Sample Category Title

USD Strengthens as US and North Korean Tensions Increase

- Sterling slips in data vacuum

- USD strengthens as US and North Korean tensions increase

- Australian Dollar stronger as Aussie employment jumps

The US Dollar strengthened a little over the last few days. Tensions around the US's warning to China over North Korean sabre rattling has dragged funds into safe US treasuries. US President Trump shook the markets on Wednesday when he suggested the US Dollar was too strong. In spite of this strength in the latter part of the week, the Dollar ended the week weaker than it started. This week brings the US Federal Reserve Beige book, manufacturing data in various forms and a slew of Purchasing Managers' Indices (PMI).

The GBP-USD rate is stuck in a narrow band for now but the US Federal Reserve, Kim Jong Un and other factors could change that.

The Sterling-Euro exchange rate is similarly range-bound but the Euro struggled to gain any traction last week as tension mounted over the French elections. Polls suggest Marine Le Pen and Emmanuel Macron are neck and neck for the Presidency with Jean-Luc Mélenchon coming up on the rails. To add to the tension, Le Pen has promised to shut France's borders to get to grips with frenzied immigration. Aside from this, Eurozone inflation data is due on Wednesday, and we'll get German and EU manufacturing PMIs on Friday. That should be enough to keep the Euro busy but perhaps not enough to break it out of its current ranges.

Higher UK inflation boosted the Pound last week but it gave up some of those gains before Thursday's Bank Holiday close. The UK data diary in this foreshortened week is pretty quiet but Friday's UK retail sales numbers will liven things before the weekend.

The Aussie Dollar was boosted last week by very positive employment data. A gain of 60,900 jobs in March trounced the forecast of roughly 20,000. That was helped by positive Chinese trade data - China is Australia's number one export market. The Aussie Dollar could tread water for most of the week, as the minutes from the last RBA meeting is the only notable news to be expected.

And The Metro is reporting about two intact Easter eggs going on display which are from the 1920s. I am mightily impressed; my children's eggs never made it past Easter Monday....and that's if we remembered to hide some.

Short Jokes

Two cows are in a field and one says, "Mooooooooooo"

The other one says, "That was what I was going to say."

Two cows are in a field and one says, "It's hot isn't it."

The other one says, "Blimey, a talking cow."

Two cows are in a field and one says, "Aren't you worried about this Mad Cow disease going around?"

The other cow says, "It doesn't bother me. I'm a hovercraft!''

I met a bloke yesterday who kept shouting about architectural elements of castles. I think he had Turrets Syndrome

What do you call a Russian tyrant with asthma? Vlad the inhaler.

Tomorrow is International Jamaican Hairstyle Day......I'm dreading it.

I have a new hobby. I like to play chess with the old men in the park although sometimes it's hard to find 32 of them.

USDJPY – Looks To Recover Further Higher

USDJPY - The pair rejected lower prices to close higher on Monday leaving risk of more gains on the cards. On the downside, support comes in at the 108.50 level where a break if seen will aim at the 108.00 level. A cut through here will turn focus to the 107.50 level and possibly lower towards the 107.00 level. On the upside, resistance resides at the 109.50 level. Further out, we envisage a possible move towards the 110.00 level. Further out, resistance resides at the 110.50 level with a turn above here aiming at the 111.00 level. On the whole, USDJPY looks to recover further.

Euro Quiet, Markets Eye CPI

EUR/USD is unchanged in the Tuesday session, as the pair trades at 1.0650. There are no eurozone events on the schedule. In the US, there are two key releases – Building Permits and Housing Starts. On Wednesday, the eurozone releases Final CPI.

It's been a quiet start for the euro this week. European markets were closed for Easter Monday, and the euro has shown little movement on Tuesday. The markets are awaiting the release of Eurozone Final CPI for March. CPI has improved over six straight months, and the February reading of 2.0% was noteworthy as it reached the ECB inflation target. This strong figure has raised speculation that if inflation levels continue to move higher, the ECB may have to consider tightening policy in order to curb inflation. However, the markets are expecting the March reading to drop to 1.5%, which would allow the ECB to hold its monetary course. The ECB's asset-purchase program is scheduled to remain in place until December, although the central bank could opt to bring up that date or taper the program if growth and inflation numbers in the eurozone are unexpectedly strong. There are also political considerations at play, as the ECB is reluctant to make any significant monetary moves with upcoming elections in France and Germany.

