Sample Category Title

Market Update – Asian Session: OPEC And Non-OPEC Officials Meet In Russia Amid Concerns Over The Global Supply

Asia Summary

The markets were mixed in the region, with the USD weaker as the US/Russia investigation related to President Trump’s election continues to widen and Jared Kushner will face a closed door hearing with the US Senate Intelligence Committee today. This combined with the lack of progress on the healthcare bill and tax reform puts US growth into question. The IMF confirmed doubts with its updated GDP forecasts. US was cut for both 2017 and 2018. Canada was raised and given the strongest outlook for 2017. UK was also cut, while France, Germany and Italy were raised.

China increased cash injections through its daily reverse repurchase operations by injecting CNY350B in 7-day and 14-day (the most funds in five weeks), this followed money rates rising last week. According to regional analysts CNY540B of reverse repos are coming due this week and such liquidity is likely to remain tight. Bank of Japan (BOJ) cut its 5-10 year JGB purchases to ¥470B from ¥500B. Markets reacted little as the markets have been expecting a reduction in purchases, though considered a bit earlier than expected.

Key economic data

(JP) JAPAN JUL PRELIM PMI MANUFACTURING: 52.2 V 52.4 PRIOR FINAL (8-month low)

(HK) Macau Jun Visitors 2.38M, -7.5% m/m; +0.9% y/y

Speakers and Press

China

(CN) China Academy of Social Sciences (CASS) report says Q3 GDP may grow 6.8% y/y; Q4 6.7% and 2017 6.8% - Chinese Press

(CN) China Iron and Steel Association (CISA) VP Xinchuang: China should be bold in protecting the interests of its own businesses

USD/CNY (CN) PBOC Adviser: Yuan exchange rate may appreciate in H2

Hong Kong

(HK) Hong Kong Monetary Authority (HKMA) said to have checked property developers' loans

Korea

(KR) South Korea parliament approves KRW11T extra budget plan Sunday July 23rd

(KR) South Korea said to seek capital gains tax increase for large shareholders - South Korean Press

Japan

(JP) In the local Sendai City mayoral elections, opposition candidate Kazuko Kori won - financial press

(JP) Japan Cabinet approval ratings decline in press polls: According to Mainichi Japan Cabinet approval rating fell 10ppts to 26%

Other

OPEC and non-OPEC officials to meet amid mounting concerns over global supply - financial press

OPEC Secretary-General Barkindo: While the rebalancing process may be proceeding at a slower than projected pace, it is expected to accelerate in H2

Asian Equity Indices/Futures (00:00ET)

Nikkei -0.9%, Hang Seng +0.5%, Shanghai Composite +0.2%, ASX200 -0.7%, Kospi -0.2%

Equity Futures: S&P500 -0.2%; Nasdaq -0.2%, Dax -0.2%, FTSE100 -0.2%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1684-1.1658; JPY 111.20-110.77; AUD 0.7931-0.7904; NZD 0.7456-0.7433

Aug Gold 0.0% at 1,254/oz; Aug Crude Oil +0.2% at $45.85/brl; Sept Copper +0.1% at $2.72/lb

(JP) Bank of Japan (BOJ) cuts JGB buying of 5-10 yr to ¥470B from ¥500B

(CN) China PBOC OMO injects CNY350B in 7 and 14 day reverse repos v CNY140B prior

USD/CNY (CN) PBOC SETS YUAN REFERENCE RATE AT V 6.7410 V 6.7415 PRIOR

(KR) South Korea sells 20-year government bonds, avg yield 2.29%

(TH) Thailand sells THB20B in 3-month and 6-month treasury bills

Equities notable movers

Australia

Newcrest Mining,NCM.AU Reports Q4 gold production 552K ozs, -7.8% q/q; copper production 13kt, -41.3% q/q; +1.8%

Hong Kong/China

China Power International,2380.HK Profit Warning: H1 Profit to decrease over 70% y/y; -5.4%

Japan

Tokyo Electric Power, 9501.JP Underwater robot has captured images of what is likely to be melted nuclear fuel at the bottom of one of its damaged reactors – Nikkei; -0.4%

South Korea

Ottogi Corp,007310.KR Strength attributed to invitation to high-level business meeting with President Moon; +7.3%

Samsung Electronics,005930.KR Said to have cut FY17 TV target to 45M units (prior 48M units) - Korean press; -0.6%

Other

BMW, BMW.DE Denies claims it formed a cartel with Daimler and Volkswagen to hold down the prices of crucial technology and that they had agreed to install emissions equipment that was inadequate to do the job - financial press

Aussie Dollar Trading Higher In The Morning Session

For the 24 hours to 23:00 GMT, the AUD declined 0.44% against the USD and closed at 0.7916 on Friday.

