Sample Category Title

European Open Briefing: The Federal Reserve Kept Rates Unchanged

Global Markets:

- Asian stock markets: Shanghai Composite down 0.10 %, Hang Seng fell 0.40 %, ASX 200 lost 0.50 %, Nikkei closed for holiday

- Commodities: Gold at $1241 (-0.60 %), Silver at $16.65 (+0.60 %), WTI Oil at $47.70 (-0.20 %), Brent Oil at $50.70 (-0.20 %)

- Rates: US 10-year yield at 2.32, UK 10-year yield at 1.08, German 10-year yield at 0.34

News & Data

- Australia Trade Balance (AUD) Mar: 3107M (exp 3250M; prev 3574M)

- Australia Exports (MoM) Mar: 2.0% (prev 1.0%)

- Australia Imports (MoM) Mar: 5.0% (prev -5.0%)

- Australia HIA New Home Sales (MoM) Mar: -1.1% (prev 0.2%)

- New Zealand ANZ Job Advertisements (MoM) Apr: 2.8% (prev 1.6%; prev rev 2.0%)

- New Zealand ANZ Commodity Price Index (MoM) Apr: -0.2% (prev 0.4%)

- South Korea BoP Current Account Balance (USD) Mar: 5931.8M (prev 8400.2M)

- PBoC Fixes USDCNY Reference Rate At 6.8957 (prev fix 6.8892 prev close 6.8985)

- Asian stocks retreat, dollar holds near six-week high on hawkish Fed – RTRS

- Fed holds interest rates steady, downplays economic weakness – RTRS

Markets Update:

The Federal Reserve kept rates unchanged, as expected. However, the statement was perceived as more hawkish than expected, as the central bank downplayed weakness in the first-quarter economic growth. This is a hint that a rate hike in June seems quite likely.

The Dollar appreciated post-FOMC, especially against the emerging market currencies. Amongst the major pairs, the commodity currencies felt most of the pressure. AUD/USD fell from 0.7470 to a low of 0.74 in Asia. Further losses to at least 0.73 seem likely in the near-term. Similar price action was seen in NZD/USD, which reversed at 0.6970 yesterday and fell to a low of 0.6870 after the FOMC.

The reaction in EUR and GBP was rather mild. EUR/USD only declined to 1.0880, and then continued with its consolidation. Meanwhile, USD/JPY caught up on momentum. The pair rallied to 112.90 in Asia. A clear break above 113 would suggest that a rally towards 115 could follow.

Upcoming Events:

- 08:45 BST – Italian Services PMI

- 08:50 BST – French Services PMI

- 08:55 BST – German Services PMI

- 09:00 BST – Euro Zone Services PMI

- 09:30 BST – UK Services PMI

- 10:00 BST – Euro Zone Retail Sales

- 13:30 BST – US Trade Balance

- 13:30 BST – Canadian Trade Balance

- 15:00 BST – US Factory Orders

- 17:30 BST – ECB President Draghi speaks

- 21:25 BST – BoC Governor Poloz speaks

Australia’s Trade Surplus Sharply Narrowed In March

For the 24 hours to 23:00 GMT, the AUD declined 1.49% against the USD and closed at 0.7426.

LME Copper prices declined 1.9% or $110.0/MT to $5636.5/MT. Aluminium prices rose 0.4% or $7.0/MT to $1916.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7411, with the AUD trading 0.2% lower against the USD from yesterday's close.

Earlier today, data showed that Australia's seasonally adjusted trade surplus narrowed more-than-expected to a level of A$3107.0 million in March, following a revised surplus of A$3657.0 million in the previous month, while market participants had envisaged for a surplus of A$3250.0 million. Further, the nation's HIA new home sales dropped 1.1% on a monthly basis in March. In the prior month, new home sales had recorded a rise of 0.2%.

Meanwhile, the Reserve Bank of Australia's (RBA) Governor, Philip Lowe, stated that surging household debt levels has led the economy in a weaker position to deal with shocks.

Elsewhere, in China, Australia's largest trading partner, the Caixin/Markit services PMI fell to a level of 51.5 in April, expanding at its weakest pace in eleven months, thus casting fresh doubts over the health of the nation's economy. The PMI had registered a reading of 52.2 in the previous month.

