Sample Category Title

Europe Boosted As Macron Retains Large Poll Lead

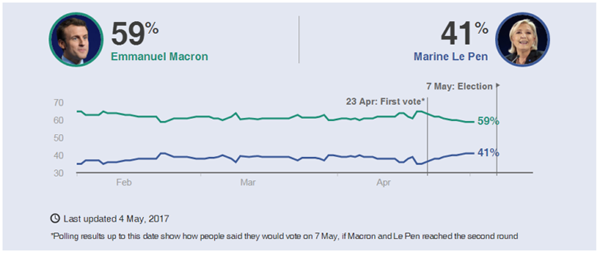

The European session is likely to get off to a positive start on Thursday after French Presidential candidate Emmanuel Macron appeared to edge one step closer to the Elysee, following Wednesday evenings debate with rival Marine Le Pen.

Macron retains poll lead after TV debate performance

With Macron already holding a considerable lead in the polls, the TV debate was Le Pen's best opportunity to close the gap ahead of voting on Sunday. While Le Pen was widely seen as being better suited to the event, it is Macron that is believed to have fared better in the scathing encounter, helping to protect his substantial lead in the process and ease concerns about a late surge by the National Front leader.

The FOMC provided some unexpected impetus

While we have seen Le Pen risk abate in recent weeks as her lead in the polls slipped and Macron took the first round, the spread between French and German 10-year yields remains at the top end of the range it traded at prior to the election premium being priced in. If this is also being reflected elsewhere then there may be potential for a small relief rally next week, should Macron win as expected.

*The polling average line looks at the five most recent national polls and takes the median value, ie, the value between the two figures that are higher and two figures that are lower.

Gold hit by Macron risk rally and dollar gains as Fed hints at June hike

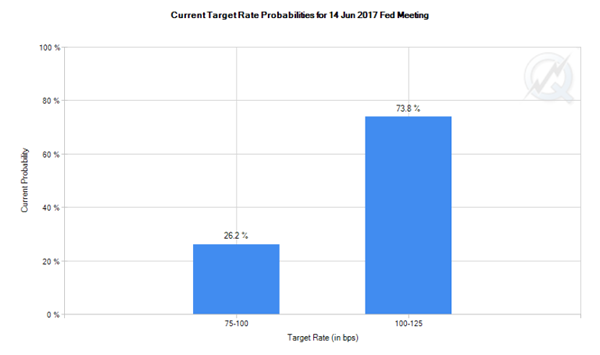

Gold has been dealt a double blow over the last 24 hours, with the post-debate boost to risk appetite and stronger dollar weighing on the yellow metal. The gains in the dollar came as the Fed indicated that it is willing to look through the first quarter weakness which it views as “transitory”, a sign that a second rate hike this year in June very much remains on the table. Markets are now pricing in a 74% chance of a hike next month, up from 68% prior to the statement.

Numerous data releases to come throughout the day on Thursday

With arguably the two biggest events this week now behind us, attention will turn to Friday's jobs report which will offer our first insight into how the US rebounded in the first month of the second quarter. Prior to that though, there is a lot of economic data to come today with services PMIs across Europe being released throughout the morning, followed later this afternoon by jobless claims, productivity, labour costs and factory orders data from the US.

USD/CAD Canadian Dollar Flat After Fed Holds Interest Rate

This morning's Chinese Caixin services PMI got us off to a rocky start but whereas the world's second largest economy is widely expected to slow following a bumper first quarter, data so far this week suggests confidence in Europe is on the rise.

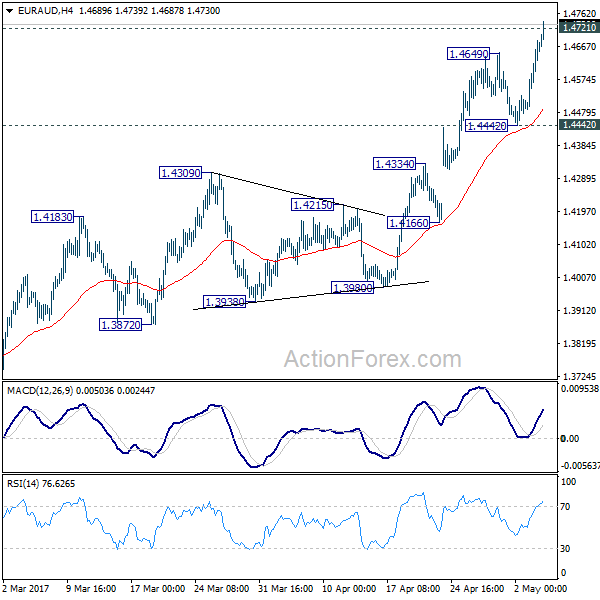

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4537; (P) 1.4612; (R1) 1.4736; More...

