Sample Category Title

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.81; (P) 114.09; (R1) 114.56; More...

A temporary top is in place at 114.36 in USD/JPY and intraday bias is turned neutral. Some consolidations could be seen but downside of retreat should be contained by 112.08 support and bring another rally. Outlook remains unchanged that correction from 118.65 has completed with three waves down to 108.12. Above 114.36 will target 115.49 resistance first. Break will resume larger rally from 98.97 to 125.85 high.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Meanwhile, break of 115.49 resistance will extend the rise from 98.97 to retest 125.85. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

Bank of England Downgrades UK Growth Forecast

The Bank of England (BoE) has lowered its economic growth forecast for the UK to 1.9 percent, lower than February's prediction of 2.0 percent. The BoE says that the downgrade follows a slowing in consumer spending. Rising inflation and poor income growth were cited as the main reasons for consumers feeling the squeeze; reflected in disappointing retail sales data and a surprisingly steep drop in new car sales.

As was widely anticipated, interest rates remain at 0.25 percent.

David Johnson, Director at Halo Financial, comments, "While the latest Consumer Spending and Gross Domestic Product (GDP) data disappointed, recent Purchasing Managers' Index (PMI) results have, in contrast, looked very positive, providing some extra momentum for the Pound and balancing sentiment to some degree."

"In advance of today's "Super Thursday" announcements, Sterling was on the rise again, reaching rates against its major currency partners not seen for months and even years. The Pound was testing the EUR 1.20 level and the USD 1.30 level. However, immediately following today's release of BoE Monetary Policy Committee meeting minutes, Sterling fell against both the Euro and US Dollar from the highs seen early this morning; falling by 0.40 percent and 0.43 percent respectively."

He continues, "Despite all these key economic figures being released and the jumpiness of the Pound in response, we believe markets will continue to focus on the UK general election and the ongoing Brexit negotiations, which are likely to have a greater impact on Sterling than snapshot economic data and forecasts. Volatility and uncertainty will continue for the Pound in its major currency pairings. We are seeing that in movement across the Euro, US Dollar, and Australian Dollars, in particular."

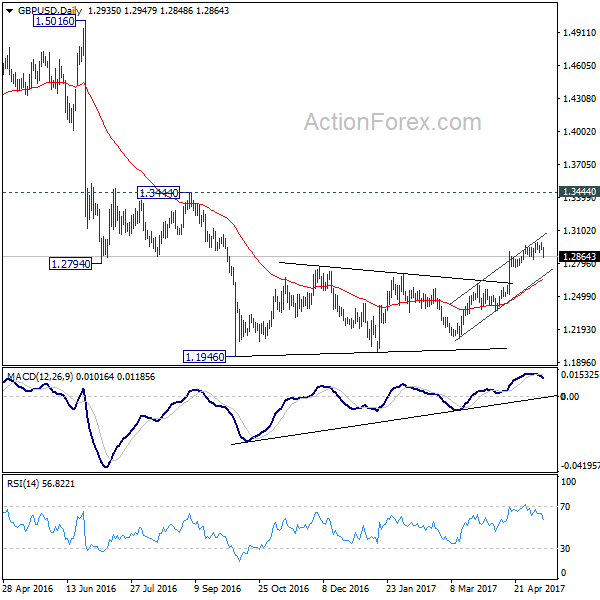

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2913; (P) 1.2950; (R1) 1.2974; More...

GBP/USD drops sharply today but stays above 1.2830 minor support so far. Intraday bias is neutral first. Another rise cannot be ruled out, but upside momentum is clearly weak with bearish divergence condition in 4 hour MACD. Also, current rally is seen as part of the corrective pattern from 1.1946. Hence, even in case of another rally, we'll look for reverse signal above 1.2987. Meanwhile, break of 1.2830 support will indicate short term topping. In such case, intraday bias will be turned back to the downside for 1.2614 support.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

British Pound Sold Off after Mixed BoE Projections, Threatening Reversal

Sterling drops sharply after BoE left monetary policies unchanged as widely expected. The updated projections are mixed at best. And more importantly, they were based on the assumption of a "smooth" Brexit, which isn't clearly defined by the central bank. Markets are clearly unhappy with the announcement and the pound suffers steep selloff. Focus will now be on 1.2830 in GBP/USD and a firm break there will indicate near term reversal. On the other hand, the greenback is trying to extend this week's rebound against Euro after solid economic data including PPI and jobless claims. But momentum in Dollar is unconvincing so far. New Zealand Dollar remains the weakest one after RBNZ disappointment.