The pair is expected to find support at 0.7368, and a fall through could take it to the next support level of 0.7325. The pair is expected to find its first resistance at 0.7489, and a rise through could take it to the next resistance level of 0.7567.

Moving ahead, traders will keep a close watch on the RBA's recent meeting statement coupled with Australia's AiG performance of construction index for April, due to release overnight.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Economy Continued To Grow In The First Quarter Of 2017

For the 24 hours to 23:00 GMT, the EUR declined 0.38% against the USD and closed at 1.0888.

On the economic front, the Euro-zone's seasonally adjusted flash gross domestic product (GDP) rose 0.5% on a quarterly basis in the first quarter of 2017, meeting market expectations, thus supporting the notion that the economy is getting back on track again. In the prior quarter, GDP had climbed by a revised 0.5%.

Elsewhere, in Germany, the seasonally adjusted unemployment rate remained steady at 5.8% in April, in line with market expectations.

The greenback traded higher against a basket of currencies after the US Federal Reserve (Fed) left the door open for a June interest rate hike.

The Fed, at its latest monetary policy meeting, opted to leave key interest rate unchanged in a range from 0.75% to 1.0%. In the statement accompanying the decision, the Fed played down weak first-quarter economic growth in US, stating that the recent slowdown was “likely to be transitory” and emphasised the strength of the nation's labour market and consumer spending. Moreover, the central bank characterised inflation as “running close to the central bank's 2.0% target.”

Earlier in the session, the greenback strengthened against its major counterparts, on the back of upbeat US economic data.

The US ISM non-manufacturing PMI advanced more-than-anticipated to a level of 57.5 in April, compared to market consensus for a rise to a level of 55.8 and following a level of 55.2 in the previous month. Also, the nation's final Markit services PMI unexpectedly climbed to a level of 53.1 in April, after recording a drop to a level of 52.5 in the preliminary print and compared to a reading of 52.8 in the previous month.

Other economic data showed that the US private sector employment increased by 177.0K in April, surpassing market expectations of an advance of 175.0K. However, it was the smallest gain since October 2016. The private sector employment had registered a revised gain of 255.0K in the previous month. In contrast, the nation's MBA mortgage applications eased 0.1% in the week ended 28 April 2017. Mortgage applications had risen 2.7% in the prior week.

In the Asian session, at GMT0300, the pair is trading at 1.0891, with the EUR trading slightly higher against the USD from yesterday's close.

The pair is expected to find support at 1.0868, and a fall through could take it to the next support level of 1.0846. The pair is expected to find its first resistance at 1.0924, and a rise through could take it to the next resistance level of 1.0958.

Moving ahead, investors will closely monitor the final print of Markit services PMI for April across the Euro-zone along with the Euro-zone's retail sales data for March, slated to release in a few hours. A speech by the ECB President, due later in the day, will also be eyed by traders. Additionally, the US trade balance, final durable goods orders and factory orders, all for March, set to release later today, will garner significant amount of market attention.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

UK’s Construction Sector Growth Surprisingly Hits 4-Month High In April

For the 24 hours to 23:00 GMT, the GBP declined 0.53% against the USD and closed at 1.2868.

Macroeconomic data indicated that activity in Britain's construction sector unexpectedly advanced to a level of 53.1 in April, hitting its highest level in four-months, suggesting that the economy might be recovering a bit, after showing a lacklustre performance at the start of 2017. Market participants anticipated the PMI to drop to a level of 52.0, compared to a level of 52.2 in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.2876, with the GBP trading 0.06% higher against the USD from yesterday's close.

The pair is expected to find support at 1.2841, and a fall through could take it to the next support level of 1.2806. The pair is expected to find its first resistance at 1.2929, and a rise through could take it to the next resistance level of 1.2982.

Looking ahead, investors will concentrate on UK's Markit services PMI for April accompanied with net consumer credit and mortgage approvals, both for March, slated to release in a few hours.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the USD rose 0.63% against the JPY and closed at 112.68.

