Sample Category Title

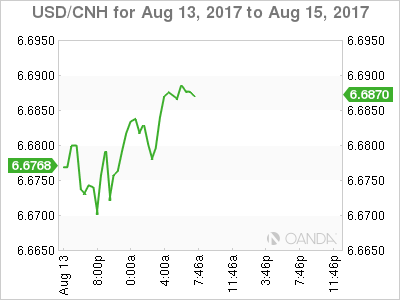

USD/CHF Mid-Day Outlook

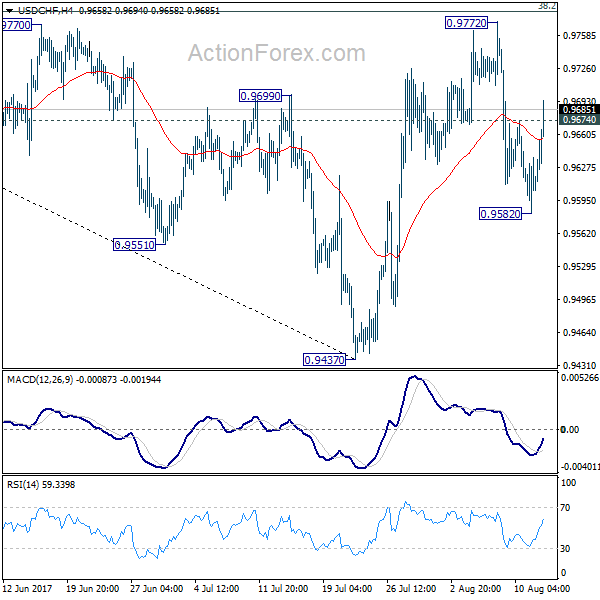

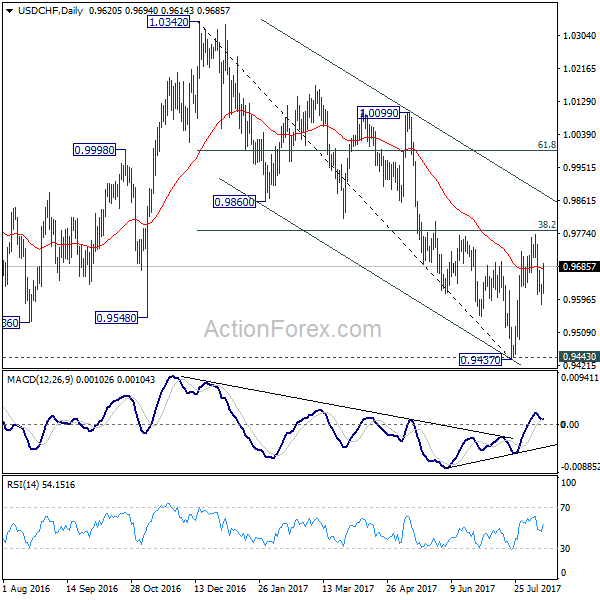

Daily Pivots: (S1) 0.9585; (P) 0.9611; (R1) 0.9641; More...

USD/CHF's strong rebound and break of 0.9674 minor resistance argues that pull back from 0.9772 is completed at 0.9582 already. Intraday bias is turned back to the upside for 0.9772 first. Decisive break there will revive the bullish case of reversal. That is, whole decline from 1.0342 has completed at 0.9437 after defending 0.9443 support. However, the pair is bounded inside medium term falling channel and limited below 38.2% retracement of 1.0342 to 0.9437 at 0.9783 for the moment. Break of 0.9582 will dampen our bullish view and turn bias back to the downside for 0.9437. This could also extend the fall from 1.0342 through 0.9437/43 key support level.

In the bigger picture, current development argues that USD/CHF has successfully defended 0.9443 key support level. And long term range trading in 0.9443/1.0342 is extending with another rise. At this point, there is no sign of an up trend yet. Hence, while further rise is expected in USD/CHF, we'll start to be cautious on loss of momentum above 61.8% retracement of 1.0342 to 0.9437 at 0.9996. However, firm break of 0.9443 will carry larger bearish implication and would target next key support at 0.9072.

