Sample Category Title

EURAUD Technical Analysis

On April 11/2017 bears pushed EURAUD lower and it seems lower prices are yet to come in the following trading sessions. At the current moment, bias remains bearish and traders should look for any possible selling opportunities.

1 Hour Chart Bearish Pattern: Bearish pattern is visible on short term analysis but traders need to be patient and wait for price to retrace higher towards the BC 0.50% Fib. retracement level and wait for the point D (blue pattern) to enter the possible reversal zone (blue box) to trigger sells. We do not recommend buying the pair to the proposed selling zone but rather advise to wait for price to enter the possible reversal zone and look for selling opportunities. There is also support/resistance levels near the BC 0.50% Fib. level so we should expect a reaction/reversal in price action in this area. Only time will tell what EURAUD will do but for now bias remains bearish.

If looking to sell EURAUD traders should wait for price to move above the BC 0.50% and watch for price to stall in the possible reversal zone (blue box) for any selling opportunities. Waiting for price to move above the BC 0.50% Fib. retracement level will offer a better risk/reward trade setup. A break above the point B high will invalidate the bearish pattern. If the pair moves lower from the possible reversal zone traders should place targets below the AB 2.24% level.

Of course, like any strategy/technique, there will be times when the strategy/technique fails so proper money/risk management should always be used on every trade.

CAC Under Pressure Ahead of French Election

The CAC 40 has dropped to the 5000 level, as the index is trading at 5,007.80 in Tuesday trade. On the release front, there are no events out of the eurozone. On Wednesday, the eurozone releases Final CPI, with the indicator expected to soften to 1.5 percent.

After an Easter holiday on Monday, the CEC has resumed trade on Tuesday. The CAC has posted losses, and briefly dropped below the symbolic 5000 level. Investors are keeping a keen eye on the French presidential election, with the first round of voting on April 23. The race remains extremely tight, with centrist Emmanuel Macron and far-right candidate Marine Le Pen tied at 22 percent. They are followed by Francois Fillon at 21% and Jean-Luc Melenchon at 18 percent. If Macron and Le Pen reach the second round, Macron is expected to win decisively by a margin of 64-36. With only a few days to go before the vote, any change in polling numbers could have a significant impact on the stock markets. Another factor weighing on the stock market is the crisis over North Korea, as the US continues to warn North Korea that that it will not allow the rogue country to continue to test ballistic missiles. US vice-president Mike Pence is in Japan for talks with Japanese officials, with trade issues and North Korea high on the agenda.

The eurozone won't release its first event this week until Wednesday, with the release of Eurozone Final CPI for March. CPI has improved over six straight months, and the February reading of 2.0% was noteworthy as it reached the ECB inflation target. This strong figure has raised speculation that if inflation levels continue to move higher, the ECB may have to consider tightening policy in order to curb inflation. However, the markets are expecting the March reading to drop to 1.5%, which would allow the ECB to hold its monetary course. The ECB's asset-purchase program is scheduled to remain in place until December, although the central bank could opt to bring up that date or taper the program if growth and inflation numbers in the eurozone are unexpectedly strong. There are also political considerations at play, as the ECB is reluctant to make any significant monetary moves with upcoming elections in France and Germany.

French Election Monitor: Mélenchon Could Enter Second Election Round in May

The most notable development since French Election Monitor #1 has been the stellar rise of left-wing candidate Mélenchon in the polls after a strong performance in the TV debates (see Chart 1). Ahead of the first election round this Sunday, the race between the four leading candidates Marine Le Pen, Emmanuel Macron, Francois Fillon and Jean- Luc Mélenchon remains wide open and the outcome is likely to be tight. Although a runoff on 7 May between Le Pen and Macron still seems to be the most likely outcome according to the polls, Mélenchon entering the second round now cannot be ruled out.