In the Asian session, at GMT0300, the pair is trading at 112.77, with the USD trading 0.08% higher against the JPY from yesterday’s close.

The pair is expected to find support at 112.19, and a fall through could take it to the next support level of 111.61. The pair is expected to find its first resistance at 113.12, and a rise through could take it to the next resistance level of 113.47.

Amid a holiday on account of Greenery day in Japan today, trading trend in the JPY is expected to be determined by global macroeconomic factors.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading Marginally Lower, Ahead Of Swiss SECO Consumer Confidence Data

For the 24 hours to 23:00 GMT, the USD rose 0.29% against the CHF and closed at 0.9942.

In the Asian session, at GMT0300, the pair is trading at 0.9944, with the USD trading slightly higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9905, and a fall through could take it to the next support level of 0.9866. The pair is expected to find its first resistance at 0.9966, and a rise through could take it to the next resistance level of 0.9988.

Going ahead, Switzerland’s SECO consumer confidence index for April, due to release in a while, will be on investors’ radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Loonie Trading Higher In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.18% against the CAD and closed at 1.3729.

In the Asian session, at GMT0300, the pair is trading at 1.3721, with the USD trading 0.06% lower against the CAD from yesterday’s close.

The pair is expected to find support at 1.3685, and a fall through could take it to the next support level of 1.365. The pair is expected to find its first resistance at 1.3748, and a rise through could take it to the next resistance level of 1.3776.

Ahead in the day, traders will look forward to Canada’s international merchandise trade balance data for March.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD, GOLD, WTI CRUDE, DJIA, FTSE100, DAX

EUR/USD

The EUR/USD pair ended the day again around 1.0900 after one of the most uneventful Fed's monetary policy meeting. The Central Bank left rates unchanged, while acknowledging weakness during the first quarter, but seeing it as 'transitory'. The accompanying statement didn't provide much clues on what or when the Fed will move next, while maintaining the overall positive outlook of the local economy.

In the macroeconomic front, news were soft in Europe, as the preliminary Q1 GDP reading came in as expected at 0.5%, but the producer price index fell by 0.3% in March, against previous 0.0% and worse than the -0.1% expected. In the US however, the ADP employment survey showed that the private sector added 177,000 new jobs in April, in line with market's forecast. Also in the US, the private sector grew at a strong pace according to the official and Markit services PMIs, both surpassing previous months' readings and expectations.

With the Fed out of the picture, market's attention now shifts to the French presidential debate between Marine Le Pen and Emmanuel Macron. The televised debate is expected to last over two hours, and take place after the Asian opening. With latest polls showing centrist candidate Macron taking the lead, there is a good chance that if he stands victorious, the EUR will likely keep on rallying on relief.

From a technical point of view, the pair retains a neutral stance, given that in the 4 hours chart, the price continues hovering around a directionless 20 SMA, whilst technical indicators head nowhere within neutral territory. The pair needs to clearly break either above 1.0950, or below 1.0820, to gather some directional momentum that could persist into the following sessions.