LME Copper prices rose 1.2% or $71.5/MT to $6001.5/MT. Aluminium prices rose 0.2% or $3.0/MT to $1901.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7921, with the AUD trading 0.06% higher against the USD from Friday’s close.

The pair is expected to find support at 0.7885, and a fall through could take it to the next support level of 0.7848. The pair is expected to find its first resistance at 0.7948, and a rise through could take it to the next resistance level of 0.7974.

Amid a lack of any macroeconomic releases in Australia today, trading trend in the AUD is expected to be determined by global macroeconomic events.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Euro Trading A Tad Lower, Ahead Of The Markit Manufacturing And Services PMIs Data Across The Euro-Zone

For the 24 hours to 23:00 GMT, the EUR rose 0.36% against the USD and closed at 1.1670 on Friday.

In the Asian session, at GMT0300, the pair is trading at 1.1668, with the EUR trading slightly lower against the USD from Friday’s close.

The pair is expected to find support at 1.1633, and a fall through could take it to the next support level of 1.1599. The pair is expected to find its first resistance at 1.1693, and a rise through could take it to the next resistance level of 1.1719.

Going ahead, investors will look forward to the flash Markit manufacturing and services PMIs for July across the Euro-zone, slated to release in a few hours. Moreover, in the US, preliminary Markit manufacturing and services PMIs for July, followed by existing home sales data for June, due to release later in the day, will garner significant amount of market attention.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Britain’s Public Sector Net Borrowing Registered A Higher-Than-Anticipated Deficit In June

For the 24 hours to 23:00 GMT, the GBP rose 0.23% against the USD and closed at 1.2993 on Friday.

In economic news, data showed that UK's public sector net borrowing posted a more-than-expected deficit of £6.3 billion in June, from a revised deficit of £6.4 billion in the prior month, while markets were anticipating public sector net borrowing to record a deficit of £4.2 billion.

In the Asian session, at GMT0300, the pair is trading at 1.301, with the GBP trading 0.13% higher against the USD from Friday's close.

The pair is expected to find support at 1.2973, and a fall through could take it to the next support level of 1.2935. The pair is expected to find its first resistance at 1.3034, and a rise through could take it to the next resistance level of 1.3057.

In absence of any crucial economic releases in the UK today, investor sentiment will be governed by global macroeconomic factors.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japan’s Manufacturing Sector Growth Slowed To An 8-Month Low In July

For the 24 hours to 23:00 GMT, the USD declined 0.7% against the JPY and closed at 111.11 on Friday.

In the Asian session, at GMT0300, the pair is trading at 111.05, with the USD trading marginally lower against the JPY from Friday's close.

Overnight data indicated that Japan's flash Nikkei manufacturing PMI dropped to a level of 52.2 in July, expanding at its weakest pace in eight months, amid weakness in export orders. The PMI had registered a level of 52.4 in the previous month.

The pair is expected to find support at 110.52, and a fall through could take it to the next support level of 109.99. The pair is expected to find its first resistance at 111.83, and a rise through could take it to the next resistance level of 112.61.

Looking ahead, traders will await the release of the Bank of Japan's (BoJ) June meeting minutes, scheduled tomorrow.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading Lower This Morning

.

For the 24 hours to 23:00 GMT, the USD declined 0.66% against the CHF and closed at 0.9452 on Friday.

In the Asian session, at GMT0300, the pair is trading at 0.9464, with the USD trading 0.13% higher against the CHF from Friday's close.

The pair is expected to find support at 0.9429, and a fall through could take it to the next support level of 0.9394. The pair is expected to find its first resistance at 0.9509, and a rise through could take it to the next resistance level of 0.9554.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Canadian Annual Inflation Grew At Its Weakest Pace In Nearly 2 Years In June

For the 24 hours to 23:00 GMT, the USD declined 0.46% against the CAD and closed at 1.2538 on Friday.

The Canadian Dollar gained ground, after Canada's retail sales rose more-than-anticipated by 0.6% MoM in May, climbing for the third straight month. Retail sales had recorded a revised rise of 0.7% in the previous month, while markets were expecting for a gain of 0.3%.

