Sample Category Title

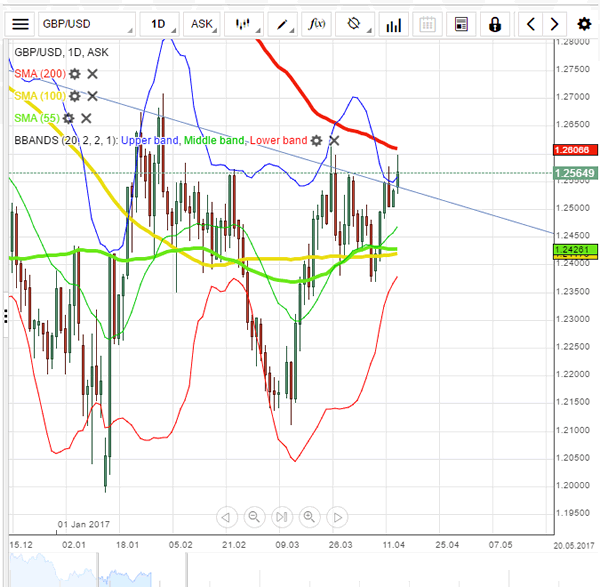

GBP/USD Analysis: Keeps Climbing Up

'There's significant resistance for GBP/USD between 1.25 and 1.2630.' – BK Asset Management (based on PoundSterlingLive)

Pair's Outlook

Monday ended with the British Pound outperforming the US Dollar, which resulted in the six-month bearish trend-line getting pierced. The Cable, however, now faces another strong resistance, namely the cluster around 1.2610, represented by the upper Bollinger band, the weekly R1 and the 200-day SMA. Technical indicators keep pointing to another potential rally today, in which case the Sterling would have the opportunity to reclaim 1.26. Nevertheless, there is no impetus present that could help the GBP/USD pair overcome the 200-day SMA at 1.2626, not yet at least.

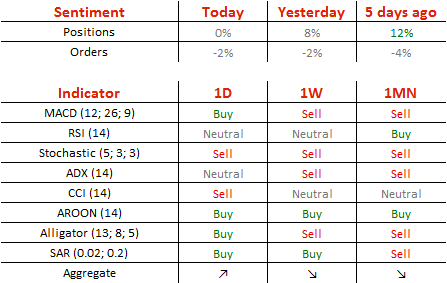

Traders' Sentiment

Market sentiment reached a perfect equilibrium today, but the portion of orders to sell the Pound remained unchanged, still taking up 51% of the market.

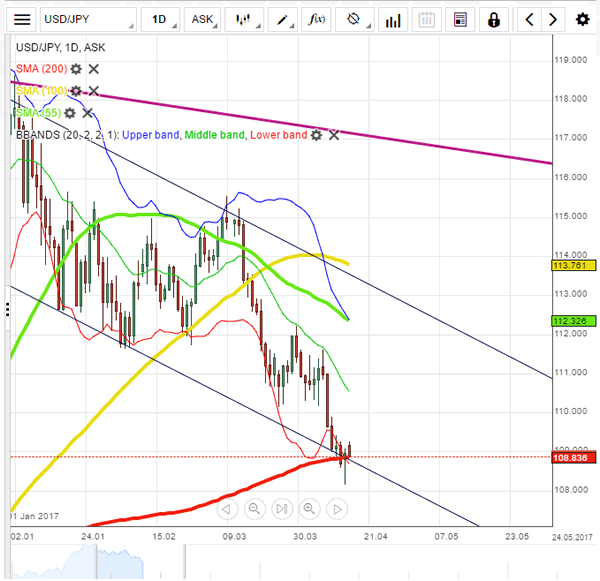

USD/JPY Analysis: Attempts To Preserve The Channel Pattern

'It is unclear whether the situation over North Korea will escalate into military action, but uncertainty is increasing and the dollar continues to edge lower. The dollar also looks shaky technically, after slipping below the 200-day moving average of 108.80 yen.' – Mizuho Securities (based on Reuters)

Pair's Outlook

Despite initial sharp downside volatility, the US Dollar managed to end the day in the green zone yesterday, adding 14 pips against the Japanese Yen. The recovery suggests that the channel pattern remains in play, but with the lower bounder now being significantly weaker. A successful rally today could be the first step towards reaching the pattern's resistance line near 112.00, but technical indicators are unable to confirm this scenario. Downside risks are also present due to the recent breach, but the US fundamental data could provide the required boost for the given pair to stabilise above 109.00.

