Sample Category Title

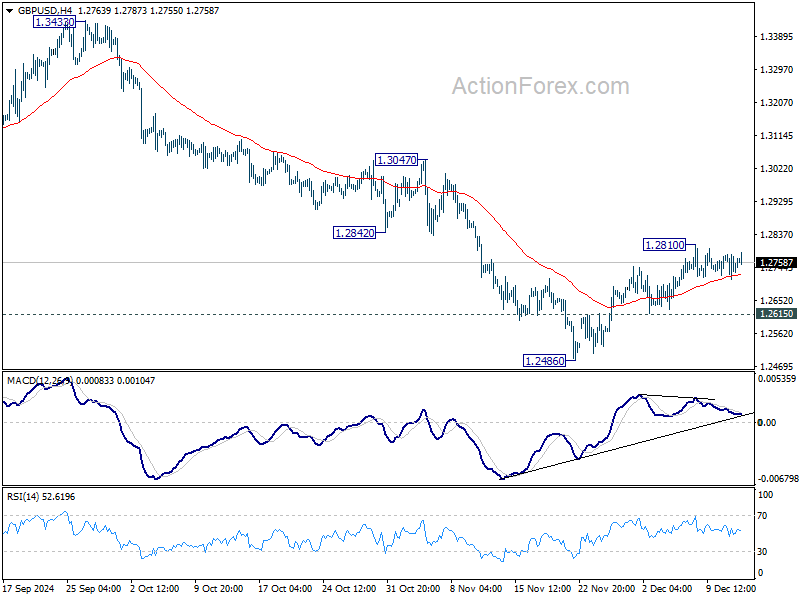

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2715; (P) 1.2749; (R1) 1.2784; More...

No change in GBP/USD's outlook as consolidations continue below 1.2810 temporary top. Rebound from 1.2486 short term bottom could still extend higher. But outlook will stay bearish as long as 55 D EMA (now at 1.2834) holds. On the downside, below 1.2615 minor support will bring retest of 1.2486 first. Firm break there will target 1.2298 cluster support zone. However, sustained break of 55 D EMA will argue that the near term trend has reversed, and targets 1.3047 resistance for confirmation.

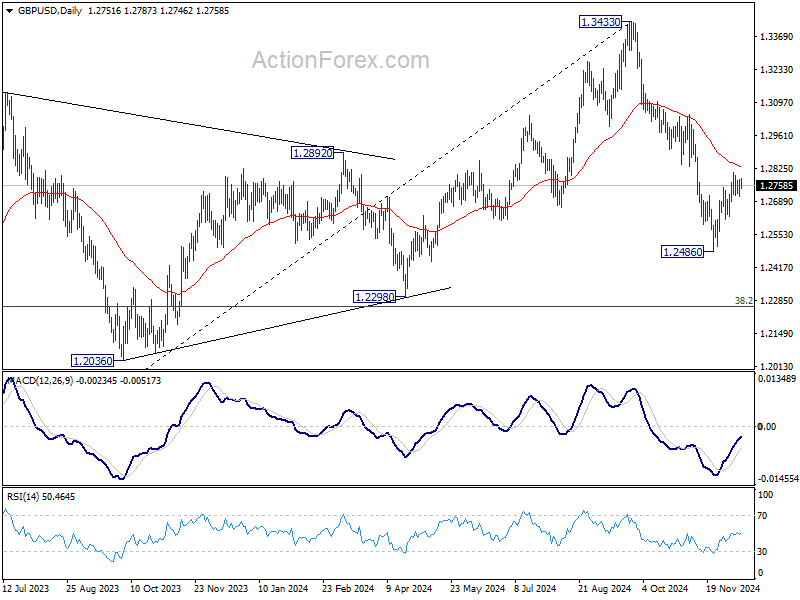

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern.