Should Mélenchon reach the run-off, opinion polls show that he could win against Fillon or Le Pen (see Chart 2). With his wish to renegotiate EU treaties and hold a subsequent EU exit referendum on the result as well as ending the independence of the ECB, his programme displays a similar EU-sceptic and anti-globalisation stance to Le Pen's. He rejects free trade agreements and the rules of the Stability and Growth Pact and advocates an alliance of southern European countries to fight austerity. Furthermore, Mélenchon wants the Bank of France to buy public debt and repeal the El Khomri labour market reforms. A potential run-off between the two EU-sceptics Mélenchon and Le Pen seems to be the biggest risk-scenario in the market at the moment and as a result we already saw the France 10Y spread to Germany widen to just a few bps from the highs in February (see Chart 3). However, even if Mélenchon should win the presidency, he faces the same parliamentary hurdles as Le Pen in implementing his programme or holding a referendum, as his party is unlikely to obtain sufficient seats for a majority.

Should he qualify for the second round, Macron is still seen winning the presidency irrespective of his opponent, according to the latest poll. However, the indecision of his supporters (only 72% are certain of their choice) and the expected lower participation rate (68%), due to widespread dissatisfaction with the established political class, could decrease his chances on election day and benefit Le Pen, whose supporters remain the most certain of their choice (89%). However, our base case remains that she will not win the presidency.

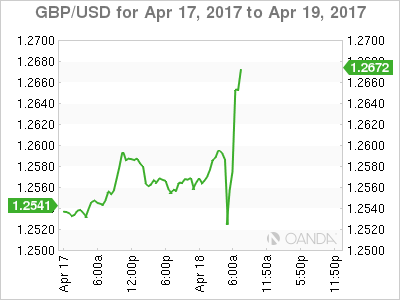

UK Snap General Election Shocker Revives British Pound

Sterling was back in fashion on Tuesday, with the GBPUSD lurching towards 1.2675 following Theresa May's unexpected announcement that there will be a snap general election on 8 June. This bombshell development has offered Sterling a solid boost, with markets now evaluating what impact this may have on the Brexit negotiations. The fact that May stated that she wants an election to ensure strong leadership that will deliver on Brexit may quell some related jitters in the short term.

While short-term bulls may reign as a result of this fresh development, longer-term bears could exploit the potential political uncertainty to drag Sterling lower. A very strong likelihood remains that Sterling sensitivity will intensify moving forward, with a vote in parliament on Wednesday to decide whether or not the election will take place acting as the first test.

From a technical standpoint, the GBPUSD is bullish on the daily charts. The upside momentum could propel prices towards the 1.2775 resistance level.

Trump rally put to the test

The ongoing anxiety surrounding geopolitical tensions across the globe has left investors jittery during Tuesday's trading session, with stock markets struggling to maintain gains. Asian shares were mostly lower amid cautious trading, with the sheer lack of appetite for risk exposing European equities to steep losses. Although Wall Street received a boost on Monday as participants redirected their attention to first quarter corporate earnings, the upside may be limited by a return of risk aversion. With confidence slowly deteriorating over Trump's ability to implement the phenomenal tax cuts and infrastructure spending he promised during his election campaign, the Trump rally could be put to test moving forward.

Dollar Trumped again

The Greenback was dealt a crippling blow last week after Donald Trump repeated his now iconic statement that the Dollar was "getting too strong". Dollar bears exploited the confusion created to attack the prices further, after Trump decided not to name China a currency manipulator. With Trump's comments on how he "liked" the low interest rates policy displaying a noticeable campaign U-turn and compounding the uncertainty, the Dollar could be in store for further punishment. The visible fact that the Greenback has found itself on the back foot every time Trump has shared his bearish thoughts on the Dollar does raise questions over whether the currency remains dictated by him in the short to medium term. From a technical standpoint, the Dollar Index has found itself pressured on the daily charts, with a break below 100.00 opening a path towards 99.50.

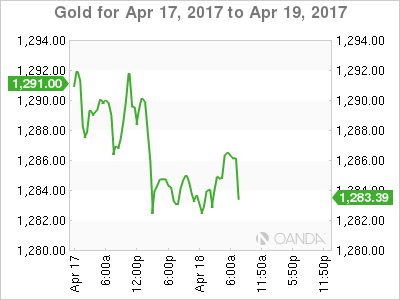

Commodity spotlight - Gold

The geopolitical tensions across the globe and political risks may continue to support Gold moving forward. Although prices edged lower on Monday, the metal remains bullish on the daily charts with buyers potentially exploiting the technical correction. From a technical standpoint, bulls remain in firm control above $1260 with $1300 acting as the next major level of interest.

