Sample Category Title

European Open Briefing: Asian Stocks Turned Lower

Global Markets:

- Asian stock markets: Nikkei fell 0.04 %, Shanghai Composite down 0.92 %, Hang Seng dropped 1.28 %, ASX 200 fell 0.21 %

- Commodities: Gold at $1282.71 (+0.27 %), Silver at $16.86 (+0.06 %), WTI Oil at $49.55 (-0.02 %), Brent Oil at $52.70 (+0.02 %)

- Rates: US 10-year yield at 2.24, UK 10-year yield at 1.10, German 10-year yield at 0.43

News & Data:

- Crude Oil Inventories -6.5 M vs -2.6 M expected

- RBNZ Interest Rate Decision 1.75 % vs 1.75 % expected

- GBP Rics House Price Balance 1 % vs 8 % expected

- CAD Building Permits m/m 2.5 % vs -1.8 %

- AUD MI Inflation Expectations 4.2 % vs 4.4 % previous

- North Korea calls Trump's warning a 'load of nonsense'- RTRS

- Japan PM should focus on regulatory reforms, say economists- RTRS

Markets Update:

Asian stocks turned lower reversing earlier gains on Thursday as investors continued to take risks off the table owing to the continued tensions between the United States and North Korea

EUR/USD was little changed and slipped down only about 0.1 percent in value to the lows of 1.1732 while the dollar index against a basket of major currencies added 0.1 percent to 93.620.

NZD/USD slipped to a near one-month low of $0.7300 losing 0.5 % after Reserve Bank of New Zealand Governor Graeme Wheeler’s comments on the NZ Dollar.

AUD/USD opened Asia 0.7991 after a steady session in the Wall Street, before reversing lower to revisit the session low at 0.7870 loosely tracked by the movements in the NZD.

USD/JPY after going as low as 109.560, its weakest in eight weeks. ticked a few points higher into the Tokyo fix time today, popping above 110.10 briefly before giving back some of its gains.

Upcoming Events:

- 08:30 GMT – (GBP) Manufacturing Production m/m

- 12:30 GMT – (USD) Unemployment Claims

- 12:30 GMT – (USD) PPI m/m

- 23:30 GMT – (AUD) RBA Gov Lowe Speaks

Market Update – Asian Session: RBNZ Assures Rate To Be Left On Hold For Now

Asia Summary

Asian equity markets opened slightly higher before falling nearly 1% across the board on continued tensions with North Korea. The US has affirmed that all options remain on the table when it comes to North Korea. USD took safety flows on the continued tension, though outside of the NZ$ there were no large moves. Moves likely to remain a bit volatile on thinner volume, as we exit the peak of earnings season and get knee deep in the largest summer holiday month. China’s yuan has been steadily appreciating recently, with today’s setting the highest since mid-September, and is up ~4% so far in 2017.

The Kiwi fell 0.7% to 0.7300 after RBNZ kept cash target rate unchanged at 1.75%. Gov Wheeler said that RBNZ is still very much Neutral on rates and for foreseeable future does NOT see OCR increasing. He did confirm monitors "traffic light system" for currency intervention 'closely', won't comment on whether currency strength is affecting the system. Later speaking to Parliament said intervention in FX market is always open to us, have intervened in the past, Then reiterated that he does not feel rate cut is needed at this time.

Key economic data

(NZ) New Zealand July Retail Card Spending M/M: -0.5% v 0.2% prior; Total Card Spending M/M: -0.7% v 8.3% prior

(JP) JAPAN JUN MACHINE ORDERS M/M: -1.9% V +3.6%E; Y/Y: -5.2% V -1.1%E

(JP) JAPAN JULY PPI M/M: 0.3% V 0.2%E; Y/Y: 2.6% V 2.3%E

(UK) JULY RICS HOUSE PRICE BALANCE: 1% V 9%E

Speakers and Press

China

(CN) Said that China Govt has summoned steel execs, regulators, bourse to discuss price surge - financial press

(CN) China propaganda chief visited govt workers holidaying at the resort of Beidaihe, signaling that an annual conclave of senior leaders was happening before an autumn party congress - Chinese press

Australia/New Zealand

(NZ) RBNZ Gov Wheeler: Still very much in Neutral on rates, for foreseeable future does NOT see OCR increasing; Structural factors weigh on inflation globally - post rate decision press conference

(NZ) RBNZ Gov Wheeler: Intervention in FX market is always open to us, have intervened in the past, always assessing criteria; Do not feel rate cut is needed - speaking to parliamentary committee