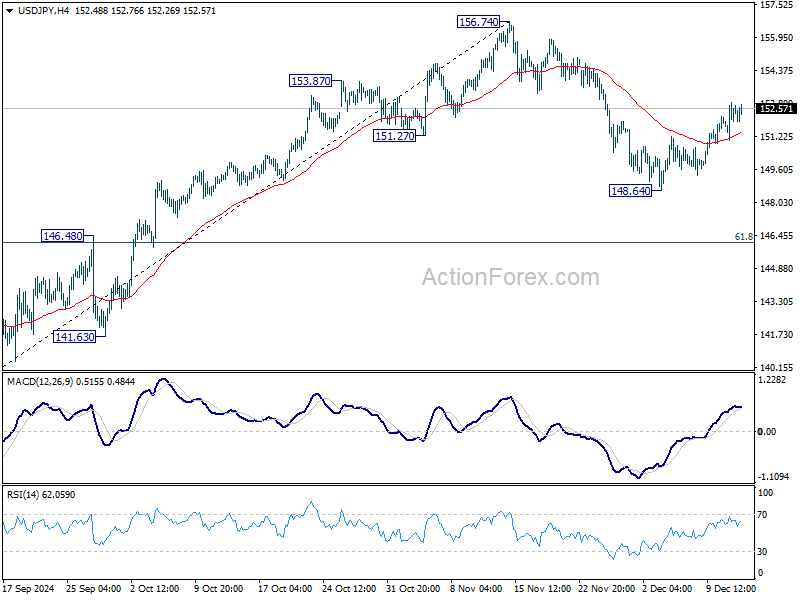

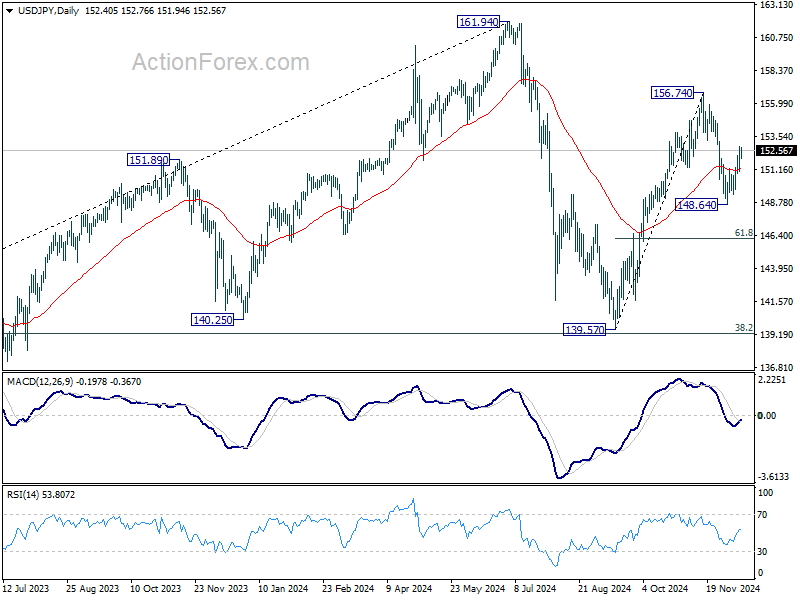

USD/JPY Daily Outlook

Daily Pivots: (S1) 151.37; (P) 152.11; (R1) 153.20; More...

Intraday bias in USD/JPY stays on the upside for retesting 156.74 high. Current development suggests that rise from 139.57 might still be in progress and break of 156.74 will confirm resumption. For now, this will be the favored case as long as 148.64 support holds, in case of retreat.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

