Sample Category Title

Empire State Manufacturing Index Turns Negative In May

'We have been expecting some cooling in the manufacturing sector following a solid start to the year, but if the orders index proves to be a reliable forward-looking indicator, the slowdown could be more severe than we had been anticipating.' - Daniel Silver, JP Morgan

Manufacturing activity in the New York state deteriorated unexpectedly in May, falling into the negative territory for the first time since October, official figures revealed. The regional Federal Reserve reported on Monday that its Empire State Manufacturing Index came in at –1.0 in the reported month, following the preceding month's 5.2 points. Meanwhile, market analysts anticipated a climb to 7.2 in May. The drop may be a sign of an activity slowdown in the manufacturing sector. Back in February, the New York Fed Index hit 18.7 points, the highest level since September 2014, boosted by optimism over the US President Donald Trump's pro-growth initiatives. However, the following Trump momentum began to wane, as the White House failed to deliver on key promises. The New Orders Index came in at -4.4, down from April's 7.0 and marking the weakest level since September. The Employment Index declined slightly to 11.9 from 13.9 points registered in the prior month. Indexes assessing the six-month outlook was little changed, falling from 39.9 to 39.13 points in May.

British Prime Minister Theresa May Promises To Protect Workers

'The Tories (the Conservatives) have spent the last seven years prioritizing the few, opposing Labour's proposals to give workers more rights and overseeing wage stagnation which has left people worse off.' - Andrew Gwynne, Labour Party

On Monday, the British Prime Minister Theresa May, appointed after the country voted to leave the European Union on June 23, promised to extend British workers' rights in both workplace and boardroom. During her visit to the southern part of England, the UK PM said that the Conservative Party would protect workers of internet delivery firms and 'gig' companies, such as Uber. Furthermore, May stated they intended to put employees on company boards. Apart from that, the British Prime Minister promised to increase the national living wage and introduce a new family care leave system. The current national living wage for workers aged 25 and over is 7.50 pounds. Moreover, May said that if the nation votes for the Conservative Party it would also protect people with mental health problems. She also noted that she would use Brexit 'to extend the protections and rights'. Later on the day, the UK PM held her first Facebook Live session, during which the proposed policy was criticised for being unpaid. Moreover, the Liberal Party questioned the Conservatives' intentions and urged Britons not to trust the Tories.

Reserve Bank Of Australia Releases Minutes Of Its Latest Meeting

'[The minutes] share the optimistic tone of May's Statement on Monetary Policy, but the more recent data releases suggest that the RBA may have to become a bit more cautious.' - Paul Dales, Capital Economics

At its last meeting the Reserve Bank of Australia expressed concerns over subdued job growth and surging housing prices, the minutes of the Monetary Policy Committee meeting revealed on Monday. The RBA noted that inflation picked up over the past few months; therefore, the Bank projected that the inflation rate would likely hit its 2% target by 2018. Rising commodity prices combined with higher building materials and utilities prices provided a boost to inflation over the last few months. The Central bank also said that data released in April suggested that the economy grew at a moderate pace in the three-month period to March. Nevertheless, policymakers that interest rates and monetary policy would remain unchanged for the rest of this year due to weak job creation and high house prices in Sydney and Melbourne. Nevertheless, figures released by CoreLogic suggested that house prices started to decline slightly. The Bank also pointed to improving industrial output and both business and consumer sentiment. However, after the release, the Australian Dollar dropped to 74.21 against its US counterpart.

UK Inflation Data In Focus

Focus on today's UK inflation report

Later this afternoon, the UK will release April's inflation report. Following last week's BoE meeting, investors will undoubtedly react negatively to an upside surprise in inflation. Indeed, Mark Carney warned that UK consumers will be squeezed this year as price pressures pick-up. Headline inflation is expected to come in at 2.6% y/y from 2.3% in the previous month, while the core measure should rise from 1.8% y/y to 2.3%.

The BoE made clear that it won't raise borrowing costs should inflation pressure be fuelled by further GBP weakness, they would only do so if the UK gets a good divorce deal with the European Union. GBP/USD was up 0.40% this morning amid a broad-based USD sell-off. However, the pound lost ground against the single currency amid renewed hopes for a stronger European Union following Emmanuel Macron taking office.