On the other hand, the nation's consumer price index (CPI) rose less-than-expected by 1.0% on an annual basis in June, advancing at its weakest pace since October 2015 and undershooting market expectations for an advance of 1.1%. In the previous month, the CPI had recorded a rise of 1.3%. In the Asian session, at GMT0300, the pair is trading at 1.2545, with the USD trading 0.06% higher against the CAD from Friday's close.

The pair is expected to find support at 1.2508, and a fall through could take it to the next support level of 1.2472. The pair is expected to find its first resistance at 1.2595, and a rise through could take it to the next resistance level of 1.2646.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

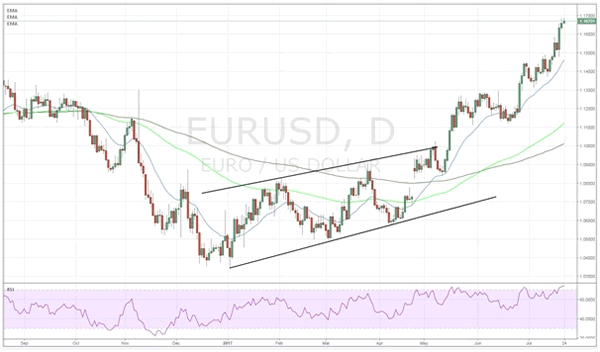

Euro To Remain Bullish In The Week Ahead

Key Points:

- Euro continues to rally following hawkish ECB statement.

- Minor support at 1.1588 remains in place.

- Watch for a continued move towards 1.18 in the week ahead.

The Euro continued to rally strongly last week and currently shows no sign of topping or a loss of momentum. Much of the bullishness came late in the week when the ECB’s Mario Draghi suggested that Eurozone growth and employment continues to strengthen and hinted that the bank could review QE in the near future. Subsequently, the EURUSD rallied strongly to close the week out around the 1.1661 mark but it remains to be seen if the currency can retain this directional bias in the week ahead.

The Euro remained strongly predisposed to the upside throughout most of last week as the pair continued to rally without a top or slowdown in sight. The primary trend driver was some statements from the ECB’s venerable Chairman, Mario Draghi, who suggested that EU growth and employment remained bright spots. In addition, he hinted that the central bank may review their QE and asset purchase program in the near term. This sent the Euro Dollar rallying sharply as speculation continues to grow that the ECB could potentially consider tapering or reducing their stimulus programs during September’s meeting. Subsequently, the Euro shot sharply higher and continued to rally late into the week, finishing around the 1.1661 mark.

Looking ahead, it’s set to be another volatile week for the EURUSD with the EU Services PMI and U.S. FOMC decision due for release. The Services PMI will be a relatively interesting figure to watch given the renewed upside risks for the Eurozone economy. The official estimate has the indicator coming in around the 54.3 mark, which would again represent growth, and further support the Euro. However, the primary event for the coming week is likely to be the U.S. FOMC decision which is likely to determine the pair’s near term fundamental trend. Most economists are predicting that the central bank will sit pat at 1.25% but watch for any jawboning in the statements following the event as volatility could ensure.

From a technical perspective, the Euro Dollar continues to roar higher and there appears to be little sign, at this stage, of a top forming. Subsequently, our initial bias for the week ahead remains bullish as long as minor support at 1.1582 remains intact. However, it should be noted that the RSI Oscillator is currently strongly overbought and may need a period of moderation in due course. Regardless, the medium term view still remains strongly bullish for the Euro and we might just see the 1.18 handle yet.Support is currently in place for the pair at 1.1478, 1.1381, and 1.1313. Resistance exists on the upside at 1.1713 1.1872, and 1.1977.

Ultimately, the coming week is likely to only bring with it increased opportunities for the Euro Dollar as it seems relatively likely that we could see a move towards the 1.18 handle. However, there could be plenty of volatility around as the Fed gets ready to meet to, potentially, jawbone the market. Subsequently, watch your positioning as Janet Yellen has been fairly apt at moving the market with her rhetoric of late.

AUD’s Future Uncertain Ahead Of FOMC

Key Points:

- After another bullish week, the AUDUSD may need to cool-off.

- The Fundamental outlook is somewhat bearish moving forward.

- Technical bias is mixed.

The AUD had yet another strong rally last week which left many traders scratching their heads given that there was little to explain the aggressive move. Nevertheless, the week's performance isn't entirely without explanation which might be worth delving into before we take a look at what is next on the agenda. Additionally, it might pay to examine what is going on technically as this is likely to have an impact on the pair moving forward.