Korea

(KR) North Korea govt: our military will have a strike plan against Guam prepared by mid-August, then await orders from our leader

Japan

(JP) Japan publicly traded foreign stock investment trust total assets likely reached record high at end of July - Nikkei

Asian Equity Indices/Futures (00:00ET)

Nikkei -0.2%, Hang Seng -1.6%, Shanghai Composite -1.1%, ASX200 -0.1%, Kospi -1.1%

Equity Futures: S&P500 -0.3%; Nasdaq100 -0.4%, Dax -0.3%, FTSE100 -0.4%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1770-1.1733; JPY 110.18-109.89; AUD 0.7911-0.7870; NZD 0.7368-0.7299

Dec Gold +0.3% at 1,282/oz; Sept Crude Oil 0.0% at $49.55/brl; Sept Copper -0.1% at $2.93/lb

(CN) China PBOC OMO injects CNY90B in 7 and 14-day reverse repos v CNY140B prior; Injects net CNY30B v CNY0B prior

USD/CNY *(CN) PBOC SETS YUAN REFERENCE RATE AT: 6.6770 V 6.7075 PRIOR (strongest setting since Sept 29th)

Equities notable movers

Hong Kong/China

Wanda Hotel Development,169.HK To acquire Wanda Culture Travel Innovation from a company indirectly owned by Wang Jianlin for CNY6.3B – filing; +20.8%

Japan

Toshiba,6502.JP Reports Q1 Net ¥50.3B v ¥79.8B y/y, Op ¥96.7B v ¥16.3B Rev ¥1.14T v ¥1.06T y/y; +1.4%

Toshiba, 6502.JP Reports delayed FY16 results, Net loss ¥966B v loss ¥460B y/y, Rev ¥4.87T v ¥5.15T y/y

Shiseido, 4911.JP Reports H1 Net ¥18.8B v ¥24.5B y/y; Op ¥34.7B v ¥19.9B y/y; Rev ¥472.1B v ¥412.3B y/y; +14.%

Australia

Virgin Australia,VAH.AU Reports FY17 Net loss A$220.3M v loss A$260.9M y/y; Rev A$5.05B v A$5.02B y/y; +5.7%

Origin, ORG.AU To recognize ~A$1.2B non-cash impairment charge in H2 from ALPNG, sees A$357M impairment related to Lattice; -1.0%

AGL.AU Reports FY17 Underlying Profit A$802M v A$788Me; underlying EBIT A$1.37B v A$1.36Be; Rev A$12.6B v A$11.9Be; +1.2%

Boart Longyear, BLY.AU Reaches settlement with First Pacific Advisors; +9.4%

India

Tata Motors,TTMT.IN Reports Q1 (INR) Net 31.8B v 22.4B y/y, Rev 598.2B v 597.9Be; -4.6%

Australia’s Consumer Inflation Expectation Fell In August

For the 24 hours to 23:00 GMT, the AUD declined 0.34% against the USD and closed at 0.7888.

LME Copper prices rose 1.6% or $101.0/MT to $6465.0/MT. Aluminium prices rose 1.9% or $37.0/MT to $2018.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7883, with the AUD trading 0.06% lower against the USD from yesterday's close.

Early morning data showed that Australia's consumer inflation expectation dropped to 4.2% in August, following a reading of 4.4% in the previous month.

The pair is expected to find support at 0.7860, and a fall through could take it to the next support level of 0.7838. The pair is expected to find its first resistance at 0.7908, and a rise through could take it to the next resistance level of 0.7934.

Looking forward, a speech by the RBA Governor, Philip Lowe, scheduled overnight, will be keenly watched by market participants.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Euro Trading Lower In The Asian Session

For the 24 hours to 23:00 GMT, the EUR slightly declined against the USD and closed at 1.1759.

On the data front, Italy’s seasonally adjusted industrial production rose more-than-expected by 1.1% on a monthly basis in June, compared to market expectations for an advance of 0.2%. In the previous month, industrial production had recorded a rise of 0.7%.

In the US, data revealed that mortgage applications rebounded 3.0% in the week ended 04 August 2017, after recording a drop of 2.8% in the prior week.

In the Asian session, at GMT0300, the pair is trading at 1.1744, with the EUR trading 0.13% lower against the USD from yesterday’s close.

The pair is expected to find support at 1.1699, and a fall through could take it to the next support level of 1.1653. The pair is expected to find its first resistance at 1.1780, and a rise through could take it to the next resistance level of 1.1815.

