Sample Category Title

(BOE) Bank Rate Held at 0.25%, Government Bond Purchases at £435bn and Corporate Bond Purchases at up to £10bn

The Bank of England's Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 10 May 2017, the Committee voted by a majority of 7-1 to maintain Bank Rate at 0.25%. The Committee voted unanimously to maintain the stock of sterling non-financial investment-grade corporate bond purchases, financed by the issuance of central bank reserves, at £10 billion. The Committee also voted unanimously to maintain the stock of UK government bond purchases, financed by the issuance of central bank reserves, at £435 billion.

As the MPC observed at the time of the United Kingdom's referendum on EU membership, the appropriate path for monetary policy depends on the evolution of demand, potential supply, the exchange rate, and therefore inflation. Aggregate demand slowed markedly in 2017 Q1, and the MPC's central projection contained in the May Inflation Report is now for quarterly growth to remain around current rates, and close to trend. The slowdown appears to be concentrated in consumer-facing sectors, partly reflecting the impact of sterling's past depreciation on household income and spending. The Committee judges that consumption growth will be slower in the near term than previously anticipated before recovering in the latter part of the forecast period as real income picks up.

In the MPC's central forecast, weaker consumption this year is largely balanced by rising net trade and investment. The outlook for global activity continues to improve. Business surveys and Bank Agents' reports imply that business investment growth is likely to be higher in 2017 than previously projected. The stronger global outlook and the level of sterling are providing incentives for many exporters to renew and increase capacity.

Sterling appreciated by 2.5% between the February and May Inflation Reports, although it remained 16% below its November 2015 peak. Over the same time period, shorter-term UK interest rates fell, with the sterling yield curve used to condition the forecast close to its lowest level since the start of the year.

CPI inflation has risen above the MPC's 2% target as the depreciation of sterling has begun to feed through to consumer prices. This impact has been offset to some extent by continued subdued growth in domestic costs. In particular, wage growth has been notably weaker than expected. The MPC expects inflation to rise further above the target in the coming months, peaking a little below 3% in the fourth quarter. Conditioned on the market yield curve underlying the May projections, inflation is forecast to remain above the MPC's target throughout the forecast period. The projected overshoot entirely reflects the effects of the falls in sterling since late November 2015 on import prices. This effect is expected to diminish towards the end of the forecast period. With unemployment falling to its estimated equilibrium rate, however, wage growth is expected to recover significantly, and the drag from domestic costs to lessen, over the same period.

Monetary policy cannot prevent either the necessary real adjustment as the United Kingdom moves towards its new international trading arrangements or the weaker real income growth that is likely to accompany that adjustment over the next few years. Attempting to offset fully the effect of weaker sterling on inflation would be achievable only at the cost of higher unemployment and, in all likelihood, even weaker income growth. For this reason, the MPC's remit specifies that, in such exceptional circumstances, the Committee must balance any trade-off between the speed at which it intends to return inflation sustainably to the target and the support that monetary policy provides to jobs and activity.

In the MPC's latest projections there is such a trade-off through most of the forecast period, with a degree of spare capacity and inflation remaining above the 2% target. In the final year of the forecast, however, the output gap closes and inflation rises slightly further above the target. This is conditioned on the assumptions that the adjustment to the United Kingdom's new relationship with the European Union is smooth, and that Bank Rate follows the market-implied path for interest rates. At its May meeting, seven members thought that the current monetary policy setting remained appropriate to balance the demands of the Committee's remit. Kristin Forbes considered it appropriate to increase Bank Rate by 25 basis points.

As the Committee has previously noted, there are limits to the extent to which above-target inflation can be tolerated. The continuing suitability of the current policy stance depends on the trade-off between above-target inflation and slack in the economy, as well as the prospects for inflation to return sustainably to target. These projections depend importantly on three main judgements: that the lower level of sterling continues to boost consumer prices broadly as projected, and without adverse consequences for inflation expectations further ahead; that regular pay growth remains modest in the near term but picks up significantly over the forecast period; and that more subdued household spending growth is largely balanced by a pickup in other components of demand.