Global Markets Rebound, Taking Dollar Higher as US Officials Talk Down War Risks

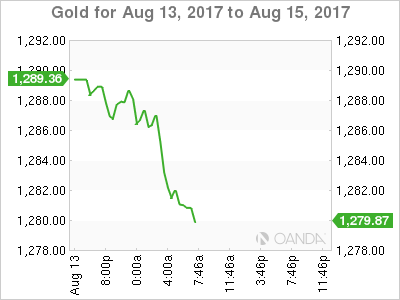

Dollar rebounds broadly today while Yen and Swiss Franc lead the way down as risk aversion seems to have eased. US officials tried to talk down the risk of war with North Korea. European indices are trading generally in positive as FTSE is gaining 0.5% while DAX is is up 1.1%. US futures point to higher open where DOW might have triple digit gain. In other markets, Gold starts to feel heavy ahead of 1300 and dips back below 1290 today. WTI crude oil is struggling in tight range below 49. The US economic calendar is empty today. The immediate focus is that US President Donald Trump would order a broad probe of China's unfair trade practices today including intellectual property thefts.

US officials talk down war risks

U.S. Joint Chiefs of Staff Chairman Joseph Dunford met with South Korean Moon Jae-in for nearly an hour and assured Moon that US will only use military options against North Korea when diplomatic and economic sanctions fail. National Security Adviser H.R. McMaster said that "we're not closer to war than a week ago, but we are closer to war than we were a decade ago". Central Intelligence Agency Director Mike Pompeo said that "I've seen no intelligence that would indicate that we're in that place today" regarding the chance of a nuclear war.

South Korea President Moon: US will respond calmly and responsibly

South Korean President Moon Jae-in emphasized that "there must be no more war on the Korean peninsula". And he urged that "whatever ups and downs we face, the North Korean nuclear situation must be resolved peacefully." He also side "I am certain the United States will respond to the current situation calmly and responsibly in a stance that is equal to ours." South Korean Vice Defence Minister Suh Choo-suk said that "both the United States and South Korea do not believe North Korea has yet completely gained re-entry technology in material engineering terms."

Japan GDP grew fastest in more than two years

Japan GDP grew 1.0% qoq in Q2, much higher than expectation of 0.6% qoq, more than triple of Q1's 0.3% qoq. On annualized balance, GDP grew 4% in the period, much higher than Q1's 1.5% annualized. The quarterly rate was the fastest pace in more than two years. That's also the sixth straight quarter of expansion as recovery gathered steam. Strong domestic demand, which grew 1.3% qoq, is seen as an encouraging sign of the recovery while private consumption also grew 0.9%. That's more than enough to offset the -0.5% qoq fall in exports of goods and services. GDP deflator dropped less than expected by -0.4% yoy.

China data showed deeper slowdown

China retails sales grew 10.4% yoy in July, down from 11% a month ago. The market had anticipated a milder moderation to 10.8%. Industrial production expanded 6.4% yoy in July, decelerating from 7.6% in the prior month. The slowdown is much sharper than consensus. Urban fixed asset investment expanded 8.3% in the first 7 months of the year, slowing from 8.6% in the first half of the year. The market had anticipated a steady growth of 8.6%. The slowdown in economic activities in China has been widely expected as the government pledged to deleverage in at attempted to defend and prevent systematic risks. However the dataflow in July suggests that the slowdown came in deeper than expected.

Hammond and Fox published joint Brexit article

In UK, Chancellor of Exchequer Philip Hammond and International Trade Secretary Liam Fox released a joint article on Brexit over the weekend. They reiterated that UK will definitely leave EU in March 2019. And, they emphasized any trade deal will not be the "back door" to stay in EU. But they emphasized that a "time-limited" transition period would "further our national interest and give business greater certainty". One of the key takeaways from the article is that Hammond and Fox appeared to be trying to settle their differences regarding Brexit. And that raised the prospect of a more united cabinet on the issue.

