Sample Category Title

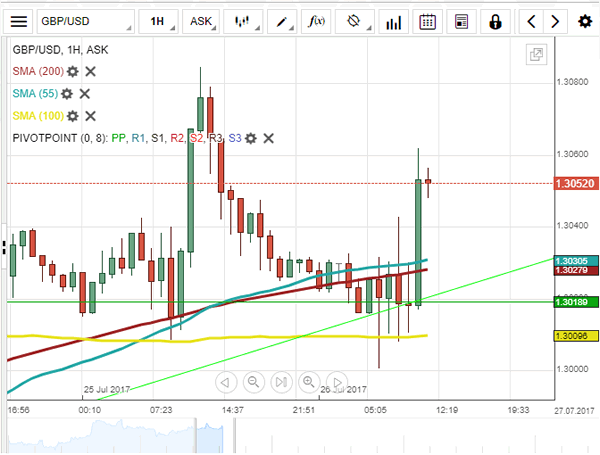

GBP/USD Analysis: Awaits Fundamentals

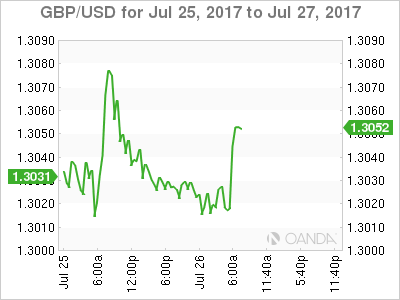

The Pound was relatively steady on Tuesday morning, being supported by the weekly PP and the 55– and 200-hour SMAs circa 1.3015. However, this stable equilibrium changed mid-session when the rate shot up near the 1.3080 mark. This upward motion was not sustainable, as the price was pressured back to the aforementioned levels. By and large, the Sterling continues to move in an up-trend. Daily technical indicators suggest that it should trade higher in respect to Wednesday morning, trying to reach the weekly R1 at 1.3104. However, some minor depreciation may still occur. In case the rate breaches the trend-line, a fall down to the bottom wedge boundary is expected. Nevertheless, two sets of important fundamentals are to be released today.

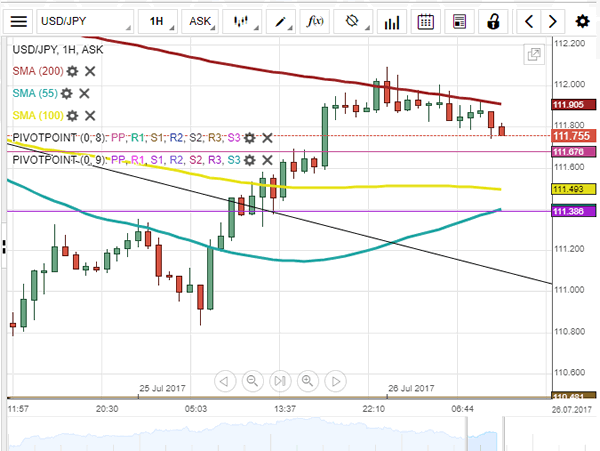

USD/JPY Analysis: Breaches Channel

On Tuesday, solid upside risks pushed the Greenback through three resistance levels, namely, the 55– and 100-hour SMAs and the weekly PP. As a result, a two-week descending channel was breached to the upside. The given momentum north was halted by the 200-hour SMA at the 112.00 mark. Despite several attempts, the rate failed to move past this level. However, trend indicators are still signalling a strong up-trend; thus, the 200-hour SMA may eventually be breached, setting the weekly R1 at 112.34 as the ultimate upside barrier for this session. Meanwhile, an immediate support is provided by the weekly PP at 111.68. This level is likely to be breached if bears prevail; thus, an intersection of the 100-hour SMA and the monthly PP is a more probable downside limit.

