Sample Category Title

Yen Dips as US Manufacturing PMI Jumps

USD/JPY has posted gains in the Monday session, gaining 0.74%. In the North American session, the pair is trading slightly above the 113 level. On the release front, Japanese Tankan Indices were both within expectations. The Tankan Manufacturing Index improved to 17, easily beating the estimate of 12. The Tankan Services Index improved to 23, just shy of the forecast of 24. Japanese Consumer Confidence softened to 43.3, missing the estimate of 43.9. In the US, ISM Manufacturing PMI climbed to 57.8, beating the estimate of 55.0.

The Japanese economy has shown some improvement, but consumer spending and inflation remain sore points. Japanese retail sales slowed to just 2.0% in May, compared to 3.2% a month earlier. The weak figure points to a Japanese consumer who is hesitant to open the purse strings. Wages have been stagnant, which has hampered consumer spending, a key driver of economic growth. Inflation is stuck below 1 percent, well below the BoJ's target of 2 percent. Tokyo Core CPI, the primary gauge of consumer inflation, edged down to 0.0%, below the estimate of 0.2%. The index has posted just one gain in the past 18 months, underscoring that the BoJ's ultra-loose monetary policy has not been able to raise inflation levels anywhere near the bank's target of 2 percent.

There was no getting around the fact that the US economy slowed down in the first quarter, but there was some good news, as the revised GDP reading was raised to 1.4%, better than the initial estimate of 1.2% in May. The improvement was attributed to stronger consumer spending and an increase in exports. Earlier in the year, the markets were braced for a very poor quarter, with the first estimate in April projecting a gain of only 0.7%. Inflation remains stubbornly low, and consumer spending is also soft, despite high consumer confidence levels. In May, Personal Spending softened to 0.1%, down from 0.4% a month earlier. If inflation levels don't show some improvement, the Federal Reserve may have second thoughts about a December rate hike.

Trade Idea: EUR/GBP – Stand aside

EUR/GBP - 0.8778

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term up

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As the single currency has retreated after rising briefly to 0.8882 last week, retaining our view that a temporary top is possibly formed there and few days of consolidation would be seen with mild downside bias, below 0.9755-60 would add credence to this view, bring retracement of recent upmove to 0.8730-35, however, still reckon downside would be limited to 0.8719 support.

In view of this, would be prudent to stand aside for now and look to turn short on recovery as 0.8840-50 should limit upside. Above 0.8882 would revive bullishness and extend recent upmove from 0.8304 low to 0.8900-10, having said that, as broad outlook remains consolidative, reckon current c leg of larger degree wave b should be limited to 0.8950 and price should falter well below 0.9000 psychological level.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Trade Idea: USD/CAD – Sell at 1.3115

USD/CAD - 1.2986

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term down

Original strategy :

Sell at 1.3115, Target: 1.2915, Stop: 1.3175

Position: -

Target: -

Stop: -

New strategy :

Sell at 1.3115, Target: 1.2915, Stop: 1.3175

Position: -

Target: -

Stop:-

As the greenback has recovered after falling to 1.2946 on Friday, suggesting minor consolidation would be seen and corrective bounce to 1.3045-50 and possibly 1.3080 is likely, however, reckon 1.3115-20 would limit upside and bring another decline later, below said support would extend the fall from 1.3794 top (wave c of larger degree wave b top) to 1.2920, however, near term oversold condition should limit downside to 1.2900 and reckon 1.2870 would hold from here, risk from there has increased for a rebound later.

In view of this, would not chase this fall here and would be prudent to sell the pair again on recovery as 1.3115-20 should limit upside. Above 1.3160-70 would defer and suggest low is formed, bring a stronger rebound to 1.3215-20 and possibly towards 1.3260-65 but only break there would abort and signal a temporary low is formed instead, then test of resistance at 1.3308 would follow.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

Sterling Hardly Suffers from Disappointing PMI

- European equities are showing gains of around 1%. American indices are joining the positive momentum. Major US indices start the quarter with gains of about 0.5% Trading volumes are light before Tuesday's US 4th of July holiday. The dollar strengthened as positions are set ahead of key US data later this week.

