Sample Category Title

ECB Will Deliver A Relatively Dovish Message Next Week

Market movers today

Focus today will be on inflation in the US and Germany, which will provide an important gauge of the underlying inflation pressures after a couple of months with volatile readings due to the timing of Easter.

In the US, the PCE inflation data for April is released. After the weak CPI report earlier in May, we estimate that PCE core rose 0.1% m/m, implying a core inflation rate of just 1.4% y/y (a decline from 1.6% in March).

As a prelude to the highly important CPI release for the whole euro area economy tomorrow, German inflation figures are released today. In line with our expectation, markets expect them to fall back in May versus April.

In Sweden, the main event this week is undoubtedly 2017 Q1 GDP data released today. We expect growth to come in at around 2.5% y/y (calendar adjusted) which is well in line with our exanteforecast . In Norway we have retail sales (for more details see page 2).

Selected market news

Yesterday, the market kept a close eye on the Draghi hearing for monetary policy clues ahead of the 8 June ECB meeting. But Draghi stuck to the party line saying that " Despite a firmer recovery, and looking through the volatile readings in HICP inflation over recent months, underlying inflation pressures have remained subdued. Domestic cost pressures, notably from wages, are still insufficient to support a durable and self-sustaining convergence of inflation toward our medium-term objective. For domestic price pressures to strengthen, we still need very accommodative financing conditions, which are themselves dependent on a fairly substantial amount of monet ary accommodation". Draghi added: "We remain firmly convinced that an extraordinary amount of monetary policy support , including through our forward guidance, is still necessary for the present level of under-utilized resources to be re-absorbed and for inflation to return to and durably stabilize around levels close to 2 percent within a meaningful medium-term horizon".

Hence, there was no sign that the ECB is about to make a U-turn despite the better economic data from the euro zone. We continue to hold the view that the ECB will deliver a relatively dovish message next week and importantly keep the commitment to low or " lower" rates.

Following the French election and the strong support for Merkel's CDU in t he German ländern elect ions, we have seen less focus on European politics and instead the focus has moved back to the Trump administration. However, yesterday Italy came into the spot light once again. 10Y Italian government bonds lost 12bp to Germany after former prime minister Mat teo Renzi suggested on Sunday that Italy's next election should be held in September around the same time as Germany's, saying that this would reduce market uncertainty about Italy, not increase it. The fixed income market obviously did not agree. Given that the media also reported that an agreement on the Italicum (electoral reform) is getting closer, a snap election in the autumn has become more likely. Most political analysts until recently had looked for elections to take place early in 2018. The Italian bond market could potentially be in for a volatile summer.

European Open Briefing: The Commodity Currencies Were Quiet Overnight

Global Markets:

- Asian stock markets: Nikkei down 0.45 %, ASX 200 gained 0.05 %, Shanghai Composite and Hang Seng closed for holiday

- Commodities: Gold at $1270 (+0.15 %), Silver at $17.45 (+0.70 %), WTI Oil at $49.75 (-0.15 %), Brent Oil at $52.40 (-0.50 %)

- Rates: US 10-year yield at 2.24, UK 10-year yield at 1.02, German 10-year yield at 0.30

News & Data

- Japan Retail Sales y/y 3.2 % vs 2.3 % expected

- Japan Unemployment Rate 2.8 % vs 2.8 % expected

- Japan Household Spending m/m 0.5 % vs 1.1 % expected

- Japan Household Spending y/y -1.4 % vs -0.7 % expected

- Australia Building Approvals 4.4 % vs 3.0 % expected

- New Zealand Building Consents m/m -7.6 % vs -1.2 % previous

- Greece, Italy tensions hit euro, Asian stocks, lift yen, gold – RTRS

- Oil inches up in quiet holiday trade, focus on crude glut – RTRS

- Dollar firms against sterling, euro amid political uncertainties – RTRS

- Draghi says ECB stimulus still needed despite better growth – RTRS

Markets Update:

The Euro came under pressure following comments from ECB President Draghi and news that there might be an early election in Italy in September. Draghi stated that there is still need for a substantial stimulus as inflation remains subdued. Meanwhile, former Prime Minister Renzi, who is looking for a political comeback, said that he supports an election as early as September. Domestic stock markets reacted negatively, and Italian government bonds also declined.