EUR/AUD's rally resumed after brief retreat and reaches as high as 1.4739 so far, breaching 1.4721 key resistance. Intraday bias remains on the upside for the moment. We'd holding on to the view of trend reversal after defending 1.3671 key support. Sustained break of 1.4721 will confirm our bullish view. In such case, the next target is 1.5455 medium term fibonacci level. On the downside, break of 1.4442 support is needed to indicate short term topping. Otherwise, outlook will remains bullish in case of retreat.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction could be completed after defending 1.3671 key support. Break of 1.4721 cluster resistance (38.2% retracement of 1.6587 to 1.3624 at 1.4756) should confirm this case and target 61.8% retracement at 1.5455 and above. Overall, we'd expect the up trend from 1.1602 to resume later. However, sustained break of 1.3671 will invalidate our bullish view and would turn extend the fall from 1.6587 towards 1.1602 long term bottom.

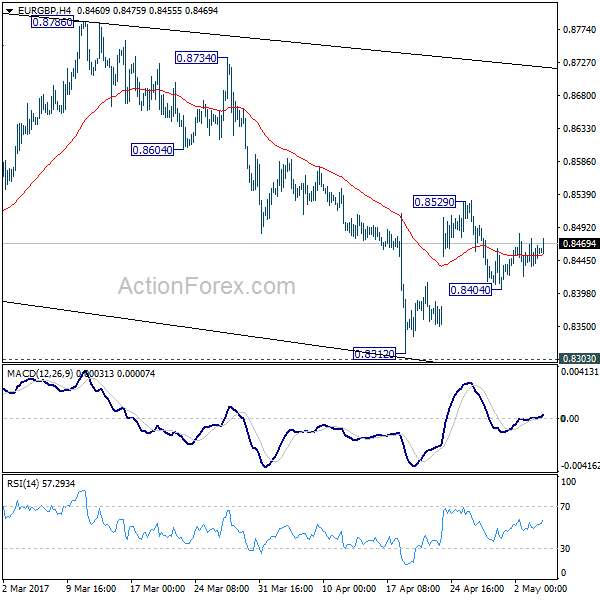

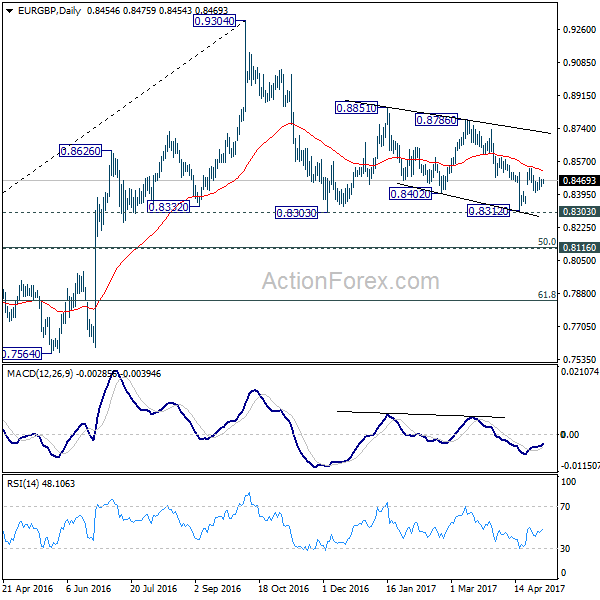

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8437; (P) 0.8456; (R1) 0.8478; More...