- Average unemployment in the Eurozone held at 9.3% in May, its lowest level since 2009, as the number of people who registered as jobless fell by 5,000 in the month. It was the weakest monthly performance of the year.

- IHS Markit's Eurozone manufacturing PMI posted another bumper month of activity with the overall index hitting 57.4 in June, its best level since April 2011 and up from the flash reading of 57.3 and the 57 in May. This makes the quarterly performance the best in over six years.

- The UK June manufacturing PMI unexpectedly declined to 54.3 from 56.3 (revised from 56.7) while a stabilisation was expected. Output, order book and employment growth all slowed and positive sentiment slipped to a seven-month low amid reports of uncertainty regarding the political outlook.

- The US manufacturing ISM improved from 54.9 to 57.8. The consensus expected only a rise to 55.3. The rebound was supported by strong orders (63.5) and a rise of the employment component. Prices rise eased more than expected. (55.0 from 60.5).

- German Chancellor Angela Merkel's party and her Bavarian CSU allies say in election platform that they oppose pooling euro-area debt. They added that they are ready to develop the Eurozone further together with the French government, for instance with the creation of its own monetary fund.

- US Carmakers outsold June estimates in US. Y/Y changes are still negative as base year 2016 was a record year.

Rates

German bonds start the week with cautious gains

After a savage sell-off last week, German bonds cautiously reversed course in technical trading, but only after a shy test of the key Bund support at 161.68/58 (Bund opened at 161.55). The down-leg was exhausted or at least needed a pause. Ahead of the closure of US markets tomorrow, that isn't a big surprise. The German 10-yr yield virtually touched the key 0.5% yield resistance. The upturn in German bonds wasn't because of bad news as the final PMI was even marginally revised higher and the unemployment rate was in line with expectations. The corrective movement was visible in other markets too, with equities and the dollar gaining some ground. With all boats rising, we cannot but conclude that the quarter started well. However, it is too early to jump on the current technically inspired rise of "all" assets. Going towards the publication of the key ISM report (after the closure of our report) core bonds are declining marginally.

At the time of writing, the German yield curve flattened slightly with yields down between 1.9 bp (2-yr) and 0.2 bp (30-yr). The US yield curve was little changed (less than 1 bp) with yields marginally up in the 2-to-5-yr sector and slightly down in the 10-30-yr segment. On intra-EMU bond markets, 10-yr yield spread changes are little changed with the exception of Italy/Spain and Ireland whose spreads narrow 1.5 to 2.3 bps.

Currencies

Dollar rebound ahead of ISM

The dollar made a cautious comeback at the start of the new trading week as investors prepared for key US eco data today and later this week. The EMU eco data were strong, but the euro didn't profit anymore. EUR/USD declined to trade in the 1.1360 area ahead of the key US ISM manufacturing release. USD/JPY changed hands in the 113 area.

Overnight, Asian equities traded mixed. The Japan Tankan business sentiment was stronger than expected. The Caixin China manufacturing PMI also improved slightly. Decent regional data don't help the yen though. USD/JPY opened slightly in the red on a negative result for PM Abe's party in regional elections, but reversed the initial loss. A further rise in the oil price and a rise in US yields supported the dollar. USD/JPY returned to the 112.50 area. EUR/USD dropped slightly to the 1.1405/20 area.

The dollar USD momentum improved during the European morning session. EUR/USD dropped below 1.14 handle. Dollar strength prevailed even as the EMU eco data remained strong (manufacturing PMI, EMU unemployment). Investors apparently reduced USD short-going into a series of key US eco data to be published this week, starting with the manufacturing ISM today. Changes on the core bond market were limited. If anything, the US/German spread widened marginally if favour of the dollar. USD/JPY also extended the intraday uptrend and rebounded to the high 112 area. The intraday dollar rebound slowed this afternoon as investors awaited the US manufacturing ISM. EUR/USD traded in the 1.1370 area. USD/JPY held close to the 113-pivot.