EUR/USD fell from 1.12 to a low of 1.1120 in Asia. Immediate support is seen at 1.111, but the next important level is 1.1050.

GBP/USD is also suffering from political developments. British Prime Minister Theresa May's lead over the opposition Labour Party dropped to 6 percentage points as the latest poll showed. Following the break below 1.2820 support, a test of 1.27 seems likely in the near-term.

The commodity currencies were quiet overnight. AUD/USD consolidated in a 0.7420-40 range, while NZD/USD traded between 0.7035 and 0.7055.

Upcoming Events:

- 07:45 BST – French GDP

- 10:00 BST – Euro Zone Consumer Confidence

- 10:00 BST – Euro Zone Business Climate

- 13:00 BST – German CPI

- 13:30 BST – US Personal Spending

- 13:30 BST – US Personal Income

- 13:30 BST – Canadian Current Account

- 15:00 BST – US CB Consumer Confidence

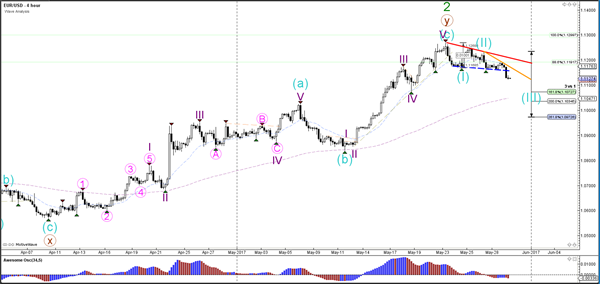

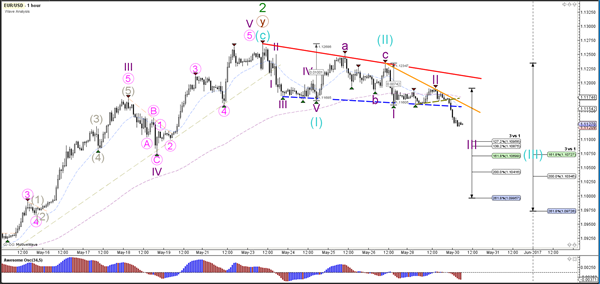

Daily Technical Analysis: EUR/USD Bearish Breakout Starts Wave 3 Momentum

Currency pair EUR/USD

The EUR/USD has broken below the support trend line (dotted blue) which could kick start momentum within wave 3 (blue) towards the Fibonacci targets. A break above the resistance (red/orange) invalidates the wave 3 formation.

The EUR/USD seems to be building a 5 wave extension (purple) within the 3rd wave (blue).

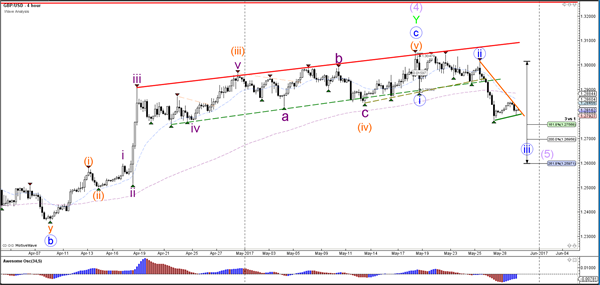

Currency pair GBP/USD

The GBP/USD is building a small correction but a break below support (green) could see wave 3 (blue) continue.

The GBP/USD stopped and reversed at the 38.2% Fibonacci level of wave 4 (orange) as expected in yesterday's analysis. A break above the trend line (orange) could see price challenge higher Fibs but a break above the 61.8% Fib makes a wave 4 unlikely.