In judging the appropriate policy stance, the Committee will be monitoring closely the incoming evidence regarding these and other factors. Monetary policy can respond in either direction to changes to the economic outlook as they unfold to ensure a sustainable return of inflation to the 2% target. On the whole, the Committee judges that, if the economy follows a path broadly consistent with the May central projection, then monetary policy could need to be tightened by a somewhat greater extent over the forecast period than the very gently rising path implied by the market yield curve underlying the May projections.

Kiwi Dollar Crash Lands, Loonie Burnt

Global equities have continued their upward momentum as volatility takes a back seat after Macron victory in France's Presidential election, corporate earnings and U.S data has maintained positive sentiment about economic growth.

Amongst signs of a strengthening U.S labor force, investors are paying closer attention to comments from Fed officials for clues on the path for interest rates this year. The odds for a June hike are already baked in, but where to from there?

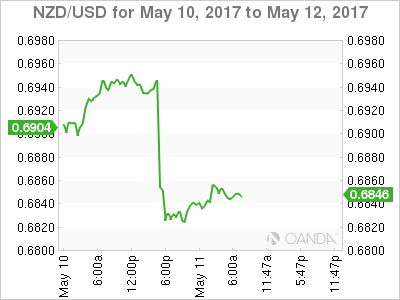

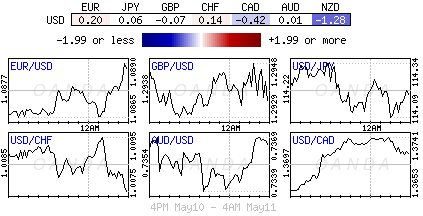

The Kiwi dollar crashed, falling more than -1.5% as the Reserve Bank of New Zealand (RBNZ) fails to live up to expectations, while Canada's loonie lost some of its shine after Moody's cut its credit ratings on six Canadian banks.

It's show time for the BoE – will sterling's double top £1.30 handle be penetrated today?

1. Global bourses hover near highs

Global stocks continue their advance, trading atop of their multi-year highs, supported mostly by a rebound in oil boosted energy producers.

In Japan, the broader Topix index rose +0.1%, while the Nikkei 225 climbed +0.3% aided by a weaker yen (¥114.11) helping exporters.

In China, the Shanghai Composite Index rallied +0.3%, the first positive day in seven sessions – investors continue to evaluate regulatory intervention in their financial markets.

In Hong Kong, the Hang Seng added +0.5%, while in New Zealand, the S&P/NZX 50 surged +0.9% to its highest level in 10-months on an unexpected ‘dovish' RBNZ (see below).

In Europe, the Stoxx Europe 600 fell -0.1%, after gaining +0.2% yesterday to its highest level in two-years. The FTSE is seeking guidance from today's BoE rate announcement.

U.S stocks are set to open in the red (-0.1%).

Indices: Stoxx50 -0.1% at 3641, FTSE flat at 7386, DAX flat at 12763, CAC-40 +0.1% at 5404, IBEX-35 -0.7% at 10961, FTSE MIB +0.2% at 21603, SMI +0.2% at 9107, S&P 500 Futures -0.1%.

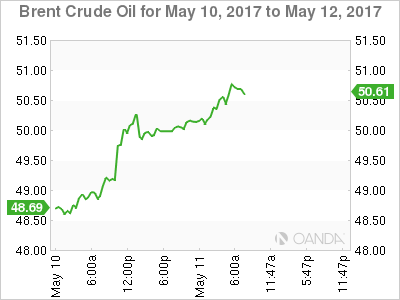

2. Oil up on falling U.S inventories, Saudi cuts to Asia

Ahead of the U.S open, oil prices remain better bid after yesterday's U.S data recorded a larger than expected fall in inventories and as the Saudi's announced a bigger than expected cut in supplies to Asia.

Brent futures are up +30c at +$50.52 a barrel, while U.S light crude (WTI) is up +35c at +$47.68.

U.S EIA data showed that crude inventories fell -5.2m barrels in the week to May 5, and at +522.5m barrels, crude stocks were the lowest since February.

Also tightening the market is Saudi Aramco announcement that they will reduce supplies to Asian customers by about -7m barrels in June.

Capping price gains is higher crude output from the U.S, particularly shale producers.

