Sample Category Title

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD, GOLD, WTI CRUDE, DJIA, FTSE100, DAX

EUR/USD

The American dollar started the second quarter with a positive tone, edging higher against all of its major rivals this Monday, although holding not far from its recent lows. The EUR/USD pair retreated further after reaching a year high of 1.1445 late last week, settling in the 1.1360 region, in spite of strong EU data released early Europe. The final revision of the EU June Markit manufacturing PMIs showed that the sector's growth extended into the end of the second quarter, with the index up to 57.4, a fresh six-year high, and above flash estimate of 57.3. Across the region, readings were mixed with the German index up to 59.6, its highest in 74 months according to Markit, while Spain and French figures suffered modest downward revisions. Unemployment in the EU surged to 9.3% in May, above previous 9.25, but below from the 10.2% printed a year earlier. The dollar found support after the US opening in the ISM manufacturing report, as according to it, economic activity expanded for the 97th consecutive month, up to 57.8 in June from previous 54.9.

The EUR/USD pair fell down to 1.1355 before paring losses, with selling interest limited after an early US close ahead of the July 4th holiday. From a technical point of view, the pair has broken below the 23.6% retracement of last week's rally, now the immediate resistance at 1.1380, but more relevant, the pair is retreating after approaching a major long-term resistance, the 1.1460 region, as the pair has been unable to surpass it pretty much since January 2015. Short term, the 4 hours chart shows that the price has also broken below a now horizontal 20 SMA, whilst the Momentum indicator keeps heading south within bearish territory, and the RSI indicator heads south at 46, supporting some further slides ahead. The immediate support comes at 1.1340, the 38.2% retracement of the mentioned rally, followed by Thursday's low of 1.1290. Below this last, an interim top will be confirmed, anticipating some additional declines for the following sessions.

Support levels: 1.1340 1.1290 1.1250

Resistance levels: 1.1380 1.1420 1.1460

USD/JPY

The American dollar started the second quarter with a positive tone, edging higher against all of its major rivals this Monday, although holding not far from its recent lows. The EUR/USD pair retreated further after reaching a year high of 1.1445 late last week, settling in the 1.1360 region, in spite of strong EU data released early Europe. The final revision of the EU June Markit manufacturing PMIs showed that the sector's growth extended into the end of the second quarter, with the index up to 57.4, a fresh six-year high, and above flash estimate of 57.3. Across the region, readings were mixed with the German index up to 59.6, its highest in 74 months according to Markit, while Spain and French figures suffered modest downward revisions. Unemployment in the EU surged to 9.3% in May, above previous 9.25, but below from the 10.2% printed a year earlier. The dollar found support after the US opening in the ISM manufacturing report, as according to it, economic activity expanded for the 97th consecutive month, up to 57.8 in June from previous 54.9.

The EUR/USD pair fell down to 1.1355 before paring losses, with selling interest limited after an early US close ahead of the July 4th holiday. From a technical point of view, the pair has broken below the 23.6% retracement of last week's rally, now the immediate resistance at 1.1380, but more relevant, the pair is retreating after approaching a major long-term resistance, the 1.1460 region, as the pair has been unable to surpass it pretty much since January 2015. Short term, the 4 hours chart shows that the price has also broken below a now horizontal 20 SMA, whilst the Momentum indicator keeps heading south within bearish territory, and the RSI indicator heads south at 46, supporting some further slides ahead. The immediate support comes at 1.1340, the 38.2% retracement of the mentioned rally, followed by Thursday's low of 1.1290. Below this last, an interim top will be confirmed, anticipating some additional declines for the following sessions.

Support levels: 1.1340 1.1290 1.1250

Resistance levels: 1.1380 1.1420 1.1460

GBP/USD

The American dollar started the second quarter with a positive tone, edging higher against all of its major rivals this Monday, although holding not far from its recent lows. The EUR/USD pair retreated further after reaching a year high of 1.1445 late last week, settling in the 1.1360 region, in spite of strong EU data released early Europe. The final revision of the EU June Markit manufacturing PMIs showed that the sector's growth extended into the end of the second quarter, with the index up to 57.4, a fresh six-year high, and above flash estimate of 57.3. Across the region, readings were mixed with the German index up to 59.6, its highest in 74 months according to Markit, while Spain and French figures suffered modest downward revisions. Unemployment in the EU surged to 9.3% in May, above previous 9.25, but below from the 10.2% printed a year earlier. The dollar found support after the US opening in the ISM manufacturing report, as according to it, economic activity expanded for the 97th consecutive month, up to 57.8 in June from previous 54.9.

The EUR/USD pair fell down to 1.1355 before paring losses, with selling interest limited after an early US close ahead of the July 4th holiday. From a technical point of view, the pair has broken below the 23.6% retracement of last week's rally, now the immediate resistance at 1.1380, but more relevant, the pair is retreating after approaching a major long-term resistance, the 1.1460 region, as the pair has been unable to surpass it pretty much since January 2015. Short term, the 4 hours chart shows that the price has also broken below a now horizontal 20 SMA, whilst the Momentum indicator keeps heading south within bearish territory, and the RSI indicator heads south at 46, supporting some further slides ahead. The immediate support comes at 1.1340, the 38.2% retracement of the mentioned rally, followed by Thursday's low of 1.1290. Below this last, an interim top will be confirmed, anticipating some additional declines for the following sessions.