GBP/USD Nears Mid-Term Major Resistance After Theresa May Calls Early General Election

The UK Prime Minister made a speech today around 11:15 am at 10 Downing Street.

She stated that the Cabinet had agreed to call an early general election, to be held on June 8. The UK government is determined to execute Brexit process and negotiation with the EU, and this is the right decision for the country's interests. The post-Brexit vote economic indicators have shown that the UK economy is more solid than expected to withstand Brexit impact.

However, some other political parties are still against Brexit and the deal the UK reach with the EU, such as the Labour, Liberal and Scottish National Party. Although the Conservative Party is the majority in the Parliament. Nevertheless, the unity of other opposing parties will outnumber the Conservative, and hence it will weaken the UK government's negotiation position with the EU.

In order to remove the political opposition and eliminate uncertainties, Theresa May attempts to increase the number of Conservative MPs by moving forward the general election.

GBP/USD saw a dramatic reversal this morning ahead of the speech due to the uncertainties. It surged around 110 points after the speech with strong bullish momentum on realization of speculation, breaking the psychological resistance level at 1.2600.

The bulls are currently edging up, with an attempt to test the next significant resistance level at 1.2700. However, the level is the mid-term major resistance level, where there is heavy pressure, be aware that the bullish momentum is likely to be restrained while nearing the level.

GBP/USD has been trading above the downside uptrend line support since April 10.

The resistance level is at 1.2680, followed by 1.2700.

The support line is at 1.2650, followed by 1.2620.

DAX Dips on North Korea, French Election Concerns

The DAX has posted slight losses on Tuesday, as the index trades at 12,025.00. On the release front, there are no events in the eurozone. On Wednesday, the eurozone releases Final CPI, with the indicator expected to soften to 1.5 percent.

The DAX was closed on Monday for Easter, and has resumed trade on Tuesday with slight losses. Investors are keeping a close eye on the French presidential election, with the first round of voting slated for April 23. The race remains extremely tight, with centrist Emmanuel Macron and far-right candidate Marine Le Pen tied at 22 percent. They are followed by Francois Fillon at 21% and Jean-Luc Melenchon at 18 percent. If Macron and Le Pen reach the second round, Macron is expected to win decisively by a margin of 64-36. With only a few days to go before the vote, any change in poll numbers could have a significant impact on the stock markets. Another factor weighing on the markets is the crisis over North Korea, as the US continues to warn North Korea that that it will not allow the rogue country to continue to test ballistic missiles. US vice-president Mike Pence is in Japan for talks with Japanese officials, with trade issues and North Korea high on the agenda.

The eurozone won't release its first event this week until Wednesday, with the release of Eurozone Final CPI for March. CPI has improved over six straight months, and the February reading of 2.0% was noteworthy as it reached the ECB inflation target. This strong figure has raised speculation that if inflation levels continue to move higher, the ECB may have to consider tightening policy in order to curb inflation. However, the markets are expecting the March reading to drop to 1.5%, which would allow the ECB to hold its monetary course. The ECB's asset-purchase program is scheduled to remain in place until December, although the central bank could opt to bring up that date or taper the program if growth and inflation numbers in the eurozone are unexpectedly strong. There are also political considerations at play, as the ECB is reluctant to make any significant monetary moves with upcoming elections in France and Germany.

RBA Minutes Reflect The Meeting Statement

Overnight, the Reserve Bank of Australia released the minutes from its latest policy meeting. The minutes reflected more or less the meeting statement, highlighting the softness in labor market indicators, and that the recently announced supervisory measures with regards to lending could ease financial stability risks.

As we noted when we had the meeting, this suggests to us that once these measures take effect, the Bank would be more flexible to cut rates again if needed without being concerned that its actions would amplify risks to the economy. However, following the remarkable jobs report for March, released after the meeting, we don't think that the Bank will proceed with something like that at its upcoming gathering, scheduled on the 2nd of May.