Note: OPEC meets on May 25 to decide on production policy for H2, 2017. The market expects the group to extend cuts until at least the end of the year.

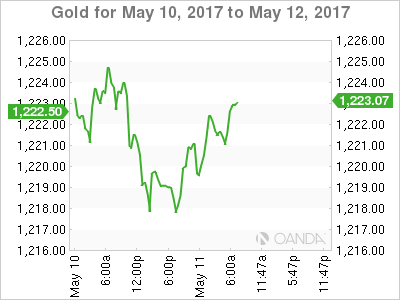

Gold (+0.2% to +$1,222.02) is steady ahead of the open, holding just above its two month low (+$1,2212) hit earlier this week, as the U.S dollar and stocks firm on expectations of a June rate hike.

3. BoE's 'Super Thursday'

It's the trifecta of events from the BoE today – rate announcement, quarterly inflation report and minutes (07:00 am GMT). Thirty minutes later (07:30 am GMT), Governor Carney will give a press conference.

The market consensus expects the BoE to revise higher its inflation outlook for the year and keep the benchmark rate unchanged at +0.25%. However, Governor Carney is bound to talk down expectations for a rate increase anytime soon. Fixed income dealers will be focusing on whether more than one person among those voting calls for a rate increase.

Elsewhere, Fed member turned ‘hawk' Eric Rosengren has warned that the central bank was in danger of lifting its foot off the policy accelerator too slowly, and called for more aggressive action to prevent the economy from overheating.

Dallas President Kaplan said his base-case for rate hikes this year is still three, but indicated that he's 'very cognizant' of the fact inflation pressures have been more muted.

The yield on U.S 10's has fallen -2 bps to +2.40%, after rising for the past three sessions. In New Zealand, its equivalent benchmark yield slipped -5bps to +3.02% on a ‘dovish' RBNZ (see below).

4. Kiwi Dollar Crash Lands, loonie burnt

NZD (N$0.6844) was ‘burnt' overnight, falling -1.5% outright, its lowest print in 11-months, when the RBNZ failed to promote the idea that it will raise interest rates this year (+1.75%).

Governor Wheeler suggested that the next move would be up, but not until the end of 2019. Markets had been pricing in tightening commencing in early 2018. The Governor cited 'extensive political uncertainty' around U.S trade and economic policy among reasons for holding rates steady.

Elsewhere, the loonie has lost its way in the overnight session with USD/CAD rallying +70 pips to a high print of C$1.3740 after Moody's cut its rating on Canada's top banks. However, CAD has found some support from the energy sector, capping those gains (C$1.3702) ahead of the U.S open.

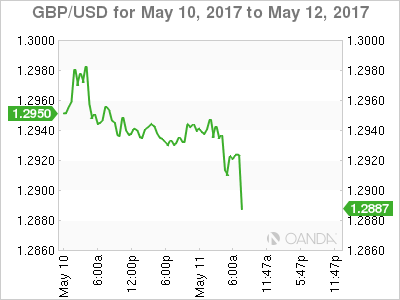

Ahead of the BoE rate announcement, the GBP (£1.2911) is weaker following data misses for March production data and wider trade deficits (see below). Next move depends on how ‘hawkish' members are.

5. U.K Industrial output disappoints, trade deficit widens

U.K. industrial production contracted in March (-0.5% vs. -0.4e m/m) as manufacturing output declined unexpectedly and unseasonably warm temperatures reduced demand for energy. Compared with the same month last year, industrial output was up +1.4%, missing market expectations of +1.9% growth.

Manufacturing output also disappointed, it declined by -0.6% versus market consensus of no change. Annual growth in manufacturing also missed expectations, with factory output growing by +2.3% vs. +2.5%e.

Other data also showed that the U.K's trade deficit (-£5.7B in Q1) with the world widened in March.

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD was indecisive yesterday. The bias remains bearish in nearest term testing 1.0850 key support which is a good place to buy with a tight stop loss as a clear break below that area would expose the pre-gap level at 1.0730 and the trend line support area as you can see on my H1 chart below. Immediate resistance remains around 1.0905 (H1 EMA 200). A clear break back above that area would give another chance to the bullish scenario testing 1.0950 or higher. Overall I remain neutral.