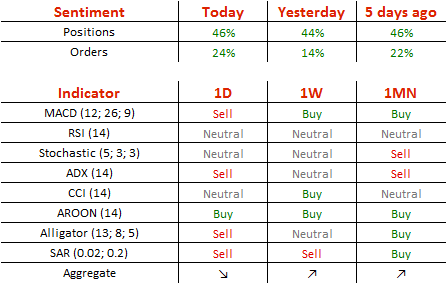

Traders' Sentiment

The Buck remains overbought, as 73% of all open positions are long (previously 72%). The number of orders to acquire the Greenback inched up from 57 to 62%.

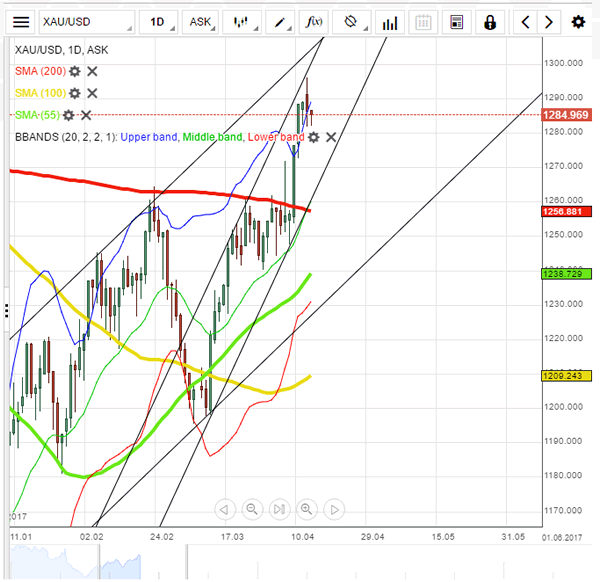

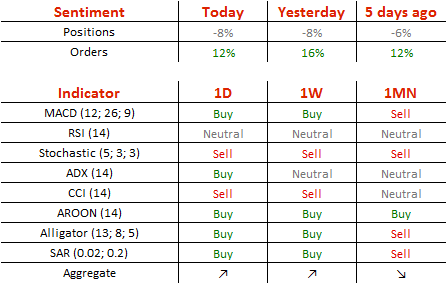

Gold Analysis: Retreats On Tuesday

'The U.S. dollar steadied after Treasury Secretary Steven Mnuchin said U.S. President Donald Trump's recent remarks that the dollar is getting too strong were about the short term.' – Nallur Sethuraman, Reuters

Pair's Outlook

After hitting a five month high level the gold price began a period of consolidation, which became a decline due to fundamental events. The main reason for the decline of the bullion's price was the comments made by the Treasury Secretary of the US Steven Mnuchin, who expressed that the US President sees the strong US Dollar only as a problem in the short term. It is most likely that the bullion will continue its surge, as turmoil around the world drives the run to safety. Moreover, a new medium term ascending channel pattern seems to have revealed itself due to the recent decline of the commodity price.

Traders' Sentiment

SWFX gold traders remain bearish, as 54% of open positions are short. However, 56% of set up orders are to buy the metal.

Investors Turn To Safe Havens On Rising Regional Tensions

Recent US military actions, such as the airstrike in Syria, the movement of an aircraft carrier strike group toward the Korean Peninsula and the dropping of 'the mother of all bombs' on ISIS in Afghanistan has led to rising tensions amongst some of the world superpowers.

The rising regional tensions have lifted the markets' risk aversion sentiment. Investors are turning away from riskier assets towards safe havens, resulting in the weakening of US equity markets. Monday April 17, saw spot gold surge to the highest level of 1295.37 since November 9, it has rallied 2.6% since Syria strike on April 7.

