited by 0.9481 fibonacci resistance. On the downside, firm break of 0.9329 support will argue that the correction has completed, and turn bias back to the downside for 0.9284 support first.

In the bigger picture, while corrective rebound from 0.9204 might extend higher, strong resistance could be seen from 38.2% retracement of 0.9928 to 0.9204 at 0.9481 to limit upside. Down trend from 0.9928 (2024 high) is still in favor to resume through 0.9204/9 support zone at a later stage.

Eurozone industrial production rises 0.2% mom in Nov, EU up 0.1% mom

Eurozone industrial production edged up by 0.2% mom in November, falling short of 0.3% mom consensus forecast. While the overall increase suggests resilience in the industrial sector, the performance was uneven across categories. Production rose by 1.5% for durable consumer goods and 1.1% for energy, highlighting strong demand in these areas. Intermediate and capital goods also posted gains of 0.5% each, while non-durable consumer goods saw a marginal uptick of 0.1%.

Across the broader EU, industrial production grew by just 0.1% on the month. The highest monthly increases were recorded in Belgium (+8.7%), Malta (+7.1%) and Lithuania (+4.3%). The largest decreases were observed in Ireland (-5.8%), Luxembourg (-3.9%) and Portugal (-3.4%).

ECB’s Guindos and Villeroy affirm progress on disinflation

ECB Vice President Luis de Guindos highlighted today that disinflation in the Eurozone is “well on track,” reinforcing optimism about the region's progress toward price stability. While December’s inflation rose to 2.4%, Guindos noted that this increase was anticipated and aligned with ECB’s projections. Domestic inflation remains elevated, but recent easing signals have provided some relief.

Guindos cautioned, however, that risks remain high. “The high level of uncertainty calls for prudence,” he said, referencing global trade frictions that could fragment the global economy further. He also warned about the fiscal policy challenges to weigh on borrowing costs and renewed geopolitical tensions to destabilize energy markets.

Despite weak near-term economic outlook, Guindos expressed cautious optimism, stating, “The conditions are in place for growth to strengthen over the projection horizon, although less than was forecast in previous rounds.”

Meanwhile, French ECB Governing Council member François Villeroy de Galhau echoed a positive sentiment, emphasizing progress against inflation.

“We have practically won the battle against inflation,” he said, projecting that it “makes sense for interest rates to reach 2% by the summer.” However, Villeroy also highlighted risks to France’s 2025 growth forecast of 0.9%, acknowledging that while downside risks persist, a recession remains unlikely.

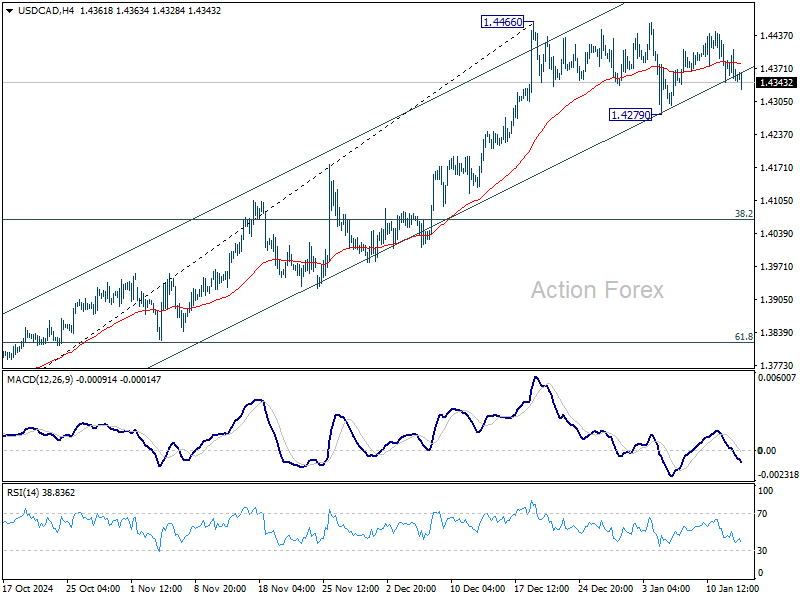

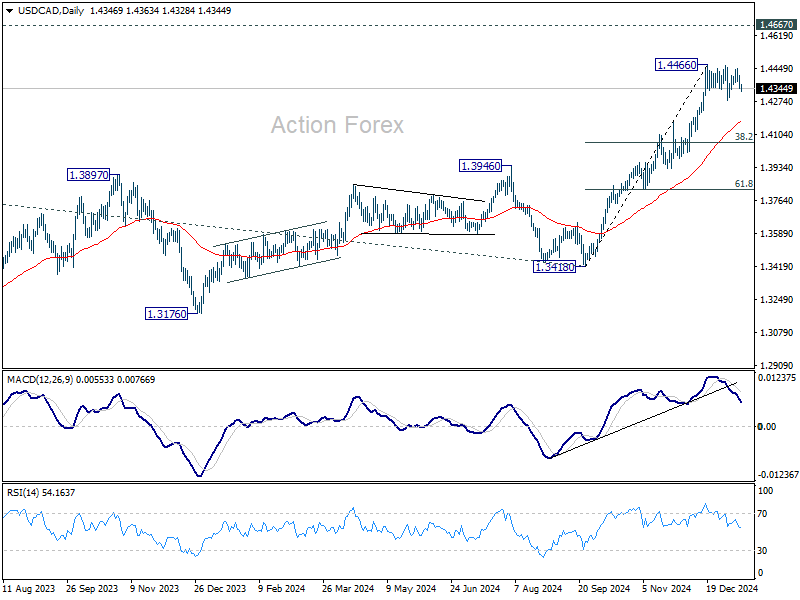

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4325; (P) 1.4367; (R1) 1.4392; More...