GBPUSD

The GBPUSD had another indecisive movement yesterday. The bias remains neutral in nearest term. Overall I still prefer a bullish scenario at this phase, but we have a triple top formation as you can see on my H1 chart below, which is not a good sign for the bullish trend. We need a clear break above 1.2985 to continue the bullish scenario. Immediate support is seen around 1.2900. A clear break below that area could trigger further bearish pressure testing 1.2865 – 1.2830 support area which remains a good place to buy with a tight stop loss.

USDJPY

The USDJPY attempted to push lower yesterday bottomed at 113.62 but closed higher at 114.28. The bias remains bullish in nearest term testing 115.00 area. Immediate support is seen around 114.00. A clear break below that area could lead price to neutral zone in nearest term testing 113.60 which is a good place to buy with a tight stop loss. Overall I still prefer a bullish scenario at this phase as a part of the bullish continuation scenario after broke above the trend line resistance as you can see on my H4 chart below.

USDCHF

The USDCHF was indecisive yesterday but overall still able to maintain its bullish bias since broke above the trend line resistance as you can see on my H4 chart below. The bias remains bullish in nearest term testing 1.0170 area. Immediate support is seen around 1.0050. A clear break below that area could lead price to neutral zone in nearest term as direction would become unclear. Overall I remain neutral.

DAX Shrugs Off Stronger German Inflation Report, German GDP Next

The DAX index continues to have a quiet week and is almost unchanged in the Thursday session. Currently, the DAX is trading at 12,765.00. On the release front, there are only a few events on the schedule. German WPI posted a gain of 0.3%, beating the estimate of 0.1%. The EU released its Spring 2017 Economic Forecast, which presented a generally optimistic picture of the economies of EU members. In the US, PPI is expected to show a slight gain of 0.2%, and unemployment claims is forecast to climb to 245 thousand. On Friday, Germany releases Preliminary GDP. It will be a busy day in the US, which will publish retail sales, CPI and consumer confidence.

ECB President Mario Draghi addressed a Dutch parliamentary committee on Tuesday, and reiterated that the ECB continues to monitor growth and inflation levels, but has no plans at present to modify its monetary policy. Draghi said that that central bank would tighten its policy once the “tail risks” of a drop in inflation receded and growth improved. Currently, the ECB is making monthly purchases of EUR 60 billion under its asset-purchase scheme, which is scheduled to expire in December. Inflation levels were higher in the first quarter, which led to calls for Draghi to tighten policy. However, the ECB was reluctant to make any moves during the French election campaign, and this aversion could continue, with Germany holding elections in September. Bottom line? We can expect the ECB to hold course, unless eurozone growth and inflation levels climb sharply.

The eurozone has posted stronger numbers in the first quarter, and this has included industrial better production and manufacturing numbers in Germany. Industrial production in March declined 0.4%, but this was just a blip, as industrial production in the first quarter posted a respectable gain of 1.6%. German Factory Orders came in at 1.0%, above the forecast of 0.7%. An improvement in global economic conditions has boosted the demand for German exports, notably cars and machinery. A weak euro has made European exports more attractive and helped boost the manufacturing sector. Germany releases Preliminary GDP for the first quarter on Friday, with the markets predicting a gain of 0.6%. A better than expected GDP report could shake the DAX out of its slumber and push the index to higher levels.

ECB Study Shows Eurozone Unemployment Higher than Official Data

Donald Trump's firing of FBI director James Comey has stunned political Washington. Trump has been embroiled in a number of controversies in his short presidency, but the political earthquake he has now stirred could become political quicksand. Comey, who has been conducting an investigation into possible collusion between Trump and Russia during the presidential campaign, clearly has been a thorn in Trump's side. The White House has claimed that it fired Comey over his handling of an email scandal involving Hillary Clinton, but the move has been roundly condemned by the Democrats, and some key Republicans have also voiced opposition as well. The firestorm could heat up further, with calls in Congress to appoint a special prosecutor into Trump's connections with Russia. Has Trump gone one step to far? If this controversy continues, jittery investors could send stock markets to lower levels.