The first round of the French election is to be held this Sunday April 23. The latest polls conducted between April 12-14 showed a tightening race: Macron, Le Pen are both 22%, Macron and Le Pen got a lower share of the vote compared to 23% from a previous poll. The far-left candidate Jean-Luc Melenchon, has slipped to third position, with 20% of voters, which surpassing Fillion's 19%. Jean-Luc Melenchon is the only candidate among the four whose share of vote saw an increase recently. The difference of votes between the 4 candidates is less than 3% which poses more uncertainty to the election.

The US retail sales and CPI data for March released last Friday both underperformed. Retail sales (MoM) fell to -0.2%, retail sales for February was revised downward to -0.3% from 0.1%, marking the first decline since August 2016. The drop was partially caused by the recent decline in automobile and petrol sales. However, consumer electronics and clothing sectors saw a growth. Retail sales exclude autos for March (MoM) fell to 0.0%, marking the lowest growth since August 2016.

US CPI and core CPI (YoY) for March were 2.4% and 2.0% respectively, marking the lowest growth since January 2017 and November 2015. Per CME's FedWatch tool, after the release of US retail sales and CPI data for March, the probability of a rate hike in June has dropped to 50.7%.

The Bank of Japan Governor Kuroda stated on Monday April 17 that employment and wages are improving steadily, consumer spending saw a pickup. The positive economic indicators continue to strengthen JPY ahead of the upcoming BoJ's meeting on April 27. Monday USDJPY hit the lowest level of 108.12 since November 15.

First Quarter Growth Sent Pleasant Surprise, Tighter Lending Drove Borrowers to ‘Shadow Bank’

China's economic activities surprised to the upside in 1Q17. GDP expanded +6.9% y/y, beating consensus of, and 4Q16's, +6.8%. Growth was led by a +7.7% expansion in the tertiary sector, followed by a +6.4% growth in the secondary industry. Economic activities also strengthened across the board in March. Retail sales expanded +10.9%, accelerating from +9.5% in the combined January to February period. Industrial production (IP) growth improved to +7.6%, the fastest pace since end-2014, from +6.3% in the January-February period. The market had anticipated a mild drop to +6.2%. Fixed asset investment (FAI) increased 9.2% y/y to March, up from +8.9% in the January-February period. Looking into the details, investment gained +19.8% in the primary sector, +4.2% in the secondary sector and +12.2% y/y in the tertiary sector. Moreover, private investment expanded +7.7% y/y in March, up from +6.7% in the prior month, while the growth in public investment slowed to +13.6%, from +14.4% in February. For the first quarter of the year, retail sales grew +10%, IP rose +6.8% with manufacturing output up +7.4% while fixed asset investment expanded +9.2%, of which real estate investment and tech investment up +9.1% and +22.6%, respectively.

Housing and lending remained the key drivers to Chinese growth in 1Q17. Besides strong FAI growth, a report from National Bureau of Statistics (NBS) shows that new home prices gained +0.6% in March, doubling the growth in February. Although property sales growth eased in March, the three-month moving average suggests that it remains in an uptrend in both volume and value terms. Growth of land sales and housing starts also stayed firm. The strong property cycle is expected to help avoid a sharp slowdown this year.

As indicated in PBOC's report published late last week, the country's new renminbi loans dropped to RMB1.02 trillion in March from RMB1.17 trillion a month ago. The market had anticipated a pickup to RMB1.25 trillion. It was estimated that 40% of the new loans was property lending loans (developers plus household) which soared +26% y/y to RMB28.4 trillion at end-March. The new loans figure would increase to RMB 1.16 trillion after adding back interbank lending. Incremental Total Social Financing (TSF) rebounded to RM 2.1 trillion. TSF outstanding balance gained +12.5% y/y. Broad money supply (M2) growth slowed to +10.6% y/y, the slowest pace in 8 months. Moderation in loan growth can be viewed as a result of the government's tighter policy measures. Yet, restrictions of acquiring loans through traditional channels have encouraged shadow lending. New shadow lending (including entrusted loans, trust loans and bank acceptances) was reported to have reached RMB2.05 trillion in the first quarter, up +320% from the same period last year.