In the US, consumer indicators wrapped up last week on a sour note. CPI declined 0.3%, and Core CPI dropped 0.1%, as both indicators missed their estimates. Consumer spending was no better, as Retail Sales and Core Retail Sales also missed estimates with readings of 0.2% and 0.0%, respectively. Earlier in the week, UoM Consumer Sentiment improved to 98.0, beating expectations and hitting a 3-month high.What is unusual is this data is that consumer confidence levels improved in March, yet consumer spending declined. The US consumer behavior continues to be marked by a “hard/soft discrepancy”, as confidence levels (“soft data”), has not translated into actual spending numbers (“hard data”). The odds of a June rate hike from the Fed has fallen to 46%, down from 64% earlier in April. Janet Yellen & C0. will likely want to see stronger inflation numbers before pressing the rate trigger.

Market Update – European Session: Pending UK PM Statement Stirs Up A Quiet EU Session

Notes/Observations

Quiet European session; Focus turning to 1st round of the French election on Sunday

UK PM to make statement at 06:15 ET/10:15 GMT (no details) but rampant speculation of 'big news'

Fed Vice Chair Fischer clarified again the Fed putting its focus on controlling volatility when reducing the size of its balance sheet

Overnight:

Asia:

China's Mar Property Prices improve, defy curbs, further tightening expected

Japan nominated Goshi Kataoka and Hitoshi Suzuki to BOJ board; will replace BOJ dissenters Sato and Kiuchi (**Note: Appointment suugests that the Abe's government wants to keep the current unprecedented stimulus program in place)

RBA Apr Minutes: Developments in the labour and housing markets warranted careful monitoring over coming months

Europe:

Turkey President Erdogan: European Union should go ahead and make its decision on Turkey; Turkey could hold referendum on suspending EU accession talks if needed

Americas:

Treasury Sec Mnuchin: timeline to get tax reform by Aug is "highly aggressive to not realistic at this point"; schedule has been slowed by the healthcare bill passage problems

Fed Vice Chairman Fischer: Reduction in size of our balance sheet that has taken place so far is that we appear less likely to face major market disturbances now than we did in the case of the taper tantrum

Energy:

EIA forecasts May total shale regions oil production at 5.19M bpd, +123K bbd m/m (vs +109K bpd rise in April)

Economic Data

(DK) Denmark Mar PPI M/M: -0.9% v +0.3% prior; Y/Y: 4.3% v 4.1% prior

Fixed Income Issuance:

(ES) Spain Debt Agency (Tesoro) sold total €1.55B vs. €1.0-2.0B indicated range in 3-month and 9-month Bills

(ID) Indonesia sold total IDR3.47T in 2-year,4-year,7-year and 15-year Project-based Sukuk (PBS)

(SK) Slovakia Debt Agency (Ardal) sold total €310.5M in 2026 and 2031 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Index snapshot (as of 10:00 GMT)

Indices [Stoxx50 -0.6% at 3,429, FTSE -1.1% at 7,249, DAX -0.3% at 12,070, CAC-40 -0.9% at 5,025, IBEX-35 -0.6% at 10,266, FTSE MIB -0.8% at 19,621, SMI -0.5% at 8,589, S&P 500 Futures -0.2%]

Market Focal Points/Key Themes: European equity indices are trading sharply lower in the morning session after a 4-day holiday weekend, as China markets also end the session lower overnight; Further geopolitical tensions adding pressure to the markets amid North Korea concerns and as the French presidential race tightens; Banking stocks trading generally lower adding weight to the indices with shares of BNP Paribas, Deutsche Bank, and SocGen trading notably lower in the Eurostoxx; Energy, commodity and mining stocks all weighing heavily in the FTSE 100 as both copper and oil prices trade sharply lower intraday ahead of API stockpile data. In large M&A news, Post Holdings in the US confirmed to acquire Weetabix for £1.4B.

Upcoming scheduled US earnings (pre-market) include Bank of America, Comerica, GNC Holdings, Goldman Sachs, WW Grainger, Harley Davidson, Johnson & Johnson, Lincoln Electric Holdings, Omnicom Group, Progressive Corp, ProLogis, Regions Financial, Charles Schwab, Synovus Financial, and UnitedHealth Group.