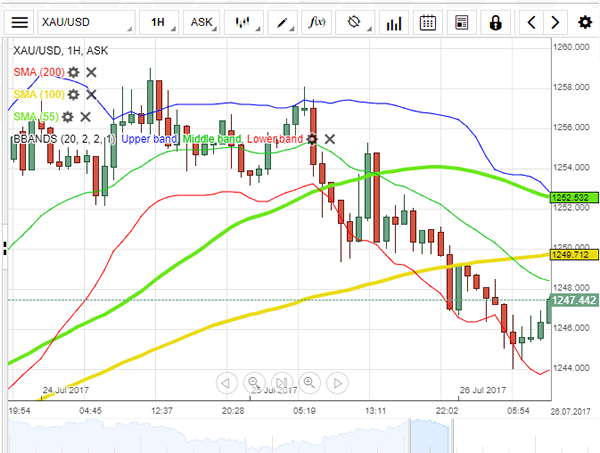

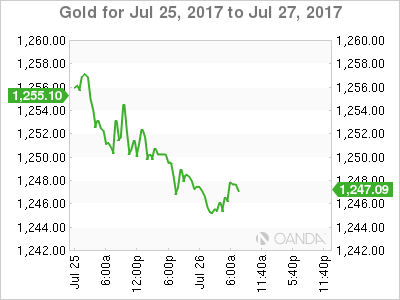

XAU/USD Analysis: Breaks Pattern

The strength of the monthly pivot point has proven itself to be strong enough to force the yellow metal's price into breaking the ascending channel pattern, which guided the bullion since July 11. The commodity price has not only passed the support of the ascending channel, but also various other support levels. Among them are the 55 and 100-hour simple moving averages and the weekly PP. On Wednesday morning the yellow metal had passed one of the last support levels before setting out to plummet down below the 1,240 mark. However, the fall of the bullion might be stopped by the 200-hour SMA, which was located at the 1,241.25 level during the early hours of the day's trading session.

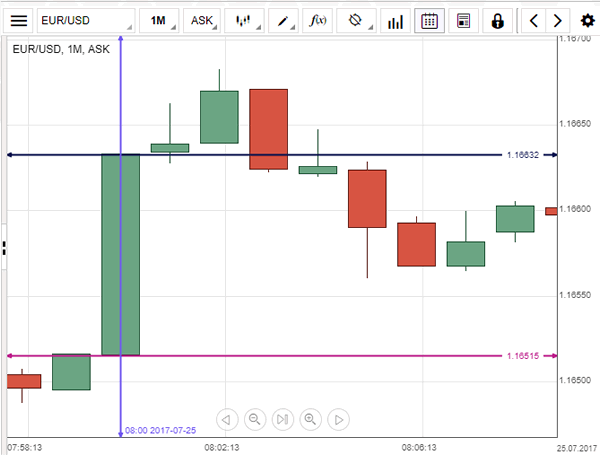

EUR/USD: German Ifo Business Climate

German business morale reached its record-high in July, which contributed to the appreciation of the EUR/USD exchange rate. Right after the better-than-expected data was published, the Euro zone's currency strengthened against the US Dollar by 11 base points to reach 1.1663. The Ifo German Business Climate Index surged to 116.0 points, while analysts' anticipated it to decrease to 114.9 from 115.2 points registered in the preceding month. Overall, sentiment among German businesses remained upbeat and is expected to improve further. Moreover, Germany is set to show strong growth in the Q2 with higher private consumption and construction activity.

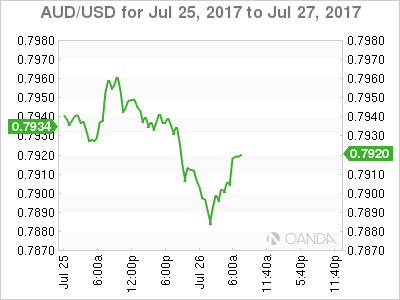

Australian CPI Q/Q

The Australian Dollar weakened against its American counterpart after the official report released by the Australian Bureau of Statistics showed that the country's consumer inflation growth slowed in the second quarter. At the moment of the data release, the AUD/USD currency pair fell by 0.16% to hit the 0.7900 level. The Consumer Price Index weakened to 0.2% in the Q2, missing expectations for a 0.4% expansion, as lower prices of oil and reduced travel and accommodation costs undercut the pace of growth. The Reserve Bank of Australia expressed doubts that inflation would reach its 2% target in the foreseeable future, suggesting keeping interest rates at the same level this and next year.