Support levels: 1.1340 1.1290 1.1250

Resistance levels: 1.1380 1.1420 1.1460

GOLD

Dollar's recovery sent gold tumbling this Monday, with spot ending the day around $1,221.00 a troy ounce, its lowest settlement since early May. A recovery in the USD-index after reaching a 9-month low last week alongside with a sharp advance in US Treasury yields undermined the precious metal, while a strong US manufacturing report revived hopes for a soon-to-come rate hike in the US. The technical picture has turned strongly bearish for the commodity, as the daily chart shows that it settled below its 200 DMA for the first time since mid May, whilst a bearish 20 DMA is crossing below the 100 DMA far above the current level. In the same chart, technical indicators head south within negative territory, approaching oversold readings , and also in line with additional slides ahead. In the 4 hours chart, the price is developing below all of its moving averages, with the 20 SMA gaining bearish momentum around 1,241.80, and technical indicators moderating their declines in oversold territory, rather reflecting the low volumes at this time of the day than suggesting downward exhaustion.

Support levels: 1,219.30 1,211.10 1,203.80

Resistance levels: 1,224.40 1,236.50 1,241.80

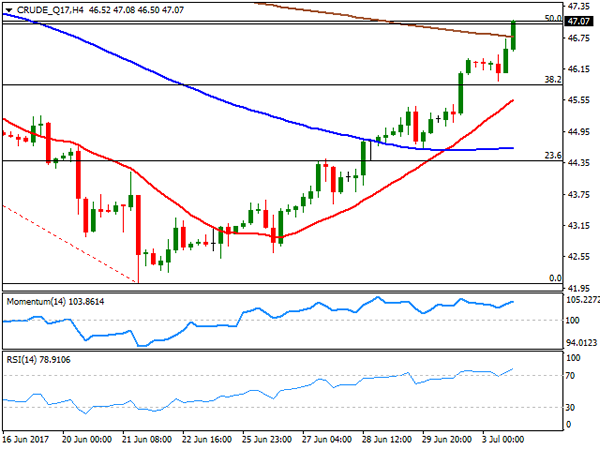

WTI CRUDE OIL

West Texas Intermediate crude oil futures closed the day at $47.05 a barrel, its highest settlement in nearly four weeks, up for an eighth straight session in a row, and despite news indicating that OPEC's output surged in June to the highest for this year. Most of the increase came from Libya and Nigeria, both countries exempted from the cut deal. News late last week, indicating that US production has decreased keep supporting the commodity that retains the positive tone seen on the previous update, given that in the daily chart, technical indicators continue heading higher within positive territory, whilst the price extended well-above its 20 SMA, now hovering around the 50% retracement of its latest daily decline. In the 4 hours chart, technical indicators accelerated their advances within overbought levels, whilst the price surpassed its 200 SMA for the first time since late May, further supporting additional gains towards 48.15, the 61.8% retracement of the mentioned slide.

Support levels: 46.30 45.80 45.20

Resistance levels: 47.60 48.15 48.80

DJIA

US indexes closed mixed, with the Nasdaq Composite down 30 points, to 6,110.06 amid a decline in tech-related equities, but the Dow Jones Industrial Average settled at 21,479.27, up 129 points and after setting a record high intraday of 21,563. The S&P also closed up at 2,429.01, advancing 0.23%. Gains were led by financials and energy-related equities, and within the Dow, Goldman Sachs was the best performer, up 2.42%, followed by JPMorgan that added 2.04%. Chevron, El du Pont and Exxon Mobil, all added over 1.50%. Microsoft was the worst performer, down 1.10%, followed by Intel that shed 0.83%. Technically, the daily chart for the DJIA shows that the index recovered after hovering around a bullish 20 DMA during the last days of the past week, whilst technical indicators have bounced from their mid-lines, with a limited upward potential ahead of Tuesday's holiday. In the 4 hours chart, the index settled above all of its moving averages, but given the strong retracement ahead of the close, technical indicators have lost upward strength, with the RSI already turning lower, but both within positive territory, limiting chances of a steeper decline ahead.

Support levels: 21,420 21,361 21,310

Resistance levels: 21,462 21,506 21,563

FTSE100

The FTSE 100 closed the day at 7,377.09, up roughly 65 points amid a continued advance in oil prices and a weaker Pound. The Footsie put a halt to a 4-day slide, helped further by a recovery in a mining sector. Glencore led advancers, settling 5.01% higher, followed by Rio Tinto and Anglo American that added 4.0% each. Provident Financial, on the other hand, was the worst performer, closing 2.67% lower, followed by Micro Focus International that lost 1.85%. The daily chart for the London benchmark shows that the index was unable to recover above its 100 DMA, whilst the 20 DMA continues heading south above the largest, and technical indicators have bounced modestly from near oversold levels, but are still within negative territory, all of which suggests that the risk remains towards the downside. In the 4 hours chart, the risk is also towards the downside, given that an early advance was contained by a bearish 20 SMA, currently at 7,380, while technical indicators hover within bearish territory, with no certain directional strength.