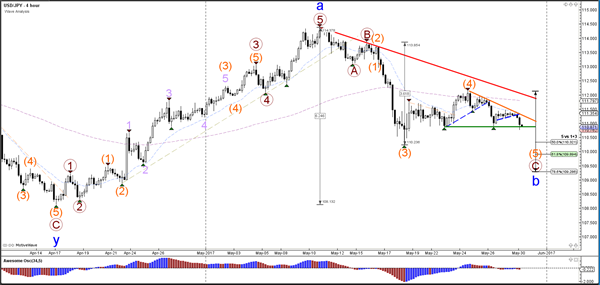

Currency pair USD/JPY

The USD/JPY is in a descending wedge pattern with support (green) and resistance (orange) nearby. A bearish break could see price fall towards the Fibonacci retracement levels of wave B (blue).

The USD/JPY broke below support (dotted blue) and completed a wave 4 (blue). Price remains in a 5th wave as long as it remains below resistance (orange).

AUDNZD Looking Ready To Recover Slightly

Key Points:

- The pair has reached a very robust level of support.

- Upsides will be tangible but not as pronounced as last time's reversal.

- Keep an eye on the RBNZ's report, due shortly.

Given the rather sedate prior session resulting from public holidays in both the US and the UK, some of the more exotic crosses are worth investigating a little more closely today. In particular, the AUDNZD has set itself up for what could be a decent rally over the coming week – at least if its technical bias is anything to go by.

As is shown below, the rout that has been gripping the pair over the past few sessions has come to an abrupt end as support kicked in strongly. However, this really shouldn't come as a total surprise given that we have reached the point of intersection of the declining trend line and the lower extreme of the regression trend channel. What's more, the presence of this channel suggests that we might now see some form of recovery as we move forward.

Indeed, we are already beginning to see buying pressure return as the market attempts to relieve the highly oversold stochastic oscillator. If this continues, it could mean that we have a near-term corrective manoeuvre on our hands which is good news for the bulls out there. This being said, we aren't currently expecting to see a huge degree of upside action moving ahead as there is a highly robust zone of resistance in place at around the 1.0611 level.

More precisely, the intersection of the regression channel's basis line and the 38.2% Fibonacci level will likely prove to be a hard cap on gains without some form of fundamental upset. This cap is only reinforced by the parabolic SAR and EMA biases – both of which are bearish. Ultimately, whilst they shouldn't hamstring the bulls altogether, these readings are likely to prevent the kind of kneejerk price spike that we saw only a few weeks ago and this means that we are unlikely to see more than 70 pips netted in a single session this week.

Overall, expect to see some buying pressure coming down the line but don't ignore the presence of that resistance level. Although, keep half an eye on the RBNZ which will be releasing its Financial Stability Report shortly as this could generate some unexpectedly strong bullish sentiment for the pair should the bank have a more dour tone than we have seen recently.

Will June Be The Lift Off Month For The Fed?

Key Points:

- Fed likely to be monitoring the PCE Deflator results closely.

- June rate hike still possible but caution is likely.

- Failure to tighten monetary policy likely to lead to a greenback depreciation.

The past few weeks have probably left many readers questioning just how strong the case for a June rate hike from the U.S. Federal Reserve is. To date, we have seen some significant tightening in labour market conditions, as well as renewed forecasts of economic growth from the Atlanta Fed. However, you would be forgiven for questioning these data points given that the last release of FOMC minutes seemed to take a dovish tone and hint at the need for additional economic strength to be seen. Subsequently, a June rate hike appears to be anything but a done deal and here's why:

Inflationary Pressures

Central banks typically love manageable inflation and the Fed is no different in this regard. However, despite tremendous amounts of QE having been injected into the U.S. economy, and falling unemployment nearing natural levels, we are yet to see much in the way of sustained inflation being reported. In fact, the Fed primarily looks at the Personal Consumption Expenditure (PCE) readings, which coincidently are due out tomorrow, as a gauge to give them a lens to measure inflationary pressures, primarily demand pull, in the domestic economy. However, the latest reading of the PCE showed a worrying downtick that largely matched the relatively lacklustre Q1 GDP results. Subsequently, the central bank will be looking for a relatively strong result before they will consider near term rate hikes.