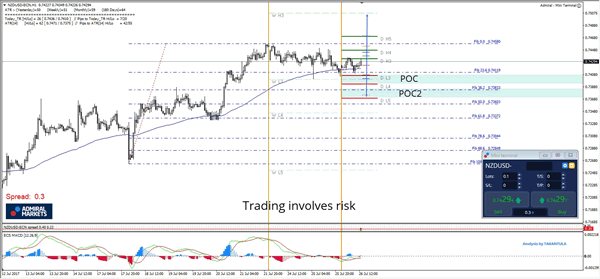

Daily Technical Analysis: NZD/USD 2 POC Zones For Possible Rejections

The NZD/USD has been in a steady uptrend and we can see the price above W L3 and D L3. The POC zones that we see at this point are clearly shown on the chart as POC 1 and POC 2. The POC1 0.7390-0.7405 (D L3, W L3, 23.6,EMA89) and POC2 0.7370 – 80 (ATR low, 38.2, D L5) could reject the price and as long as the price is above W L4 0.7345 , the bulls will have the upper hand. Targets are 0.7470 and 0.7505.

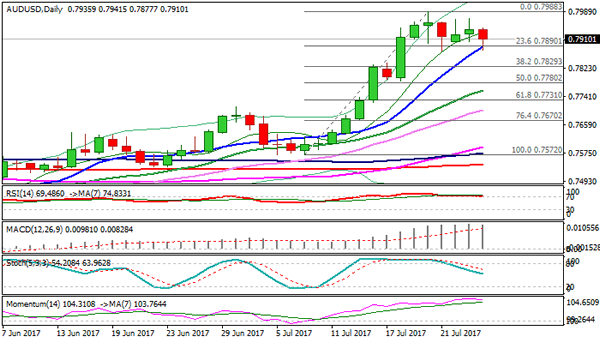

Technical Outlook: AUDUSD – Limited Downside Attempts For Now

The Aussie dollar eased in early Wednesday's trading after inflation in Australia missed its forecasts in the second quarter (Q2 CPI 0.2% q/q vs 0.4% f/c, annualized at 1.9% vs 2.2% f/c) but dips were contained just above last Friday's low at 0.7875.

Rising thick 4-hr cloud also underpins the action, as probes below cloud top (0.7902) were so far short-lived.

Immediate downside risk will be minimized while supports at 0.7900/0.7875 hold, while break lower would risk extension towards 0.7856 (rising daily Tenkan-sen) and pivotal support at 0.7830 (Fibo 38.2% of 0.7527/0.7988 upleg).

Firm break here is needed to sideline larger bulls and signal deeper correction.

Res: 0.7941, 0.7970, 0.7988, 0.8000

Sup: 0.7900, 0.7875, 0.7856, 0.7830

D-Day For The Fed

Wednesday July 26: Five things the markets are talking about

What to expect from the Fed statement today?

Note: There is no press conference and the Fed minutes in a couple of weeks will provide fuller details.

Today's statement is likely to provide the following signals on three issues:

1. Caution ahead

Recent rhetoric from many of the voting members would suggest that on the U.S economic outlook that they are more cautious and a tad less confident about the strength of the economic recovery, pointing to headwinds to both higher growth and inflation.

The 'big' dollars recent demise is expected to help out on both accounts, but not enough to offset the concerns about Trumponomics (pro-growth policies that include tax reform and infrastructure spend).

2. Rates – to maintain a tightening bias

Despite the cautious tone, the Fed is not prepared to abandon its tightening bias theme any time soon – expect them to reiterate at least one more hike in 2017 (consensus expects December). But, this is expected to be quantified – more sensitive and more data dependent.

3. Balance Sheets: Prepping the market.

The Fed will continue to prepare markets for the beginning this year of a gradual shrinkage in their balance sheets through a reduction in its holdings of U.S Treasury and mortgage securities.

Expect them to downplay the potential impact on the market by signalling that the reduction will be very slow.

1. Stocks mixed results

Global equity markets are mixed after yesterday's lackluster session with the focus on today's Fed statement.

In Japan, strong earnings supported the Nikkei (+0.5%), rising for the first time in four sessions, but gains were capped by profit taking ahead of Fed decision.