Intraday bias in EUR/GBP remains neutral for the moment. On the downside, below 0.8404 will turn focus back to 0.8303 low. Break there will extend the whole corrective pattern from 0.9304. On the upside, above 0.8529 will resume the rebound from 0.8312 towards 0.8786 resistance. Overall, price actions form 0.9304 are seen as a corrective pattern and is extending.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. In case of deeper fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Rise from 0.6935 (2015 low) will resume at a later stage to 0.9799 (2008 high). However, sustained break of 0.8116 could bring deeper decline to next key support level at 0.7564 before the correction completes.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 144.60; (P) 144.97; (R1) 145.45; More....

GBP/JPY continues to lose upside momentum as seen in 4 hour MACD. But with 143.79 minor support intact, further rally is still expected. Sustained trading above 144.77 resistance will resume the whole rebound from 122.36 through 148.42 high to 150.42 fibonacci level. On the downside, though, break of 143.79 minor support will bring pull back to 4 hour 55 EMA (now at 143.18) and below, before staging another rally.

In the bigger picture, based on current momentum, rise from 122.36 bottom should be developing into a medium term move. Break of 38.2% retracement of 195.86 to 122.36 at 150.42 should pave the way to 61.8% retracement at 167.78. This will now be the favored case as long as 135.58 support holds.

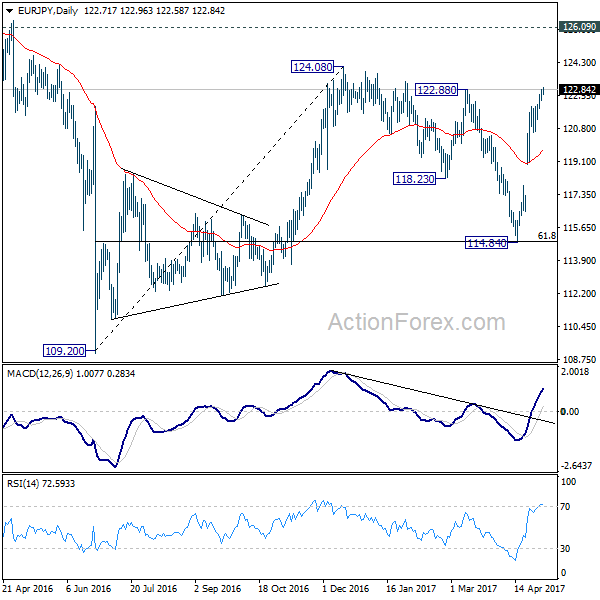

EUR/JPY Daily Outlook

Daily Pivots: (S1) 122.41; (P) 122.64; (R1) 122.96; More...

Upside momentum in EUR/JPY is a but unconvincing as seen in 4 hour MACD. But further rally is still expected with 120.60 support holds. As noted before, the correction from 124.08 should have completed with three waves down to 114.84 already. Firm break of 122.88 resistance will extend larger rise from 109.20 through 124.08 high. On the downside, break of 120.60 will indicate short term topping and bring deeper pull back, possibly to 55 day EMA (now at 119.71).

In the bigger picture, focus is back on 126.09 support turned resistance. Decisive break there will confirm completion of the down trend from 149.76. And in such case, rise from 109.20 is at the same degree and should target 141.04 resistance and above. Meanwhile, rejection from 126.09 and break of 114.84 will extend the fall from 149.76 through 109.20 low.

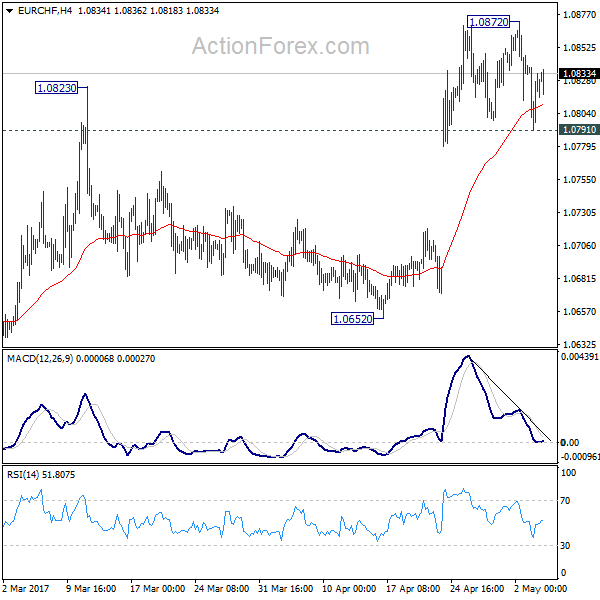

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0798; (P) 1.0819; (R1) 1.0845; More...