New Zealand retail sales jumped on sporting events

New Zealand retail sales rose strongly by 2.0% qoq versus expectation of 0.7% qoq. Core retail sales rose 2.1% qoq, above expectation of 0.7% qoq. Sporting events were the main drivers in the strong growth. More than 28000 people attended the World Masters Game back in April. And there were 23000 visitors from UK and Ireland for the Lions rugby series in June. But these event driven figures won't alter RBNZ's neutral stance.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9585; (P) 0.9611; (R1) 0.9641; More...

USD/CHF's strong rebound and break of 0.9674 minor resistance argues that pull back from 0.9772 is completed at 0.9582 already. Intraday bias is turned back to the upside for 0.9772 first. Decisive break there will revive the bullish case of reversal. That is, whole decline from 1.0342 has completed at 0.9437 after defending 0.9443 support. However, the pair is bounded inside medium term falling channel and limited below 38.2% retracement of 1.0342 to 0.9437 at 0.9783 for the moment. Break of 0.9582 will dampen our bullish view and turn bias back to the downside for 0.9437. This could also extend the fall from 1.0342 through 0.9437/43 key support level.

In the bigger picture, current development argues that USD/CHF has successfully defended 0.9443 key support level. And long term range trading in 0.9443/1.0342 is extending with another rise. At this point, there is no sign of an up trend yet. Hence, while further rise is expected in USD/CHF, we'll start to be cautious on loss of momentum above 61.8% retracement of 1.0342 to 0.9437 at 0.9996. However, firm break of 0.9443 will carry larger bearish implication and would target next key support at 0.9072.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Retail Sales Q/Q Q2 | 2.00% | 0.70% | 1.50% | 1.60% |

| 22:45 | NZD | Core Retail Sales Q/Q Q2 | 2.10% | 0.70% | 1.20% | 1.50% |

| 23:50 | JPY | GDP Q/Q Q2 P | 1.00% | 0.60% | 0.30% | |

| 23:50 | JPY | GDP Deflator Y/Y Q2 P | -0.40% | -0.50% | -0.80% | |

| 2:00 | CNY | Retail Sales Y/Y Jul | 10.40% | 10.80% | 11.00% | |

| 2:00 | CNY | Fixed Assets Ex Rural YTD Y/Y Jul | 8.30% | 8.60% | 8.60% | |

| 2:00 | CNY | Industrial Production Y/Y Jul | 6.40% | 7.10% | 7.60% | |

| 9:00 | EUR | Eurozone Industrial Production M/M Jun | -0.60% | -0.50% | 1.30% | 1.20% |

Market Update – European Session: European Indices Kick Start The Week On Stronger Footing, As Geo-Political Tensions Subside

Notes/Observations

European Indices rise on easing Geo-Political tensions between the US and North Korea

China warns US there is no future in a trade war

Overnight

Asia:

Japan GDP rises at fastest pace in over 2 years with Domestic demand accounting for 1.3 percentage points.

US Trade representatives to investigate whether Chinese trade practices force US firms operating in China to turn over intellectual property

China Industrial production and Retail Sales falls short of expectations, with crackdown on property speculation and rising debt levels started to filter through

PBOC strengthened the yuan to the strongest setting since September 2016.

Europe:

UK Brexit Minister Davis urges talks with the EU to move onto next phase, beyond starter issues. Emphasizes the need to discuss bigger issues around the future of UK-EU partnership.

Eurozone Industrial production falls more than expectations. Only Energy showed a positive reading.

Banca Monte dei Paschi reports over a €3B loss as expected after intervention by the state. Italy now hows over 52% stake.

Americas:

Overnight Fed's Kashkari (Vote) noted the weak CPI readings in the US is another reason to holding off rate hikes.