In Hong Kong, shares rallied despite profit taking, helped by energy stocks. The benchmark Hang Seng index finished +0.3% higher, while the Hang Seng China Enterprises Index was up +0.5%.

In China, blue-chip stocks fell for a second consecutive day overnight on investor fears of further regulatory tightening. The blue-chip CSI300 index fell -0.4%, while the Shanghai Composite Index was little changed, up +0.1%.

In Europe, indices trade higher following generally positive earnings out of Europe. The Swiss SMI, FTSE and CAC are outperforming.

U.S stocks are expected to open little changed (+0.1%).

Indices: Stoxx600 +0.5% at 382.8, FTSE 0.6% at 7476, DAX +0.4% at 12306, CAC-40 +0.6% at 5190, IBEX-35 0.3% at 10550, FTSE MIB 0.2% at 21509, SMI +0.7% at 9002, S&P 500 Futures 0.1%

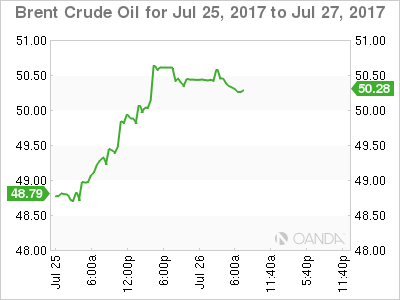

2. Oil prices are firmer on optimism of declining stocks

Oil prices again firmed overnight, holding atop of their two month highs hit on Tuesday, on expectations of a drawdown in U.S stocks and as a rise in shale oil production shows signs of slowing.

Brent crude has rallied +41c, or +0.8%, to +$50.61 a barrel, after rallying more than +3% in yesterday's session. U.S West Texas Intermediate futures have climbed +49c, or +1%, to +$48.38 a barrel.

Data from the API yesterday showed that U.S crude stocks fell sharply last week as refineries boosted output, while gas inventories increased and distillate stocks decreased.

Crude inventories declined by -10.2m barrels in the week ending July 21 to +487m, compared with expectations for a decrease of -2.6m barrels.

Prior to yesterday's inventory report, crude prices had been supported by Monday's OPEC announcement by the Saudi's that they would limit its crude exports to +6.6m bpd next month, almost -1m bpd below the levels of a year ago, while Nigeria voluntarily agreed to cap or cut its output from +1.8m bpd, once it stabilizes at that level – up to now, Nigeria had been exempt from the output cuts.

However, current price levels may be soon capped, as it's a level that could attract increased U.S shale oil production.

Next up is this morning's EIA inventory report at 10:30 am EDT. Consensus is looking for a drawdown of -3.3m barrels.

Gold prices are steady (fell -0.1% to +$1,246.94 per ounce) as investors await U.S Fed policy statement. The market is looking for any comment regarding inflation for directional guidance.

3. Yields await Fed

U.S government bonds pulled back for their second consecutive session yesterday, signalling an end to its recent rally amid continued focus on a possible shift by G7 members towards a tighter monetary policy.

Putting further pressure on prices is a large volume of new Treasury notes being sold this week, and the Fed's pending policy statement (2:00 pm EDT). U.S policy makers are not expected to hike rates, but the market is looking for any change in tone from policy makers, especially since they have leaned towards being a little 'dovish' in recent weeks. U.S 10-year yield is trading atop of +2.31%.

Note: The U.S Treasury will sell +$34B 5-year notes today and +$28B 7-year notes Thursday.

Elsewhere, Germany's 10-year Bund yield has fallen -2bps to +0.55%, while U.K Gilts yield has declined -3 bps to +1.232%.

Down-under, Australia's Q2 CPI data overnight showed that core inflation remains well below the +2-3% targeted by the RBA, which suggests that rates should be kept on hold for some time. Aussie futures suggest that there is +54.5% chance that the RBA will keep rates on hold until May 2018.

4. Dollar tame ahead of Fed statement

Sterling (£1.3016) has dipped after data this morning showed the U.K. economy expanded at a meager pace (see below). EUR/GBP trades at €0.8928.

Australia's muted inflation is being attributed to weaker wages and lower fuel costs. The AUD has fallen -0.5%, trading atop of its overnight lows of €0.7892. RBA Governor Lowe warned that there could be financial stability risks from “additional easing.” He also reiterated preference for a weaker currency.