Starting with last week, the Aussie Dollar continued to post record gains, smashing through its 2-year high to close the week out at the 0.7912 handle. Whilst many other majors posted strong gains over the past 7 days, what saw the AUDUSD stand out was the fact that almost all of its overall upsides accrued on Tuesday. Whilst some of this is undoubtedly due to the weaker USD, the majority of the sentiment swing reflects the pricing in of rather hawkish meeting minutes from the RBA. Indeed, contrary to the broader market trend, the pair actually spent the remainder of the week moderating away some of this surprise upswing, despite the generally on-target Australian Unemployment rate outcome of 5.6% and the dip in the US Philadelphia Federal Manufacturing index to 19.5.

As for what lies ahead, Wednesday is poised to be a highly volatile session for the Aussie Dollar as important economic news is due out for both sides of the quote. On the AUD side of things, the CPI data is set to be posted and is expected to show a y/y increase to 2.2%. Obviously, if this forecast is achieved it will help the pair to recover some of the losses incurred late last week, maybe even seeing the 0.7950 handle challenged again. However, also due out during the session is the FOMC's Interest rate decision which could be highly disruptive if the Fed opts to defy expectations and lift rates once again. Nevertheless, we are also expecting a large uptick in the US GDP figure to 2.6% on Friday which could undo any bullishness seen earlier in the week.

On the technical front, it's a bit of a mixed bag for the AUD which could see the pair enter a near-term ranging phase unless a major fundamental upset is seen. On the one hand, the EMA bias and the parabolic SAR are rather buoyant and should help to recruit the bulls as the week opens. On the other hand, we can't escape the fact that the pair is highly overbought and it is well and truly above its 2-year high which could see traders spook ahead of the FOMC meeting. If this is the case, we expect near-term losses to be limited as the 2016 high could act as a support moving forward. More precisely, support should be strongest around the 0.7890, 0.7836, and 0.7778 levels. In contrast, resistance should be clear at the 0.7956, 0.7984, and 0.8035 levels.

Overall, our outlook is rather mixed going forward and we are likely to be relying on the fundamentals more than the technicals to inform price action in the week to come. As mentioned, the FOMC and the US GDP data are likely to be the key things to watch for and both of these are likely to put pressure on the AUDUSD.

Oil Output Cut Deal Amid Higher Production In Nigeria And Libya

Market Movers Today

Today, focus will be on global PMI figures for July. In the euro area, we look for a slight ly weaker manufacturing PMI although it should stay at a high level, signalling continued robust GDP growth. The service PMI should also be a bit weaker but still point s to ongoing solid demand from consumers.

In the US, we estimate PMI manufacturing rose slightly as it has been much weaker than ISM and regional PMIs recent ly. Still, the level is likely to stay lower than the peak earlier this year.

OPEC is due to meet today to discuss the oil output cut deal amid higher production in Nigeria and Libya.

Jared Kushner, Senior Adviser to President Trump and married to Ivanka Turmp is due to appear before the Senate Intelligence Commit tee in connect ion with the Russian probe today. However, the hearing will not be public, so there will be no headlines.

The main event this week is the FOMC meeting on Wednesday. We do not expect any policy changes (and no announcement on quantitative tightening yet ) at this meeting, although risks are skewed towards a slightly more dovish statement given inflation continues to disappoint .

Focus will also be on German Ifo expectations, Q2 GDP growth figures in the UK, US and France as well as German HICP inflation. In Scandi markets, the key data releases will be Norwegian unemployment and Swedish GDP growth in Q2.

Selected Market News

On Friday, Der Spiegel wrote that German car companies have run a secret cartel since the1990s. The EU Commission is looking into the claim, which could lead potentially to high fines to the companies (10% of global turnover).

In France, Emmanuel Macron's approval rating has fallen 10 percent age point s t o 54%, the second biggest fall so soon after an elect ion on record, underlying that it may not be so easy for him to win popular support for his plans to reform France.

On Saturday, Poland's upper house passed the controversial law, which put s t he juridical syst em under polit ical cont rol, with 55 votes out of 100. The EU is threatening Poland with Article 7 (losing voting rights) and demonstrations in Poland in front of the Polish parliament continue.

Ahead of European and US PMIs later today, Japanese PMI manufacturing fell to 52.2 in July from 52.4, the lowest since November 2016.

The ‘summer mode' in the primary market means lower-than-normal activity; however, today, Belgium will be in the market with a tap in the 23s, the 27s and the 47s. On Friday , Italy will be coming to the market with its usual month-end tap in 5Y and 10Y.