AUD/USD reacted little at the time the minutes came out. The pair has been trading south ahead of the release, and continued drifting lower in the aftermath. It started sliding after it hit resistance near the 0.7600 (R1) barrier and the 50% retracement level of the March 21st – April 12th downtrend. The decline was stopped by the 0.7555 (S1) support, where a decisive dip is possible to carry more bearish extensions, perhaps towards our next support of 0.7515 (S2) marked by the inside swing high of the 11th of April.

With regards to the bigger picture of the pair, the price structure on the daily chart suggests a neutral outlook. The pair has been oscillating within a wide range between the 0.7160 and 0.7800 zones for more than a year.

US Treasury Secretary helps the dollar recover somewhat

On Monday, the US dollar recovered some of its latest losses against the yen after the US Treasury Secretary Steven Mnuchin told the Financial Times that a strong dollar would be a good thing in the long term. His remarks come a few days after US President Trump jawboned the currency by saying that it is “getting too strong”. However, Mnuchin said that Trump's remarks were about the short-term and agreed that this is hurting exports.

USD/JPY traded higher after it hit support near the 108.15 (S2) level, and broke back above 108.80 (S1). The recovery was stopped slightly below our resistance of 109.30 (R1). Even if the pair continues to trade higher for a while, we would tread any further recovery as a corrective move and we expect it to remain limited. Tensions over North Korea are far from diminished and as such, headlines that could heighten these concerns further may cause the pair to turn down again. A dip back below 108.80 (S1) may confirm the case and is possible to pave the way for another test near 108.15 (S2). The nervousness over the economic dialog between the US and Japan, as well as the upcoming French presidential elections could also keep any USD/JPY rebounds limited.

Today:

From the US we get industrial production for March. Expectations are for industrial output to have accelerated to +0.5% mom from +0.1% mom the previous month, which could support somewhat the greenback. However, for the reasons we just outlined, we expect any possible USD-strength from this data point to remain short-lived, especially against safe havens like the yen. We also get building permits and housing starts, both for March.

From New Zealand, the GDT (Global Dairy Trade) index is coming out, though no forecast is available. Although this could impact the Kiwi at the release, we believe that NZD-traders have their gaze locked on the nation's CPI data for Q1 due out on Thursday. As such, any reaction on the GDT index could stay limited.

As for the speakers, we have one scheduled on the agenda: Kansas City Fed President Esther George.

AUD/USD

Support: 0.7555 (S1), 0.7515 (S2), 0.7475 (S3)

Resistance: 0.7600 (R1), 0.7625 (R2), 0.7650 (R3)

USD/JPY

Support: 108.80 (S1), 108.15 (S2), 107.70 (S3)

Resistance: 109.30 (R1), 110.00 (R2), 110.75 (R3)

Daily Technical Analysis: EUR/USD Breaks Resistance And Continues Retracement To 1.0750

Currency pair EUR/USD

The EUR/USD broke above the resistance trend line (dotted red) as expected which could signal a larger retracement within wave 2 (brown). Price could head back to 1.0750-1.0775 at the 50-61.8% Fibonacci levels.

The EUR/USD break above the resistance trend line (dotted orange) which could trigger the development of an ABC (purple) zigzag.

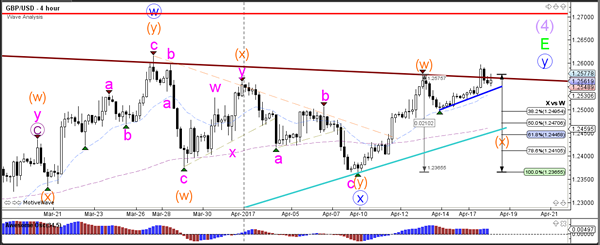

Currency pair GBP/USD

The GBP/USD is challenging the resistance trend line (brown) which is a bounce or break decision zone. A bearish bounce could price fall towards the Fibonacci levels of wave X (orange) whereas a bullish breakout could see price complete wave Y (blue).

The GBP/USD is testing the Fibonacci levels of potential wave B (pink). A break above the 138.2% Fibonacci level would invalidate the wave B (pink).