Support levels: 1.0855 1.0820 1.0785

Resistance levels: 1.0950 1.1000 1.1045

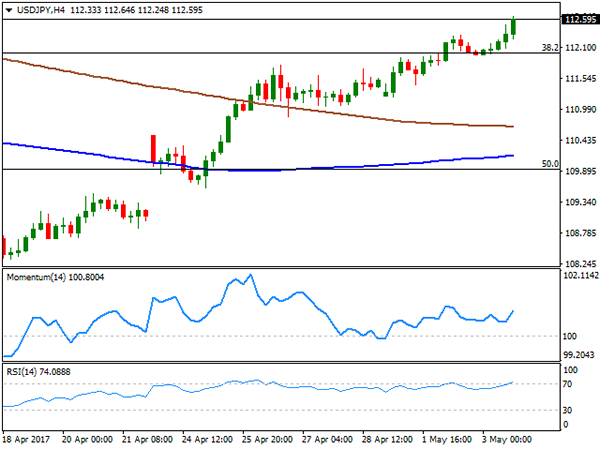

USD/JPY

The USD/JPY pair advanced up to 112.64, its highest since March 21st, and settled a few pips below the level, backed by strong US data released earlier on the day and a modest recovery in US Treasury yields. A firm ADP survey, in line with market's expectations, and steady growth in the services sector in the US, kept the pair firm above the 112.00 level at the beginning of the day, while after trading softly for most of session, yields advance following Fed's announcement, with the 10-year benchmark regaining the 2.30% threshold. The pair's advance stalled around 112.60, where it has the 100 DMA. The price has been developing below the indicator ever since mid March, and a firmer recovery above it will likely anticipate a steeper recovery during the upcoming sessions. Short term, the 4 hour chart shows that the RSI indicator holds around 74, while the Momentum indicator also heads north well above its mid-line. Additionally, the 100 SMA keeps advancing below the 200 SMA, both far below the current level.

Support levels: 112.45 112.00 111.60

Resistance levels: 112.90 113.30 113.80

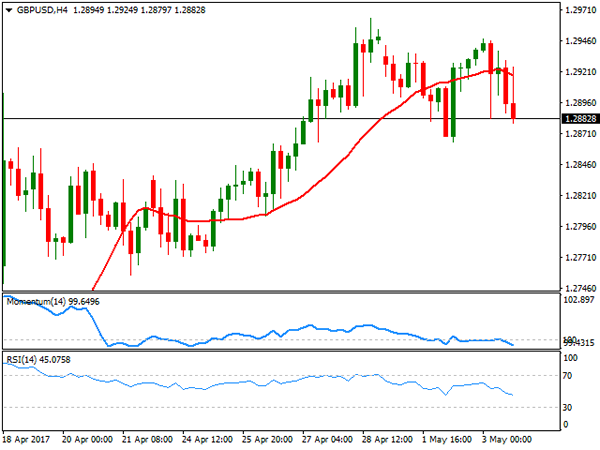

GBP/USD

The GBP/USD pair trimmed all of its Tuesday gains and closed the day around its low of 1.2879, as the greenback advanced marginally following the Fed's monetary policy announcement. In fact, the US Central Bank offered little to work with, as it kept rates, and the economic outlook unchanged, without hinting next moves. The Pound traded as high as 1.2947 early London, as the UK Markit Construction PMI reached 53.1 in April, from 52.2 in March. The reading came after strong manufacturing index earlier on the week, and ahead of the Services PMI to be released this Thursday. From a technical point of view, and despite still within a well limited range the GBP/USD upward momentum seems to be fading, as in the daily chart, technical indicators are retreating from overbought territory, heading modestly lower at two-week lows. In the shorter term, and according to the 4 hours chart the pair is biased lower, declining below a flat 20 SMA that offers a dynamic resistance around 1.2930, while technical indicators accelerate south within bearish territory, also at fresh 2-week lows.

Support levels: 1.2880 1.2830 1.2795

Resistance levels: 1.2965 1.3010 1.3060

GOLD

Spot gold settled at $1,245.50 a troy ounce, its lowest settlement since late March, after the US Federal Reserve's monetary policy statement suggested that policymakers are still confident over the economic recovery, and therefore fueling speculation that the year will bring two more rate hikes. Odds for a June move rose slightly above 70% after the statement that anyway provided no clear clues. From a technical point of view, the commodity retains the negative tone seen on previous updates, with the price accelerating further below a now horizontal 20 SMA, and the RSI indicator heading sharply lower around 39. In the same chart, the 100 and 200 SMAs, converge around 1,234.60, providing a critical dynamic support, as a break below it will probably trigger additional slides. In the shorter term, and according to the 4 hours chart, the 20 SMA heads sharply lower above the current level and after breaking below the 100 and 200 SMAs, whilst technical indicators maintain their sharp bearish slopes, despite being in oversold territory, in line with the longer term perspective.