Sterling hardly suffers from disappointing PMI

Sterling trading was mostly driven by the price moves in the dollar and the euro. The overall rebound of the dollar pushed cable back below the 1.30 barrier. There was also a small fall-out from the EUR/USD decline on EUR/GBP. The pair dropped to the 0.8760 area. Mid-morning, the UK manufacturing PMI unexpectedly declined to 54.3 from 56.3 (earlier reported as 56.7). A stabilisation was expected. Sterling lost modest ground after the release. EUR/GBP rebounded to the 0.8775/80 area. Cable declined further. The release further complicates the internal debate in the BoE on the need for a rate hike. However, in this respect, the services PMI to be published on Wednesday will probably be more important. EUR/GBP trades currently in the 0.8780 area; Cable is changing hands around 1.2950.

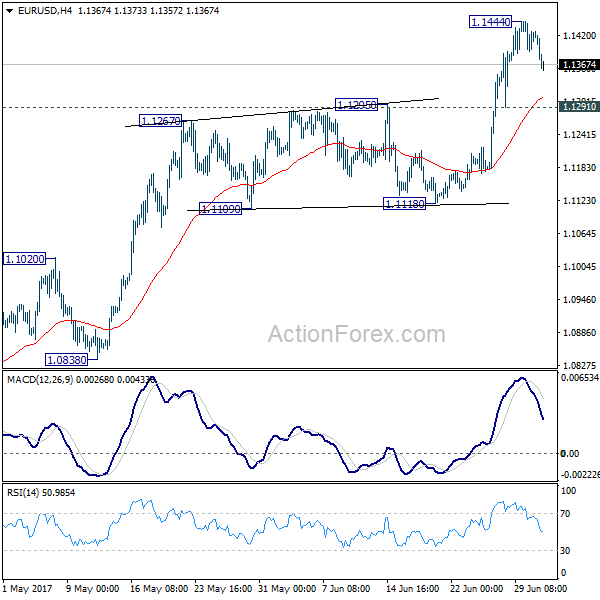

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1394; (P) 1.1419 (R1) 1.1447; More.....

EUR/USD's retreat from 1.1444 is still in progress and intraday bias remains neutral. Deeper fall cannot be ruled out. But downside should be contained by 1.1291 support to bring another rise. Break of 1.1444 will extend the rally from 1.0339 low to 1.1615 resistance next.

In the bigger picture, the firm break of 1.1298 resistance further affirm medium term reversal. That is an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1776). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.