Support levels: 7,331 7,294 7,256

Resistance levels: 7,380 7,424 7,452

DAX

The German DAX advanced 1.22% or 152 points at the beginning of the week to settle at 12,471.31, with all European index closing with gains as banks and mining-related equities led the way higher. The Markit manufacturing PMI was revised higher in Germany, up to 59.6 from 59.5 in May, the highest in 74 months according to the official report. Commerzbank was the best performer within the DAX, up 4.29%, followed by ThyssenKrupp that added 4.01%. Vonovia topped losers' list, with a 0.89% decline. The recovery was not enough to revert the negative tone in the benchmark, as in the daily chart, it remains well below a bearish 20 DMA, whilst technical indicators have barely lost downward strength, holding near oversold readings. In the same chart, a light of hope comes from the fact that the price has extended its bounce from its 100 DMA. Shorter term, and according to the 4 hours chart, the upside also seems limited as the intraday advance stalled well-below a still strongly bearish 20 SMA, whilst technical indicators resumed their declines within negative territory, after correcting oversold readings.

Support levels: 12,420 12,364 12,310

Resistance levels: 12,448 12,490 12,542

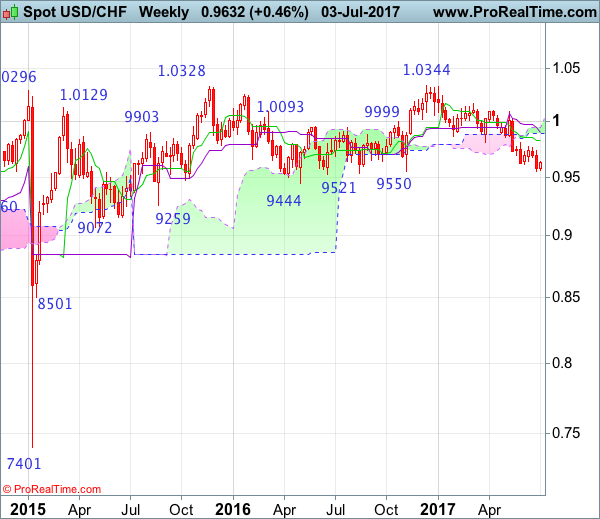

USD/CHF Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting star

• Time of formation: 7 Mar 2017

• Trend bias: Sideways

Daily

• Last Candlesticks pattern: Morning star

• Time of formation: 9 May 2017

• Trend bias: Near term up

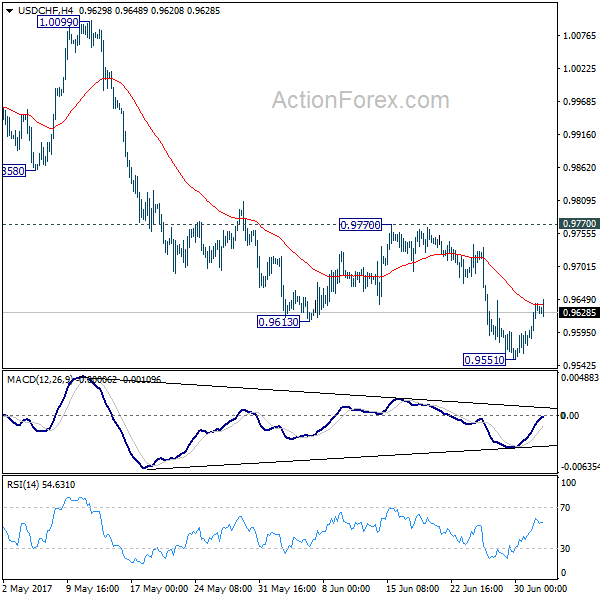

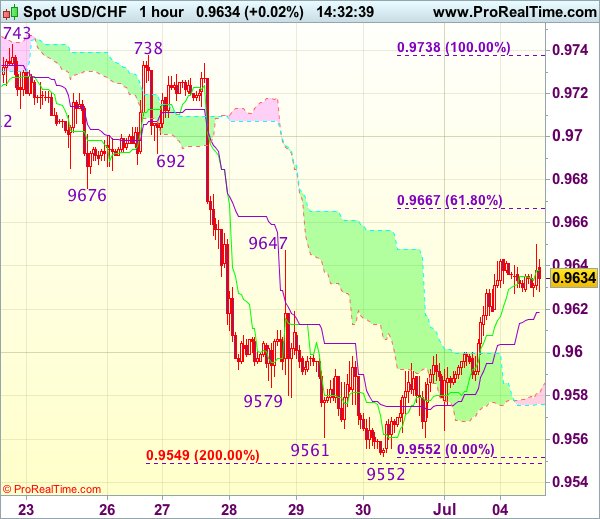

USD/CHF – 0.9628

Although the greenback resumed recent decline and fell to as low as 0.9552 (just held above previous chart support at 0.9550), the subsequent rebound formed a white candlestick yesterday and consolidation above this level would be seen, above the Tenkan-Sen (now at 0.9648) would bring test of the Kijun-Sen (now at 0.9680) but a daily close above this level is needed to add credence to this view, bring retracement of recent decline to 0.9700, then test of 0.9738 resistance. A break above there would encourage for a stronger rebound to previous resistance at 0.9771 but reckon resistance at 0.9808 would hold on first testing.