Support levels: 1,242.50 1,234.60 1,226.90

Resistance levels: 1,249.80 1,260.00 1,272.05

WTI CRUDE OIL

Crude oil prices extended their weekly decline, with West Texas Intermediate crude futures settling around $47.70 a barrel, undermined by dollar's broad strength and a disappointing EIA report, as US stockpiles declined by less than expected. According to the Energy Information Administration, crude stocks fell by 930,000 barrels in the week ended April 28, below market's expectations of a 2.9 million decline. Earlier on the day, the commodity attempted to advance, as the API report released late Tuesday showed a sharp drop in US oil and gasoline stocks, but WTI was unable to recover the 48.00 level. The daily chart for US oil continues supporting additional slides ahead, as the price is further below its moving averages, as technical indicators enter oversold territory. In the 4 hours chart, the price is further below a bearish 20 SMA, this last providing a dynamic resistance at 48.50, while technical indicators hold within bearish territory, with no clear directional strength.

Support levels: 47.10 46.60 46.00

Resistance levels: 47.90 48.50 49.20

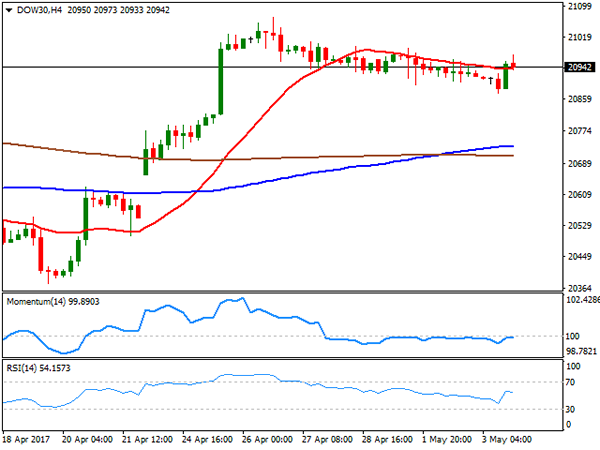

DJIA

US indexes trimmed most of its intraday losses after a confident Fed, with major indexes closing mixed, not far from their daily opening levels. The Dow Jones Industrial Average managed to settle 8 points higher at 20,957.90, while the Nasdaq and the S&P closed lower, with the first shedding 22 points, to 6,072.55 and the second down 0.13% to 2,388.13. Within the Dow, Merck was the best performer, ending the day up 1.48%, followed by Chevron that gained 1.29%. Disney led decliners, shedding 2.43%, while El du Pont closed 1.18% lower. The benchmark kept trading within a narrow intraday range, unable to establish a clear direction. In the daily chart, the index holds well above its moving averages, while the RSI indicator hovers around 61, as the Momentum indicator eases within positive territory, rather as a consequence of the absence of directional strength that a sign of upcoming weakness. In the 4 hours chart, the index settled a few points above its 20 SMA, but technical indicators have returned to their usual neutral stance after a short-lived intraday slide.

Support levels: 20,913 20,869 20,819

Resistance levels: 20,989 21,035 21,071

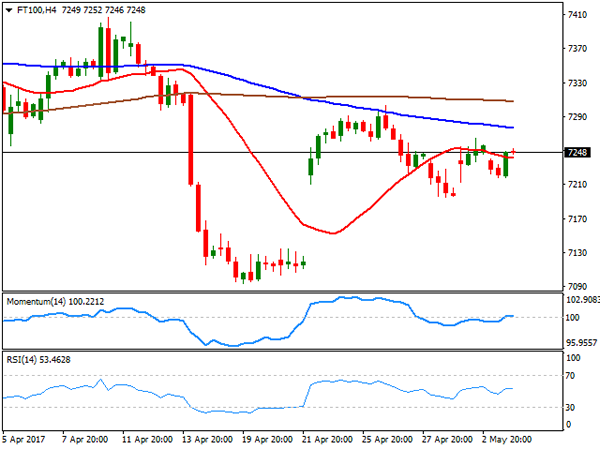

FTSE100

The FTSE 100 closed the day at 7,234.53, down 15 points, hit by lower metals prices that kept mining-related equities in the red. Sainsbury led decliners, plunging 5.72% after reporting a 0.6% fall in full-year like-for-line sales, and cutting dividends by 16%. Among the worst performers were also Glencore, down 3.71%, and Anglo American that shed 3.20%. Only 39 members managed to close in the green, with Sage Group being the best performer, up 3.44%. Mounting Brexit concerns, on market rumors suggesting the EU will demand up to €100bn in payments from the UK, also weighed on investors' mood. The index recovered some ground in after-hours trading, but the daily chart shows that it holds below a bearish 20 SMA, whilst technical indicators hold flat within negative territory, maintaining the risk towards the downside. In the 4 hours chart, the index hovers around a modestly bearish 20 SMA while technical indicators have also turned flat around their mid-lines, limiting chances of a stronger advance.