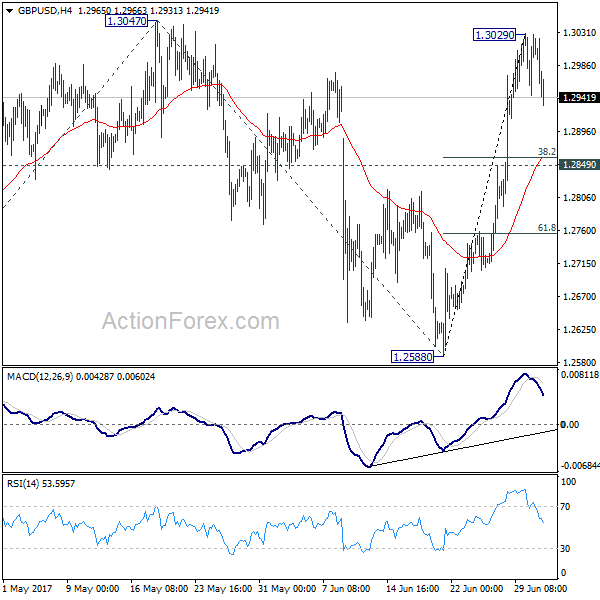

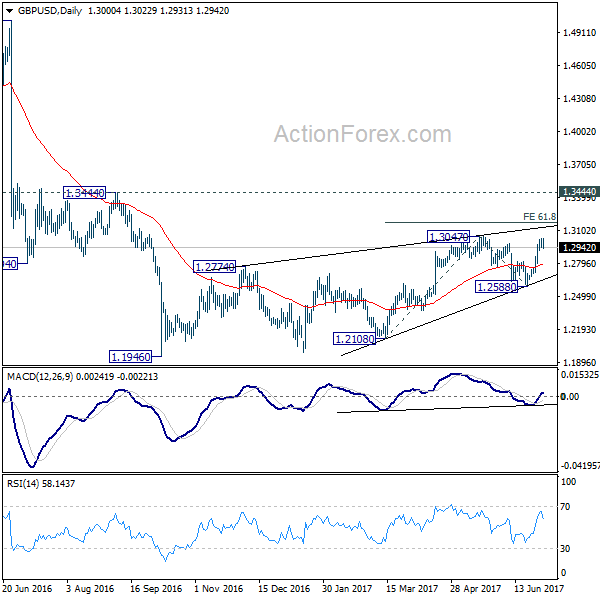

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2970; (P) 1.3000; (R1) 1.3056; More...

GBP/USD's consolidation from 1.3029 is still in progress and intraday bias remains neutral. Deeper retreat could be seen but downside should be contained above 1.2849 support to bring rise resumption. Break of 1.3029 should then send GBP/USD through 1.3047 to 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168 next.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is now in favor, overall outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

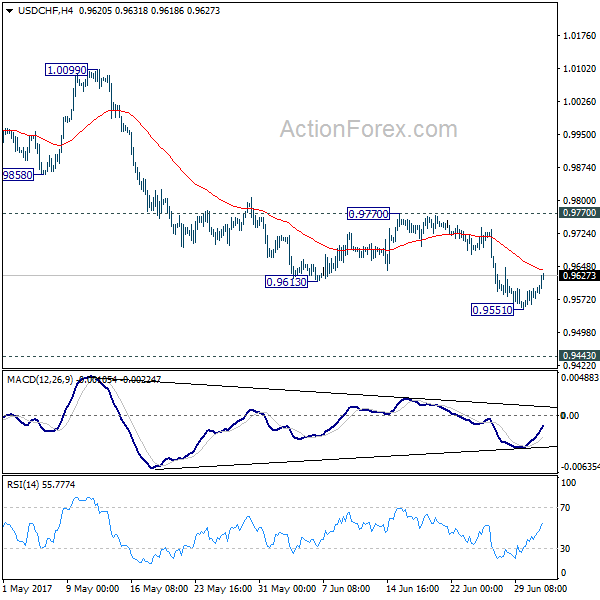

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9558; (P) 0.9578; (R1) 0.9604; More......

USD/CHF's recovery continues in early US session and outlook is unchanged. Intraday bias remains neutral for consolidation above 0.9551. Upside of recovery should be limited below 0.9770 resistance and bring resumption. Below 0.9551 will extend the decline from 1.0342 to 0.94443 key support level. At this point, we'd expect strong support from there to bring rebound.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

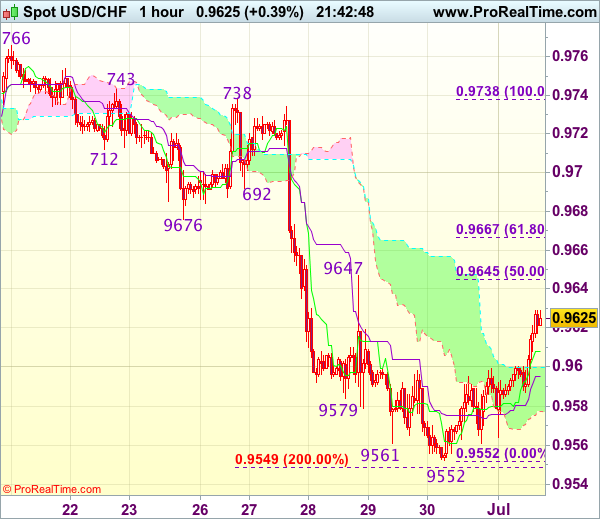

Trade Idea Update: USD/CHF – Sell at 0.9645

USD/CHF - 0.9623

Original strategy :