On the downside, whilst pullback to 0.9590-00 cannot be ruled out, said support at 0.9552 should hold and bring another rebound to aforesaid retracement targets. Below indicated support at 0.9550-52) would signal recent decline from 1.0344 top (2016 high) is still in progress and may extend further weakness to psychological support at 0.9500, having said that, loss of downward momentum should prevent sharp fall below another previous chart support at 0.9444 and risk from there has increased for a rebound later.

Recommendation: Buy at 0.9600 for 0.9800 with stop below 0.9500

On the weekly chart, although the greenback dropped again last week to as low as 0.9552, dollar needs to penetrate support at 0.9550 to retain bearishness and extend the decline from 1.0344 to 0.9500, then towards another previous support at 0.9444, however, loss of near term downward momentum should prevent sharp fall below 0.9400 and reckon 0.9350 would hold from here, risk from there has increased for a rebound later.

On the upside, although initial recovery to 0.9700 and then 0.9735-40 cannot be ruled out, reckon resistance at 0.9808 would limit upside and bring another decline. A weekly close above the Tenkan-Sen (now at 0.9826) would defer and risk a stronger rebound to 0.9940-50 but 1.0007 (previous resistance) should limit upside and price should falter well below 1.0100, bring another selloff later. Above 1.0100 would signal low is formed instead and suggest the aforesaid decline from 1.0344 has ended, bring test of 1.0171 resistance next.

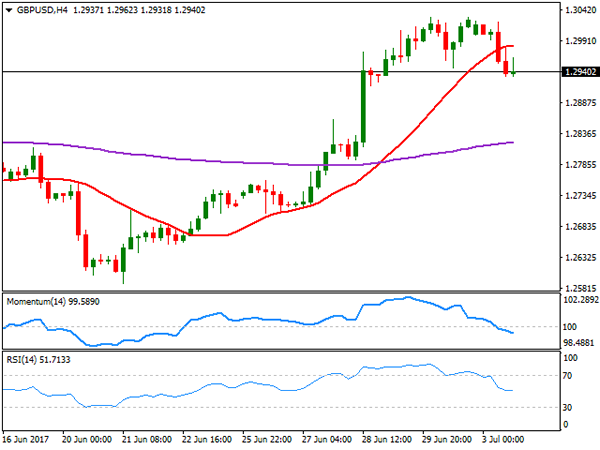

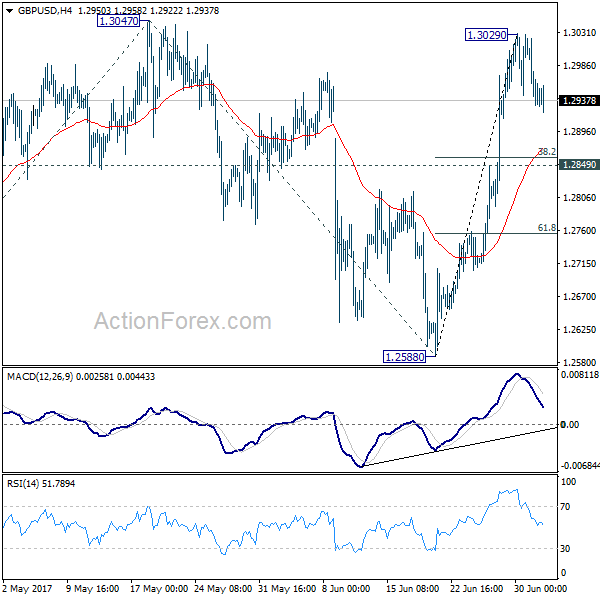

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2904; (P) 1.2963; (R1) 1.2996; More...

Intraday bias in GBP/USD remains neutral as consolidation from 1.3029 continues. At this point, deeper retreat cannot be ruled out. But downside should be contained above 1.2849 support to bring rise resumption. Break of 1.3029 should then send GBP/USD through 1.3047 to 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168 next.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is now in favor, overall outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9590; (P) 0.9616; (R1) 0.9661; More......

USD/CHF's recovery is still in progress and is pressing 4 hour 55 EMA. Further rise cannot be ruled out, but still, upside of recovery should be limited below 0.9770 resistance and bring resumption. Below 0.9551 will extend the decline from 1.0342 to 0.94443 key support level. At this point, we'd expect strong support from there to bring rebound.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

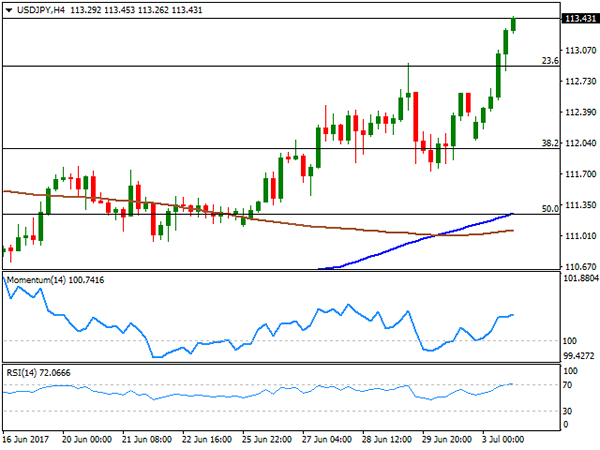

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.46; (P) 112.97; (R1) 113.88; More...