Support levels:7,215 7,173 7,126

Resistance levels: 7,264 7,303 7,340

DAX

Major European benchmarks closed generally lower, although the German DAX managed to advance 20 points to 12,527.84, backed on strong local employment data. Fresenius lead advancers, adding 2.42%, while banks also made it to the top ten list, with Commerzbank adding 1.42% ad Deutsche Bank 1.18%. E.ON was the worst performer, down 1.62%, followed by Volkswagen that shed 0.94%, with most auto-makers closing in the red after disappointing April auto sales in the US. The index holds near fresh multi-month highs ahead of the Asian opening, retaining the bullish bias in the daily chart, as technical indicators advanced within positive territory as the benchmark keeps developing above all of is moving averages. In the 4 hours chart, the technical outlook is neutral-to-bullish, as the index held above its 20 SMA that anyway remains flat, whilst the Momentum indicators hovers around its 100 level, but the RSI indicator resumed its advance, heading north around 69.

Support levels: 12,495 12,440 12,391

Resistance levels: 12,537 12,580 12,625

FOMC Sent Important Rate Hike Hint In An Apparently-Uneventful Meeting

As widely anticipated, the FOMC left the target range for the Fed funds rate unchanged at between 0.75- 1%. Although the accompanying statement was largely unchanged from the previous month, the implications were important in light of the slowdown in the first quarter. While acknowledging the recent weakness in growth and inflation, policymakers attributed it to 'transitory effects'. The downplaying of 1Q17's disappointments underpinned the Fed's determination to carry on its normalization plan. The FOMC maintained its economic outlook and the gradual rate-hike approach. We continue to expect two more rate hikes this year with one coming in June.

It is undeniable that US macroeconomic indicators surprised to the downside in 1Q17: GDP expanded at a modest +0.7%, core CPI fell -20 bps to 1.6% y/y since the previous meeting, while consumer spending rose only modestly. The FOMC acknowledged all these weaknesses. As suggested in the statement, the central bank noted that 'growth in economic activity slowed' during the intermeeting period. Yet, it pointed out that 'the labor market has continued to strengthen', 'job gains were solid, on average, in recent months, and the unemployment rate declined'. It acknowledged that 'household spending rose only modestly, but the fundamentals underpinning the continued growth of consumption remained solid'. The statement affirmed that 'the slowing in growth during the first quarter as likely to be transitory'. Yet, policymakers used a less strong tone in stressing that the inflation weakness was transitory. As noted in the statement, the Fed indicated that 'excluding energy and food, consumer prices decline in March and inflation continued to run somewhat below 2%'. The Fed continued to guide that monetary accommodation should support 'a sustained return to 2% inflation'. Overall, near-term risks to the economic outlook appeared 'roughly balanced' and the members would continue to 'closely monitor inflation indicators and global economic and financial developments'.

The approach of the Fed's rate hike schedule would remain 'gradual adjustments' and 'gradual increases'. Guidance on the reinvestment policy stayed unchanged with the FOMC reiterating that the reinvestment would continue 'until normalization of the level of the Fed funds rate is well under way'. Despite heightening speculations that the Fed would begin unwinding its balance sheet (worth of US$ 4.5 trillion) later this year, the Fed refrained from offering any hints on this issue. The Fed's stance to looking through the soft data in the first quarter signals its inclination to hike rate in June. Certainly, any action would be data-dependent but the bar seems to be high for the Fed to decide not raise the policy rate in the coming month. Explicit guidance of the balance sheet normalization would unlikely come unless the members have reached a consensus on the scaling-back of redemptions and the balance on the mix of Treasury securities and MBS in its portfolio.