CRUDE OIL – Extends Bullish Offensive On Correction

CRUDE OIL - With the commodity continuing to retain its recovery threats to close higher on Wednesday, more strength is expected in the days ahead. On the downside, support resides at the 47.00 level where a break will expose the 46.50 level. A cut through here will set the stage for a run at the 46.00 level. Further down, support resides at the 45.50 level. On the upside, resistance resides at the 48.00 level. Further out, resistance comes in at the 48.50 level. A break above here will aim at the 49.00 level and then the 49.50 level followed by the 50.00 level. All in all, CRUDE OIL remains biased to the upside on correction

GOLD Weakening, SILVER Weakening Towards $16.00, CRUDE OIL Bouncing Back.

GOLD Weakening.

Gold continues its decline after the yellow metal has faded near the hourly resistance at 1295 (18/04/2017 high). Hourly support is now located at 1195 (10/03/2017 low). The road is wide-open for further decline.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

SILVER Weakening towards $16.00.

Silver's bearish pressures are still lively. Strong support is given at 15.63 (20/12/2017 low). Closest support is given at 16.20 (04/05/2017 low). Key resistance is given at a distance at 19.00 (09/11/2017 high). Expected to see continued bearish pressures until at least $16.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

CRUDE OIL Bouncing back.

Crude oil is bouncing back on short-squeeze move. The commodity has bounced from a level below $44. Strong support is given at 42.20 (14/11/2017 low). Expected to see renewed bearish pressures.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 24.82 (13/11/2002) while resistance can now be found at 55.24 (03/01/2017 high).

Market Update – European Session: Focus On BOE Rate Decision And Whether More Dissenters Climb On Board

Notes/Observations

BOE expected to keep policy steady but the big question is whether more dissenters will join MPC member Forbes?

UK Mar Industrial and Manufacturing data misses; registers wider-than-expected trade deficits

EU Commission raises its GDP growth forecasts of euro zone for both 2017 and 2018

Overnight:

Asia:

New Zealand Central Bank (RBNZ) left its Official Cash Rate (OCR) unchanged at 1.75% (as expected). Monetary policy to remain accommodative for a considerable period. Numerous uncertainties remain and policy might need to adjust accordingly. Headline inflation to reach to midpoint of their target band over the medium term while growth overall remained positive. The Overall Cash Rate (OCR) seen steady at 1.8% over the two-year horizon period

RBNZ Gov Wheeler: Lack of inflation pressure is the main reason for maintaining neutral stance. Have not seen acceleration of wage pressures.

RBNZ's McDermott: RBNZ saw as much chance of a rate cut as a hike adding that markets were ignoring downside risks

Europe:

UK Apr RICS House Price Balance beats expectations but still matched its 7-month low (22% v 20%e)

Americas:

Treasury official: Treasury Sec Mnuchin will discuss Russia and Iran sanctions issues with G7 as well as discuss Trump administration's tax and regulatory reform efforts

Energy:

Saudis to inform OPEC that Saudi April output raised to 9.95M bpd (prior 9.90M bpd in March)

Economic Data

(JP) Japan Apr Eco Watchers Current Survey: 48.1 v 47.8e; Outlook Survey: 48.8 v 48.2e

(DE) Germany Apr Wholesale Price Index M/M: 0.3% v 0.0% prior; Y/Y: 4.7% v 4.7% prior

(TR) Turkey Mar Current Account Balance: -$3.1B v -$3.2Be

(CH) Swiss Apr CPI M/M: 0.2% v 0.2%e; Y/Y: 0.4% v 0.5%e

(CH) Swiss Apr CPI EU Harmonized M/M: 0.5% v 0.1% prior; Y/Y: 0.7% v 0.5% prior

(SE) Sweden Apr CPI M/M: 0.6% v 0.4%e; Y/Y: 1.9% v 1.7%e

(SE) Sweden Apr CPI CPIF M/M: 0.6% v 0.4%e; Y/Y: 2.0% v 1.8%e

(PH) Philippines Central Bank (BSP) left its Overnight Borrowing Rate unchanged at 3.00% (as expected)