With 111.72 minor support intact, near term outlook is USD/JPY remains bullish for further rise to 114.36 resistance. Current development suggest that whole corrective pull back from 118.65 has completed at 108.12 already. Break of 114.36 will confirm this bullish view and target 118.65 again. On the downside, break of 111.72 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85.

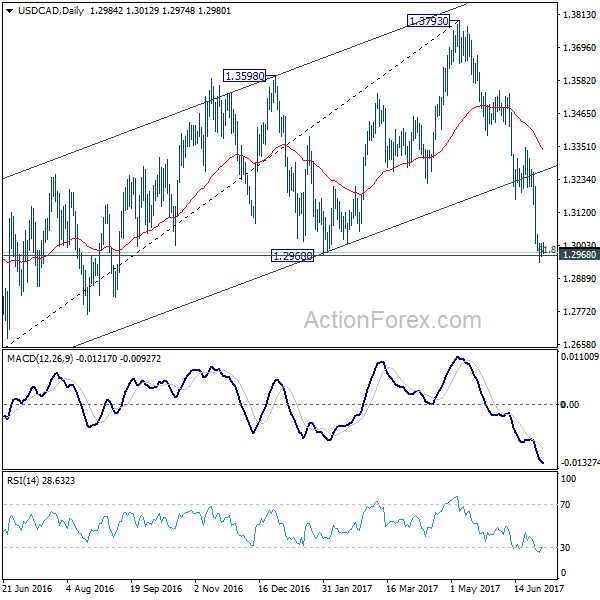

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2976; (P) 1.2994; (R1) 1.3023; More....

No change in USD/CAD's outlook as it's gyrating in tight range around 1.3 cluster support. With 1.3045 minor resistance intact, further decline is expected. Sustained trading below 1.2968 cluster support, 61.8% retracement of 1.2460 to 1.3793 at 1.2969 will pave the way to retesting 1.2460 low. On the upside, above 1.3045 will indicate short term bottoming, possibly on bullish convergence condition in 4 hour MACD. In such case, stronger rebound would be seen back to 1.3164/3346 resistance zone first, before staying another decline.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The second leg should have finished at 1.3793. Break of 1.2460 will tend such correction to 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. However, firm break there will target 100% projection of 1.4689 to 1.2460 from 1.3793 at 1.1564.

Trade Idea : USD/CHF – Buy at 0.9590

USD/CHF - 0.9625

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9636

Kijun-Sen level : 0.9619

Ichimoku cloud top : 0.9584

Ichimoku cloud bottom : 0.9576

Original strategy :

Buy at 0.9600, Target: 0.9700, Stop: 0.9565

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9590, Target: 0.9690, Stop: 0.9555

Position : -

Target : -

Stop : -

As the greenback staged a strong rebound after finding good support at 0.9552, suggesting a temporary low has been formed there and consolidation with mild upside bias is seen for this move to bring retracement of recent decline, hence gain to 0.9667-76 (61.8% Fibonacci retracement of 0.9738-0.9552 and previous support turned resistance) is likely, however, reckon upside would be limited to 0.9700 and price should falter below resistance at 0.9738.

In view of this, we are looking to turn long on pullback as the upper Kumo (now at 0.9584) should limit downside and bring another rise later. Below the lower Kumo (now at 0.9576) would abort and signal intra-day top is formed, risk retest of 0.9552 first.

US Dollar Attempts To Make A Comeback On Manufacturing PMI

The US dollar index was seen trading stronger on Monday after data from the Institute of Supply Management (ISM) showed that manufacturing activity rose to 57.8 in the month of June. The ISM's reading marked the highest level in the index since August 2014 and reversed the declining trend over the past few months.

As a result, the euro and the British pound continued to weaken, while the Japanese yen fell against the US dollar. While the ISM manufacturing activity increased, Markit's measure of manufacturing activity in the US slipped to 55.0, missing estimates of 58.5 and declined from 60.5 posted the month before.

Looking ahead, the US markets are closed today on account of the US Independence Day holiday. Data from the US is, therefore, limited for today. Traders are likely to shift focus to the RBA's meeting followed by UK's construction PMI data.

EURUSD intraday analysis

EURUSD (1.1371): The EURUSD extended the declines for a second consecutive day, giving up the gains above $1.1400. Price action is now seen testing the support level at 1.1357. Lack of any clear fundamentals today and slow trading is likely to keep the EURUSD trading flat. With the support level seen holding currently, EURUSD could be attempting to post another high off the bounce from 1.1357 support. A lower high could signal that the currency pair could be potentially breaking below the support at 1.1357 with the next level at 1.1300 coming into focus. To the upside, a continuation is required with further gains coming only on a convincing close above the previous high that was formed at 1.1445.