Wage Inflation

In extension to the PCE, wage inflation is also another measurement that can be applied to provide us some insight into pent up demand within the economy. Unfortunately, hourly earnings have been relatively flat over the past year which shouldn't be surprising given the rise in part time employment. The reality is that without well paying, fulltime jobs, people are typically loathe to spend what money they possess on consumable items.

1st Quarter GDP Growth

The central bank was a little shell shocked when the Q1 GDP was revised downwards and immediately reached into the bucket of excuses to explain why. Chiefly amongst them was the suggestion that this was just a transitory weakness and that they expected the following quarter to drive additional growth to match the Atlanta Fed's GDPNow forecasts. However, this has largely turned into farce with the forecast seemingly changing weekly. Subsequently, some members on the FOMC are now clearly expressing concern that the downward GDP revisions could, in fact, form a trend.

Slowdown in China

China was always going to experience a slow down at some stage given the successive years of a rapidly growing economy. Unfortunately, for the Federal Reserve, the slowdown appears to coincide right when the bank is thinking of normalising their interest rates and winding back their balance sheet. Subsequently, the FOMC is right to be concerned as to the impact on trade and demand as the juggernaut that is/was the Chinese economy starts to slow down.

Ultimately, I suspect that the FOMC's decision is likely to hinge upon the PCE Deflator results due out tomorrow. An abject lack of inflationary pressures in the indicator could very well cause the Fed to remain cautious and hold off on a rate rise to their next FOMC meeting. However, that will surely lead to the USD falling further and the bubble that is the S&P growing ever more present.

Elliott Wave View: GBP/JPY More Downside Expected

Short Term Elliott Wave view in GBPJPY suggests the decline from 5/10 peak is unfolding as a double three Elliott Wave structure where Minor wave W ended at 143.33 and Minor wave X ended at 145.45. The subdivision of Minor wave W unfolded as a zigzag Elliott Wave structure where Minute wave ((a)) ended at 145.61 and Minute wave ((b)) ended at 147.12. After ending Minor wave X at 145.45, pair has since resumed lower and broken below 143.33. This creates a bearish 5 swing incomplete sequence from 5/10 peak and favors more downside in the near term.

The decline from 145.45 looks to be unfolding as a zigzag Elliott Wave structure where Minute wave ((a)) ended at 142.11 and Minute wave ((b)) ended at 143.08. Pair has also broken below 142.11 which suggests that Minute wave ((c)) lower has already started. Near term, while bounces stay below 143.08 in the first degree, but more importantly below 5/25 high (145.45), expect pair to continue lower towards 139.51 – 140.65 area before cycle from 5/10 peak ends. Buyers should then appear from the aforementioned area for at least a 3 waves bounce at later stage. In case pair breaks above 143.08 now, then the move from 5/26 low can be labelled as a Flat and pair should extend higher to correct cycle down from 5/25 high (145.45) but it still expected to turn lower again afterwards provided that pivot at 145.45 high stays intact.

GBPJPY 1 Hour Elliott Wave Chart

Market Morning Briefing: The Dovish Sentiment Expressed In The ECB Chief Draghi’s Statement

STOCKS

Dow (21080.28, -0.01%) was closed yesterday. As mentioned yesterday, 21200 is an important resistance for the near term. In case it breaks on the upside, the index could rally towards 21400-21600 else a fall back towards 21100 is possible in the coming sessions.

Dax (12628.95, +0.21%) is stable and may continues to remain sideways within 12800-12400 (broad region of trade for at least this week)

Shanghai (3110.06, +0.07%) looks bullish in the near term towards 3170. A small dip to 3070 is also possible before the index starts to rise higher.