Equities (as of 09:50 GMT)

Consumer Discretionary: [Casino Guichard CO.FR -2.0% (Q1 sales), Hennes & Mauritz HMB.SE -0.5% (March sales)]

Consumer Staples: [Refresco Gerber RFRG.NL +2.4% (PAI said to consider raising bid to ~€20/shr)]

Financials: [Gam Holding GAM.CH -1.2% (Q1 AUM)] - Healthcare: [Circassia CIR.UK -2.2% (Top-Line Results from House Dust Mite Allergy Field Study did not meet primary endpoint)]

Speakers

IMF chief Lagarde reiterated call that Euro Area needed a common finance minister. Reform of euro area remains incomplete as all budgetary measures still taken at national level

Swiss Govt: SNB is independent; currency purchases not aimed at devaluing CHF currency (Swiss Franc) to gain export advantage. Reiterated view that CHF currency remains over-valued

Sweden Fin Min Andersson: Govt considering a sovereign wealth fund as a way of solving its illiquid bond market problem. Ready to take more measures over housing market if needed

Sweden govt present Spring Budget raised both 2017 and 2018 GDP growth forecasts. Forecasted 2017 budget surplus at 0.3% of GDP and 2018 at 0.6% surplus.

Bank of Spain (BOS): Feb Bad loans at 9.1%

Japan Fin Min Aso: Japan and US agreed to combat unfair trade practices - comments alongside US VP Pence

BOJ reportedly considering a slight cut to its FY17/18 inflation estimate of 1.5%

Australia PM Turnbull: To introduce stricter rules on working visas. Our reforms will have a simple focus: Australian jobs and Australian values S&P affirmed Japan's sovereign rating at A+; outlook stable

UAE Energy Min Al Mazrouei reiterated view that compliance between both OPEC and non-OPEC members was improving month by month

Saudi Arabia Feb oil production at 10.011M v 9.748M bpd prior. On Apr 12th OPEC Mar Monthly Report showed Saudi Arabia Mar production at 9.90M vs. 10.01M bpd m/m (Feb)

Fixed Income

Bund futures trade at 163.57 up 3 ticks trading mid range ahead of a busy data week. Futures look to 163.82 initially, with a break back above targeting 163.99 followed by 164.20. A reversal targets 163.41 former high followed by 163.18.

Gilt futures trade at 128.73 up 16 ticks trading approaching 129.00 on risk aversion flows. Support moves to 128.56 followed by 128.24 then 127.94. Continuation higher targets 128.96 followed by 129.24. Short Sterling curve trades flat with Jun17Jun18 trading steady at 9.5bp choice.

Tuesday's liquidity report showed Monday's excess liquidity fell to €1.587T a fall of €9B from €1.596T prior. Use of the marginal lending facility rose to €721M from €271M prior.

Corporate issuance saw just $800M come to market via a sole issuer in a light day, with activity expected to pick up today, following the long weekend.

Currencies

FX markets were little changed but the USD remained facing headwinds following the recent string of soft economic data.

USD/JPY began the session back above the 109 level aided by comments from US Treasury Sec Mnuchin suggesting that the US remained committed to its strong USD long-term strategy.Reports circulated that BOJ was considering a slight cut to its FY17/18 inflation estimate of 1.5% at its next policy decision on Apr 27th. The EUR/USD steady in the mid-1.06 area. Focus turning to 1st round of the French election on Sunday

GBP/USD initially hit 3-year highs as the pair tested above the 1.26 level. GBP was softer after PM Theresa May would make a statement (no dteails). The rumor mill went into high gear with suggestions of snap elections or that PM might step down due to health concerns. Dealers noted that the suggested 10:15 GMT time slot was historically used for most serious moments. Pair tested below 1.2550 just ahead of the NY morning.