Despite dipping to 1.0791, EUR/CHF quickly recovered and intraday bias remains neutral first. At this point, further rally is still expected and break of 1.0872 should target 1.0897 resistance. Decisive break there should confirm our bullish view of reversal and will target 1.0999 resistance next Nonetheless, break of 1.0798 support will indicate short term topping and turn focus back to 55 day EMA (now at 1.0735).

In the bigger picture, the price actions from 1.1198 are seen as a corrective move. Current strong rebound is raising the chance that it's completed after defending 38.2% retracement of 0.9771 to 1.1198 at 1.0653. Decisive break of 1.0999 resistance will target a test on 1.1198 high. For now, this will be the preferred case as long as 1.0652 support holds.

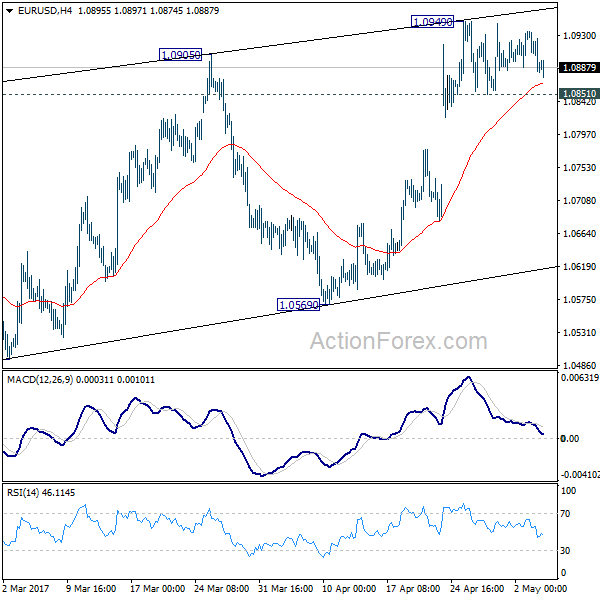

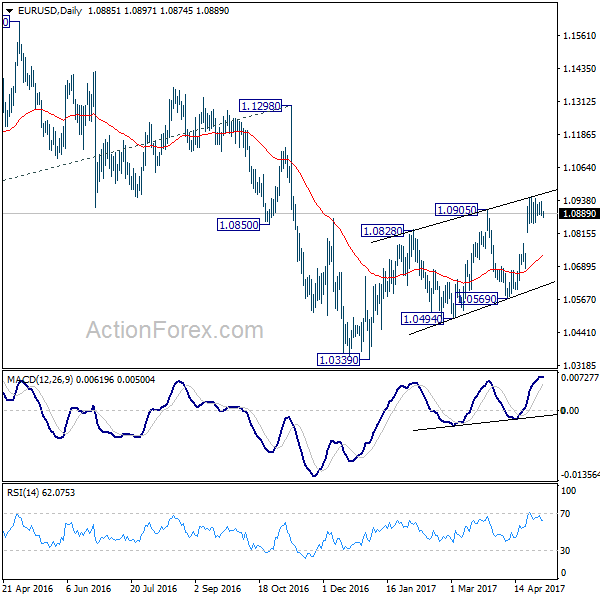

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0865; (P) 1.0900 (R1) 1.0919; More....

EUR/USD is still bounded in range of 1.0851/0949 and intraday bias remains neutral. At this point, further rise is still in favor as long as 1.0851 minor support holds. However, choppy rebound from 1.0339 is seen as a correction. Hence we'd look for topping again on next rise. Meanwhile, on the downside, break of 1.0777 will turn turn bias to the downside for 1.0851 support first.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. This would also be supported by sustained trading above 55 week EMA.