Nikkei (19576.19, -0.54%) seems to be confused on which direction to take. Immediate movement within 19500-20000 is possible but only if it breaks on either side, can we confirm on further direction. For now, some sideways consolidation is possible.

Nifty (9604.90, +1%) has been rising in line with our expectation. 9700-9800 is on the cards for medium term.

COMMODITIES

As this moment, the Support at 1248 has held on intra-day basis and Gold (1270) has moved up a bit. Given that the Support at 1248 has held, some more rise towards 1275-80 is possible. For the near term, the market seems to be trading in a 1248-80 range now and the medium term range is now 1220-1280. The big question is whether we will see a rise past 1280-1300 or not in June.

Nothing new to add in Silver (17.43) also as the recent trading range is 17.36-87 and the medium term range is now 16.69-17.87. Both Gold and Silver are entering in a short term overbought zone thus chances of a correction can't be completely ignored.

Copper (2.55) is hovering around it's support area of the short term range of 2.55-2.62 with no directional clarity. Only above 2.62, higher resistances of 2.67-72 can come into consideration. A close below 2.55 levels could open up 2.44-46 levels as well.

Brent (52.20) and WTI (49.84) are hovering around their respective pivots of 52.77 and 49.54 of their short term trading ranges of 51.32-54.60 and 47.50-51.20 respectively. We will be assured of strength of Brent and WTI only when a firm and sustainable closing above 54.60 and 53 are made by both of them. A daily close below the respective supports could open up 49.50 levels for Brent and 47.50 for WTI as well.

FOREX

The dovish sentiment expressed in the ECB chief Draghi's statement about the European bond buying program has kept Euro (1.1128) weak but the proximity of the major support 1.1100-1.1075 and the lack of downside momentum still point towards the possibility of a turnaround this week. In a similar vein, the strength of Dollar Index (97.67) looks suspect even above the interim resistance of 97.55 and the near term upside may be limited to 98.00 at most.

Dollar Yen (110.87) keeps oscillating in the range of 110-112 and may continue that for a few sessions more. The bullish options remain open till 110 holds but the prolonged weakness in EURJPY (123.38), which may 122.80-60 or even 122.00 before bouncing back, raises questions about the upside chances. If a break below 110 is seen, then a resumption of the larger downtrend may be confirmed. Waiting for clarity.

The major support of Pound (1.2818) around 1.2750-00 holds for now and short covering may push the currency higher to 1.2900. The volatility is expected to remain high till the June 8 election with 1.2750-00 being the make or break support level for the near to medium term trend.

Aussie (0.7424) has been trading sideways in the range of 0.74-0.75 as expected and may continue that for the rest of the week.

Dollar Rupee (64.49) remains in a consolidative mode as expected which may continue for another couple of sessions. The immediate range is expected be 64.35-64.70.

INTEREST RATES

The UK 10Yr (1.01%) is testing support near current levels and could bounce back in the near term while the 20Yr (1.57%) and the 5Yr (0.46%) have some more scope on the downside to test medium term supports.

The Japanese yields have risen slightly and could move up in the near term. The US-Japan 10Yr (2.20%) could be headed towards 2.15% in the near term.

The resistances coming from mid-2015 have held well for the German yields and the yields have come off sharply in the last few sessions. The yields look bearish in the near term. The German-Us 10YR (-1.94%) and the German-US 2Yr (-2.04%) have fallen sharply but could face some support just below current levels from where a bounce is possible for the near term.

The 10Yr GOI (6.8125%) may rise towards 6.85% or higher in the near term. Immediate support is visible in the 6.75-6.70% region.