GBPUSD intraday analysis

GBPUSD (1.2942): The British pound was weaker yesterday following the disappointing manufacturing PMI data. Price action posted a reversal near the 1.2975 - 1.3000 resistance zone. Further declines could be seen coming with GBPUSD likely to fall back to the support level at 1.2800. On the 4-hour chart, any near-term bounce could see the 1.2975 price level being tested for resistance. This could confirm the downside towards 1.2800. Failure to limit the gains near 1.2975 could signal a continuation to the upside.

USDJPY intraday analysis

USDJPY (113.23): USDJPY posted strong gains yesterday, and price action managed to clear the 112.00 resistance level. The rally to 113.36 marks the completion of the bullish flag pattern. We could now expect to see some consolidation take place unless USDJPY can clear the 113.36 level which is currently acting as resistance. There is a risk of the downside in prices as the support level at 110.70 is likely to be tested in the medium term. Watch for the initial support at 112.00 which could be in focus immediately. Failure to contain the declines here could push USDJPY lower to 110.78.

Market Update – Asian Session: RBA Leaves Rate And Policy Stance Unchanged

Asia Summary

Markets were mixed in the session. North Korea launched a ballistic missile, which was said to have traveled for forty minutes before landing in the sea in Japan’s EEZ. South Korea vowed to sternly respond to the provocation. US President Trump tweeted he hoped that China would take care of North Korea. The USD/KRW stayed little changed, while the USD/JPY fell 0.3% to 113.09.

AUD/USD climbed into the target rate decision but then fell to session lows of 0.7621 after RBA left target rate unchanged at 1.5% and reiterated its policy stance from prior meetings. RBA commented it sees some signs that housing conditions are starting to ease and inflation will increase gradually.

China and Hong Kong markets traded lower, the PBOC skipped OMO for the 8th consecutive day and the yuan mid-point was set at its weakest level in 2-weeks. In an SCMP piece, said that the PBOC is likely to succumb to Fed tightening. Japan auto maker US sales were all higher y/y, while Kia/Hyundai reported weak figures in China vehicle sales.

Reminder US markets are closed for the July 4th holiday.

Key economic data

(AU) RESERVE BANK OF AUSTRALIA (RBA) LEAVES CASH RATE TARGET UNCHANGED AT 1.50% (AS EXPECTED)

(AU) AUSTRALIA MAY RETAIL SALES M/M: 0.6% V 0.2%E

(NZ) NEW ZEALAND Q2 NZIER BUSINESS CONFIDENCE: 18% V 17% PRIOR

(KR) SOUTH KOREA JUN CPI M/M: -0.1% V -0.1%E; Y/Y: 1.9% V 2.0%E; CPI CORE Y/Y: 1.4% V 1.5%E

(AU) Australia ANZ Roy Morgan Weekly Consumer Confidence Index: 114.5 v 111.8 prior

(JP) JAPAN JUN MONETARY BASE Y/Y: 17.0% V 19.2%E; MONETARY BASE END OF PERIOD: ¥468.0T V ¥455.9T PRIOR

(KR) South Korea Q2 Foreign Direct Investment (FDI) y/y: -9.0% v -9.2% prior

Speakers and Press

China

(CN) PBOC Deputy Gov Gonsheng : China looking at allowing foreign agencies to assign credit ratings on onshore bonds – SCMP

(CN) China's 2017 GDP growth may be higher than 2016 - Chinese Press

Japan

(JP) PM Abe expected to continue to pursue plan to revise Japan's constitution - Japanese Press

(JP) Bank of Japan (BoJ) Survey: Japan companies expect 1-year inflation at 0.8% y/y

(JP) Japan Fin Min Aso: Will discuss problems facing global economy at G20

Korea

(KR) Bank of Korea (BOK) Gov Lee: Central bank govs at the recent BIS meeting agreed that while monetary policies in developed countries are headed for a change, financial market instability seen during 2013 taper tantrum is unlikely to be repeated

(KR) North Korea has launched ballistic missile, around 09:40AM, said to have traveled 40 minutes - Korean press

(KR) US President Trump: North Korea has just launched another missile. Does this guy have anything better to do with his life? Hard to believe that South Korea and Japan will put up with this much longer. Perhaps China will put a heavy move on North Korea and end this nonsense once and for all! - tweet

Asian Equity Indices/Futures (00:30ET)

Nikkei +0.2%, Hang Seng -0.7%, Shanghai Composite -0.5%, ASX200 +1.7%, Kospi -0.2%

Equity Futures: S&P500 +0.0%; Nasdaq -0.1%, Dax +0.1%, FTSE100 +0.1%

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.1377-1.1363; JPY 113.41-113.13; AUD 0.7682-0.7654; NZD 0.7296-0.7263

Aug Gold +0.3% at 1,223/oz; Aug Crude Oil -0.5% at $46.84/brl; Sept Copper -0.4% at $2.67/lb