(UK) Mar Industrial Production M/M: -0.5% v -0.4%e; Y/Y: 1.4% v 2.0%e

(UK) Mar Manufacturing Production M/M: -0.6% v -0.2%e; Y/Y: 2.3% v 3.0%e

(UK) Mar Visible Trade Balance: -£13.4B v -£11.6Be; Overall Trade Balance: -£4.9B v -£3.0Be; Trade Balance Non EU: -£4.7B v -£3.3Be

Fixed Income Issuance:

(SE) Sweden sold SEK750M vs. SEK750M indicated in 0.125% I/L 2027 bond; Avg Yield: -1.0527% v -1.0657% prior; Bid-to-cover: 1.92x v 1.46x prior

(IT) Italy Debt Agency (Tesoro) sold total €2.5B vs.€1.75-2.5B indicated range in 2044 and 2047 BTP Bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Indices [Stoxx50 -0.1% at 3641, FTSE flat at 7386, DAX flat at 12763, CAC-40 +0.1% at 5404, IBEX-35 -0.7% at 10961, FTSE MIB +0.2% at 21603, SMI +0.2% at 9107, S&P 500 Futures -0.1%]

Equities

Consumer discretionary [ SuperGroup [SGP.UK] -7.0% (Earnings)]

Industrials: [ Deutsche Post [DPW.DE] -3.5% (Earnings)]

Financials: [Unicredit [UCG.IT] +3.7% (Earnings), Credit Agricole [ACA.FR] -1% (Earnings), Aegon [AGN.NL] -5.2% (Earnings)]

Telecom: [BT [BT.UK] -3.2% (Earnings), Telefonica [TEF.ES] -2.8% (Earnings),

Healthcare: [Hikma Pharma [HIK.UK] -7.8%, Vectura [VEC.UK] -89.4% (update on the status of its ANDA for generic Advair Diskus, low likelihood of approval this year)]

Energy: [SolarWorld [SWVK.DE] -79% (Files for insolvency)]

Speakers

ECB publishes Economic Bulletin which reiterated the Draghi press conference that it would maintain a very substantial monetary accommodation. If the outlook became less favorable, the Governing Council stood ready to increase the asset purchase program in terms of size and/or duration.

EU Commission Spring Economic Forecast raised its GDP growth forecasts of euro zone for both 2017 and 2018. Raised Euro Zone 2017 GDP growth from 1.6% to 1.9% and 2018 GDP growth from 1.8% to 1.9%. On inflation the EU raised 2017 Euro Area inflation (HICP) from 1.7% to 2.0% and maintained 2018 Euro Area inflation (HICP) at 1.4%

Norway revised its 2017 budget and maintains 2017 Mainland GDP growth forecast at 1.6%. Cut 2017 Core CPI forecast from 2.1% to 1.7%

Philippines Central Bank Policy Statement noted that inflation risks were tilted to the upside and would remain vigilant against CPI risks. It would adjust policy as needed

Iraq Oil Min Al-Luaibi: Iraq raising oil output to 5M bpd will not conflict with OPEC's cuts; Reiterated OPEC view that OPEC and non-OPEC consensus view was to extend cuts for 6-months

Currencies

The focus was on the BOE rate decision and whether more hawks will show their feathers. With a vacancy on the MPC analyst foresee a 7-1 vote for unchanged rates instead of 8-1 (Dep Gov Hogg resigned a few weeks ago). Updated economic projections contained within the May BoE QIR will likely show modest downside revisions to both growth and inflation. If more hawks appear the GBP/USD could see another attempt on the $1.3000 level. The GBP was weaker following data misses for Mar production data and wider trade deficits and hovering just above its 1-week low of 1.2902

During Asia the NZD currency (Kiwi) saw volatility following the RBNZ rate decision which was viewed more neutral than anticipated. RBNZ was looking past the rising inflation with its neutral stance given the recent cooling in Auckland housing market, and its latest projections only see the next rate hike in late 2019 compared to analyst projections of late 2018. The NZD/USD pair fell to 10month lows below 0.6820 on the decision before recovering slightly

Fixed Income

Bund futures trade at 160.17 down 16 ticks, breaking through trend support at the 160.22 region. A break of 160.01 support level could see lows target 159.01 followed by 157.50. Resistance lies at 160.81 level followed by 162.10.