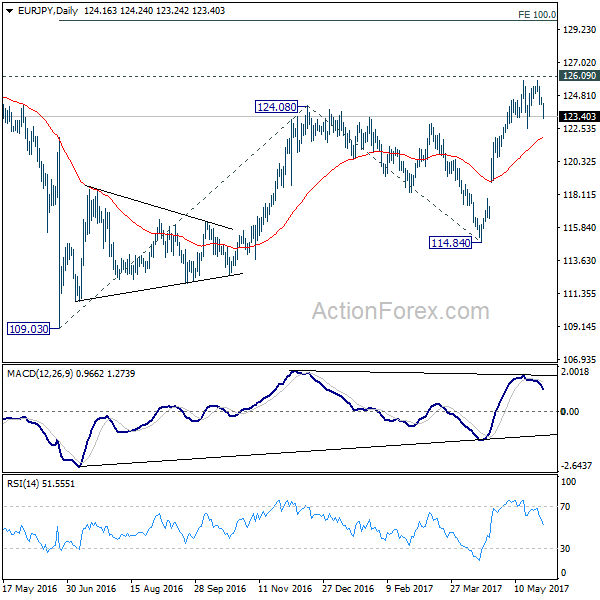

EUR/JPY Daily Outlook

Daily Pivots: (S1) 124.03; (P) 124.33; (R1) 124.48; More...

EUR/JPY drops sharply to as low as 123.24 so far and deeper decline might be seen. But after all, it's staying in the consolidation pattern from 125.80. Hence, we'd expect downside to be contained by by 38.2% retracement of 114.84 to 125.80 at 121.61 to bring rise resumption. We're staying mildly bullish in the cross. And, break of 126.09 key resistance will extend the whole rebound from 109.03 to 100% projection of 109.03 to 124.08 from 114.84 at 129.89. Nonetheless, firm break of 121.61 will dampen our bullish view and bring deeper fall to 61.8% retracement at 119.02.

In the bigger picture, focus is back on 126.09 support turned resistance. Decisive break there will confirm completion of the down trend from 149.76. And in such case, rise from 109.20 is at the same degree and should target 141.04 resistance and above. Meanwhile, rejection from 126.09 and break of 114.84 will extend the fall from 149.76 through 109.20 low.

Euro Tumbles on Increasing Chance of Early Italian Election, Outlook Stays Bullish Though

Euro tumbles broadly this week as some traders are betting on an early election in Italy, that creates some political uncertainty again. Leaders of major political parties are going to discuss, in the coming weeks, a new electoral law with a proportional system similar to the German model. And it's believed that an agreement is close between the leaders that could pull ahead the elections original scheduled in early 2018. Former Prime Minister and Democratic Party leader Matteo Renzi, who's desperate to seek a come back after the referendum defeat, is pushing for an early election as soon as in September, at the same time as Germany's own election. But ultimately, the move would also require President Sergio Mattarella's decision to dissolve the government. After all, the markets are starting to price in the development.

Technically, EUR/USD failed to take out key resistance at 1.1298 and retreated. Near term outlook, though, stays bullish as long as 1.1020 support holds. EUR/JPY also lost momentum ahead of 126.09 key resistance. But similarly, near term outlook stays bullish as long 121.61 fibonacci level holds. EUR/GBP also lost momentum ahead of 0.8786 resistance but outlook stays mildly bullish as long as 0.8602 minor support holds. Overall, Euro remains the strongest major currency, next to Kiwi, for the month, as boosted by French election results and positive economic data.

ECB Draghi delivered cautious message to European parliament

ECB President Mario Draghi sounded cautious in the hearing in European parliament yesterday. Draghi said policy makers are "firmly convinced" that extraordinary amount of monetary policy support is "still necessary" for the Eurozone. He pointed out that support is needed for reabsorbing present level of "under-utilized resources" and for brining back inflation to 2% target and "durably stabilize" around there. Meanwhile, Draghi expects new staff economic projections at the June monetary policy meeting. ECB would then be able to reassess the risks to outlook for growth and inflation.

Currently, it's expected that the new June staff projections to provide upward revision to growth and inflation forecast, at least for 2017. ECB policies makers would probably start discussing exit of stimulus but there wouldn't be any decision made. Instead, Draghi might hint at an announcement of some sort in the September meeting, in particular as the current asset purchase program will end in December. So, there are still some food to digest for Euro traders in the June meeting.