(CN) PBOC skips open market operations (8th straight skip)

(CN) PBOC SETS YUAN MID POINT AT 6.7889 V 6.7772 PRIOR (weakest setting in 2-weeks)

(KR) South Korea sells 30-yr bonds at 2.365%

USD/CNY Commerzbank analyst: PBOC may allow controllable yuan drop; could see yuan at 7.1 by the end of 2017

(TH) Thailand sells combined THB60B in 3-month and 6-month bonds

USD/CNY China State owned banks seen selling dollars at CNY6.80 in onshore forex market - financial press

JGB (JP) Japan MoF sells ¥1.86T in 10-yr 0.1% bonds; Avg yield 0.079%; bid-to-cover 4.77x v 3.64x prior (highest since February 2005)

Asia equities notable movers

Australia

Emeco Holdings, EHL.AU Morgans Financial Ltd Initiates EHL.AU with Add, price target: A$0.15, +11.4%

88 Energy, 88E.AU Provides project update on Project Icewine, -7.7%

Japan

Idemitsu Kosan, 5019.JP Planning ¥140B, 49M share sale (30% of shares outstanding), against the founders wishes; -11.2%

Show Shell, 5002.JP Idemitsu has no plans to call a shareholders' meeting to vote on a merger with rival Showa Shell Sekiyu after the issuance of new shares, which would dilute the stake held by the refiner's founding family; +6.7%

Hong Kong/China

PetroChina, 857.HK Announcement regarding the approval of the proposed Issuance of exchangeable Corporate Bonds by the Controlling Shareholder, +4.8%

Sinolink Securities ,600109.CN Tsinghua Holdings plans to cut stake by up to 5% within 6 months, -4.8%

US Session Highlights

US markets closed early ahead of the 4th of July holiday

Trump set to use US LNG as a political tool when he meets leaders from a group of a dozen countries. He is to tell the group, known as the “Three Seas” summit, that Washington wants to make it easier for US gas to reach these nations; which are often held to ransom by their dependence on Russia.

ISM Manufacturing Index rose to an unexpected 57.8 last month, for its best reading since August 2014. The components contributing the most were New Orders, showing a very strong 63.5, and Production also high at 62.4.

Contrasting positive manufacturing data, major US Automakers reported a decline in sales for June, for a fourth consecutive monthly decline. GM said it expected June sales to show 16.6 million units, down 1% from the same period last year.

Treasury yield curve continues to flatten as yields rise across the curve. 10-year yield up 5bps to 2.35%, and 30-year yield up at 2.87%. The 10s/30s yield curve flattening further to 52bps.

US markets on close: Dow +0.7%, S&P500 +0.9%, Nasdaq +1.4%

Best Sector in S&P500: Energy

Worst Sector in S&P500: IT

Biggest gainers: RIG +5.4%; CF +4.5%; GPS +4.2%; MOS +4.1%

Biggest losers: WDC -3.7%; NVDA -3.6%; SYMC -2.8%; AMD -2.6%

At the close: VIX 11.22 (+0.4%); Treasuries: 2-yr 1.41% (+2.0%), 10-yr 2.35% (+2.0%), 30-yr 2.86% (+0.9%)

Notable US Equities

TSLA Reports Q2 deliveries just over 22.0K v 24.2Ke v just over 25.0K q/q; Provided global economic conditions do not worsen considerably, company is confident that combined deliveries of Model S and Model X in H2 of 2017 will likely exceed deliveries in H1 of 2017.

Currencies: Risk-Off To Set The Tone For FX Trading?

Sunrise Market Commentary

- Rates: Geopolitical tensions to give bonds some respite?

Strong US ISM aborted a sluggish corrective upturn during the US session with US Treasuries now underperforming Bunds. Geopolitical tensions may give Bunds some upside, but this might be temporary. Mind the technical pictures: red alert in the Bund and code orange for US Treasuries. Sell-on upticks preferred. - Currencies: Risk-off to set the tone for FX trading?

Yesterday, the dollar rebounded as investors anticipated good US eco data. Today, US markets are closed. Geopolitical tensions triggered a risk-off correction in Asia. Such a correction might cap the USD/JPY rebound. The impact on EUR/USD is less straightforward. A correction in EUR/JPY might weigh also weigh on EUR/USD.

The Sunrise Headlines

- US equities closed with modest gains for the S&P 500 with NASDAQ again underperforming (-0.49%) on tech declines. Initially, Asian markets followed but sentiment turned as Asian stocks dropped on political tensions and losses in technology shares.

- President Jinping complained about a 'negative' turn in China's relationship with the US after several assertive US moves in Asia. Tensions are heating up in Asia as North Korea again fired a ballistic missile into the Sea Of Japan.

- The Reserve Bank of Australia is leaving its benchmark interest rate unchanged at 1.5%. There was little change in the RBA statement compared to previous months despite a general move of other central banks to more hawkish stances.

- The US manufacturing ISM was better than expected in June with a reading of 57.8 (55.3 consensus and 54.9 in May). Growth in production, employment and new orders indices point to a vibrant pace of activity in manufacturing.