Currency pair USD/JPY

The USD/JPY is building a potential wave 4 correction (orange), which would become invalid if price retraced above the bottom of wave 1 (red line).

The USD/JPY could be building an ABC (purple) zigzag correction towards the Fibonacci levels of wave 4 (orange). A break below the support trend line (blue) could indicate the completion of that wave 4 (orange).

U.K’s May Calls June Election

Tuesday April 18: Five things the markets are talking about

While many markets were closed for Easter Monday, the pace of new economic data releases picks up today, especially in the U.S.

Gains are expected for the U.S industrial production report (+0.5%e vs. +0.0%) despite last month's poor weather having pulled down factory hours. Housing starts and permits have been good of late, but the March outlook is to be mixed with a dip expected for starts, but continued strength for permits.

The first round of the French presidential elections is this Sunday (April 23) and any anxiety surrounding the outcome is likely to push market risk sentiment higher closer to the end of this week.

Marine Le Pen is expected to be one of the top two to make it to round two, but markets will be content to a certain extent if the socially liberal and pro-business Emmanuel Macron, and not the far-left anti-austerity candidate Jean-Luc Melenchon, is to be her opponent in the run-off vote in a fortnight (May 7).

However, if Melenchon makes it into the next round with Le Pen, markets will be gripped by a new source of fear, bigger than Brexit!

Elsewhere, U.K Prime Minister Theresa calls a snap general election for June 8.

1. Stocks see Red

Markets in Sydney, Hong Kong and Europe have dropped after the Easter holidays, as investors caught up with global markets that have been weighed down by geopolitical concerns.

Japan's Topix has advanced +0.4% overnight on the back of a weaker yen (¥108.88) after U.S Treasury Secretary Mnuchin said the dollar's strength is “a good thing.” In Indonesia, the benchmark jumped +0.7%, while South Korea's Kospi added +0.1%.

In Australia, a selloff in iron ore has pulled down commodity producers. The S&P/ASX 200 fell -0.9%, the most thus far in April. Raw-materials shares in the benchmark index have retreated -4.5% over the past two sessions, the biggest drop for that period in almost a year.

In Hong Kong, stocks played catch up after the four-day long weekend. The Hang Seng lost -1.1% and the Hang Seng China Enterprises Index slumped -1.4%, its lowest close in nearly three months. In China, the Shanghai Composite lost -0.8%, after plummeting -1.6% in the previous two-sessions.

In Europe, equity indices are trading sharply lower after the holiday weekend. Banking stocks are trading generally lower weighing the Eurostoxx, while energy, commodity and mining stocks are all weighing heavily in the FTSE 100.

U.S stocks are set to open in the red (-0.2%).

Indices: Stoxx50 -0.6% at 3,429, FTSE -1.1% at 7,249, DAX -0.3% at 12,070, CAC-40 -0.9% at 5,025, IBEX-35 -0.6% at 10,266, FTSE MIB -0.8% at 19,621, SMI -0.5% at 8,589, S&P 500 Futures -0.2%

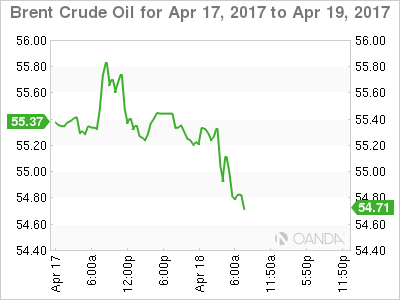

2. Oil under pressure from a hike in U.S output, gold holding firm

Crude prices fall in thin trade overnight as a U.S. government report indicated a rise in production.

Brent crude futures are down -4c at +$55.32. Yesterday they ended a quiet down -53c, after rising the three previous weeks. U.S. West Texas Intermediate (WTI) crude futures are also down -4c at +$52.61 a barrel. On Monday, they settled down -53c at +$52.65 a barrel.

U.S data yesterday showed that domestic shale production for May is likely to post the biggest monthly gain in more than two-years as producers step up the pace of drilling with oil prices holding above the psychological +$50 a barrel.

The EIA expects the month of May's output to rise by +123k bpd to +5.19m bpd. If so, it will be the biggest monthly increase since February 2015 and the highest monthly production level since November 2015.