Economic Calendar

(EU) EURO ZONE JUN INDUSTRIAL PRODUCTION M/M: -0.6% V -0.5%E; Y/Y: 2.6% V 2.8%E

(NL) Netherlands Jun Retail sales y/y: 4.7% v 5.8% prior

(IN) INDIA JULY WHOLESALE PRICES

(WPI) Y/Y: 1.9% V 1.4%E

(CH) SNB Total Sight Deposits for week ending Aug 11th

(CHF): 578.9B v 578.6B prior

(SE) Sweden Jun Household Consumption M/M: 0.0% v 0.3% prior; Y/Y: 2.4% v 2.8% prior

(CZ) Czech Jun Current Account

(CZK): -14.5B v -3.0Be

Fixed Income Issuance:

Non seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx50 1.1% at 3,441, FTSE +0.6% at 7,347, DAX +1.1% at 12,141, CAC-40 +1.0% at 5,110, IBEX-35 +1.2% at 10,409, FTSE MIB +0.9% at 21,556, SMI +1.2% at 8,995, S&P 500 Futures +0.6%]

Market Focal Points/Key Themes: European stocks open slightly higher and gain substantially as the session progressed; easing geopolitical concerns help support risk sentiment; all sectors moving higher, lead by financials; automakers also outperforming; oil price dipped, but didn't drag on energy stocks enough to pull them negative; tomorrow sees several European markets closed due to holiday; upcoming earnings in the US session include Sysco and Canadian Solar.

Equities

Consumer discretionary: Danone BN.FR +1.5% (bid speculation), Berentzen BEZ.DE -12.2% (results)

Materials: Wienerberger WIE.AT +3.2% (analyst action)

Industrials: SMT Scharf S4A.DE +1.9% (results), Hamburger Hafen HHFA.DE +2.7% (earnings), Gesco GSC1.DE +2.8% (earnings)

Financials: Deutsche Pfandbriefbank PBB.DE +4.58% (results), Talanx TLX.DE +1.6% (earnings)

Technology: Rocket Internet RKET.DE +5.8% (buyback)

Telecom: Telit Communications TCM.UK +13.7% (confirms CEO departure)

Healthcare: UDG Healthcare UDG.UK -2.8% (analyst action)

Energy: RWE RWE.DE +1.6% (earnings)

Speakers

(CN) China Foreign Ministry: No future in a China/US trade war

Currencies

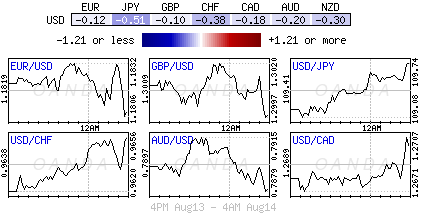

The USD gains ground this morning as GBPUSD drops back below 1.30, while the EURUSD approaches the 1.17 handle coming off the 1.1840 high. Continued downside targets 1.1750. Overall Equity strength has helped the USDYEN firmer, rebounding over 100 pips from Friday lows.

Fixed Income

Bund futures trades at 163.96 down 61 ticks, after breaking below key support at the 164.01 level. Downside targets 163.75 followed by 162.56. To the upside the 165.00 to 165.20 remains key resistance.

Gilt futures trades at 127.70 down 17 ticks, steadily flattened over last week. A resumption to the upside could eye 128.25 then 128.75. A move back below 126.51 targets 125.97

Monday's liquidity report showed Friday's use of the marginal lending facility rose to €189M from €116M prior.

Corporate issuance saw $43B last week with talk that this week could see between $30B coming to market, as we enter the back half of earning season.