- Multiple Nasdaq-listed stocks, including Amazon, Microsoft and Apple, saw their share price change to exactly $123.47 on multiple platforms. Nasdaq said this was due to 'improper use of test data' sent to third party data providers.

- Bank of Canada governor Poloz expects inflation to be 'well into an uptrend' in 2018 as the output gap in the economy closes. He added that the BoC should not wait to react until inflation hits the target otherwise it could be too late.

- With the 4th of July Holiday in the US, the eco-calendar is thin. The Swedish Riksbank rate decision and ECB's Praet's speech are the only interesting items on the agenda. The wildcard for today is the tension in international politics

Currencies: Risk-Off To Set The Tone For FX Trading?

Risk-off correction to drive FX trading today?

The dollar made a cautious comeback at the start of the week as investors prepared for key US data to be released this week. Interest rate differentials also (re)widened slightly in favour of the US currency. EUR/USD returned below the 1.14 handle. USD/JPY regained the 113 barrier. The EMU eco data were strong, but the euro didn't profit. Later, the US manufacturing ISM printed a strong 57.8, but didn't cause any significant additional USD gains as US markets headed into an early close. EUR/USD finished the session at 1.1364 (from 1.1426). USD/JPY extended its uptrend to close the day at 113.38 (from 112.3).

Overnight, sentiment on Asian equity market deteriorated during the session. Especially Hong Kong stocks are hit hard. A new missile test from North Korea played a role. Tech stocks also remain under pressure. The yen profits slightly from the intraday equity decline. USD/JPY is drifting back to the 113 area. EUR/USD is also losing a few ticks and trades in the 1.1345/50 area (EUR/JPY driven?). The Reserve Bank of Australia left its policy rate unchanged at 1.5%. The RBA maintains a constructive view on the economy but wage growth remains low. The RBA didn't hint at a change in its policy bias, disappointing hawks. AUD/USD dropped from the 0.7680 area to the 0.7620 area.

Today, there are only second tier eco data in Europe and US markets are closed for the 4th of July National Holiday. In such a context, one expects directionless trading in thin markets. This might still be the case, but we keep an eye on equities after the intraday sell-off in Asia. Will the correction in tech stocks spread to other parts of the market. Will political tensions (North Korean, reaction of Trump/discord between the US and China) cause additional volatility going into this weekend's G20 meeting? Of late, politics seldom was a lasting issue for global markets' trading. Even so, we keep an eye on it.

Yesterday, the dollar was well bid as investors anticipated good US eco data this week. However, if sentiment on risk deteriorates, this picture might change. A risk-off correction might cap the recent USD/JPY rebound. Remarkably, EUR/USD declined this morning despite the risk-off sentiment. After the recent EUR/JPY rally, time might be ripe for a correction in this cross-rate. This could cap the upside in EUR/USD. More still, it could weigh on this cross-rate in case of a temporary risk-off.

Technical picture: USD looking for a bottom

A combination of hawkish ECB comments and weaker US eco data pushed EUR/USD last week above the 1.1300/66 resistance area with a new high at 1.1448. The next resistance is now the 1.15 area. Further out LT-correction tops are coming in at 1.1616/1.1714. A break would end the long consolidation period that followed the sharp decline of EUR/USD in 2014/early 2015. Such a key area will be difficult to break for now. A drop below 1.1119 would suggest the pair enters calmer waters.

The USD/JPY rally ran into resistance in early May and the pair returned lower in the 108.13/114.37 range. The post-Fed USD rebound pushed the pair the 112.13 correction top early last week, but follow-through gains were modest. So, the jury is still out. A sustained break would improve the ST-picture. Even so, were remain cautious on further USD/JPY gains

EUR/USD correcting off last week's top.

EUR/GBP

Sterling declines against dollar; stable against euro.

Yesterday, the sterling trading was driven by the price moves in the dollar and the euro. The overall rebound of the dollar pushed cable back below the 1.30 barrier. There was also a small fall-out from the EUR/USD decline on EUR/GBP. The UK manufacturing PMI unexpectedly declined to 54.3 from 56.3. Sterling lost only modest ground after the release. EUR/GBP closed session at 0.8882 (from 0.8771). Cable finished the day at 1.2940.

Today, the UK construction PMI is expected decline slightly from 56.0 to 55.0. We see slight downside risks. The reaction of sterling to the release is likely limited. The Brexit negotiations are on ongoing issue. A risk-off sentiment, if it would occur, most often is a slightly negative for sterling. Short-term, we see EUR/GBP staying below the key resistance of 0.8866/80 as markets still digest the recent decline of sterling/rise of EUR/GBP. Cable's fate will depend on EUR/USD.

From a technical point of view, EUR/GBP set a minor top north of the 0.8854/66 resistance (2017 top). A sustained break didn't occur, causing a correction on the recent EUR/GBP rebound. A return below the 0.8655 correction low would indicate easing pressure on sterling. Such a break lower will be difficult. A EUR/GBP buy-on-dips approach remains favoured

EUR/GBP topside test rejected. A modes/temporary sterling comeback might be on the cards