The current environment suggests that China's property market has remained buoyant, despite the government's tightening measures. Investors/speculators have been driven to shadow lending, an activity that the government has been trying to curb, for funding. Yet, we expect the government would have few choices but to continue its monetary tightening measured targeting the asset markets

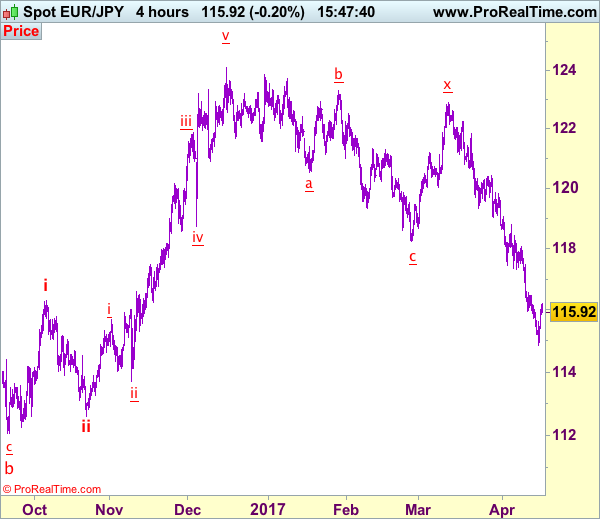

Trade Idea: EUR/JPY – Sell at 118.00 or buy at 115.25

EUR/JPY - 115.93

Recent wave: wave v of (C) ended at 94.12 and major correction in wave A has ended at 149.79

Trend: Near term down

Original strategy:

Sell at 118.00, Target: 116.00, Stop: 118.60

Position: -

Target: -

Stop: -

New strategy :

Sell at 118.00, Target: 116.00, Stop: 118.60

O.C.O.

Buy at 115.25, Target: 117.25, Stop: 114.65

Position: -

Target: -

Stop:-

Although the single currency extended recent decline to as low as 114.85 yesterday, the subsequent rebound suggests a temporary low is possibly formed there and consolidation with mild upside bias is seen for retracement of recent decline, hence gain to 117.00 and then 117.45-50 is likely, however, reckon resistance at 118.07 would limit upside and bring another decline later.

In view of this, whilst we are looking to turn long on dips, we would also sell euro on subsequent rebound towards 118.00. Below said support at 114.85 would signal recent entire fall from 124.10 top is still in progress and downside risk remains for further weakness to 114.40-50, then towards 114.00-10, however, near term oversold condition should prevent sharp fall below latter level and risk from there is seen for a much-needed rebound to take place later.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).

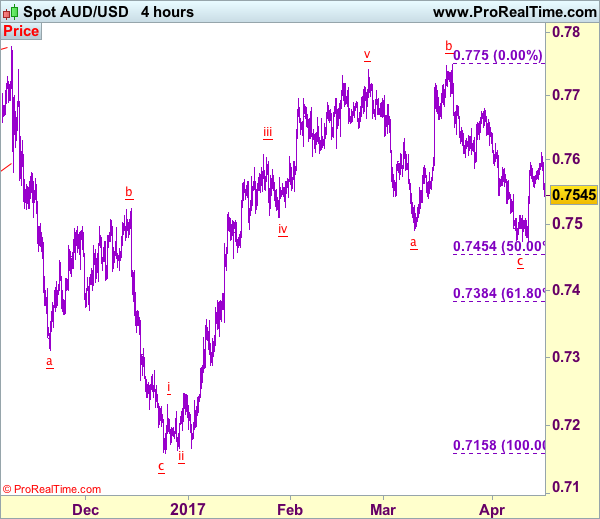

Trade Idea: AUD/USD – Exit long entered at 0.7525

AUD/USD – 0.7555

Recent wave: Wave 5 ended at 1.1081 and major correction has commenced for fall to 0.7000 and then towards 0.6500-10