May and Corbyn take different Brexit negotiation stance

In UK, the focus in the election to take place on June 8 could be starting to narrow to the parties' Brexit negotiation stance while Conservatives' lead over Labour has been narrowing. Prime Minister Theresa May is clear that she's taking a tough stance with the snap election to secure her mandate. And May reiterated that "no deal is better than a bad deal", and, "we have to be prepared to walk out". On the other hand, Labour leader Jeremy Corbyn set out a totally different approach and emphasized that "there's going to be a deal" and "we will make sure there is a deal".

The negotiation is scheduled to start on June 19. Ahead of that, EU's chief Brexit negotiator Michel Barnier urged the European MPs to be vigilant throughout the negotiation. Barnier wanted that once it leaves EU, UK could be "tempted to distance itself from our standards" like consumer projection or financial stability. And, he urged to ensure that this "inevitable divergence" won't become "unfair competition". And he emphasized "full transparency for these negotiations". He reiterated his stance with EU leaders that "sufficient progress" is needed on the issues of the "divorce bill", citizens right and Ireland border arrangements before the talk of a trade deal.

On the data front...

New Zealand building permits dropped -7.6% mom in April. Australia building approvals rose 4.4% mom in April. Japan unemployment rate was unchanged at 2.8% in April, household spending dropped -1.4% yoy, retail sales rose 3.2% yoy. Eurozone confidence indicators, Germany import price and CPI, France GDP will be featured in European session. Swiss will also release KOF leading indicator. In US, session, US personal income and spending, S&P Case-shiller house price and consumer confidence will be featured. Canada will release current account, IPPI and RMPI.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 124.03; (P) 124.33; (R1) 124.48; More...

EUR/JPY drops sharply to as low as 123.24 so far and deeper decline might be seen. But after all, it's staying in the consolidation pattern from 125.80. Hence, we'd expect downside to be contained by by 38.2% retracement of 114.84 to 125.80 at 121.61 to bring rise resumption. We're staying mildly bullish in the cross. And, break of 126.09 key resistance will extend the whole rebound from 109.03 to 100% projection of 109.03 to 124.08 from 114.84 at 129.89. Nonetheless, firm break of 121.61 will dampen our bullish view and bring deeper fall to 61.8% retracement at 119.02.

In the bigger picture, focus is back on 126.09 support turned resistance. Decisive break there will confirm completion of the down trend from 149.76. And in such case, rise from 109.20 is at the same degree and should target 141.04 resistance and above. Meanwhile, rejection from 126.09 and break of 114.84 will extend the fall from 149.76 through 109.20 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Apr | -7.60% | -1.80% | -1.20% | |