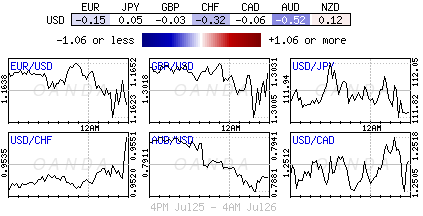

The EUR has inched lower in early U.S trade, down -0.14% to €1.1630. On the release front, there are no events out of the eurozone. Markets are waiting for the Fed's rate announcement.

5. U.K economy posts lackluster growth

Data this morning showed that U.K economic growth remained subdued in Q2, expanding at a +0.3% q/q pace, as weak performances from the manufacturing and construction industries offset an improvement in services.

It's a slight improvement on the +0.2% growth rate of Q1, but still less than half the pace of growth at the end of 2016.

Note: The headline print was in line with consensus and the data covers the first three-months of the two-year Brexit negotiation period.

On an annualized basis, growth accelerated to +1.2%, from +0.9% in Q1.

Digging deeper, the expansion was driven largely by an improvement in services, which grew +0.5%.

DAX Moves Higher, Fed Statement Looms

The DAX index has posted gains for a second straight day. In Wednesday’s European session, DAX is trading at 12,308.00, up 0.36% on the day. On the release front, there are no events out of the eurozone. In the US, the Federal Reserve releases its rate statement and is expected to maintain the benchmark at 1.25%. On Thursday, Germany releases GfK Consumer Climate, which is expected to remain unchanged at 10.6 points.

German indicators continue to point higher, underscoring a strong German economy. On Tuesday, German Ifo Business Climate climbed higher, as the indicator strengthened for a sixth straight month. The indicator hit another record high of 116.0, surprising the markets which had forecast a small drop from the previous reading. Clements Fuest, president of the Ifo Institute, continues to use superlatives to describe the German economy, calling sentiment in the business sector “euphoric”. Fuest added that optimism in the business sector is at its highest since Germany’s reunification. The robust economy has been the locomotive behind a reinvigorated eurozone economy, with stronger growth and lower unemployment. The marked improvement in economic conditions in the eurozone has sent the euro soaring, as the currency is up 9.8% since March 1. Although, the strong euro has not put a dent in business sentiment, this has not been the case with German stock markets. The high exchange rate has weighed on exporters’ shares, such as European automakers, and the DAX has declined 2.7% since June 1.

The Federal Reserve concludes its monthly policy meeting on Wednesday, and is not expected to alter its interest rate policy. However, traders should not assume this will be a non-event. The rate statement will be under careful scrutiny, as analysts will be looking for any references to the “I” word. Inflation continues to hover around 1.4% (based on the Fed’s calculations), well below the Fed target of 2%. In June, Janet Yellen described low inflation as “transitory”, but recent comments from Yellen and other policymakers have shifted in tone, an apparent acknowledgment that inflation may remain stuck at low levels. This has raised doubts as to whether the Fed will indeed raise rates one more time this year. No move is expected before December, and the odds of a December hike have fallen to just 37%, according to the CME Group. If today’s rate statement fails to reassure the markets that a December hike is planned, investors could respond by selling dollar-denominated assets in favor of other currencies or gold.

Aside from interest rates, Fed members will be discussing when to commence tapering the Fed’s $4.2 trillion bond portfolio. The bloated balance sheet is a result of the aggressive quantitative easing program which was put in place after the financial crisis in 2008. In June, the Fed outlined plans to taper purchases, with experts circling September as the start date of the reduction. This would involve the Fed tapering the purchases of Treasury bonds and mortgage securities, with an initial taper likely of $10 billion/month. Analysts expect the taper to begin in September, so we could see the Fed make reference to this in the July statement.