Trend: Near term down

Original strategy :

Bought at 0.7525, Target: 0.7680, Stop: 0.7465

Position: - Long at 0.7525

Target: - 0.7680

Stop: - 0.7465

New strategy :

Exit long entered at 0.7525

Position: - Long at 0.7525

Target: -

Stop:-

Although aussie rose briefly to 0.7611 yesterday, lack of follow through buying and the subsequent retreat suggest consolidation would be seen and downside risk has increased for weakness to 0.7500, however, only break of last week’s low at 0.7473 would signal the decline from 0.7750 top has resumed and extend weakness to 0.7450-55 (50% Fibonacci retracement of 0.7158-0.7750) but oversold condition should limit downside to 0.7380-85 (61.8% Fibonacci retracement), risk from there is seen for a rebound later.

In view of this, would be prudent to exit long entered at 0.7525 and stand aside for now. Above said resistance at 0.7611 would revive bullish view that low has been formed at 0.7473 last wee, bring further gain towards resistance at 0.7680 but break there is needed to retain bullishness and signal the fall from 0.7750 has ended, bring further gain to 0.7700-10 first.

On the 4-hour chart, the move from 0.8066 is the wave 5 with i: 0.8860, ii: 0.8315, wave iii is an extended move ended at 1.0183, iv: 0.9706 and wave v has ended at 1.1081 (also the top of entire wave 5). The subsequent selloff is the major correction which is unfolding as ABC-X-ABC and 2nd A leg has ended at 0.8848, followed by a-b-c wave B which ended at 0.9758, hence, 2nd C wave is now in progress and indicated downside target at 0.7000 and 0.6950 had been met, so further fall to 0.6710-20 cannot be ruled out.

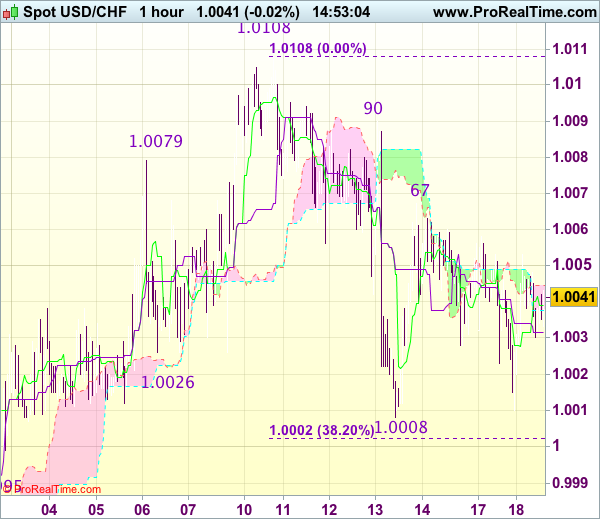

Trade Idea : USD/CHF – Stand aside

USD/CHF - 1.0032

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.0039

Kijun-Sen level : 1.0032

Ichimoku cloud top : 1.0045

Ichimoku cloud bottom : 1.0039

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite falling to 1.0010 yesterday, as the greenback has rebounded again after holding above last week’s low at 1.0008, suggesting further choppy trading within near term established range would be seen and risk of another bounce to 1.0067 resistance cannot be ruled out, however, break there is needed to signal low has been made at 1.0008, bring test of 1.0090, once this level is penetrated, this would suggest the fall from 1.0108 high has ended, bring retest of this last week’s high first.

On the downside, below said support at 1.0008 would extend the fall from 1.0108 top to previous support at 0.9995, however, still reckon downside would be limited to 0.9970 (50% Fibonacci retracement of 0.9831-1.0108) and 0.9940-50 should hold from here, bring rebound later. As near term outlook is still mixed, would be prudent to stand aside for now.