BoE delivered mixed economic projections

BoE left key interest rate unchanged at 0.25% with 7-1 vote. Kristin Forbes remained the only one voting for a hike. Meanwhile, Charlotte Hogg did not participate. Asset purchase target was held at GBP 435b by 8-0 vote. In the quarterly Inflation Report, UK growth is projected to be at 1.9% in 2017, revised down from prior 2.0%. Growth projections for 2018 and 2019 were revised up, to 1.7% and 1.8% respectively, from 1.6% and 1.7%.

For inflation, BoE raised 2017 CPI projections to 2.7%, up from prior 2.4%. However, for 2018 and 2019, inflation is projected to be 2.6% and 2.2%, down from prior 2.8% and 2.5%. It also noted that "through its effects on costs, the fall in sterling is likely to keep inflation above the 2% target throughout the next three years."

The central bank also noted that "if the economy follows a path broadly consistent with the May central projection, then monetary policy could need to be tightened by a somewhat greater extent over the forecast period than the very gently rising path implied by the market yield curve underlying the May projections." However, BoE also emphasize that "this is conditioned on the assumptions that the adjustment to the United Kingdom's new relationship with the European Union is smooth, and that Bank Rate follows the market-implied path for interest rates."

Released from UK, industrial production dropped -0.5% mom, rose 1.4% yoy in March. Manufacturing production dropped -0.5% mom, rose 2.3% yoy in March. Construction output dropped -0.7% mom in March. Visible trade deficit widened to GBP -13.4b in March. RISC house price balance was unchanged at 22 in April.

US continuing claims dropped to 28 year low

Initial jobless claims dropped -2k to 236k in the week ended May 6, below expectation of 245k. Initial claims now stayed below 300k threshold for 114 straight weeks. Continuing claims dropped -61k to 1.91m in the week ended April 29. That's the lowest level since November 1988. PPI rose 0.5% mom, 2.5% yoy in April, above expectation of 0.2% mom, 2.2% yoy. Core PPI rose 0.4% mom, 1.9% yoy, above expectation of 0.2% mom, 1.7% yoy.

New York Fed Dudley: Protectionism is a dead end

New York Fed President William Dudley said that "protectionism can have a siren-like appeal". And, "viewed narrowly, it may be potentially rewarding to particular segments of the economy in the short term." But he warned that "viewed more broadly, it would almost certainly be destructive to the economy overall in the long term." He further said that "there are many approaches to dealing with the costs of globalization, but protectionism is a dead end." Also, "trying to achieve a high standard of living by following a policy of economic isolationism will fail." Nonetheless, Dudley didn't mention US President Donald Trump and administration in his speech.

Boston Fed Rosegren: Three more hikes this year

Yesterday, Boston Fed President Eric Rosengren mapped out a more hawkish policy path for Fed this year. He noted that Fed should hike three more times this year. In parallel, Fed should also start shrinking the balance sheet. That is, he doesn't advocate a "brief pause". Rosengren said that "along with a gradual reduction in the level of the balance sheet, it would still be reasonable to have three rate increases over the remainder of this year." And "I do not regard the weakness in first quarter data as a harbinger of softness in the underlying economy, and the strength of the labor market report on Friday provides some strong confirmation of that view."