Sell at 0.9645, Target: 0.9545, Stop: 0.9680

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9645, Target: 0.9545, Stop: 0.9680

Position : -

Target : -

Stop : -

Dollar’s recovery after falling to 0.9552 last week suggests minor consolidation would be seen and corrective bounce to 0.9645-47 (50% Fibonacci retracement of 0.9738-0.9552 and previous resistance) is likely, however, reckon upside would be limited and bring another decline later, below 0.9585-90 would bring test of said support, break there would signal recent decline from 0.9771 top has resumed for further weakness to 0.9545-49 (2 times extension of 0.9771-0.9676 measuring from 0.9738) but reckon downside would be limited to 0.9525-30 (50% projection of 1.10100-0.9613 measuring from 0.9771) and 0.9500 should hold, price should stay above 0.9470 (61.8% projection), bring rebound later.

In view of this, would not chase this fall here and we are looking to sell dollar on further recovery as resistance at 0.9647 should limit upside. Only above previous support at 0.9676 (now resistance) would defer and suggest a temporary low is formed, risk test of another previous support at 0.9692.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.85; (P) 112.23; (R1) 112.73; More...

USD/JPY's rise from 108.81 resumed by taking out 112.91 and reaches as high as 113.27 so far. The break of medium term channel resistance suggests that whole corrective pull back from 118.65 has completed at 108.12 already. Intraday bias is back on the upside for 114.36 resistance. Decisive break there should confirm this bullish view and target 118.65 again. On the downside, break of 111.72 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85.

Dollar Regaining Ground in Subdued Trading, With a Little Help from ISM Manufacturing

Trading remains rather subdued in the forex markets today. Dollar is trying to regain some ground after last week's steep selloff. The stronger than expected ISM manufacturing is giving the greenback extra fuel. But the recovery looks nothing more than a recovery so far, except versus Yen. Sterling is also under some pressure after PMI disappointment. But loss is limited. Yen, on the other hand, is trading weakly, in particular to greenback, despite an upbeat Tankan report. The biggest news from Japan was the humiliating defeat of Prime Minister Shinzo Abe's fulling LDP in Tokyo's local election. Meanwhile, Canadian Dollar is staying firmly in tight range as WTI crude oil is extending it's rebound to as high as 46.65.

Sterling mildly lower as PMI manufacturing dropped

Sterling trades mildly lower today after PMI disappointment. UK PMI manufacturing dropped to 54.3 in June, down from 56.3 and missed expectation of 56.3. Markit noted that "while the survey data add to signs that the economy is likely to have shown stronger growth in the second quarter, further doubts are raised as to whether this performance can be sustained into the second half of the year." There are talks after the releases that the economy data could paint a picture that counter the view of the BoE hawks. But judging from reactions in the markets, traders don't buy into this view.

Economist said Eurozone PMIs exaggerated

Eurozone PMI manufacturing was finalized at 57.4 in June, revised up from 57.3. The global economist and managing director at UBS Wealth Management Paul Donovan, interviewed by CNBC, criticized that the numbers point to 3.5 or 4% growth in Europe and that is wildly exaggerated. He pointed out that the PMI is a "sentiment indicator" and "not a real-world indicator." Also he said that the survey quality has been in decline in recent years. Also from Eurozone, Italy PMI manufacturing rose to 55.2 in June, up from 55.1. Eurozone unemployment rate was unchanged at 9.3% in May.

Also from from Europe, Swiss retail sales dropped -0.3% yoy in May. SVME PMI rose to 60.1 in June.