Market Morning Briefing: The Fed Kept The Rates Unchanged

STOCKS

The stock markets are al stable and no fresh impact is seen after the FOMC yesterday as it kept rates unchanged and reiterated its maintenance of the existing policy.

Dow (20957.90, +0.04%) is finding some difficulty to move above 20980 just now. The index could possibly test levels near 20800 before bouncing back towards 21000-21200 in the medium term. Note important resistances seen near 21200 and 21400 respectively.

Dax (12527.84, +0.16%) is slowly inching up towards 12550-12600 levels from where a short dip could be possible. The channel on the daily charts are holding well for now.

Shanghai (3126.44, -0.28%) lacks the upward momentum required to take it above 3160 and while trading below, it could test 3100 or even lower in the coming sessions. But note important channel support on the 3-day charts which of holds could lead to a sharp rise in the longer run.

Nifty (9311.95, -1.85%) could spend the rest of the week in the 9300-9400 levels and a fresh move could be expected next week. Note 9400 is an important resistance and is expected to hold in the medium term.

COMMODITIES

Bullion had moved lower due to recent strength in Dollar Index and trading near their key support areas. Gold (1241) is hovering around its crucial support of 1239. We might see some corrective bounce towards 1260 due to short term oversold condition. A close below 1235 could open up 1220 and 1200 as well.

Silver (16.43) is highly Oversold on the near-term charts and trading within the range of 15.73-16.94.The bias will remain bearish while it is trading below 17.50 levels.

Copper (2.52) had failed to close above 2.62 levels and came down in line with our expectation. Current trading range could be 2.45-2.54. There are supports at current levels of 2.50-52 which may hold for few days but a close below that could open up 2.45 levels as well.

Brent (51.73) and WTI (47.70) both had moved lower in line with our expectation. They are within their trading ranges of 50 -52. and 46.20 – 48.80 respectively. Brent may consolidate within these levels for few more sessions though the possibility of a corrective bounce towards resistance can't be ruled out. We will remain bearish while Brent and WTI are trading below 53 and 51 levels respectively.

FOREX

The Fed kept the rates unchanged and shrugged off the poor first quarter weakness in US (0.7% annualized). The June rate hike odds have jumped from 70% to 90%, strengthening the Dollar in the process.

Boosted by the continued Fed confidence in the economy, Dollar Index (99.32) has rallied to test our resistance area of 99.35-50 but yet to rise above it to confirm the near term reversal. It's a tough and go situation right now for Dollar and a similar situation is seen for Dollar Yen (112.80) which is trading close to the immediate resistance of 112.90-113.00. The pair is already enjoying the longest rally in 2017 from 108.10 to the current swing high of 112.89 and it should be clear in a day or two if the rally is to continue or reverse to the downside.

Euro (1.0892) has corrected a bit due to the recovery in Dollar Index but it isn't too affected yet as the correction remains shallow so far. The near term strength remains intact as long as it trades above 1.0850.

Pound (1.2874) is consolidating at the higher levels but it may bounce back towards 1.3000 in the next couple of sessions if the immediate support of 1.2830 holds.

Aussie (0.7418) has fallen in a much sharper way than previously expected as the largest decline in Copper (2.538) since 2015 has affected the currency (Check Commodities section). Immediate support comes at 0.7380-70 which must hold to keep any chances of a bounce open.

Dollar-Rupee (64.15) may test 64.00 with a maximum extension to 63.80 before rallying towards 64.20 and higher this month. Immediate downside below 63.80 is not preferred for Dollar-Rupee in the near term.

INTEREST RATES

The US yields could remain stable and move sideways in the near term. The 5yr (1.86%) could move to 1.9% and then come back towards 1.80% while the 10yr (2.32%) could rise towards 2.4%. The 30yr (2.97%) could come down to test support near 2.9% before again moving higher in the longer run.

The Japan-Us 10Yr (2.30%) is rising for the past couple of sessions and in case it rises above 2.32%, we could see some Yen weakness against the US Dollar going forward. Else the yield spread could come off towards 2.2%.

The UK-US 10Yr (-1.25%) is coming off and is likely to move down towards -1.235 or lower in the near term, indicating that the upside for pound could be limited in the coming sessions.