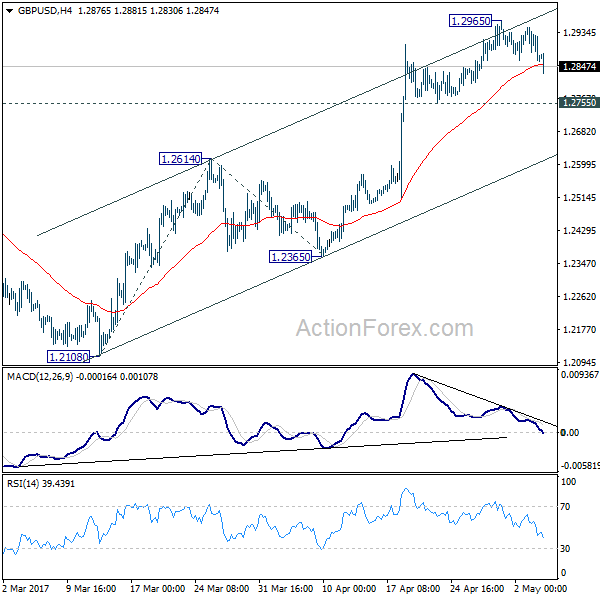

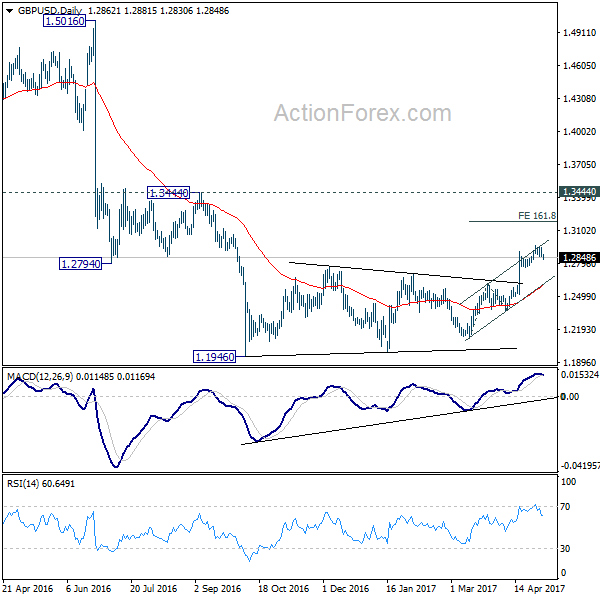

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2838; (P) 1.2893; (R1) 1.2921; More...

GBP/USD's pull back from 1.2965 extends today but it's staying above 1.2755 support. Intraday bias remains neutral with another rise in favor. Break of 1.2965 will target 161.8% projection of 1.2108 to 1.2614 from 1.2365 at 1.3184. At this point, price actions from 1.1946 are still interpreted as a correction pattern. Therefore, we'd expect strong resistance below 1.3444 to bring larger down trend resumption. On the downside, break of 1.2755 minor support will turn bias to the downside. Further break of 1.2614 resistance turned support will now indicate near term reversal.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Market Update – Asian Session: China PMI Figures Continue To Signal More Pronounced Slowdown

Asia Mid-Session Market Update: China PMI figures continue to signal more pronounced slowdown; USD consolidates post-FOMC gains

US Session Highlights

(US) APR ADP EMPLOYMENT CHANGE: +177K V +175KE (lowest since Oct); March revised lower

(US) APR FINAL MARKIT SERVICES PMI: 53.1 V 52.5E

(US) Puerto Rico reportedly increases offer to general obligation bondholders to as much as 90 cents on the dollar - press

(US) APR ISM NON-MANUFACTURING COMPOSITE: 57.5 V 55.8E; new orders jump to highest since 2005

(US) DOE CRUDE: -0.9M V -2ME; GASOLINE: +0.2M V +0.5ME; DISTILLATE: -0.6M V +0.5ME

FOMC statement cited recent economic data weakness and wouldn't change current stance on the progression of interest rate increases. The statement also mentioned that the labor market continued to show signs of strength and consumer spending was solid, with inflation close to target. Overall, the reading remains for a further two rate hikes this year.