Intraday bias in USD/CAD stays neutral as range trading continues. Break of 1.4279 support will bring deeper correction. But downside should be contained by 55 D EMA (now at 1.4172) to bring rebound. On the upside, break of 1.4466 will resume larger up trend to 1.4667/89 long term resistance zone.

In the bigger picture, up trend from 1.2005 (2021) is in progress for retesting 1.4667/89 key resistance zone (2020/2015 highs). Medium term outlook will remain bullish as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.

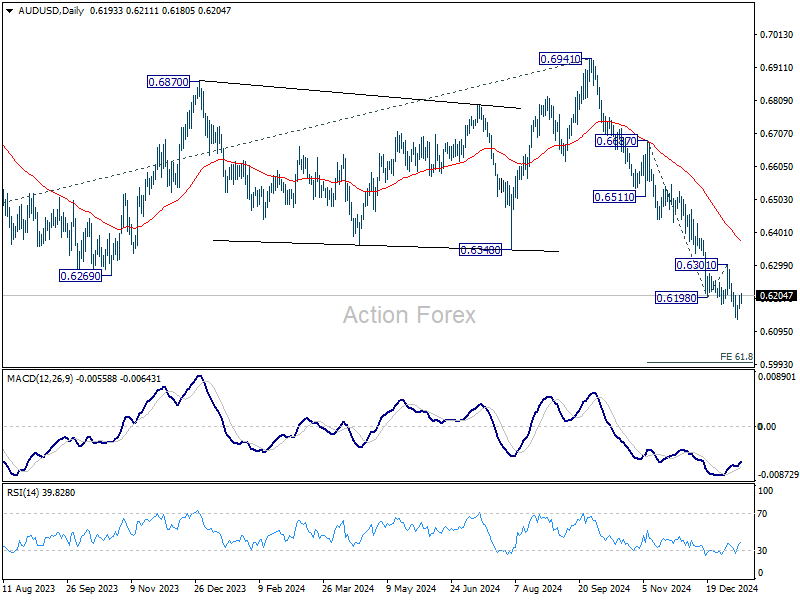

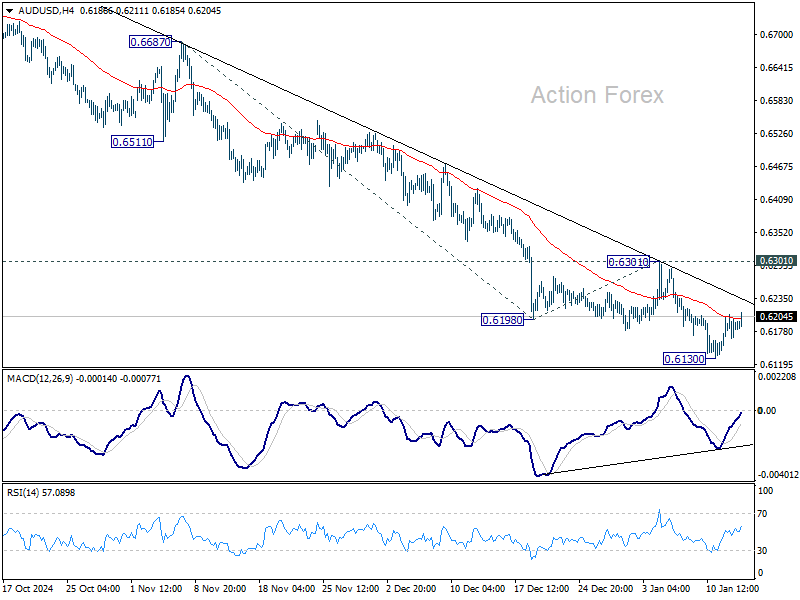

AUD/USD Daily Report

Daily Pivots: (S1) 0.6171; (P) 0.6189; (R1) 0.6213; More...

Intraday bias in AUD/USD remains neutral as consolidations continue above 0.6130. Further decline is expected as long as 0.6310 resistance holds. Break of 0.6130 will resume the fall from 0.6941 to 61.8% projection of 0.6687 to 0.6198 from 0.6301 at 0.5999. However, considering bullish convergence condition in 4H MACD, break of 0.6310 will indicate short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, down trend from 0.8006 (2021 high) is resuming with break of 0.6169 (2022 low). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806, In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6587) holds.