Looking Ahead

06:00 (PL) Poland Q2 Labour Costs

07:25 (BR) Brazil Weekly Economist Survey

07:30 (TR) Turkey TCMB Survey of Expecations

08:00 (PL) Poland July CPI Core M/M: 0.0%e v 0.0% prior; Y/Y: 0.8%e v 0.8% prior

08:00 (IN) India July CPI Y/Y: 2.0%e v 1.5% prior

08:30 (CA) Canada July Teranet/National Bank HPI M/M: No est v 2.6% prior; Y/Y: No est v 14.2% prior

09:00 (BE) Belgium trade balance

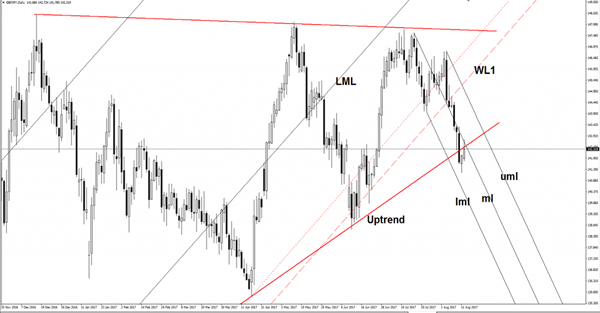

GBP/JPY Selling Opportunity?

Price rebounded and now is retesting the broken red uptrend line, a valid breakdown will validate a further drop. Technically is expected to drop further after the failure to reach the down red sloping line and to stay above the warning line (WL1). A further drop will be confirmed if will decrease again after the minor rebound. Will drop quickly if will stay below the median line (ml) of the minor descending pitchfork.

USD/JPY Valid Or False Breakout

USD/JPY increased significantly today after the Friday’s indecision. Is pressuring the downside line of the symmetrical triangle and the 50% retracement level. Price continues to move in range between the 23.6% retracement level and the 50% level, only a valid breakdown below the 50% retracement level will confirm a large drop.

EUR/GBP Breakout Favored

EUR/GBP is still bullish on the Daily chart and looks motivated to take out a dynamic resistance. Price is going higher as the Euro has managed to increase versus its rivals, but we have to wait for a valid breakout to be sure that will resume the upside movement. Euro is bullish versus the Cable, even if the Euro-zone Industrial Production dropped by 0.6% in June, more versus the 0.4% estimate. The economic indicator plunged after the 1.3% growth in the former reading period.

We have a poor economic calendar today, the rate is driven by the technical factors, so a breakout above the third warning line (wl3) of the former descending pitchfork looks favored. I’ve said in the previous report that will climb much higher if will have enough energy to stabilize above the 50% Fibonacci line.

The next major upside target will be at the upper median line (UML) of the major ascending pitchfork, could also hit the 0.9226 static resistance. Price is trading in the green as the Cable is bloodless on the short term, GBP slips lower also versus the USD.

It is expected to approach and reach the 0.9226 major resistance because is moving in range, you can see that we have an extended sideways movement on the Daily chart.

Only a breakout above the 0.9226 swing high will confirm a medium and long term increase, but is premature to say what will happen because a rejection here will send the rate tumbling on the short term.

Yen Fails To Strengthen Despite Japanese GDP Growth Beating Forecasts

On Monday, the yen dipped into losses against the dollar after a strong rally on Friday, reacting reversely to government preliminary GDP growth data. The figures showed that the Japanese economy grew more than expected for the sixth consecutive quarter, posting its fastest expansion in more than two years.According to the preliminary data released by the cabinet office, the Japanese economy expanded by 4% year-on-year in the second quarter, surprising analysts who expected a growth rate of 2.5%. This was well above the upwardly revised reading of 1.5% seen in the previous quarter and was the highest rate recorded since 2015. On a quarterly basis, GDP growth more than doubled the previous mark of 0.4% (upwardly revised from 0.3%), rising by 1% and exceeding the 0.6% forecasted.

The economy strengthened significantly as private consumption and capital expenditure experienced the highest improvement in more than three years, offsetting the contraction in external demand. With households spending more in durable goods and leisure despite subdued wage growth, private consumption expanded by 0.9%, surpassing the forecast of 0.5% and the previous mark of 0.4%.

Capital expenditure posted the highest growth since June 2015, growing twice the forecast of 1.2% at 2.4% q/q and jumping above the 0.9% (upwardly revised from 0.6%) observed in the first quarter. This expansion happened mainly due to higher business investments in software and construction equipment.