US markets on close: Dow +0.2%, S&P500 +0.1%, Nasdaq +0.1%

Best Sector in S&P500: Financials

Worst Sector in S&P500: Real Estate

Biggest gainers: FSLR +11.8%; DLPH +10.9%; CTXS +7.1%

Biggest losers: FTR -16.5%; AKAM -15.5%; APC -7.7%

At the close: VIX 10.7 (+0.1pts); Treasuries: 2-yr 1.30% (+4bps), 10-yr 2.31% (+1bps), 30-yr 2.95% (-3bps)

US movers afterhours

TLRD Raises FY17 $1.60-1.90 v $1.66e (prior $1.45-1.75); to wind down partnership with Macy's; +10.0% afterhours

DATA Reports Q1 -$0.03 v -$0.10e, R$200M v $201Me- Non-GAAP op margin -2.1% v -0.7% y/y - Customer account adds 3.3K, total 57K; +7.3% afterhours

FIT Reports Q1 -$0.15 v -$0.18e, R$298.9M v $277Me- Guides Q2 -$0.17 to -$0.14 v -$0.11e, R$330-350M v $340Me; +7.2% afterhours

SQ Reports Q1 +$0.05 v -$0.08e, R$462M v $451Me- Guides Q2 adj +$0.03-0.05 v -$0.07e; EBITDA$25-28M, adj Rev $223-226M v $532Me; +5.0% afterhours

TSLA Reports Q1 -$1.33 v -$0.55e, R$2.70B v $2.56Be; -2.4% afterhours

FB Reports Q1 $1.04 v $1.10e, R$8.03B v $7.85Be- Monthly active users (MAUs) 1.94B, +17% y/y; -2.5% afterhours

CAR Reports Q1 -$0.94 v -$0.51e, R$1.80B v $1.85Be- Cuts FY17 $2.85-3.50 v $3.16e, Affirms Rev +2-3% y/y, implies $8.8-8.95B v $8.81Be; -6.0% afterhours

CAKE Reports Q1 $0.72 v $0.73e, R$563.4M v $565Me; -7.6% afterhours

Key economic data

(CN) CHINA APR CAIXIN PMI SERVICES: 51.5 V 52.2 PRIOR; 4th month of sequential decline and weakest level since May 2016

(AU) AUSTRALIA MAR TRADE BALANCE (A$): +3.11B V +3.25BE (5th consecutive surplus)

(NZ) NEW ZEALAND APR ANZ JOB ADVERTISEMENTS M/M: 2.8% V 2.0% PRIOR

(NZ) NEW ZEALAND APR ANZ COMMODITY PRICE M/M: -0.2% v 0.4% PRIOR

(SG) SINGAPORE APR PMI COMPOSITE: 52.6 V 52.2 PRIOR; highest since Nov 2016

Asia Session Notable Observations, Speakers and Press

Asia indices are mixed in the wake of modest gains on Wall St, as surprisingly less cautious than anticipated Fed statement in light of disappointing US economic data of late supported expectations for pre-charted FOMC policy course. Australia remains among the worst performers in the region, with mining space hit by another steep decline in iron ore prices while Japan remains closed for holiday. In Hong Kong, defensive Utilities fared better, while autos, banks, and tech shares slumped. In commodities, WTI remains under slight pressure, though Copper prices are off their lows following the steep plunge in US hours.

FX is also more rangebound after US midday volatility saw USD/JPY hit 6-weeks highs just shy of 113 level on higher post-FOMC short-term rates. AUD was dented by softer China Caixin Services/Composite PMIs before erasing its losses on comments from RBA Gov Lowe, who was discussing the risks of record high household debt to income ratio in the context of inevitably tighter policy.

In economic data, China Caixin Services PMI hit an 11-month low with its 4th straight sequential decline, as new order rate of growth slowed, employment growth eased to the weakest level this year, backlogs of work fell, and cost pressures eased across all sectors. Aussie Trade Balance saw its 5th straight month of surplus, with export growth edging higher to 2.0% from 1.5% and imports up 5% v decline of 5% in prior month. Iron ore shipments rose to 3-month highs.