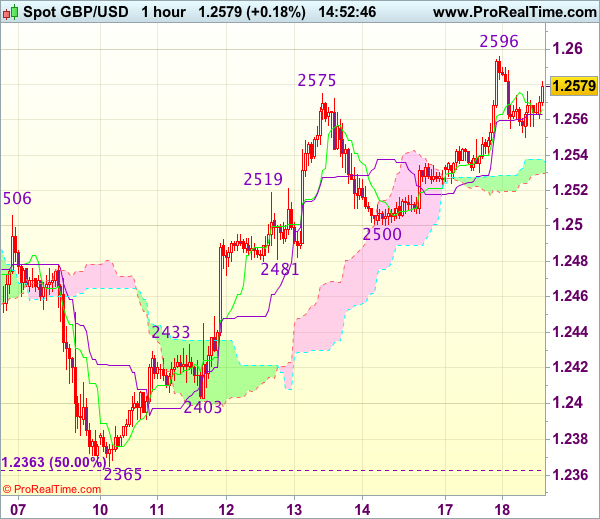

Trade Idea : GBP/USD – Buy at 1.2510

GBP/USD - 1.2589

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2573

Kijun-Sen level : 1.2563

Ichimoku cloud top : 1.2536

Ichimoku cloud bottom : 1.2530

Original strategy :

Buy at 1.2480, Target: 1.2580, Stop: 1.2445

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2510, Target: 1.2610, Stop: 1.2475

Position : -

Target : -

Stop : -

As cable found renewed buying interest at 1.2500 late last week and has surged again, adding credence to our bullish view that recent upmove is still in progress and upside bias remains for last week’s rise from 1.2365 to extend gain to previous resistance at 1.2616, however, break there is needed to retain bullishness and bring subsequent upmove to 1.2650-60 which is likely to hold on first testing due to near term overbought condition.

In view of this, would not chase this rise here and would be prudent to buy cable on pullback as said support at 1.2500 should limit downside and bring another upmove later. Below another previous support at 1.2481 would abort and suggest top is formed, risk test of 1.2433 (previous resistance) later.

Mixed Messages On The U.S. Dollar, Who Should You Listen To?

The U.S. dollar continued to recover from a five-month low against the Yen early Tuesday, after testing 108.11 yesterday. Comments from U.S. Secretary of the Treasury Steven Mnuchin, stating that a strong dollar is good in the long run, offset previous remarks from President Trump who last week said that the dollar is getting too strong and that it is hard to compete when other countries devalue their currency. However, Mnuchin also agreed that the dollar’s strength in the short run is hurting exports and the economy;based on such mixed signals, traders are finding it difficult to choose on which side to take a trade.

Since both the U.S. President and Secretary of the Treasury agree that the greenback is overvalued in the short-term perspective, dollar bulls shouldn’t get overexcited on the long run views. Instead, I would suggest ignoring what politicians are claiming for the time being and to focus on what most recent economic data is saying:

- U.S. inflation expectations fell to their lowest levels in 2017

- Retail sales fell for a second month in March

- Consumer prices dropped for the first time in over a year

- Atlanta Fed cuts U.S. first quarter GDP to 0.5%

- U.S. non-farm payrolls marked the smallest gain since May 2016

This set of most recent economic hard data indicates that the robust soft data reflecting consumer and business sentiment didnot translate into spending, investing and hiring. There’s a clear gap here and such a divergence may not last for long. Either hard data should agree with sentiment surveys, or optimism will start to fade.

Mnuchin sent another signal on tax reforms on Monday, saying that expecting one before August is highly aggressive and not realistic. Investor and traders are likely to start questioning whether Trump will be able to deliver on tax reform and stimulus but so far most signs are negative, thus another negative factor affectingthe USD.

Expectations of a wider divergence in monetary policy also took a hit. Markets expectations for a June rate hike have fallen below 50%, down from more than 60% just a week ago according to the CME FedWatchTool. Moreover, chances of two rate hikes in 2017 dropped below 40%, so traders betting on interest rates differentials should tweak their model assumptions.

Overall, there’s a high chance that the dollar could have already topped out for the year, but whether more declines willbe seen relies heavily on fundamental drivers, not verbal interventions. I would prefer selling the rallies than buying the dips on the short-run until we see solid evidence of U.S. fiscal stimulus.