With the Japanese output recording its longest pace of growth since 2005-2006, analysts are more confident that improvements in consumption which account for the two-thirds of the economy will lift inflation toward the 2% Bank of Japan target. Note that the BOJ lowered the timing of inflation reaching the target six times so far due to weaker consumption. However, the Ministry of finance, Toshimitsu Motegi, commenting the data, said that more policies are needed to ensure a continuing recovery in domestic demand, pledging to apply further reforms to improve human capital and productivity. Moreover, he added that for the meantime there is no need to stimulate monetary policy further as consumption and business investments are following the appropriate direction.

Looking at the reaction in the forex markets, the upbeat Japanese data could not provide support to the yen. Dollar/yen climbed by 0.47% to 109.68 after touching a three-month low of 108.71 on Friday. Euro/yen surged by 0.28% to 129.43 following a downtrend which led the pair to a six-week low of 128.03.

Safe Haven Fears Abate, Dollar Capped On Fed Hike Doubts

Monday August 14: Five things the markets are talking about

Last weeks geopolitical worries sent investors scampering for safe havens.

However, the fears of an escalation of tensions between the U.S and North Korea is showing signs of easing this Monday morning as equity markets in Europe follows Asia higher and U.S stock futures are in the black. Gold prices have slipped with U.S Treasuries and the yen.

Nevertheless, the dollar gains seem somewhat capped by the tensions on the Korean peninsula and doubts that the Fed will hike interest rates again this year.

Stateside this week, U.S consumer spending gets things rolling on Tuesday with U.S retail sales (08:30am EDT). The market is looking for it to rebound in ‘moderate' strength.

From a manufacturing data perspective, there is Tuesday's Empire state manufacturing index (08:30 am EDT), Thursday's industrial production (09:15am EDT) and the Philly Fed (08:30am EDT) which all are expected show some moderate strength to keep the market ticking over.

The highlight of the week will be Wednesday's FOMC minutes from last month's meeting which produced no action and no hint on when balance sheet unwinding begins.

Friday winds up with August's consumer sentiment (10:00am EDT), a report that is running well behind its rival consumer confidence report, which has been holding steady at massive highs.

That aside, geopolitical risks are expected to remain a key theme for the global markets in the near term – North Korea celebrates Liberation Day tomorrow to mark the end of Japanese rule.

The market should also be bracing itself for tensions ahead of August 21, when an annual joint U.S-South Korean military exercise is due to begin.

1. Stocks see the light of day

Global equity markets have retraced some of last week's pullback, as robust Asian corporate earnings and reduced fears of imminent military conflict between the U.S and North Korea lifted buying interest.

In Japan, the Nikkei share average fell -1.0% to a 3-month low following a holiday weekend (Japan markets were closed Friday and investors were basically playing catch up), as North Korean tension drove investors to lighten up on riskier assets. The yen's gains last week overshadowed data showing Japan's economic grew at a much stronger pace than expected in Q2 (see below). The broader Topix index finished -1.1% lower.

In South Korea, stocks rebound Monday after ending down for four consecutive sessions on geopolitical fears. The Kospi closed up +0.6%.

Down-under, Australia's S&P/ASX 200 Index rallied +0.7%, while in Hong Kong, the Hang Seng Index gained +1.3%, while the Shanghai Composite Index rose +0.9%.

In China, stocks closed higher on a tech-fuelled rebound. The blue-chip CSI300 index rose +1.3%, while the Shanghai Composite Index gained +0.9%. Investors were unperturbed by data overnight showing that China's factory output slowed more than expected last month, while investment and retail sales also disappointed (see below).

In Europe, easing geopolitical concerns is helping support risk sentiment – all sectors are moving higher, lead by financials and automakers. Lower oil prices are not dragging on energy stocks enough to pull them into negative territory.

Note: Tomorrow sees several European markets closed due to a holiday (France, Greece, Poland and Italy).