China

(CN) China FX regulator (SAFE) vice chair Zheng Wei: China to manage companies with high FX business risk more strictly - press

(CN) Analyst: China should consider introducing new bond products to raise funds for market-oriented debt-to-equity swaps - CSJ

Australia

(AU) RBA Gov Lowe: Should not expect rates to always be this low, households should be prepared for an increase in interest rates in Australia at some point

(AU) Australia Port Hedland Apr Iron Ore Exports 42.2Mt, +12% y/y

Asian Equity Indices/Futures (00:30ET)

Nikkei closed, Hang Seng -0.5%, Shanghai Composite -0.1%, ASX200 -0.6%, Kospi +0.7%

Equity Futures: S&P500 +0.1%; Nasdaq +0.1%, Dax +0.2%, FTSE100 +0.1%

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.0880-1.0900; JPY 112.60-112.90; AUD 0.7405-0.7430; NZD 0.6875-0.6895

June Gold -0.6% at 1,241/oz; June Crude Oil -0.2% at $47.72/brl; July Copper +0.8% at $2.54/lb

(CN) PBOC to inject combined CNY50B v CNY200B prior in 7-day, 14-day and 28-day reverse repos

(CN) PBOC SETS YUAN MID POINT AT 6.8957 V 6.8892 PRIOR; Weakest Yuan fix since Apr 11th

Asia equities notable movers

BoCom (3328.HK) -1.2%; Bocom International Holdings unit looking to raise up to HK$2.07B from IPO; May issue USD bond as early as next week - financial press

Galaxy Entertainment (27.HK) -0.8%; Q1 results

NAB (NAB.AU) -0.2%; H1 result

Vocus (VOC.AU); -1.8% In talks to sell data center business

Kathmandu (KMD.AU) +4.5%; Q3 sales

Currencies: Dollar Modestly Higher On FOMC Statement

Sunrise Market Commentary

- Rates: June rate hike discounted after FOMC meeting

The FOMC kept policy unchanged but labelled the Q1 growth slowdown as 'transitory', suggesting they remain on track to hike rates in June. The market implied probability of a June rate hike increased from 66% to 97.5%, triggering a modest repositioning in US yields (higher, front end underperforming). Today's focus turns to US Congress. - Currencies: Dollar modestly higher on FOMC statement

The dollar gained modest ground as the Fed didn't change rate hike expectations. The technical picture of USD/JPY improved as the pair regained the 112.20 level. Today, FX traders will keep an eye at the Healthcare vote in the US Congress and look forward to the payrolls. The dollar probably needs high profile good news to regain sustained ground against the euro.

The Sunrise Headlines

- US stock markets ended marginally lower with Nasdaq underperforming, dragged down by mediocre Apple earnings. Overnight, Asian stocks trade mixed with China underperforming following a weaker Caixin services PMI.

- The Fed kept policy unchanged and said it expected economic growth to rebound after a soft first quarter, signaling the central bank is likely to continue gradually raising short-term interest rates this year if it is right.

- France's two presidential candidates clashed on primetime over the economy, home-grown jihadism and the EU, in a fierce showdown. An Elabe poll suggested that centrist Macron had appeared more convincing for 63% of the viewers.

- Theresa May has accused 'European politicians and officials' of threatening Britain and trying to sabotage her attempt to win the general election in an apparently deliberate move to stoke Brexit tensions with Brussels.

- House Republican leaders said the chamber would vote today on their bill to replace most of Obamacare, in a show of confidence that they can lock down enough Republican support for a bill that sparked a nationwide debate.

- Belgium sold about a quarter of its stake in BNP Paribas to raise cash (€2.03B), taking advantage of a rally in the stock as it neared a post-crisis high. The government's stake drops from 10.3% to 7.8%

- Today's eco calendar contains services PMI's in EMU (final) and the UK and US weekly jobless claims. ECB Lautenschlaeger, Praet and Draghi are scheduled to speak. Spain and France tap the market. Norges bank decides on policy

Currencies: Dollar Modestly Higher On FOMC Statement

Dollar gains modest ground after Fed decision

Trading in EUR/USD and USD/JPY was locked in tight ranges yesterday as investors awaited guidance from the Fed's policy statement later in the evening. The Fed kept its policy unchanged and basically maintained its assessment from March. Q1 economic weakness is considered transitory. So, the expected path of (at least) two additional rate hikes this year remains valid. The dollar gained modest ground after the Fed's policy statement. EUR/USD closed the session at 1.0886 (from 1.0930). USD/JPY finished the day at 112.75, from 111.99.