Kiwi tumbled after RBNZ

RBNZ left the OCR unchanged at 1.75% in May. Policymakers shrugged off the recent NZD depreciation and the rise in inflation, indicating that the monetary policy would likely stay unchanged for the rest of the year and probably until 2020 before tightening. The market was disappointed by the lack of hawkish comments and the unchanged forward guidance. Down -1.85, NZDUSD slumped to an 11-month low of 0.6816 after the announcement. More in RBNZ To Leave Rates Unchanged Until 2020, Downplayed Rising CPI And NZD Weakness

ECB Draghi: Too early to declare success

ECB President Mario Draghi said at a Dutch Parliament hearing yesterday that "the economic recovery has evolved from being fragile and uneven into a firming, broad-based upswing. However, he emphasized that "it is too early declare success". Draghi said that incoming data "confirm that cyclical recovery of the euro area economy is becoming increasing solid and that downside risks have further diminished. But, "underlying inflation pressures continue to remain subdued and have yet to show a convincing upward trend." And, the "time to exit or to time to think about exit or not" hasn't come yet. Draghi said "this will happen when inflation" is durable, "self-sustained, and it's for the whole of the euro area."

Also from Europe, Germany WPI rose 0.3% mom in April. Swiss CPI rose 0.2% mom, 0.7% yoy in April.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2913; (P) 1.2950; (R1) 1.2974; More...

GBP/USD drops sharply today but stays above 1.2830 minor support so far. Intraday bias is neutral first. Another rise cannot be ruled out, but upside momentum is clearly weak with bearish divergence condition in 4 hour MACD. Also, current rally is seen as part of the corrective pattern from 1.1946. Hence, even in case of another rally, we'll look for reverse signal above 1.2987. Meanwhile, break of 1.2830 support will indicate short term topping. In such case, intraday bias will be turned back to the downside for 1.2614 support.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% | 1.75% | |

| 23:01 | GBP | RICS House Price Balance Apr | 22% | 20% | 22% | |

| 05:00 | JPY | Eco Watchers Survey Current Apr | 48.1 | 47.8 | 47.4 | |

| 06:00 | EUR | German Wholesale Price Index M/M Apr | 0.30% | 0.10% | 0.00% | |

| 07:15 | CHF | CPI M/M Apr | 0.20% | 0.20% | 0.20% | |

| 07:15 | CHF | CPI Y/Y Apr | 0.70% | 0.50% | 0.60% | |

| 08:00 | EUR | ECB Economic Bulletin | ||||

| 08:30 | GBP | Industrial Production M/M Mar | -0.50% | -0.40% | -0.70% | -0.80% |

| 08:30 | GBP | Industrial Production Y/Y Mar | 1.40% | 1.90% | 2.80% | 2.50% |

| 08:30 | GBP | Manufacturing Production M/M Mar | -0.60% | -0.20% | -0.10% | -0.30% |

| 08:30 | GBP | Manufacturing Production Y/Y Mar | 2.30% | 3.00% | 3.30% | 3.00% |

| 08:30 | GBP | Construction Output M/M Mar | -0.70% | 0.30% | -1.70% | |

| 08:30 | GBP | Visible Trade Balance (GBP) Mar | -13.4B | -11.6B | -12.5B | -11.4B |

| 09:00 | EUR | European Commission Economic Forecasts | ||||

| 11:00 | GBP | BoE Rate Decision | 0.25% | 0.25% | 0.25% | |

| 11:00 | GBP | BoE Asset Purchase Target May | 435B | 435B | 435B | |

| 11:00 | GBP | MPC Official Bank Rate Votes | 1--0--7 | 1--0--8 | 1--0--8 | |

| 11:00 | GBP | MPC Asset Purchase Facility Votes | 0--0--8 | 0--0--9 | 0--0--9 | |