Note: OPEC is due to meet on May 25 to weigh an extension of output cuts beyond June to alleviate a glut that has depressed prices for nearly three-years.

Gold prices held firm overnight (unchanged at +$1,284.56 per ounce) supported by geopolitical tensions over North Korea and market uncertainty re-French presidential election after falling from a five-month high on Monday (+$1,295.80) on a firmer dollar.

Elsewhere, Iron ore futures on the Dalian exchange dropped -4%, after sliding almost -3% yesterday.

3. French/Bund spread remains wide on election jitters

The French Presidential forecast remains too close for comfort. This morning's Ifop poll puts Macron and Le Pen each on +23%, just +3% ahead of Fillon and the far-left Melenchon.

The spread between French and German 10-year bond yields – another indicator of market worries – ranged from +0.767 bps as markets opened, to +0.72 bps ahead of the U.S open. In November, the spread was as little as +0.22 bps.

Elsewhere, the yield on U.S 10's fell -1 bps to +2.24%, while the Aussie benchmark yield backed up +1 bps to +2.49%.

4. Pound collapse on May's impromptu announcement

The pound fell sharply against the USD (£1.2525) and EUR (€0.8490) on the news that U.K PM Theresa May would make an unexpected statement at 11:15 a.m. GMT. It has since taken back some of those earlier losses after PM Theresa May called a June 8 snap election (see below).

EUR/USD will be driven this week by French political development ahead of Sunday's first round of presidential elections. Currently, the EUR is up +0.06% outright (€$1.0650), but stress relating to the French election remains clear in other parts of the currency market.

Note: One-month Euro-dollar risk reversals, which measure the cost to investors of protecting against a sudden decline in the single unit, touched -4.3, the most extreme reading in six-years.

U.S Treasury Secretary Mnuchin has also talked up the USD after Trump's remarks last week that the greenback has gotten “too strong,” noting that “strength of dollar over the long term is a positive.” USD/JPY is trading at ¥108.90 ahead of the U.S open.

5. PM Theresa calls snap election

PM Theresa May has called a snap general election for June 8. Her obvious aim is to strengthen her position going into talks on leaving the European Union. Technically, she seeks a direct mandate to take the country through the “divorce” with the E.U.

Note: Two polls over the weekend put the Conservatives +21 points ahead of Labour, a lead that is likely to greatly increase.

In Brussels May's announcement is likely to be seen as merely adding to the unpredictability of relations with the U.K since last years Brexit referendum.

Stocks, Dollar And Yields Under Geopolitical And Economic Pressure

Global equities and the 'mighty' dollar have again dipped overnight while U.S Treasury yields have fallen to new five-month lows after soft U.S data on Friday hurts investor sentiment already in distress by worries over North Korea and upcoming French elections.

Note: U.S. retail sales dropped more than expected in March (+0.0% vs. +0.2%) while annual core inflation slowed to +2.0%, the smallest advance since November 2015, from +2.2% in Feb.

A raft of Chinese economic data (see below) beat market expectations, but did not produce a notable market reactions, as investors had been already optimistic following a recent string of positive China numbers.

In Turkey, President Erdogan snatched a victory in a referendum Sunday to grant him sweeping powers in the biggest overhaul of modern Turkish politics.

Note: Markets in Australia, New Zealand and Hong Kong, as well as most European exchanges, are closed for Easter Monday.

1. Global equities under pressure

Stock markets across Asia ended mostly lower overnight, as China's securities regulator urged tighter supervision of listed companies, while geopolitical tensions in Korea continued to discourage investors from buying.

Japan's Nikkei Stock Average opened lower, but later recouped the declines to end up +0.1%, snapping a four-session losing streak – the yen (¥108.76) spiked to new yearly highs (¥108.13).

In China, investor market sentiment has worsened over an escalating regulatory crackdown on stock manipulation, despite stronger-than-expected economic data for the Q1. The Shanghai Composite Index ended down -0.7%, while the Shenzhen Composite Index lost -1.4%.

Elsewhere, Singapore's Straits Times Index lost -0.9%, while Taiwan's Taiex ended down -0.2%.