In absence of any major macroeconomic releases in the Euro-zone today, investors will keep a close watch on the US initial jobless claims and the monthly budget statement for July, slated to release later in the day.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

UK’s RICS House Prices Rose At Its Slowest Rate In Over 4 Years In July

.

For the 24 hours to 23:00 GMT, the GBP rose 0.12% against the USD and closed at 1.3010.

In the Asian session, at GMT0300, the pair is trading at 1.3, with the GBP trading 0.08% lower against the USD from yesterday's close.

Overnight data indicated that Britain's RICS house price balance unexpectedly fell to a level of 1.0% in July, hitting its lowest since March 2013. In the prior month, house price balance recorded a level of 7.0%, while market participants were expecting for a rise to a level of 9.0%.

The pair is expected to find support at 1.2971, and a fall through could take it to the next support level of 1.2943. The pair is expected to find its first resistance at 1.3028, and a rise through could take it to the next resistance level of 1.3057.

Ahead in the day, traders will look forward to Britain's total trade balance, manufacturing as well as industrial production and NIESR GDP estimate data, to gauge strength in the nation's economic activity.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Japan’s Machinery Orders Surprisingly Fell In June, Tertiary Industry Index Remained Flat In The Same Month

For the 24 hours to 23:00 GMT, the USD declined 0.15% against the JPY and closed at 109.96.

On the data front, Japan's preliminary machine tool orders recorded a rise of 26.3% on an annual basis in July. In the prior month, machine tool orders had risen 31.1%.

In the Asian session, at GMT0300, the pair is trading at 110.07, with the USD trading 0.1% higher from yesterday's close.

Overnight data indicated that the nation's machinery orders unexpectedly dropped 1.9% on a monthly basis in June, compared to a drop of 3.6% in the prior month, while markets were anticipating for a gain of 3.6%. Meanwhile, the nation's tertiary industry index remained flat in July, compared to a fall of 0.1% in the prior month. Market participants had expected the index to rise 0.2%.

The pair is expected to find support at 109.69, and a fall through could take it to the next support level of 109.32. The pair is expected to find its first resistance at 110.31, and a rise through could take it to the next resistance level of 110.56.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Swiss Franc Reverses Its Gains In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.93% against the CHF and closed at 0.9637.

The Swiss Franc jumped against the USD, as excessive geopolitical fears surrounding North Korea lured investors to the safe-haven appeal of the currency.

In the Asian session, at GMT0300, the pair is trading at 0.9655, with the USD trading 0.19% higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9607, and a fall through could take it to the next support level of 0.9559. The pair is expected to find its first resistance at 0.9708, and a rise through could take it to the next resistance level of 0.9761.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Canada’s Housing Starts Surprisingly Climbed In July, Building Permits Recorded An Unexpected Rise In June

For the 24 hours to 23:00 GMT, the USD rose 0.24% against the CAD and closed at 1.2698.

Macroeconomic data indicated that Canada's seasonally adjusted housing starts surprisingly advanced to a level of 222.3K in July, defying market expectations for a fall to a level of 205.0K and highlighting resilience in the nation's housing market. In the prior month, housing starts had recorded a revised level of 212.9K. Moreover, the nation's building permits unexpectedly climbed 2.5% on a monthly basis in June, amid increased plans for commercial buildings. Building permits registered a revised rise of 10.7% in the previous month, while markets had envisaged for a drop of 1.9%.

In the Asian session, at GMT0300, the pair is trading at 1.2713, with the USD trading 0.12% higher against the CAD from yesterday's close.

The pair is expected to find support at 1.2680, and a fall through could take it to the next support level of 1.2648. The pair is expected to find its first resistance at 1.2733, and a rise through could take it to the next resistance level of 1.2754.

Ahead in the day, the release of Canada's new house price index for June, will be on investors' radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages

Elliott Wave View: FTSE 100 Pullback In Progress

Short term FTSE 100 ( UKX-FTSE ) Elliott Wave view suggests that Minor wave B ended on 6/30 low 7302.7 and the rally from there is unfolding as a double three Elliott wave structure where wave ((w)) ended at 7515.12 and wave ((x)) pullback ended at 7338.2. Index has reached 100% from 6/30 low so cycle is mature and Minor wave 1 has ended at 7551.85. Index is currently pulling back in Minor wave 2 to correct cycle from 6/30 low before the rally resumes. As far as pivot at 7302.7 low remains intact, Index should find buyers in the sequence of 3, 7, or 11 swing at 7361.91 – 7427.76 area for further upside. If pivot at 7302.7 low fails during later pullback, the Index would be still remain in the same cycle from 6/2 peak. Index should then extend the correction to the downside. We don’t like selling the Index.