EUR/GBP returned to 0.8537 on Tuesday morning and is currently trying to break its 50dma, which currently stands at 0.8541, to the upside. We maintain our long EUR / short GBP view on the pair, especially since Macron and Angela Merkel seem to want a closer relationship in order to shake up Europe. That does not bode well for the Brexit negotiation as it increases the odds that the EU will take a tougher stance towards the United Kingdom.

US data on deck

The lack of a real driver has created choppy directionless trading. Yet for today, traders' attentions will focus back on the US data for support of the Fed policy path. After yesterday's fall in the Empire State manufacturing headline index, expectations for evidence of economic strengthening will be needed. Much of the optimism around the US economy was driven by sentiment surveys, which in recent reads have declined from the elevated reading that came post-US election. That said, data coming from the US housing sector remains solid as the NAHB housing index rose to 70 in May from 68 in April. Today's Industrial Production should moderate from March's 0.5% rise to 0.4%.

Yet given the volatility in the indicator plus recent deceleration in sentiment, there is room for a downside disappointment. Housing starts with homebuilding activity strong and after a weak read in March, markets expect a recovery of 3.7% m/m.

There is also healthy consumer demand and solid labour markets (which is finally seeing wage gains) and while building permits should weaken slightly after a strong March down 0.2% from 3.6%, there is room yet for a quickening pace as the weather has been unseasonably warm. Weaker US data and domestic political confusion has dimmed expectations both for a faster Fed hiking cycle and faith in the USD (DXY fallen to 98.78 from 99.88).

However, the resilience of US short end yields suggest longer-term support for the USD. We caution investors from becoming too bearish on the USD ahead of 14th June Fed rate decision. The stability in US rates is the primary reason the USDJPY has not corrected further of the 114.38 resistance barrier.

Strong German economy brings optimism

The Eurodollar pair has broken 1.1000 following the French Presidential election. It seems markets are now leaving European political uncertainties behind. Yesterday, new French President Emmanuel Macron met with German Chancellor Angela Merkel and said he is willing to accelerate European construction, in particular the fiscal side.

For financial markets, the demand for euro is growing. In Germany, the ZEW confidence index - a survey of around 300 economists - is set to be issued and the consensus estimates the current situation in Germany is better. The German economy has been strong for the first quarter and investment and retail sales have been the key driver.

It is worth noting that Germany has a massive trading surplus and this is because the euro is way too low, given the strength of the country's economy. We reload our EUR bullish positions for the time being.

Technical Outlook: USDJPY – Bullish Bias Above 100SMA At 112.92

The pair stands at the back foot on Tuesday after failing to extend strong rally on Monday which also managed to register marginal close above pivot at 113.75 (broken Fibo 76.4%of 115.49/108.11 descend).

Overall picture remains biased higher for renewed attempts towards recent peaks and upside rejection at 114.36.

Rising daily Tenkan-sen that contained action of yesterday/ today, offers immediate support at 113.21, followed by key near-term support at 112.92 (100SMA) which is expected to hold current corrective phase and keep overall bulls intact.

Otherwise, stronger correction of 108.11/114.36 rally could be anticipated on sustained break below 100SMA pivot.

Res: 113.75, 113.93, 114.36, 114.87

Sup: 113.21, 113.07, 112.92, 112.38

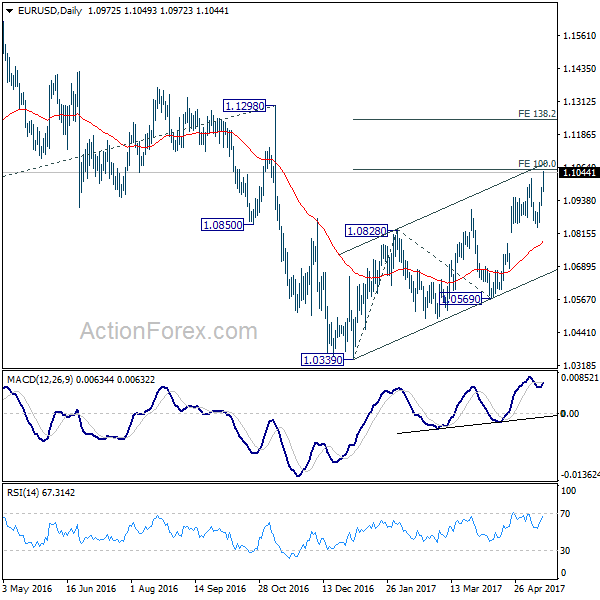

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0934; (P) 1.0962 (R1) 1.1001; More....