Japan large manufacturers sentiment hits 3 year high

Japan Tankan large manufacturers index jumped to 17 in Q2, up fro 12, and beat expectation of 15. That's the highest reading in three years. Large manufacturers outlook improved to 15, up from 11, above expectation of 14. Non-manufacturing index rose to 23, up from 20, and met consensus. Non-manufacturing outlook rose to 18, up from 16, but missed expectation of 21. The survey was generally consistent with recent upgrade of economic assessment by BoJ. But still, the positive developments in the economy is not being translated into price pressure yet. And BoJ is far from stimulus exit.

Rebound in China manufacturing may be temporary

The Caixin China PMI manufacturing rose to 50.4 in June, up from 49.6 and beat expectation of 49.8. That's back in expansion territory and was the highest level in three months. However, a CEBM Group economist noted in the accompany statement for the release that "based on the inventory trends and confidence around future output, the June reading was more like a temporary rebound, with an economic downtrend likely to be confirmed later."

Elsewhere, Australia TD Securities inflation rose 0.1% mom in June. Building approvals dropped -5.6% mom in May.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.85; (P) 112.23; (R1) 112.73; More...

USD/JPY's rise from 108.81 resumed by taking out 112.91 and reaches as high as 113.27 so far. The break of medium term channel resistance suggests that whole corrective pull back from 118.65 has completed at 108.12 already. Intraday bias is back on the upside for 114.36 resistance. Decisive break there should confirm this bullish view and target 118.65 again. On the downside, break of 111.72 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Tankan Large Manufacturers Index Q2 | 17 | 15 | 12 | |

| 23:50 | JPY | Tankan Large Manufacturers Outlook Q2 | 15 | 14 | 11 | |

| 23:50 | JPY | Tankan Non-Manufacturing Index Q2 | 23 | 23 | 20 | |

| 23:50 | JPY | Tankan Non-Manufacturing Outlook Q2 | 18 | 21 | 16 | |

| 23:50 | JPY | Tankan Small Mfg Index Q2 | 7 | 7 | 5 | |

| 23:50 | JPY | Tankan Small Mfg Outlook Q2 | 6 | 4 | 0 | |

| 23:50 | JPY | Tankan Small Non-Mfg Index Q2 | 7 | 6 | 4 | |

| 23:50 | JPY | Tankan Small Non-Mfg Outlook Q2 | 2 | 3 | -1 | |

| 00:30 | JPY | Manufacturing PMI Jun F | 52.4 | 52 | 52 | |

| 01:00 | AUD | TD Securities Inflation M/M Jun | 0.10% | 0.00% | ||

| 01:30 | AUD | Building Approvals M/M May | -5.60% | -1.30% | 4.40% | |

| 01:45 | CNY | Caixin PMI Manufacturing Jun | 50.4 | 49.8 | 49.6 | |

| 05:00 | JPY | Consumer Confidence Jun | 43.3 | 43.9 | 43.6 | |

| 07:15 | CHF | Retail Sales (Real) Y/Y May | -0.30% | -0.80% | -1.20% | |

| 07:30 | CHF | SVME PMI Jun | 60.1 | 56.3 | 55.6 | |

| 07:45 | EUR | Italy Manufacturing PMI Jun | 55.2 | 55.3 | 55.1 | |

| 07:50 | EUR | France Manufacturing PMI Jun F | 54.8 | 55 | 55 | |

| 07:55 | EUR | Germany Manufacturing PMI Jun F | 59.6 | 59.3 | 59.3 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Jun F | 57.4 | 57.3 | 57.3 | |

| 08:30 | GBP | PMI Manufacturing Jun | 54.3 | 56.3 | 56.7 | 56.3 |

| 09:00 | EUR | Eurozone Unemployment Rate May | 9.30% | 9.30% | 9.30% | |

| 14:00 | USD | ISM Manufacturing Jun | 57.8 | 55 | 54.9 | |

| 14:00 | USD | ISM Prices Paid Jun | 55 | 58.5 | 60.5 | |

| 14:00 | USD | Construction Spending M/M May | 0.00% | 0.20% | -1.40% | -0.70% |