Looking Ahead

(UK) House of Commons reconvenes after Easter Recess

05.30 (UK) Weekly John Lewis LFL sales data

05:30 (EU) ECB allotment in 7-Day Main Refinancing Tender

05:30 (HU) Hungary Debt Agency (AKK) to sell 3-month Bills

05:30 (NL) Netherlands Debt Agency (DSTA) to sell up to €2-4B in 3-month and 6-month bills

06:00 (IL) Israel to sell 2020, 2021, 2025, 2027 and 2045 bonds

06:15 (UK) PM Theresa May to make statement

06:30 (EU) ESM to sell €1.5B in 6-month Bills

06:45 (US) Daily Libor Fixing

07:00 (BR) Brazil Central Bank (BCB) Apr COPOM Minutes

07:45 (US) Weekly Goldman Economist Chain Store Sales

08:00 (BR) Brazil CONAB Report

08:00 (IS) Iceland Mar Unemployment Rate: No est v 2.9% prior

08:00 (RU) Russia announces weekly OFZ bond auction

08:15 (UK) Baltic Dry Bulk Index

08:30 (US) Mar Housing Starts: 1.25Me v 1.288M prior; Building Permits: 1.25Me v 1.213M prior

08:30 (CA) Canada Feb Int'l Securities Transactions (CAD): No est v 6.2B prior

08:55 (US) Weekly Redbook Sales

08:50 (FR) France Debt Agency (AFT) to sell combined €5.1-6.3B in 3-month, 6-month and 12-month BTF Bills

09:00 (BE) Belgium Feb Trade Balance: No est v -€1.6B prior

09:00 (CA) Canada Mar Existing Home Sales M/M: No est v 5.2% prior

09:00 (NZ) Fonterra Global Dairy Trade Auction

09:00 (US) Fed's George (non-voter)

09:30 (UK) Chancellor Hammond in House of Commons

09:15 (US) Mar Industrial Production M/M: 0.4%e v 0.0% prior; Capacity Utilization: 76.1%e v 75.4% prior, Manufacturing Production: 0.1%e v 0.5% prior

09:30 (EU) ECB announces Covered-Bond Purchases

10:30 (CA) Canada to sell 3-month, 6-month and 12-motn Bills

11:00 (BR) Brazil to sell I/L 2022, 2026, 2035 and 2055 Bonds

11:30 (US) Treasury to sell 4-Week Bills

16:30 (US) Weekly API Oil Inventories

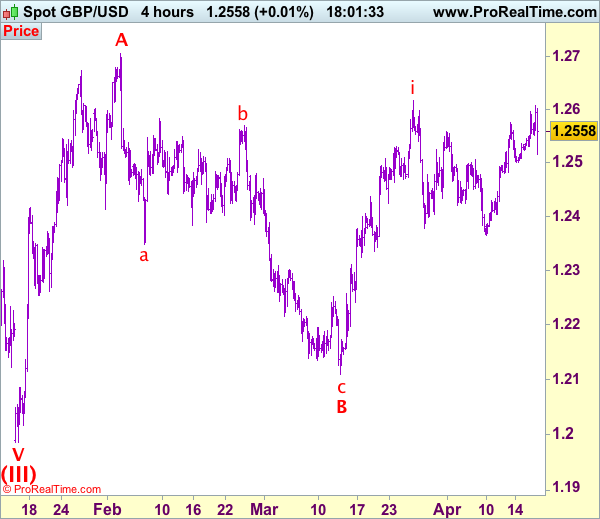

Trade Idea: GBP/JPY – Buy at 136.00

GBP/JPY - 136.75

Recent wave: Medium term low formed at 120.50 and (A)-(B)-(C) major correction has commenced with (A) leg ended at 148.45, hence wave (B) is unfolding for retreat to 131.00-10.

Trend: Near term down

New strategy :

Buy at 136.00, Target: 138.00, Stop: 135.40

Position: -

Target: -

Stop:-

Sterling found good support at 135.60 early last week and staged a strong rebound from there, suggesting a temporary low has been formed there and consolidation with mild upside bias is seen for this move to bring retracement of recent decline, above resistance at 137.30-35 would add credence to this view, then further subsequent gain to 138.00 and possibly test of resistance at 138.25 would be seen, however, near term overbought condition should limit upside to resistance at 138.70 and price should falter well below resistance at 139.00.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.

On the downside, although initial pullback to 136.00-10 cannot be ruled out, reckon 135.70-75 would contain downside and bring another rise later. Only below said support at 135.60 would abort and signal recent decline has resumed, then further fall to 135.00, then 134.40-50 would follow.