In Turkey, the Borsa Istanbul 100 Index climbed +0.6% – the highest level in more than two-years after President Erodgan's referendum victory yesterday (see below).

In Europe, markets remain closed due to Easter Monday holiday.

U.S stocks are set to open in the 'red' (-0.1%).

2. Oil falls after failed North Korean missile test, U.S rig count gains

Crude oil prices are again under pressure overnight in quiet trading after the Easter break on signs that the U.S continues to add output, undermining OPEC efforts to support prices, and as the market digest North Korea's failed missile launch yesterday.

Ahead of the U.S open, Brent crude futures are down -56c at +$55.33, while West Texas Intermediate (WTI) crude futures are down -51c at +$52.67 a barrel.

Note: Both benchmarks last week rose for a third consecutive week, with Brent adding +1.2% over the four days (Good Friday holiday) while WTI was up +1.8%.

Last Thursday's Baker Hughes (energy services) report indicated that drillers added +11 oil rigs in the week to April 13, bringing the count up to 683, highest in about two-years.

Note: The latest EIA report shows that U.S crude oil production has climbed to +9.24m barrels per day (bpd), making it the world's third-largest producer after Russia and Saudi Arabia.

Gold prices hit a five-month high overnight (+$1,295.42 an ounce) as the dollar weakened with investors taking refuge in safe-haven assets in the wake of rising geopolitical tensions over North Korea.

The 'yellow' metal last week rose +2.5%, posting its biggest weekly gain in 10-months.

3. Global yield curves flatten

Last Friday's disappointing U.S data (retails sales and CPI) has helped to drive down the U.S 10-year Treasury yield to +2.20%, its lowest level since mid-Nov.

In March, U.S 10's were trading atop of +2.6% on expectations of a Trump stimulus package. However, with Trump expected to struggle to push any tax cuts and fiscal spending programs through Congress has supported the markets unwinding of the “Trump” trade.

Current Fed fund futures for June are now pricing in less than a +50% chance of a rate hike in its June 13-14 meeting for the first time in about a month.

Elsewhere, geopolitical and French Presidential election risks have seen the yield on 10-year Bunds fall over -33 bps from its mid-March peak of +0.51% to +0.18%.

The gap between French and German 10-year borrowing costs, an indicator of concerns over the election, is at +71.4 bps, +4 points off one-month highs hit earlier last week.

4. Dollar under geopolitical pressure

The Turkish Lira (TRY) has rallied over +2.4% outright in the wake of this weekend's referendum to expand the executive powers of President Erdogan.

While the “Yes” vote was deemed victorious, the margin of victory at 51.3% vs. 48.7% opposed was well below the 55% mandate predicted by Erdogan and is expected to be challenged by the opposition.

Note: Under upcoming constitutional changes, the winner of next election in 2019 will “gain full control of the government, ending the current parliamentary system, which treated office of the president as a role without full executive authority.”

The 'mighty' USD is trading a tad softer across the board after last week's release of March CPI and retail sales data both underwhelmed. Fixed income dealers are paring back the probability of another Fed rate hike in June.

The EUR is trading +0.2% higher at €1.0630 in quiet trading with most European markets remaining closed for Easter Monday holiday. USD/JPY is trading softer, down -0.3% at ¥108.32. Expect geopolitical worries to continue to support the yen's strength.

5. China data beats expectations

Over the weekend, China economic data offered some positive surprises – GDP, industrial output, and retail sales for Q1 all topped consensus to hit multi-month rates of growth.

Note: The world's second-biggest economy accounted for about one-third of global growth last year and, given the strong Q1, is on track to contribute at least as much this year.

Digging deeper, Q1 GDP y/y rallied to a six-quarter high of +6.9%. Consumption accounted for +77.2% of that growth, up from +64.6% in 2016. Fixed asset investment rose over +10% as property investment value rose +9%, sales value rose +25% and construction up +11%.

Industrial output growth was similarly impressive, rising at the fastest pace in three-years. Power generation was up +7%, while coal and steel output were both up +2% despite the recent production curbs. While March retail sales y/y was +10.9% vs. +9.7%e (3-month high).