Overnight, Asian equities show a mixed picture. Japan is still closed for the golden week holidays. Chinese equities again underperform. After the Caixin manufacturing PMI, also the services PMI declined, from 52.1 to 51.2. Yesterday's substantial decline of several industrial commodities might be a (slightly) negative for some Asian markets this morning. The dollar maintains most of its post-Fed gains. EUR/USD trades around 1.0895. USD/JPY is changing hands in the 112.80 area. The Aussie dollar is trading at the lowest level since mid-January (0.74 area). The stronger US dollar and lower commodities weighed on AUD. RBA's Lowe warned that high household debt makes the economy less resilient to shocks.

EMU data (final April services PMI and EMU March retail sales) probably won't move FX trading today. US eco data are plentiful (Challenger layoffs, initial claims, nonfarm productivity, factory orders and the March trade balance ) but the impact on the dollar, if any, should only be of intraday significance on the eve of the US payrolls report. Speeches of ECB president Draghi and Executive Board members Praet and Lautenschlaeger might be more important. Draghi last week held off the debate on policy normalization. Since, inflation came out much stronger than expected, but it is unlikely that he will already change his view. However, we are keen the hear the view of Praet and hawk Lautenschlaeger. Will she start the offensive of the hawks?

In a daily perspective, the dollar might be better supported after yesterday's Fed statement. The market almost fully discounts a June rate hike (97.5%). This should be modestly USD supportive. ECB speakers are a wildcard for the euro. As we don't expect Draghi or Praet to already signal a change in their assessment, the euro reaction should be limited. However, any small hint might be euro supportive. Of late, USD/JPY profited most from a rise in core yields. This trend might continue. For EUR/USD, we expect the pair to stay away from the 1.0950 resistance going into the payrolls. However, really strong US data/or other good news (Healthcare bill?) are probably needed to push the pair back south.

Last week, the European risk trade supported USD/JPY, but also EUR/USD and EUR/JPY. The market pondered whether declining political risk could bring forward the ECB's normalisation process. This hope was moderated after the ECB press conference. The Fed confirming its intentions on policy normalisation is also slightly USD supportive. From a technical point of view, USD/JPY started a bottoming out process and yesterday's re-break above 112.20 improved the technical picture. Next intermediate resistance comes in at 115.51. EUR/USD extensively tested the topside of the MT range (1.0874/1.0906 area) late March. The pair returned to the range top after the French election and set minor new highs. Yesterday's move slightly eased the upside momentum, but the technical picture hasn't changed. A decline below 1.0821 would suggest that the dollar is regaining traction against the euro. For now, we maintain a neutral bias.

R/USD declines modestly after Fed policy statement, but technical picture is little changed

EUR/GBP

Brexit tensions slightly weigh on sterling

Sterling was under pressure at the start of European trading yesterday as an FT article indicated that the EU could demand the UK a ‘separation charge' of up to €100B. The report followed other recent signals that the UK and the EMU might be heading for very tough Brexit-negotiations. EUR/GBP touched an intraday top of 0.8476. Cable spiked to the 1.2885 area. However there was no follow-through sterling selling. The UK April construction PMI rebounded to 53.1 from 52.2 (52.0 was expected). The release is not that important for markets, but it helped to put a floor for sterling even as the political bickering between the EU and the UK continued. EUR/GBP closed the session at 0.8460. Cable finished the day at 1.2867, but part of the intraday decline was due to the post-Fed USD rebound.

Today's eco calendar contains the services PMI and the monetary data. The services PMI is expected to decline slightly from 55.00 to 54.5. However, the manufacturing measure and the construction PMI surprised on the upside. A really strong figure might be slightly supportive for sterling. Over the previous days, Brexit tensions between the UK and the EU came again more to the forefront as a driver for sterling trading. Overnight, UK PM May accused EU officials of interfering in the UK election process. If the bickering continues it might be a further negative for sterling. We have the impression that the downside in EUR/GBP has become better protected.

Two weeks ago, EUR/GBP dropped below EUR/GBP 0.84 support, (temporary) improving the sterling picture. The pair came within reach of the key 0.8305 support (Dec low), but no real test occurred. After last week's EUR/GBP rebound, the range bottom is better protected. Longer term, Brexit-complications remain potentially negative for sterling. On technical considerations we are inclined to reconsider a cautious EUR/GBP buy-on-dips approach.

EUR/GBP: downside better protected after last week's rebound