U.S stocks are set to open deep in the black (+0.6%).

Indices: Stoxx50 1.1% at 3,441, FTSE +0.6% at 7,347, DAX +1.1% at 12,141, CAC-40 +1.0% at 5,110, IBEX-35 +1.2% at 10,409, FTSE MIB +0.9% at 21,556, SMI +1.2% at 8,995, S&P 500 Futures +0.6%

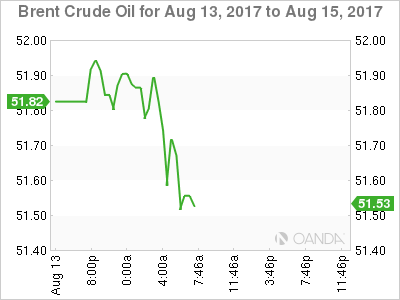

2. Oil prices dip on weak Chinese refining activity, gold lower

Ahead of the U.S open, oil prices are a tad softer as a slowdown in Chinese refining activity growth is casting some market doubts over its crude demand outlook, while rising U.S shale output suggests supplies would likely remain high.

Brent crude futures are at +$51.92 per barrel, down -18c or -0.4% from Friday's close. U.S West Texas Intermediate (WTI) crude futures are at +$48.70 a barrel, down -12c or -0.3%.

Note: Chinese refineries processed +0.4% more crude oil in July y/y at +45.5m tonnes, or about +10.71m bpd – the lowest amount on a daily basis 10-months.

Despite the possible slowdown in China, the IEA indicated last week it expects 2017 oil demand growth of +1.5m bpd, up from a previous expectation of +1.4m bpd.

On Friday, Baker Hughes energy services firm said U.S drillers' added 3-rigs looking for new oil in the week to Aug. 11 bringing the total count up to 768, the most since April 2015.

Expect the usual inventory reports from API and EIA to shape the oil futures curve.

Gold starts the week under pressure (down -0.2% at +$1,286.39 per ounce) as the dollar inches away from last week's lows, but continues to trade atop of its two-month highs touched last week as the market keeps an eye on developments in the North Korean peninsula.

3. Global yields back away from their recent low

U.S Treasury yields fell further on Friday on the soft U.S. consumer prices data (+0.1% vs. +0.2%e). The 10-year Treasury yield touched +2.182% intraday, its lowest since late June, before pulling back a little to trade +2.204% ahead of this morning's session.

In Europe, government bond yields have rallied +2-3 bps across the board, bouncing from their recent lows following stronger-than-expected Japanese growth.

Note: Stronger G7 data further supports expectations that the global economy is on the mend and central banks can start to unwind extraordinary monetary stimulus.

The yield on Germany's 10-year Bunds is up +3.5 bps to +0.42%.

In contrast, Japanese government bond prices mostly edged higher; shrugging off the stronger data to catch up to global market moves after Tokyo markets were closed on Friday. The 10-year cash JGB's yield inched down -0.5 bps to +0.050%.

4. Dollar gains some traction

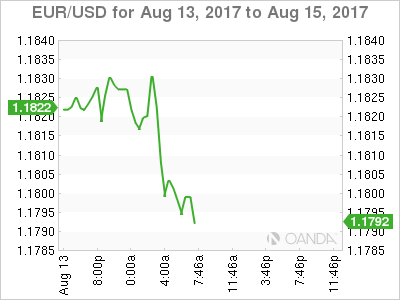

The mighty dollar trades a tad higher this Monday as tensions between the U.S and North Korea calm down a tad. This is keeping the EUR (€1.1800) down outright. However, the market remains a better EUR buyer on dips despite the fact that eurozone June industrial production came in worse-than-expected (see below).

Sterling (£1.2975) has dropped back below the psychological £1.3000 handle. Overall global equity strength has helped the USD/JPY (¥109.70) to strengthen. The pair has rebounded +100 pips from Friday lows.