Market Update – European Session: UK Q2 Advance GDP In-Line But Shows Lackluster Growth

Notes/Observations

Fed decision in focus. Dealers await for clues on whether the Fed might raise rates again this year, and when it will begin paring its massive bond portfolio

European confidence data mixed (France misses, Italy beats)

UK Q2 Advance GDP in-line with consensus (QoQ: 0.3%; YoY: 1.7%

RBA will not be peer-pressured into tightening policy

Overnight

Asia:

Australia Q2 CPI data softer than expected; Q/Q: 0.2% v 0.4%e; Y/Y: 1.9% v 2.2%e

Reserve Bank of Australia (RBA) Gov Lowe: RBA does not need to follow other central banks in policy moves. Welcomed a recent pick up in the labour market, although subdued wages and high household debt meant that policy rates would stay lower for longer

Bank of Japan Deputy Gov Nakaso: Reiterates still long way to go to meet 2% inflation target and will persistently pursue current powerful easing

Europe:

EU Commissioner Oettinger (Germany): the UK is legally obligated to pay for the current EU budget, and the assumption is that UK payments to continue. UK leaving EU will create €10-12B gap in EU budget after 2020

Americas:

House of Representatives approved new sanctions bill on Russia, Iran and North Korea (as expected)

Republicans secured enough votes to begin debate on Healthcare vote

Senate Republican plan to repeal and replace Obamacare failed to get votes needed for approval (43 in favor and 57 against). Senate rejected the health-bill amendment with the Cruz and Portman plans

President Trump: Chair Yellen is definitely still in the running for the new Fed Chair term; Economic adviser Cohn and two or three other candidates remain potential

Energy:

Weekly API Oil Inventories: Crude: -10.2M v +1.63M prior

Economic Data

(JP) Japan July Small Business Confidence: 50.0 v 49.8e (1st non-contraction in 4 months)

(SG) Singapore Jun Industrial Production M/M: 9.7% v 3.6%e; Y/Y: 13.1% v 8.5%e

(CH) Swiss Jun UBS Consumption Indicator: 1.38 v 1.32 prior

(FR) France July Consumer Confidence: 104 v 108e

(ES) Spain Jun Adjusted Retail Sales Y/Y: 2.5% v 2.2%e; Retail Sales Y/Y: 2.8% v 3.9% prior

(DK) Denmark Jun Retail Sales M/M: No est v 0.1% prior; Y/Y: No est v 1.6% prior

(SE) Sweden Jun Trade Balance (SEK): 4.3B v 1.8B prior

(IT) Italy July Consumer Confidence Index: 106.7 v 106.3e; Manufacturing Confidence: 107.7v 107.0e; Economic Sentiment: 105.5 v 106.3 prior

(CH) Swiss July Credit Suisse Survey Expectations: 34.7 v 20.7 prior

(UK) Q2 Advance GDP Q/Q: 0.3% v 0.3%e; Y/Y: 1.7% v 1.7%e

(UK) Jun BBA Loans for House Purchase: 40.2K v 40.0Ke

Fixed Income Issuance:

(IN) India sold total INR170B vs. INR170B indicated in 3-month and 6-month Bills

(EU) ECB alloted $35M in 7-day USD Liquidity Tender at fixed 1.65% vs $85M prior

(IT) Italy Debt Agency (Tesoro)sold €2.0B vs. € 1.5-2.0B indicated range in zero coupon May 2019 CTZ bonds; Avg yield: -0.160% v -0.167% prior; Bid-to-cover: 1.64x v 1.56x prior

(IT) Italy Debt Agency (Tesoro sold €1.25B vs. €0.75-1.25B indicated range in 1.3% Mar I/L 2028 Bonds (BTPei); Avg Yield: 1.24% v 1.21% prior; Bid-to-cover: 1.39x v 1.67x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.5% at 382.8, FTSE 0.6% at 7476, DAX +0.4% at 12306, CAC-40 +0.6% at 5190, IBEX-35 0.3% at 10550, FTSE MIB 0.2% at 21509, SMI +0.7% at 9002, S&P 500 Futures %]

Market Focal Points/Key Themes: European Indices trade higher following generally positive earnings out of Europe. The Swiss SMI, FTSE and CAC outperform with notable gains from PSA Group following strong results and guidance, whilst Daimler trades flat after falling slightly shy of estimates. In the UK ITV, Tullow Oil and Compass group all trade higher following solid results, whilst in Switzerland Lafarge Holcim trades slightly lower after lowering demand outlook and Lonza shares surge following a 15% rise in H1 sales. Looking ahead to the US morning notable earners include Ford, Boeing, Anthem and Thermo Fisher.