Asia’s Equity Mixed Bag As GBP Stay’s Away From May

The Nikkei bucks the trend Australian and China indices wilt.

Another game of two halves in Asia today albeit in still subdued post-Easter trading. Treasury Secretary Mnuchin's strong dollar comments overnight saw U.S. equities rally along with the greenback. A perceived lightning in regional tensions in Asia should have been the green light for a sea of green today, but only Japan and South Korea's Kospi, in particular, managed to benefit from the good news.

As we roll into a returning Europe, the signals don't look so rosy. Europe continues to be weighed down by French election anxiety and the U.K Prime Minister, Theresa May, has announced she will make a statement outside Number 10 at 1015 GMT this morning. There is no visibility on what it will be about, but the FTSE doesn't like it, down 1 % to February lows in early trading.

Nikkei 225

The Japan 225 had a good day as a stronger USD/JPY, and lower regional tensions boosted exporter stocks on the Nikkei. It has given part of this back late in the afternoon as Europe opens in the red.

Support lies at 18,280, the year's lows with the 200-day moving average behind that at 18,020.

Resistance rests at 18,6250 and then 18,955.

ASX 200

The Australia market returned to work today, but there was no Easter cheer as the index proceeded directly South. The RBA minutes highlighted worries about an overheated housing market and a weak labour market. Iron ore and rebar futures fell again in China marking a miserable week for commodities. Unsurprisingly, resource companies and banks were the hardest hit in Australia today.

The ASX is testing support at 5825 with a break opening up a move to the 5675/5700 region on the charts. This marks the March lows and the 100-day moving average.

Resistance lies at 5890 and then the month's highs at 5950.

HONG KONG

The Hang Seng also returned to work today, but again sentiment locally overrode, and geopolitical feel good factor, falling over 1.4%. Although yesterday's China data was good, the feeling persists in the local market that yesterday may be the best of it for a while and that growth will slow over the remainder of the year as Government stimulus runs its course.

Worries also persist around property cooling measures on the mainland and PBOC tightening going forward. Transport and property companies fell today.

The Hang Seng finishes on its lows in an ominous technical picture. Support is here at 23,820 initially with a break implying a move to the 23,400 area.

Resistance is well defined on the daily charts at 24470 followed by the years high at 24,580.

FRANCE 40

France has also been 'an vacance,' and its return has not been pretty, down 1.1 % in early trade. Saturday's first round voting gets murkier the closer it gets. Investors are saying 'zut alor' and running for the door. With four candidates from all extremes of the political spectrum running neck and neck now, the old adage that France changes by revolution, not evolution, has gained more poignancy.

The CAC-40 is testing trendline support as I write at 5000. This line goes all the way back to December last year. The next support being 4930, the March lows.

Resistance intra-day sits at 5100 and then the year's highs at 5150.

UK 100

The FTSE 100 is down 1% in early trading along with a sell-off in GBP/USD which has fallen from 1.2600 to 1.2535. PM May is due to make an unexpected statement on the steps of Downing Street at 1015 GMT. There is no official word about what it is about, but the rumour mill is suggesting SHE MAY CALL A SNAP ELECTION. Machiavelli couldn't have written this. Traders should stay tuned to their news feeds for developments.

The FTSE is testing support at 7250 as I write with the next support at 7195. This is the February low and the 100-day moving average.

Resistance above sits at 7350 and 7410.

GBP/USD

Not an index but worth a mention in dispatches as the situation develops. GBP/USD has sold off 70 points from 1.2600 to around 1.2530 on speculation about the May announcement.

GBP/USD has support at 1.2500 and then 1.2430 the 100-day moving average. Resistance lies at 1.2610 the overnight high and the 200-day moving average. Technicals may not mean a lot if an election is indeed announced.

Summary

There are a lot of moving parts this morning as Europe (and Britain) return from Easter holidays. The UK announcement at 1015 GMT could be particularly significant with stocks and currencies moving on headlines rather than data this morning.