Gilt futures trade at 127.18 modestly lower by 3 ticks, after initially trade much lower ahead of the Industrial data, which disappointed across the board. The focus will remain on the BOE rate decision later today. A continuation of the pullback from the 129.14 April 18th high has price eyeing the 126.41 support level. An acceleration lower could test the 125.80 region. Resistance stands at 128.01 then 128.51 followed by 129.14.

Thursday’s liquidity report showed Wednesday’s excess liquidity ticked lower to €1.6537T a decline of €0.3B from €1.6540T prior. Use of the marginal lending facility fell to €232M from €342M prior.

Corporate issuance saw over $4.4B come to market via 4 issues headlined by RBS $3.2B in a 2-part senior unsecured note offering

Looking Ahead

(IT) Italy Debt Agency (Tesoro) to sell €3.75-4.75B in 2020 and 2024 BTP Bonds

05:30 (ZA) South Africa Mar Total Mining Production M/M: No est v 2.9% prior ; Y/Y: 4.7%e v 4.6% prior; Gold Production Y/Y: No est v -16.8% prior; Platinum Production Y/Y: No est v 47.2% prior

05:30 (DE) German Chancellor Merkel with NATO Sec Gen Stoltenberg in Berlin

05:30 (HU) Hungary Debt Agency (AKK) to sell Bonds (3 tranches)

06:00 (PT) Portugal Apr CPI M/M: No est v % prior; Y/Y: No est v % prior

06:00 (PT) Portugal Apr CPI Harmonized M/M: No est v % prior; Y/Y: No est v % prior

06:00 (IE) Ireland Apr CPI M/M: No est v 0.6% prior; Y/Y: No est v 0.7%prior

06:00 (IE) Ireland Apr CPI EU Harmonized M/M: No est v 0.6% prior; Y/Y: No est v 0.6%prior

06:25 (US) Fed’s Dudley (voter, dove) in India

06:30 (IS) Iceland to sell Bills

06:45 (US) Daily Libor Fixing

07:00 (UK) Bank of England Bank (BOE) Interest Rate Decision: Expected to leave Interest Rates unchanged at 0.25%; maintain Asset Purchase Target (AFT) at £435B

07:00 (UK) Bank of England Bank (BOE) May Minutes

07:00 (UK) Bank of England Bank (BOE) Quarterly Inflation Report (QIR)

07:00 (ZA) South Africa Mar Manufacturing Production M/M: +0.5%e v -0.4% prior; Y/Y: -2.4%e v -3.6% prior

07:00 (BR) Brazil May IGP-M Inflation (1st Preview): -0.6%e v -0.7% prior

07:30 (UK) BOE Gov Carney QIR press conference

08:00 (UK) Apr NIESR GDP Estimate: 0.4%e v 0.5% prior

08:00 (BR) Brazil CONAB Report

08:00 (BR) Brazil Mar Retail Sales M/M: -0.6%e v -0.2% prior; Y/Y: -1.8%e v -3.2% prior

08:00 (BR) Brazil Mar Broad Retail Sales M/M: -0.1%e v +1.4% prior; Y/Y: +0.4%e v -4.2% prior

08:15 (UK) Baltic Dry Bulk Index

08:30 (US) Initial Jobless Claims: 245Ke v 238K prior; Continuing Claims: 1.98Me v 1.964M prior

08:30 (US) Apr PPI Final Demand M/M: +0.2%e v -0.1% prior; Y/Y: 2.2%e v 2.3% prior

08:30 (US) Apr PPI Ex-Food&Energy M/M: 0.2%e v 0.0% prior; Y/Y: 1.6%e v 1.6% prior

08:30 (US) Apr PPI Ex-Food, Energy & Trade M/M: 0.2%e v 0.1% prior; Y/Y: No est v 1.7% prior

08:30 (CA) Canada Mar New Housing Price Index M/M: 0.2%e v 0.4% prior; Y/Y: No est v 3.3% prior