Equities

Consumer discretionary [ ITV [ITV.UK] +2.2% (Earnings)]

Consumer Staples [Compass Grp [CPG.UK] +1.8% (Earnings) ]

Materials: [Lonza [LONN.CH] +5.7% (Earnings), LafargeHolcim [LHN.CH] -1.3% (Earnings)]

Industrials: [PSA Grp [UG.FR] +4.0% (Earnings), Daimler [DAI.DE] +0.4% (Earnings), Thales [HO.FR] +3.5% (Earnings) ]

Technology: [ST Micro [STM.FR] +1.3% (Earnings), Atos [ATO.FR] +1.9% (Earnings)]

Telecom: [KPN [KPN.NL] +2.8% (Earnings)]

Energy: [Tullow Oil [TLW.UK] +3.3% (Earnings)]

Speakers

Chancellor of Exchequer Hammond (Fin Min): Cannot be complacent on growth and focus on restoring productivity

Russia Senator Kosachyov: Russia must prepare a "painful" response to US sanctions; there can be no improvement in Russia/US ties after new sanctions, relations to only worsen

Sweden Alliance (opposition) called for no-confidence vote against three ministers (Defense, Infrastructure and Interior)

China govt said to be planning rollover of CNY600B in bonds that back the sovereign fund that come due in Aug

Currencies

USD consolidated its recent losses ahead of the Fed rate decision later today. Dealers await for clues on whether the Fed might raise rates again this year, and when it will begin paring its massive bond portfolio

The GBP had little reaction as UK Q2 Advance GDP as the data was in-line with consensus. GBP/USD drifted lower towards 1.3010 in the aftermath.

AUD currency was softer during the Asian session after Australia Q2 core inflation remained well below the 2-3% targeted by the RBA, which meant that rates should be kept on hold for some time. AUD/USD hovering around the 0.79 area, -0.5%

Fixed Income

Bund futures trade at 161.89 down 28 ticks but still holding the July 20th low of 161.55. Resistance lies near the 162.75 level followed by 163.50. A break of the 160.00 support level could see lows target 159.25 followed by 157.50.

Gilt futures trade at 125.99 up 28 ticks, with a limited reaction to UK Q2 advance GDP reading Price finds key support at the 125.42 support level. An acceleration lower could test the 122.88 region. Resistance remains the noted 126.51 region, followed by 127.50.

Wednesday's liquidity report showed use of the marginal lending facility rose to €496M from €250M prior.

Corporate issuance saw $5.95B come to market via 4 issuers headlined by Codelco $2.75B 2-part senior note offering and Crown Castle $1.75B 2- part senior unsecured note offering.

Looking Ahead

(CO) Colombia Jun Retail Confidence: No est v 15.3 prior; Industrial Confidence: No est v -8.8 prior

(BR) Brazil July CNI Consumer Confidence: No est v 100.5 prior

05:30 (EU) ECB Long-Term Refinancing Operation Result

06:45 (US) Daily Libor Fixing

07:00 (RU) Russia to sell combined RUB30B in 2020 and 2022 OFZ Bonds

07:00 (US) MBA Mortgage Applications w/e July 14th: No est v +6.3% prior

08:00 (UK) Baltic Dry Bulk Index

08:30 (CL) Chile Central Bank's Traders Survey

09:30 (ZA) South Africa 6th summer-crop output forecast

10:00 (US) Jun New Home Sales: 615Ke v 610K prior

10:30 (US) Weekly DOE Crude Oil Inventories

11:30 (BR) Brazil weekly Currency Flows Weekly

11:30 (US) Treasuries to Sell 2-Year Floating Rate Notes

13:00 (US) Treasuries to Sell 5-Year Notes

14:00 (US) FOMC Interest Rate Decision: Expected to leave Interest Rates unchanged

14:30 (US) Fed Chair Yellen post rate decision press conference

16:00 (BR) Brazil Central Bank (BCB) Interest Rate Decision: Expected to cut Selic Target Rate by 100bps to 9.25%