| 11:00 | GBP | BoE Inflation Report | ||||

| 12:00 | GBP | NIESR GDP Estimate Apr | 0.20% | 0.40% | 0.50% | |

| 12:30 | CAD | New Housing Price Index M/M Mar | 0.20% | 0.30% | 0.40% | |

| 12:30 | USD | PPI M/M Apr | 0.50% | 0.20% | -0.10% | |

| 12:30 | USD | PPI Y/Y Apr | 2.50% | 2.20% | 2.30% | |

| 12:30 | USD | PPI Core M/M Apr | 0.40% | 0.20% | 0.00% | |

| 12:30 | USD | PPI Core Y/Y Apr | 1.90% | 1.70% | 1.60% | |

| 12:30 | USD | Initial Jobless Claims (MAY 06) | 236K | 245K | 238K | |

| 14:30 | USD | Natural Gas Storage | 67B |

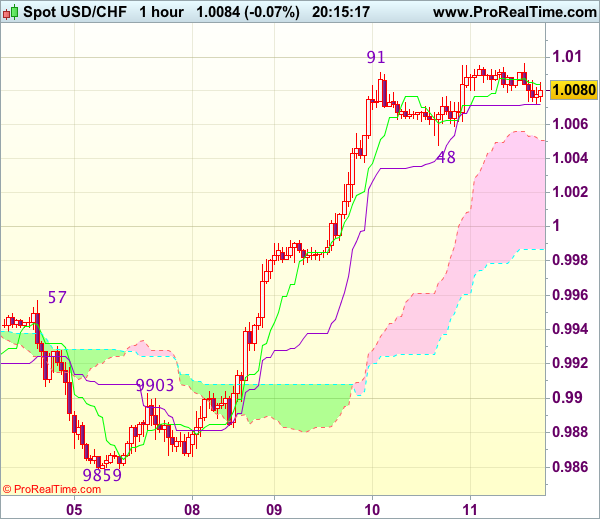

Trade Idea Update: USD/CHF – Buy at 1.0015

USD/CHF - 1.0088

Original strategy :

Buy at 1.0015, Target: 1.0115, Stop: 0.9980

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0015, Target: 1.0115, Stop: 0.9980

Position : -

Target : -

Stop : -

As the greenback has continued trading with a firm undertone after this week’s rally, adding credence to our view that recent upmove is still in progress and may extend further gain to previous resistance at 1.0108, break there would confirm resumption of early rise and encourage for headway to 1.0130 and then 1.0150-55 which is likely to hold from here due to loss of near term upward momentum.

In view of this, would not chase this rise here and we are looking to buy dollar on pullback as 1.0010-15 should limit downside. Only below previous resistance at 0.9957 would defer and suggest top is possibly formed, bring test of 0.9920-25 but break of previous resistance at 0.9903 is needed to add credence to this view, bring further fall to 0.9880-85.

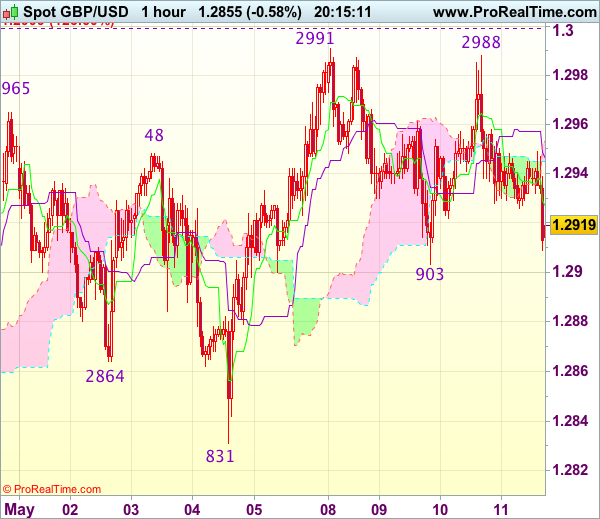

Trade Idea Update: GBP/USD – Sell at 1.2900

GBP/USD - 1.2858

New strategy :

Sell at 1.2900, Target: 1.2800, Stop: 1.2935

Position : -

Target : -

Stop : -

As cable has dropped below support at 1.2903 (now resistance) on dovish BOE, signaling top is formed at 1.2991 earlier and consolidation with downside bias is seen for further fall to 1.2831 support, break there would add credence to this view and extend the fall from 1.2991 top to 1.2805 and later towards 1.2770 but reckon previous support at 1.2757 would hold from here.

In view of this, we are looking to sell cable on recovery as said resistance at 1.2903 should limit upside and bring another decline. Above 1.2930-35 would risk test of 1.2950-60 but break there is needed to signal low is formed, bring another bounce towards 1.2988-91 resistance but break of 1.2999-00 (1.236 times projection of 1.2109-1.2616 measuring from 1.2365 and psychological resistance) is needed to revive bullishness.

Trade Idea Update: EUR/USD – Sell at 1.0930

EUR/USD - 1.0850

Original strategy :

Sell at 1.0955, Target: 1.0855, Stop: 1.0990

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0930, Target: 1.0820, Stop: 1.0965

Position : -

Target : -

Stop : -

As the single currency has remained under pressure after this week’s selloff, adding credence to our view that the fall from 1.1025 top is still in progress, hence bearishness remains for this decline to bring at least a strong retracement of early upmove towards 1.0825-30, then 1.0800 but reckon 1.0770-75 would hold from here due to near term overbought condition.

In view of this, we are looking to sell euro on recovery as 1.0930-35 should limit upside. Above 1.0955-60 would defer and risk a stronger rebound but still reckon upside would be limited to resistance at 1.0997 and price should falter below this week’s high at 1.1025.

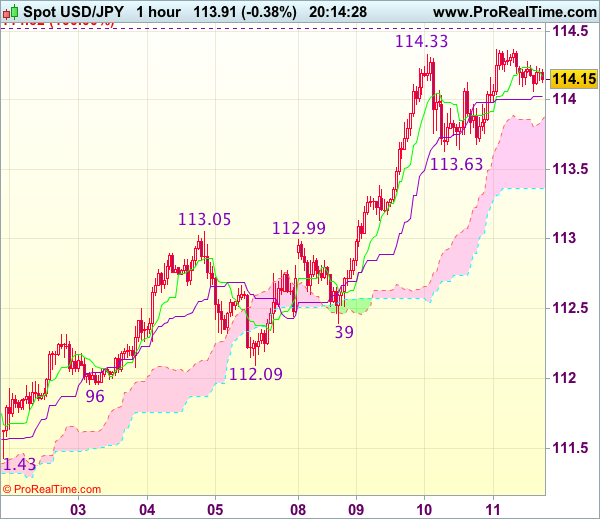

Trade Idea Update: USD/JPY – Buy at 113.40

USD/JPY - 113.92

Original strategy :

Buy at 113.40, Target: 114.45, Stop: 113.05

Position : -

Target : -

Stop : -

New strategy :

Buy at 113.40, Target: 114.45, Stop: 113.05

Position : -

Target : -

Stop : -

As the greenback has maintained a firm undertone after this week’s rally, suggesting recent upmove is still in progress and may extend further gain to 114.50-55 (100% projection of 108.13-111.78 measuring from 110.87), however, near term overbought condition should limit upside to 114.75-80 and price should falter below 115.00, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy dollar on pullback as 113.35-40 should contain downside. Only below previous resistance at 113.05 would defer and suggest top is formed, bring correction of recent upmove to 112.70-80 but reckon support at 112.39 would remain intact.

CAC Flat Ahead of French Nonfarm Payrolls, German GDP

The CAC is unchanged in the Thursday session, as the index is trading at 5,396.80. On the release front, there are no eurozone or French economic releases on the schedule. The EU released its Spring 2017 Economic Forecast, which presented a generally optimistic picture of the economies of eurozone members. In the US, PPI is expected to show a slight gain of 0.2%. On Friday, Germany releases Preliminary GDP. It will be a busy day in the US, which will publish retail sales and CPI reports.

The eurozone economy received a passing grade on Thursday, as the European Commission released its Spring 2017 Economic Forecast. The report noted that the European economy is in its fifth year of recovery, and forecast eurozone GDP growth of 1.7% in 2017 and 1.8% in 2018. On the inflation front, the report stated that inflation had risen in recent months, but this was mainly due to an increase in oil prices. Still, inflation was expected to reach 1.6% in 2017 and 1.3% in 2018, compared to just 0.2% in 2016. Stronger growth has led to lower unemployment, and the report projected that eurozone unemployment rate would drop to 9.4% in 2017 and 8.9% in 2018. The report reiterated what ECB president Mario Draghi has long been saying, namely, that risks to the eurozone economy remain tilted to the downside. These risks include US economic and trade policy under President Trump, the banking sector in Europe and the UK's exit from the EU. This forecast is considerably more optimistic than the Winter 2017 forecast, as is apparent from the captions in the press releases for these two reports: The Winter forecast was entitled "Navigating through choppy waters", while the caption for the Spring forecast reads "Steady growth ahead".

Anytime Mario Draghi is talking, the markets are all ears. The ECB president spoke about monetary policy before a Dutch parliamentary committee, but there was nothing new in his remarks. Draghi reiterated that the ECB continues to monitor growth and inflation levels, but has no plans at present to modify its monetary policy. Draghi said that that central bank would tighten its policy once the "tail risks" of a drop in inflation receded and growth improved. Currently, the ECB is making monthly purchases of EUR 60 billion under its asset-purchase scheme, which is scheduled to expire in December. Inflation levels were higher in the first quarter, which led to calls for Draghi to tighten policy. However, the ECB was reluctant to make any moves during the French election campaign, and this aversion could continue, with Germany holding elections in September. The central bank appears satisfied with the status quo, and can be expected to hold course, unless eurozone growth and inflation levels climb sharply.

Donald Trump has been embroiled in a number of controversies in his short presidency, but the political earthquake he has now stirred could become political quicksand for the new president. Trump abruptly fired FBI director James Comey on Tuesday, stunning lawmakers on both sides of the aisle in Congress. Comey, who has been conducting an investigation into possible collusion between Trump and Russia during the presidential campaign, clearly has been a thorn in Trump's side. The White House has claimed that it fired Comey over his handling of an email scandal involving Hillary Clinton, but the move has been roundly condemned by the Democrats, and some key Republicans have also voiced opposition as well. The firestorm could heat up further, with calls in Congress to appoint a special prosecutor into Trump's connections with Russia. Has Trump gone one step to far? This latest controversy could cause some jitters among investors and hurt the US dollar.

NZ Dollar Struggles after Reserve Bank of New Zealand Holds Rates

- NZ Dollar struggles after Reserve Bank of New Zealand holds rates

- Markets await Bank of England interest rate decisions

The New Zealand Dollar depreciated against its major counterparts after the Reserve Bank of New Zealand (RBNZ) held rates unchanged in May as widely expected. While that was priced in, recent positive economic news flow out of the nation has helped build interest rate hike expectations. In particular, the unemployment rate fell to 4.9% in the first quarter and Consumer Price Index (CPI) reached 2.2% year-on-year in the fourth quarter of 2016. The central bank practically dismissed those hopes, mentioning recent CPI gains as temporary. Central Bank Governor Wheeler stated that wages had not risen significantly and that he did not see inflationary pressures as being a concern. He stated that the RBNZ remains neutral and that interest rates should stay at current levels for the foreseeable future.

The Pound will be in focus this morning, with the release of the May quarterly inflation report and the Monetary Policy Committee's (MPC) policy decision. Analysts expect policy to remain unchanged, however, there is growing chatter that another member of the MPC may vote for a hike in rates. A 6-2 vote would not be a surprise, with Saunders expected to have joined Forbes in voting for a hike. Consumer Spending and Gross Domestic Product (GDP) data have been disappointing, however, recent Purchasing Managers' Index (PMI) data has been encouraging, helping Sterling along, which has been gently squeezing higher since the call for a snap election. If the Bank of England is remotely hawkish in the press conference, expect Sterling to continue its rise.

Later this afternoon, there is a smattering of US data, including Producer Price Index (PPI) and Jobless Claims, which are unlikely to be market moving. Attention will then turn to tomorrow's important retails sales data.

Films plots badly explained

Inception

A series of naps

Shrek

A guy learns to love a girl without her Instagram filters

The Martian

Billions of Dollars in subsidies for a potato farmer

Batman Versus Superman

Paranoid billionaire afraid of immigrant