The People's Bank of China (PBoC) strengthened the yuan to its strongest setting outright since September 2016. It was a fifth consecutive increase in the daily fix today by the PBoC amid continued dollar softness. The daily trading midpoint was put at ¥6.6601 as authorities try to guide market expectations of a firmer yuan.

5. Japan, China and Eurozone data

Overnight, Japan's economy grew in the Q2 at the fastest pace in more than two-years as consumer spending and capital expenditure both rose at the fastest in more than three years, highlighting stronger domestic demand. GDP expanded an annualized +4.0% in April-June, more than the median estimate for +2.5%.

In China, July industrial production came in lower than expected at +6.4% vs. +7.1%e – coal and power output all rose; while oil output fell. Other data showed that retail sales were also a bit weaker at +10.4% vs. +10.9%e.

In the Eurozone, industrial production for June was lower than expected, a hint that H2 may be slightly weaker than H1. Eurostat says the output of factories, mines and utilities was -0.6% lower than in May, while up +2.6% from the same month a year earlier. The market was looking for a -0.4% drop.

Euro Steady At 1.18, German Preliminary GDP Ahead

EUR/USD rose to the 1.18 line on Friday, and is showing little movement to start off the week. In the Monday session,the pair is trading at 1.1797, down 0.21% on the day. On the release front, it’s a quiet start to the week. In the Eurozone the sole event is Industrial Production, which came in at -0.6%, missing the estimate of -0.4%. On Tuesday, Germany releases Preliminary GDP, and the US publishes retail sales reports.

The euro continues to trade at high levels, and last week marked a fifth consecutive winning week for the currency. Tensions between North Korea and the US remain high, but the prevalent sentiment in the markets is that a diplomatic solution will be found to end the crisis. European stock markets have started the week with considerable gains, and EUR/USD is subdued in the Monday session. Still, Donald Trump and Kim Jon-un are unpredictable leaders, and any move by either side could easily ratchet up tensions and unnerve investors. Donald Trump continues to deal with domestic problems as well, and the White House faced stinging criticism from both Republicans and Democrats, as Trump failed to single out white supremacists for the violence in Charlottsville, Virginia, where one person was killed at a demonstration against far-right marchers.

For months, the ECB has consistently said that will not begin winding down its asset purchases program until inflation rises, but last month, the bank appeared to change its tune. In July, the ECB said it would hold discussions on the quantitative easing (QE) scheme in “the autumn”, and analysts are split as to whether that means September or October. Either way, this means that the markets expect to hear an announcement regarding QE. The bank tapered QE earlier in 2017, from EUR 80 billion to 60 billion/mth, and there are calls to reduce this to EUR billion/mth. The ECB is scheduled to terminate the asset purchases program in December, and could start tapering in early 2018. The bloc’s economy is forecast to expand a healthy 2.0% this year, and the eurozone outperformed both the US and the UK in the first half of 2017. The sore point remains inflation, which is stuck at low levels, despite the ECB’s ultra-accommodative monetary policy. Another factor which policymakers must deal with is the ECB’s bloated balance sheet, which stands at more than EUR 2 trillion.

Technical Outlook: WTI Oil Retests Key Fibo Support At $48.49 As N/T Risk Remains Shifted Lower

WTI oil's near-term action remains bearishly aligned and may revisit Friday's low at $47.98 (reinforced by 100SMA) as last Thursday's long red daily candle continues to weigh.

Oil price is attacking again strong support at $48.49 (Fibo 38.2% of $45.39/$50.41 upleg, currently reinforced by rising 20SMA) which contained multiple attacks in past two weeks and was cracked on Thu/Fri but without close below it so far.

Return to $47.98 pivot would further weaken near-term structure and risk further downside on sustained break lower.

At the upside, 10SMA turned south and offers initial resistance at $49.04, guarding 200SMA at $49.43 and psychological $50 barrier, which capped upside attempts during past two weeks.

Res: 48.88, 49.04, 49.43, 50.00

Sup: 48.24, 47.98, 47.31, 47.00