FTSE 1 Hour Elliott Wave Chart

7 swings structure is one of the most common patterns in the theory of New Elliott Wave & it is also mainly know as double three Elliott Wave pattern. Market find that very often nowadays in many instruments in almost all time frames. It is a very reliable structure by which we can make a good analysis and what is more important is giving us good business inputs with clearly defined levels invalidation and destination areas.

The image below shows what Elliott wave pattern Double Three looks like. It has (W), (X), (Y) and 3,3,3 internal structure, which means that all these 3 legs are corrective sequences. Each (W), (X) and (Y) are made of three waves, which are having the structure W, X, Y in lesser degree as well. Elliott Wave principle is a form of technical analysis that traders use to analyze the cycles of financial markets and market trends forecast by identifying extremes in investor psychology, high and low prices, and other collective factors. Important to Note that 3 waves could also be labeled ABC (5-3-5) structure as well. How are labeled 3 waves it depends on the internal price structure subdivisions waves i.e. whether the price action is corrective or motive.

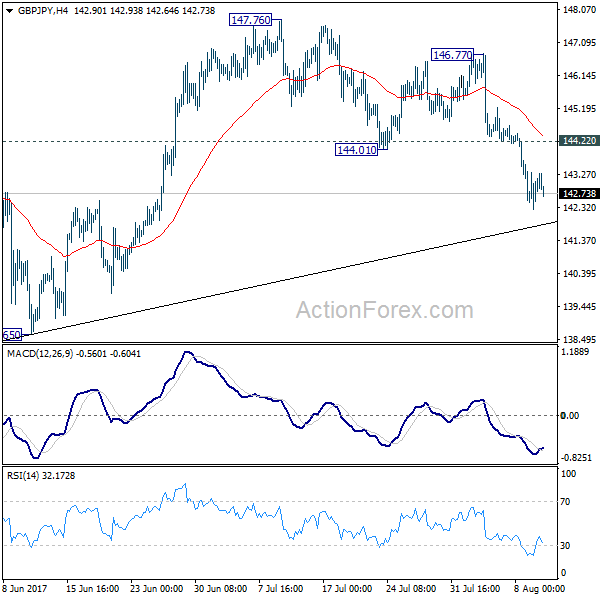

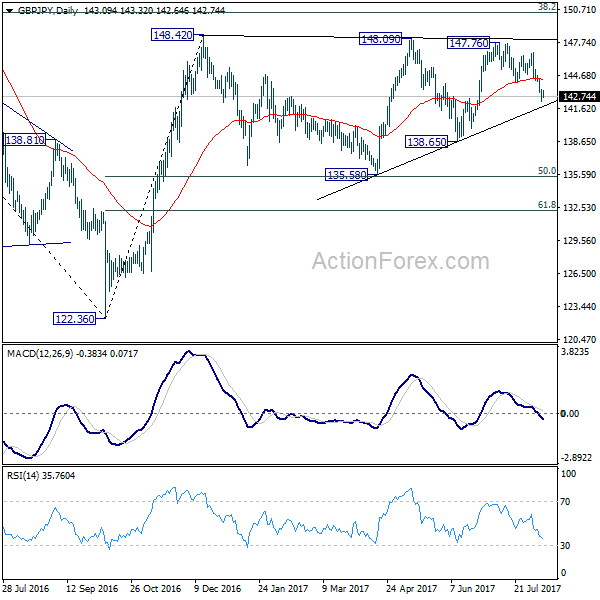

GBP/JPY Daily Outlook

Daily Pivots: (S1) 142.45; (P) 142.91; (R1) 143.55; More

GBP/JPY's fall from 147.76 is still in progress for trend line support (now at 141.87). Break there will target 135.58/138.65 support zone. As GBP/JPY is seen as staying in consolidation pattern from 148.42, we'd expect strong support from 135.58 to contain downside. On the upside, above 144.20 minor resistance will argue that the decline from 147.76 might be completed. In such case, intraday bias will be turned back to the upside for rebound.

In the bigger picture, rise from medium term bottom at 122.36 is expected to continue to 38.2% retracement of 196.85 to 122.36 at 150.43. Decisive break there will carry long term bullish implications and pave the way to 61.8% retracement at 167.78. In case the sideway pattern from 148.42 extends, we'd be looking for strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside.