Sample Category Title

CRUDE OIL – Vulnerable Short Term

CRUDE OIL - With the commodity remaining weak and vulnerable , more decline is expected in the days ahead. Though with caution. On the downside, support resides at the 48.00 level where a break will expose the 47.50 level. A cut through here will set the stage for a run at the 47.00 level. Further down, support resides at the 46.50 level. Its daily RSI is bearish and pointing lower supporting this view. On the upside, resistance resides at the 50.00 level. Further out, resistance comes in at the 50.50 level. A break above here will aim at the 51.00 level and then the 51.50 level followed by the 52.00 level. All in all, CRUDE OIL remains biased to the downside.

Aussie Rejected Off Resistance

Remember this set of Aussie resistance levels that we had been watching?

With this latest round of Aussie Dollar weakness, I wanted to feature one set of touches across both AUD/USD and AUD/CAD. Did you trade the level?

First up, we have the AUD/USD Daily:

AUD/USD Daily:

After stepping down following the textbook technical structure on the weekly, AUD/USD has bottomed out and found some serious resistance at the most recent higher time frame swing low.

Keep that chart open…

Next up, we come to AUD/CAD Daily:

AUD/CAD Daily:

Was AUD/CAD really ever going to break through that same level while AUD/USD was so far away from it?

The FOMC Provided Some Unexpected Impetus

The FOMC provided some unexpected impetus

A combination of improving US economic data and confident sounding Fed steering a steady path to a June rate hike has provided the market with some food for thought over night.

On the US economic front, the ISM Non-manufacturing index rebounded from 55.2 to 57.5 in April, beating consensus at 55.8 while the ADP printed 177k for April slightly above consensus inspiring the dollar bulls in early trade

AS the expected, the Feds delivered a rather benign statement and while acknowledging growth had slowed, but they recognised this as transitory, and labour trends were expected to strengthen further in 2017.

Japanese Yen

USDJPY continues to trade constructively despite lacking any spirited upside momentum.Overnight the pair was steadily bid on stronger US ISM print, but the improving employment trends comment in the FOMC statement provided the catalyst to push the pair to 112.75. Barring any unexpected shock, we should see the Greenback supported until Friday; then we should expect the markets to then move on the NFP report, especially the wage growth component. Also, the markets are keying on Fed speak later that day hoping that Yellen and Fischer will provide a more detailed policy forward guidance at that time.

Australian Dollar

Commodities are once again in the driving seat of the Australian Dollar indicating the signals generated by the sliding CRB Index of commonly traded commodities were sound in spite of all the questionable noise surrounding this week’s RBA event. Base metals laboured overnight, and after seeing Chinese and Australian equity indexes trading heavily, London walked in and hit the sell AUDUSD button.

But the Aussie dollar slide started early yesterday in part driven by an interest to sell AUDNZD after a bumper New Zealand Q1 jobs report and then was hammered mercilessly lower after a 6.5 % slide in iron ore with Copper down over 3 % and Gold technical floor giving way. The weaker China Manufacturing PMI print this week has stoked fears of China growth worries which is fueling further downside momentum for the entire commodity complex.

The AUDUSD remained offered leading up to the FOMC, and the convincingly hawkish tone from the FOMC did the Aussie bulls little favour, as there was renewed interest to sell Aussie late in the NY session.

If you trade the Aussie from the three C’s perspective ( Commodity, Carry, China) . with all three signals pointing lower for AUDUSD it more likely we will see a test of .7400 as opposed to a retracement to .7500 in the near term.

The convince break of the .7400 level will send the Aussie longs running for the exit and could add more fuel to the downside momentum

Euro

Continues to trade sideways ahead of the Key French vote on the weekend with dealers likely willing to fade either side of the moves through 1.0850-1.0950 as in all likelihood barring any surprises we’re likely going to straddle 1.0900 at weeks end. Getting some air time on market Chat rooms was Reuters latest survey of 65 strategists on EUR, while the general smorgasbord predictions were on offer for the plight of the EUR, one part of the study most are buying into is how to view the post-French election fall out. Most see a 1% gain on a (highly expected) Macron victory versus -5% loss on Le Pen. Reuters adds: “Analysts were split on what margin Macron needs to win by for their forecasts to hold, with the range varying from as little as five percentage points to more than 20%.”

EM Asia

The dollar bulls are holding court today with the FED’s convincingly steering the market to a June rate hike. Post-China Manufacturing PMI jitters continue to resonate while the slide in global commodity prices has weighed on regional sentiment overnight

Gold

For the ASX miner, the question now is how low gold can go? Gold could eventually move below $ 1200 on a combination of improving US economic data higher US interest rates and easing Geopolitical tensions. Near-term risks are skewed to Friday’s US employment report and Fedspeak. A positive outcome for the wage component in the NFP release and a confident sounding Yellen and Fischer will likely see XAU test 1225 level heading into the weekend

WTI

The DoE inventory report disappointed OIL bulls after the US Energy Information Administration (EIA) said weekly crude stocks fell by 930,000 barrels to 527.8 million. That was less than half the forecast draw of 2.3 million bpd. And WTI saw a knee-jerk reaction from $48.00 to $47.30 on results but has since recovered. But I think more importantly with commodities driving some G-10 currencies, the statement from Saudi oil ministers indicated that oil would be kept in a range from $45 – $55 per barrel and if usual trends remain intact that means the markets will have a greater propensity to test the base range resolve as opposed to the upside. So I would expect seller to remain dominant near-term

French Pre-Election Debate

The rancorous French pre-election TV debate had little influence on markets as 63 percent of viewers found Macron more convincing than Le Pen in the discussion, according to a snap opinion poll by Elabe for BFMTV. This supports the market’s view that Macron will win Sunday ballot. Clearly, Le Pen Europhobic stance is not winning any favours with the undecided vote.

USD/CAD Canadian Dollar Flat After Fed Holds Interest Rate

The Canadian dollar will end Wednesday trading nearly flat after having gained some traction early in the session only to give it back after the U.S. Federal Reserve kept rates unchanged in May. The American central bank kept the wording in their statement with a comment on the economic slowdown seen in the first quarter as transitory. While not necessarily dovish, it was very neutral on what policy makers intend to do next. The FOMC members voted unanimously to keep the benchmark rate in a 0.75 to 1 percent range. May was seen as a long shot given that Fed member comments have not put the market on alert ahead of a move unlike March and there was no press conference scheduled. June 14 is the next monetary policy meeting and expectations are high as the next rate hike depends on how transitory the current economic slowdown really is.

The drop in metal prices hit the Canadian stock market in a day with no local economic indicator releases. Tomorrow the publication of the trade balance at 8:30 am EDT with an improvement to the shock deficit last month. Later in the day Bank of Canada (BoC) Stephen Poloz will speak in Mexico City at the Canadian Chamber of Commerce. The Trump administration has put Canadian exports to the US in the spotlight ahead of a NAFTA renegotiation.

The USD/CAD lost 0.136 percent in the last 24 hours. The pair is trading at 1.3699 after the U.S. Federal Reserve kept rates unchanged and the loonie appreciated slightly ahead of Friday’s employment data in both nations. The Canadian currency has been caught in a perfect storm as oil prices have retreated, the economy has failed to regain traction and to make matters worse its biggest trading partner is threatening to tear up the pact that it depends on.

Housing market worries continue to gain traction as troubled mortgage lender Home Trust Capital’s liquidity issues put the real estate bubble to the forefront. The Bank of Canada (BoC) has issued multiple warnings about the housing bubble, but without hiking rates Canadians are going deeper into depth and keep boosting speculative prices even higher. The central bank was proactive in 2015, but is now very hands off as the government’s initiatives have been insufficient in the current macro climate.

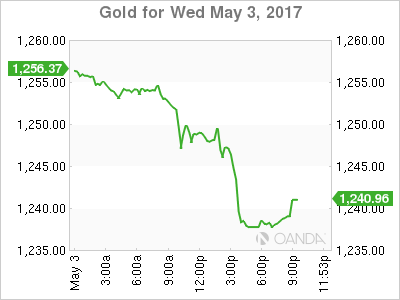

Gold lost 1.417 percent on Wednesday. The price of the yellow metal is trading at $1,239.20. Gold has lost near 2.4 percent in the last week and is now trading near monthly lows. The U.S. Federal Reserve acted as expected at the end of the May Federal Open Market Committee (FOMC) meeting and held rates, but kept a June rate hike on the table putting downward pressure on gold. The US avoided a government shutdown reducing political risk in the US reducing investor appetite in the metal as a safe haven.

Market events to watch this week:

Wednesday, May 3

4:30am GBP Construction PMI

8:15am USD ADP Non-Farm Employment Change

10:00am USD ISM Non-Manufacturing PMI

10:30am USD Crude Oil Inventories

2:00pm USD FOMC Statement

USD Federal Funds Rate

9:30pm AUD Trade Balance

11:10pm AUD RBA Gov Lowe Speaks

Thursday, May 4

4:30am GBP Services PMI

8:30am CAD Trade Balance

USD Unemployment Claims

4:25pm CAD BOC Gov Poloz Speaks

9:30pm AUD RBA Monetary Policy Statement

11:00pm NZD Inflation Expectations q/q

Friday. May 5

8:30am CAD Employment Change

8:30am USD Average Hourly Earnings m/m

8:30am USD Non-Farm Employment Change

Fed Brushes Off Q1

The Fed brushed off a weak first quarter and that was seen as a signal that Yellen still intends to hike in June. The US dollar led the way while the Australian dollar lagged to a 3-month low. Australian trade balance and comments from Lowe are out next. The Premium long in GBPJPY was closed with a 205-pip gain as a tactical positioning trade ahead of the Fed and the French elections. 7 trades remain progress.

The Fed didn't offer anything new in the way of guidance in Wednesday's statement. The same 'gradual' language remained without committing to a timeline. But that's not how the market took it. The probability of a June hike rose to 93% from 70% after the statement. What the market latched onto was a line saying that the slowdown in Q1 growth was likely to be transitory. The assumption is that the Fed is brushing it off and still wants to hike in June. That may turn out to be true but not if data continues to miss. At 93%, it doesn't leave much room for error.

On the data front – at least on the soft data front – the Fed got some good news. The April ISM non-manufacturing index was at 57.5 vs 55.8 expected. In addition, the new orders component was at the best level in 11 years, jumping to 63.2 from 58.9. That will help convince the Fed that good growth is still right around the corner.

The other main release was ADP employment at 177K compared to 175K expected.

In the bigger picture, we're increasingly convinced that jobs growth and unemployment rates are nearly irrelevant to trading. Yesterday's New Zealand jobs numbers were extremely strong with unemployment falling to 4.9% from 5.2% a great jobs growth overall. The kiwi initially jumped 30 pips but was sold heavily for the remainder of the day in large part because wage growth was disappointing. Expect the market to have the same focus on wages in Friday's non-farm payrolls report.

The principal question is: Can a tight labour market still producer wage growth in a world of offshoring and automation?

The kiwi fell alongside AUD/USD which wiped out three days of gains and fell to the lowest since mid-January. Up next is the 0130 GMT trade balance report; it's expected to show a $A3.25m surplus.

The bigger potential market mover comes at 0310 GMT when Governor Lowe speaks on household debt, housing prices and resilience. That topic sounds ripe for hawkish comments but even if that's the case he will want to jawbone AUD lower at the same time.

Fed Holds Rates Steady; Views Q1 Slowdown as Transitory

Our Take:

Today's policy statement managed a fairly balanced tone considering a number of soft data releases in recent weeks: most significantly a slowdown in Q1 GDP growth, but also weaker-than-expected payroll and inflation readings for March. The Fed explicitly noted that slower Q1 activity is "likely to be transitory" and that growth should return to a moderate pace even as monetary policy stimulus continues to be gradually pared back. It sounds like their take on Q1 growth was similar to ours: a slowdown in consumer spending appears anomalous given solid fundamentals, while other details were a bit more encouraging, including a pickup in business fixed investment. The statement made little mention of March's disappointing payroll figure, simply noting that recent job gains have been solid on average and that the unemployment rate declined. The Committee did, however, make note of softer core inflation in March, though we would add that about half of the dip in core PCE and CPI inflation reflected lower prices for mobile phone services (something policymakers would be expected to look through). Nonetheless, it is fair to say that underlying inflation remains slightly below the Fed's 2% objective.

Aside from tweaks to the economic assessment, there were no notable changes in today's policy statement. The Committee reiterated their expectation that economic conditions will warrant a gradual removal of accommodation but gave no overt signal on the timing of the next hike. Our forecast assumes the next move will be in June; while we are encouraged by indications the Fed will look past the Q1 slowdown, we think the Committee will want to see evidence of a pickup in economic activity before continuing their tightening cycle. Data releases over the next six weeks supporting our call for GDP growth to rebound to 2.9% in Q2 would help firm up expectations for a hike at the June 13-14 meeting.

Dollar Mildly Higher as Fed Talks Down Q1 Weakness

Dollar strengthens against most major currencies after FOMC left interest rate unchanged at 0.75-1.00% as widely expected. Most importantly, Fed dismissed the weakness in Q1 and noted in the accompanying statement that "slowing in growth during the first quarter as likely to be transitory". Fed maintained that "with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace". Meanwhile Fed also noted that " labor market has continued to strengthen even as growth in economic activity slowed". And, "job gains were solid, on average, in recent months, and the unemployment rate declined." "Labor market conditions will strengthen somewhat further, and inflation will stabilize around 2 percent over the medium term." And, risks are "roughly balanced". While there is no hint about the timing of the next hike, the statement does nothing to change the expectation of a hike in June.

In response to the announcement, USD/JPY extends recent rally to as high as 112.65 and is still on course for next resistance at 115.49. USD/CHF stages a strong rebound after breaching 0.9893 low briefly. AUD/USD took out 0.7439 support to resume recent decline from 0.7748 and is on course for a test on 0.7158 support. USD/CAD is firm in tight range and more upside is expected with 1.3649 minor support intact. Nonetheless, while the greenback strengthens against Euro and Sterling, EUR/USD and GBP/USD are just kept in very tight range. In other markets, DJIA recovers mildly after trading in red in initial part of the session. Meanwhile, NASDAQ and S&P too are trading slightly down. 10 year yield trading up mildly but struggles to gain momentum above 2.3 handle. Gold extends recent decline and took out 1250 handle. WTI crude oil is trying to find support above 47 handle.

Thanks to the resilience in Euro, Dollar index continues to hover in tight range around 99 handle even though it recovers mildly after FOMC. We maintain the view that corrective pattern from 103.83 is still in progress. And such pattern is likely a triangle. There is prospect of another dip but there should be strong support above 50% retracement of 91.91 to 103.82 at 97.86 to bring rebound.

Fed to Seek Confirmation from the Data Before Telegraphing Near-Term Hike

As widely expected, the Federal Open Market Committee (FOMC) left the target range for the federal funds rate unchanged at between 3/4 and 1 percent.

The Committee was fairly upbeat indicating that the labor market "continued to strengthen" with job gains solid "on average" and unemployment having declined, even as growth in economic activity "slowed."

The statement highlighted consumer spending "rose only modestly" but indicated that the Committee believes that "fundamentals underpinning … consumption remained solid." Moreover, the Committee viewed business investment as having "firmed," dropping the "somewhat" qualifier used in the March statement.

Inflation was viewed as "running close to the … longer-run objective," while the core measure was flagged as having "declined in March" and running "somewhat below 2 percent."

The decision was unanimous, with Kashkari (FRB Minneapolis) voting alongside the remaining Committee members given the status-quo decision.

Key Implications

This was largely a status-quo statement that highlighted the continued labor market improvement, while seeing through the deceleration in economic activity during the first-quarter. This was expected and is reasonable given the transitory effects which slowed growth during the quarter, including the inventory cycle and the warmer weather. In particular, the slowdown in consumption was played down, with an acceleration expected given solid supporting fundamentals.

The weak March inflation numbers were also highlighted, suggesting the slowdown in the metric was not taken lightly, particularly in light of low measures of inflation compensation. Still, the monthly pullback is unlikely to sway the Fed unless the weakness persists, something that we don't anticipate.

At this point, we expect the Fed to be in wait-and-see mode in the coming weeks, as second quarter data begins to trickle in. Should figures over the coming weeks confirm a rebound in consumer spending and inflation, we expect the Fed raise rates in June. Still, this is far from a done deal, and potential weakness could delay any hike further into the year.

(FED) FOMC Statement Release Date: May 03, 2017

Information received since the Federal Open Market Committee met in March indicates that the labor market has continued to strengthen even as growth in economic activity slowed. Job gains were solid, on average, in recent months, and the unemployment rate declined. Household spending rose only modestly, but the fundamentals underpinning the continued growth of consumption remained solid. Business fixed investment firmed. Inflation measured on a 12-month basis recently has been running close to the Committee's 2 percent longer-run objective. Excluding energy and food, consumer prices declined in March and inflation continued to run somewhat below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee views the slowing in growth during the first quarter as likely to be transitory and continues to expect that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace, labor market conditions will strengthen somewhat further, and inflation will stabilize around 2 percent over the medium term. Near-term risks to the economic outlook appear roughly balanced. The Committee continues to closely monitor inflation indicators and global economic and financial developments.

In view of realized and expected labor market conditions and inflation, the Committee decided to maintain the target range for the federal funds rate at 3/4 to 1 percent. The stance of monetary policy remains accommodative, thereby supporting some further strengthening in labor market conditions and a sustained return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. The Committee will carefully monitor actual and expected inflation developments relative to its symmetric inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipates doing so until normalization of the level of the federal funds rate is well under way. This policy, by keeping the Committee's holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Charles L. Evans; Stanley Fischer; Patrick Harker; Robert S. Kaplan; Neel Kashkari; and Jerome H. Powell.

Gold Dips as Markets Await Fed Rate Statement

Gold has posted losses in the Wednesday session. In North American trade, spot gold is trading at $1247.86 an ounce. On the release front, ADP Nonfarm Payrolls dropped to 177 thousand, very close to the forecast of 178 thousand. The ISM Non-Manufacturing PMI improved to 57.5, beating the estimate of 56.1 points. Today's key event is the Federal Reserve's policy statement, with no change expected in the benchmark interest rate.

All eyes are on the Federal Reserve, which holds its monthly policy meeting later on Wednesday. A rate hike is extremely unlikely this time around, with the CME Group pricing in a hike at just 5%. This means that the markets will be focusing on the rate statement and the views of policymakers concerning economic conditions. The Fed has two key goals which have been achieved, namely full employment and an inflation rate of 2%. One area of concern which policymakers have circled is the Fed's balance sheet, which stands at $4.5 trillion. The minutes of the March meeting stated that policymakers want to start reducing this figure before the end of 2017, so the markets will be looking for another reference to the balance sheet in the rate statement or the minutes of the meeting. The markets are fairly confident that the Fed will press the rate trigger in June, as the odds for a hike have improved to 63%. If the rate statement is more hawkish than expected, we could see these odds increase.