Trade Idea: GBP/USD – Buy at 1.2400

AUD/USD – 1.2554

Recent wave: Wave 5 ended at 1.1081 and major correction has commenced for fall to 0.7000 and then towards 0.6500-10

Trend: Near term up

New strategy :

Buy at 1.2400, Target: 1.2600, Stop: 1.2340

Position: -

Target: -

Stop:-

Cable found decent demand at 1.2109 earlier last month and staged a strong rebound from there since, suggesting the wave c as well as larger degree wave B has ended there, hence impulsive wave C has commenced from there with wave i of C ended at 1.2616, follow by a corruption back to 1.2365 (either end of wave ii or first a-b-c of ii). Although sterling staged a strong rebound from there, break of 1.2616 is needed to confirm upmove has resumed and extend gain to 1.2660-70, then 1.2706 (wave A top) but reckon upside would be limited to 1.2770-80.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has ended at 1.7192, the subsequent selloff is the larger degree wave (C) which is still unfolding with minor wave (III) of larger degree wave 3 ended at 1.1986, hence wave (IV) correction is in progress which could either be a triangle wave (IV) of a complex formation but upside should be limited to 1.3500 and price should falter well below 1.4000, bring another decline in wave (V) of 3 for weakness to 1.1500, then 1.1200.

On the downside, whilst initial pullback to 1.2495-00 is likely, reckon downside would be limited to 1.2440-50 and 1.2395-00 should attract renewed buying interest and bring another rally later. Only a break of said support at 1.2365 would abort and shift risk to downside for a deeper wave ii correction later.

Daily Technical Analysis: USD/JPY In Downtrend But Possible Inverted Head And Shoulders At 118.70

The USD/JPY has been dropping substantially but at this point it seems that a dip might have found the support around L4/ATR low confluence at 108.36. At this point the pair is still in downtrend but watch for any signs of possible rejection around 108.70 as the rejection might form inverted head and shoulders where the bottom of the right shoulder could form a rally towards POC. The POC for short trades is 109.30-40 (D H4, W H3, Bearish order block) and rejection should target 108.70. H1 momentum below 108.60 aims for 108.35.

GOLD Bullish Pause, SILVER Bullish Pause, Crude Oil Breaks Rising Trendline.

GOLD Bullish Pause.

Gold has broken the key resistance area 1263. This validates a bullish reversal pattern with an upside potential at 1337. The hourly support at 1263 (previous resistance) has induced some buying interest. Another hourly support lies at 1260 (rising trendline). An hourly resistance can now be found at 1280 (intraday high).

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

SILVER Bullish pause.

Silver is rising sharply above 18.49, validating the recent technical improvements. Strong resistance is given at a distance at 19.00 (09/11/2017 high). Key support is given at 17.74 (10/04/2017 low) then 16.82 (15/03/2017 low).

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

Crude Oil Breaks rising trendline.

Crude oil has pulled-back after its recent sharp rise. Support can be located at 50.71 (08/02/2017 low). Hourly resistance can be located at 54 (07/04/2017 high then strong resistance stands at 55.24 03/01/2017 high).

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 24.82 (13/11/2002) while resistance can now be found at 55.24 (03/01/2017 high).

EUR/CHF Moving Sideways, EUR/CHF Moving Sideways, EUR/GBP Declining Toward The Support At 0.8450.

EUR/CHF Moving sideways.

EUR/CHF remains weak as can be seen by the succession of lower highs and lower lows. Hourly resistances can be found at 1.0691 (07/04/2017 high). The medium-term pattern suggests us to see continued bearish pressures towards key support that can be found at 1.0623 (24/06/2016 low). Expected to see further decline.

In the longer term, the technical structure is mixed. Resistance can be found at 1.1200 (04/02/2015 high). Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

EUR/CHF Moving sideways.

EUR/CHF remains weak as can be seen by the succession of lower highs and lower lows. Hourly resistances can be found at 1.0691 (07/04/2017 high). The medium-term pattern suggests us to see continued bearish pressures towards key support that can be found at 1.0623 (24/06/2016 low). Expected to see further decline.

In the longer term, the technical structure is mixed. Resistance can be found at 1.1200 (04/02/2015 high). Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

EUR/GBP Declining toward the support at 0.8450.

EUR/GBP has broken the key supports area between 0.8787 (13/03/2017) high and 0.8484 (31/03/2017 low). The short-term technical structure is negative as long as the hourly resistance at 0.8596 holds. Another resistance can be found at 0.8645. An hourly support lies at 0.8450 (03/01/2017 low). Expected to show continued weakness.

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.