08:30 (US) Weekly USDA Net Export Sales

09:00 (RU) Russia Gold and Forex Reserve w/e May 5th: No est v $401.1B prior

10:30 (US) Weekly EIA Natural Gas Inventories

11:00 (US) Treasury announces issuance for upcoming 10-year Tips auctions for May 18th

11:00 (BR) Brazil to sell Fixed Rate 2023 and 2027 Bonds

11:00 (BR) Brazil to sell 2019, 2020, 2027 LTN Bills

12:30 (CH) IMF's Obstfeld speaks in Geneva

13:00 (US) Treasury to sell 30-Year Bonds

EUR/JPY Bullish Pause, EUR/GBP Weakening, EUR/CHF Fading Below 1.1000.

EUR/JPY Bullish pause.

EUR/JPY's bullish run has stalled below range resistance at 124.59 (07/05/2017 high), Hourly resistance can be located at 124.43 (intraday low). Major support is given at 114.90 (18/04/2017low). Expected to see further renewed buying pressures towards 125.00.

In the longer term, the technical structure validates a medium-term succession of lower highs and lower lows. As a result, the resistance at 149.78 (08/12/2014 high) has likely marked the end of the rise that started in July 2012. Strong support at 94.12 (24/07/2012 low) looks nonetheless far away.

EUR/GBP Weakening.

EUR/GBP is trading lower. The technical structure remains negative as long as the resistance at 0.8530 (25/04/2017 low) holds. Expected to show continued weakness until support given at 0.8304 (05/12/2017 low).

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.

EUR/CHF Fading below 1.1000.

EUR/CHF's volatility is getting stronger. Resistance given at has been broken 1.0898 (08/12/2017 high). Despite the sharp increase and the recent bullish breakout which is very likely psychological, we believe that the medium-term pattern suggests us to see at some point renewed bearish pressures towards key support that can be found at 1.0623 (24/06/2016 low).

In the longer term, the technical structure is mixed. Resistance can be found at 1.1200 (04/02/2015 high). Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

USD/CHF Bullish Pause, USD/CAD Range Bound, AUD/USD Bearish Pause.

USD/CHF Bullish pause.

USD/CHF has paused after sharp reversal off 0.9864 low. The technical structure has invalidated the short-term negative momentum. Hourly resistance is given at 1.0107 (10/04/2017 high). Support can be located at 1.0049 (10/05/2017 low).

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/CAD Range bound.

USD/CAD has declined after failing to reach 1.3800 before bouncing back. Hourly support can be found at 1.3411 (24/04/2017 high) then 1.3353 (20/01/2017 high). Expected to show renewed bullish pressures as long as the pair remains above 1.3530 (27/04/2017 low).

In the longer term, there is a golden cross with the 50 dma crossing the 200 dma indicating further upside pressures. Strong resistance is given at 1.4690 (22/01/2016 high). Long-term support can be found at 1.2461 (16/03/2015 low).

AUD/USD Bearish pause.

AUD/USD has paused above key support at 0.7339 (intraday low). As long as prices remain below the resistance at 0.7608 (17/04/2017 high), the short-term technical structure is negative. Key resistance stands at 0.7681 (30/03/2017 high). Expected to show further weakness.

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.

EUR/USD Short-Term Weakness, GBP/USD Pushing Higher Towards 1.3000, USD/JPY Bullish!!

EUR/USD Short-term weakness.

EUR/USD is trading lower. Hourly support is given at 1.0852 (27/04/2017 low) then 1.0682 (21/04/2017 base). Stronger support can be found at 1.0494 (22/02/2017 low). Expected to show another leg higher towards 1.10.

In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD Pushing higher towards 1.3000.

GBP/USD is trading mixed. The pair is trading around former hourly resistance given at 1.2966 (30/04/2017 high). Hourly support can be found at 1.2757 (21/04/2017 low). An unlikely break of this support would indicate further weakness. Expected to push higher.

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY Bullish!!

USD/JPY is pushing higher since the pair broke resistance given at 112.20 (31/03/2017 high). Hourly support can be found at 110.88 (26/04/2017 low). Stronger support is located at 108.13 (17/04/2017 low). Other key supports lie at a distant 106.04 (11/11/2016 low). Expected to show continued bullish pressures.

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).