| 23:30 | JPY | Unemployment Rate Apr | 2.80% | 2.80% | 2.80% | |

| 23:30 | JPY | Household Spending Y/Y Apr | -1.40% | -0.70% | -1.30% | |

| 23:50 | JPY | Retail Trade Y/Y Apr | 3.20% | 2.20% | 2.10% | |

| 1:30 | AUD | Building Approvals M/M Apr | 4.40% | 3.00% | -13.40% | -10.30% |

| 6:00 | EUR | German Import Price Index M/M Apr | 0.10% | -0.50% | ||

| 6:45 | EUR | French GDP Q/Q Q1 P | 0.30% | 0.30% | ||

| 7:00 | CHF | KOF Leading Indicator May | 106.2 | 106 | ||

| 9:00 | EUR | Eurozone Business Climate Indicator May | 1.11 | 1.09 | ||

| 9:00 | EUR | Eurozone Economic Confidence May | 110 | 109.6 | ||

| 9:00 | EUR | Eurozone Industrial Confidence May | 3.1 | 2.6 | ||

| 9:00 | EUR | Eurozone Services Confidence May | 14.1 | 14.2 | ||

| 9:00 | EUR | Eurozone Consumer Confidence May F | -3.3 | -3.3 | ||

| 12:00 | EUR | German CPI M/M May P | -0.10% | 0.00% | ||

| 12:00 | EUR | German CPI Y/Y May P | 1.60% | 2.00% | ||

| 12:30 | CAD | Current Account (CAD) Q1 | -11.4B | -10.7B | ||

| 12:30 | CAD | Industrial Product Price M/M Apr | 0.80% | |||

| 12:30 | CAD | Raw Materials Price Index M/M Apr | -1.60% | |||

| 12:30 | USD | Personal Income Apr | 0.40% | 0.20% | ||

| 12:30 | USD | Personal Spending Apr | 0.40% | 0.00% | ||

| 12:30 | USD | PCE Deflator M/M Apr | 0.20% | -0.20% | ||

| 12:30 | USD | PCE Deflator Y/Y Apr | 1.70% | 1.80% | ||

| 12:30 | USD | PCE Core M/M Apr | 0.10% | -0.10% | ||

| 12:30 | USD | PCE Core Y/Y Apr | 1.50% | 1.60% | ||

| 13:00 | USD | S&P/Case-Shiller Composite-20 Y/Y Mar | 5.60% | 5.90% | ||

| 14:00 | USD | Consumer Confidence May | 120 | 120.3 |

Inflation Is The Key

Inflation is the Key

The shortened Memorial day week is chalk full of critical data but Tuesdays PCE and Friday’s Payrolls results will be crucial in shaping the markets near term structural view for the USD. Given the Fed’s concern about realised inflation, dealers will be directed to the Average Hourly Wages Friday as this week’s print can cause massive volatility in Financial Markets given the releases proximity to the anticipated June US interest rate hike

Similarly, Wednesday’s EU inflation data will play a significant role in Euro fortunes. Moreso given the market’s high expectations for a more hawkish change in the ECB’s forwarding guidance, While the markets have been watching ECB speeches more intently, ECB Draghi stuck to the script while addressing a committee of the European Parliament suggesting the ECB’s extraordinary amount of monetary policy support is still required.

While most markets sleep walked through yesterday’s session the same can not be said for the CNH as volumes s were trading well above average.The fallout from last week’s stronger CNY fixing and the latest funding squeeze are taking their toll on newly minted dollar longs and dampening enthusiasm for CNH trade. If this were the objective of the Pboc latest temper tantrum, after the Moody’s downgrade, the job was well done, given the huge carry, investors would likely prefer short USDCNH exposure. If the non-existent funding conditions persist, with T/N trading at 175 at one stage, we may see the USDCNH eventually test the key psychological 6.80 level as this short term carry is too juicy to ignore.

Euro

In early Asia, the EURO toppled from 1.1170 to 1.1130 after a headline surfaced that Greece may opt out of next payment without debt deal ( BILD). With the war of words escalation between the ECB and Greece regarding the inclusion in ECB bond buying program, the uptick in Greece risk premium is weighing on Eurozone sentiment.

The Euro was trading a tad dark as Draghi’s latest comments suggest the EU still needs stimulus, sounding much less hawkish than the market lean. The headline saw fast short term money take advantage of both market positioning and early morning liquidity to drive the Euro to lower with ease Positioning is a bit stretched on the EUR and EUR crosses so there could be some additional follow through on the headlines

Australian Dollar

The Aussie is under the gun in early trade more so from a general view that downside risk to the commodity space abounds rather than any one particular headline. With this dispirited near-term view for iron ore prices and the Feds all but certain to raise interest rates in June, the Aussie appears poised for a significant move lower

Japanese Yen

USDJPY has extended its decline below 111 as EURJPY positioning unwinds on this morning Greece headline But overall risk, in general, is struggling this morning on Greece and the latest UK election poll.

The Pound

But risk, in general, is struggling on the latest UK election poll.The gap between Conservatives and Labour parties is narrowing in the most recent polls in UK elections. The Times cites a Survation poll as showing that Conservatives are at 43% versus 37% for Labour- a lead of 6 points down from 9 points a week earlier.