EUR/USD rises to as high as 1.0492 so far as recent rebound resumed after taking out 1.1020 resistance. Intraday bias is back on the upside for 100% projection of 1.0339 to 1.0828 from 1.0569 at 1.1058. Based on current momentum, this projection level would be taken out. In that case, EUR/USD would target 138.2% projection at 1.1245, which is close to 1.1298 key resistance. For now, rise from 1.0339 is still viewed as a corrective move. Hence we'd expect strong resistance below 1.1245/98 to limit upside and bring reversal. Nonetheless, break of 1.0838 support is needed to indicate short term topping. Otherwise, further rise will remain in favor even in case of retreat.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate long term reversal.

USD/JPY Analysis: Continues To Weaken

'And unfortunately for yen bulls, the weaker yen hasn't led to a pickup in Japanese exports. Until this happens, the yen will likely continue to weaken.' – Marc Chandler, BBH (based on Market Watch)

Pair's Outlook

A relatively strong recovery yesterday was almost sufficient to erase Friday's losses completely, leaving the USD/JPY pair just few pips away from that day's opening price. The Buck, however, remains under pressure and is likely to slide down due to a stronger Yen. The weekly pivot point is now the immediate support, but the cluster around 112.90 is much more reliable. A failure to find support around this area would open the way towards the 112.00 major level, where the 20-day SMA coincides with the 55-day one, but a plunge that far is out of reach for now.

Traders' Sentiment

Traders remain bearish towards the Greenback, as 65% of all open positions are currently short. At the same time, there are 52% of orders to acquire the US Dollar, up from 50% yesterday.

EUR/USD Analysis: Reaches Above 1.10 Mark

'The greenback, lower versus most of its G-10 peers, was down for a fourth day, with the Bloomberg dollar index nursing losses of about 0.2 percent after dropping to its lowest since April 26.' – Alexandria Arnold and Dennis Pettit, Bloomberg

Pair's Outlook

The common European currency continued to surge against the US Dollar on Tuesday morning. The currency exchange rate reached above the 1.10 mark and was set to score additional gains. The pair is most likely going to reach the resistance put up by the weekly R1, which is located at the 1.1025 level. Due to the fact that the first weekly resistance is strengthened by three more additional levels of significance, it is highly unlikely that the rate will pass the resistance cluster, which is located from 1.1025 to 1.1057. The rate is more likely to retreat after a few failed attempts.

Traders' Sentiment

SWFX market sentiment remains bearish, as 63% of open positions are short, and 61% of trader set up orders are to sell the Euro.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2867; (P) 1.2903; (R1) 1.2930; More...

GBP/USD is staying in tight range below 1.2987 and intraday bias stays neutral first. With 1.2830 minor support intact, another rise could be seen. However, firstly, price actions from 1.1946 are viewed as a corrective pattern. Secondly, bearish divergence condition is seen in 4 hour MACD. Hence, in case of another rise, we'd start to look for reversal signal again above 1.2987. Meanwhile, break of 1.2830 will indicate short term topping. In such case, intraday bias is turned back to the downside for 1.2614 resistance turned support first.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

GBP/USD Analysis: Puts Consolidation Trend At Risk

'Due to the level of expectation in the market for a big CPI number, the bigger risk is a disappointing number that could weigh on the Pound. Key support levels to watch include 1.2900 for GBP/USD and 0.8500 for EUR/GBP.' – City Index (based on PoundSterlingLive)

Pair's Outlook

Monday ended with the Sterling once again being unable to post solid gains against the US Dollar, thus, prolonging its consolidation trend for another day. Nevertheless, the Cable has the opportunity to reach the trend's resistance line at 1.30 today and possibly even break it. Although technical indicators are in favour of the positive outcome, it still remains somewhat unlikely, as the Pound is eventually expected to test the wedge's lower boundary near 1.28. Assuming the pair consolidates until next week, a good confirmation of both trend support's would be achieved around 1.2850—where they coincide.

Traders' Sentiment

Market sentiment reached a perfect equilibrium today, while pending orders are close to that as well, with 51% of them set to sell the British currency.