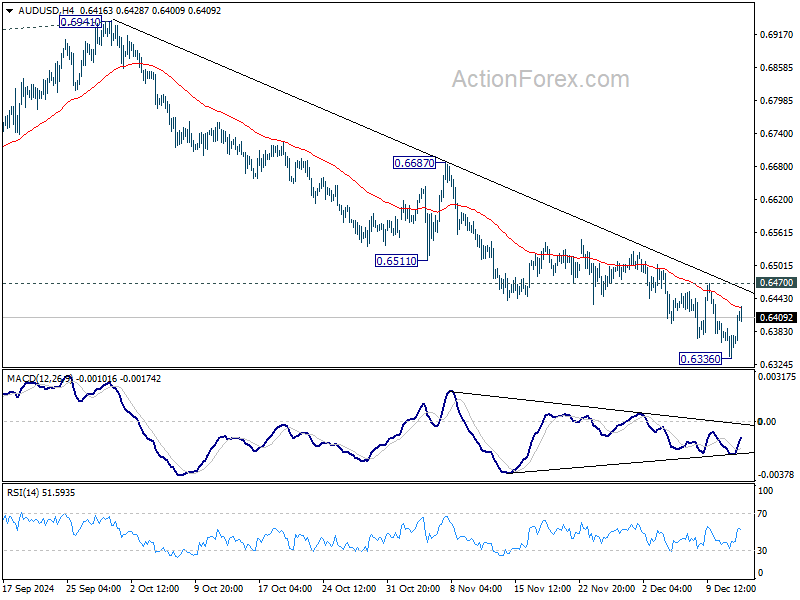

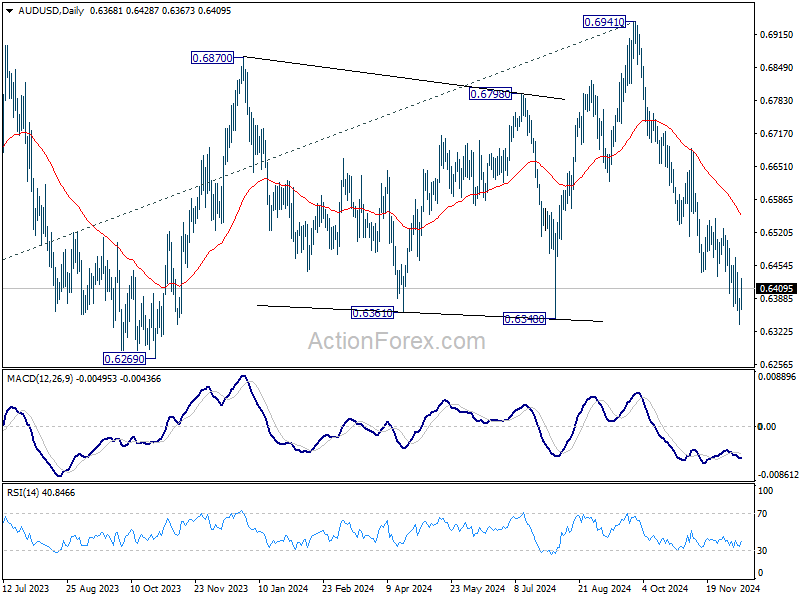

AUD/USD Daily Report

Daily Pivots: (S1) 0.6341; (P) 0.6365; (R1) 0.6393; More...

Intraday bias in AUD/USD is turned neutral again with current recovery. Some consolidations would be seen above 0.6336 temporary low. But outlook will stay bearish as long as 55 D EMA (now at 0.6554) holds. Break of 0.6336 will resume the fall from 0.6941 to 0.6269 support next.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006. More sideway trading could be seen above 0.6169, but overall outlook will stay bearish as long as 0.6941 resistance holds. Firm break of 0.6169 will resume the down trend to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next.

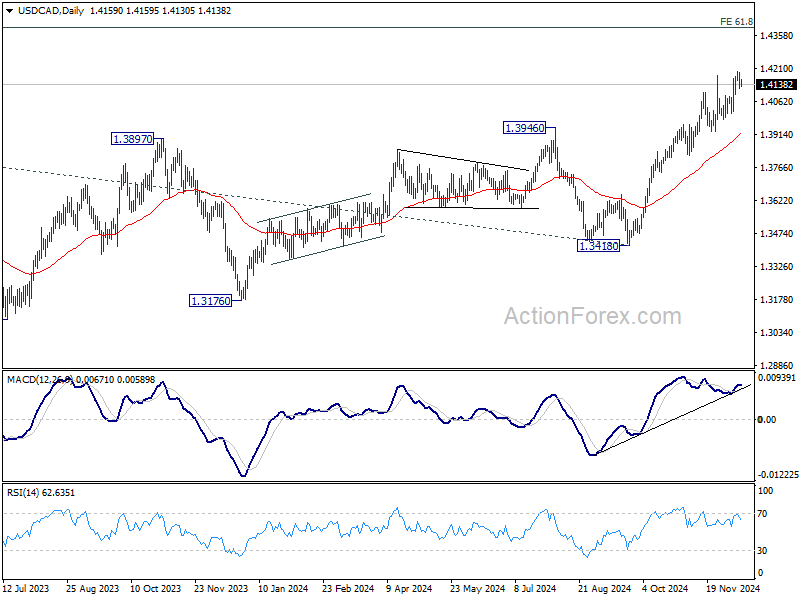

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4121; (P) 1.4158; (R1) 1.4195; More...

Intraday bias in USD/CAD remains neutral for consolidation below 1.4194 temporary top. Outlook will remain bullish as long as 1.4009 support holds. Break of 1.4194 will resume larger up trend to 1.4391 projection level. However, considering bearish divergence condition in 4H MACD, firm break of 1.4009 will indicate short term topping, and turn bias back to the downside for correction to 55 D EMA (now at 1.3925).

In the bigger picture, up trend from 1.2005 (2021) is in progress. Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391. Now, medium term outlook will remain bullish as long as 1.3418 support holds, even in case of deep pullback.

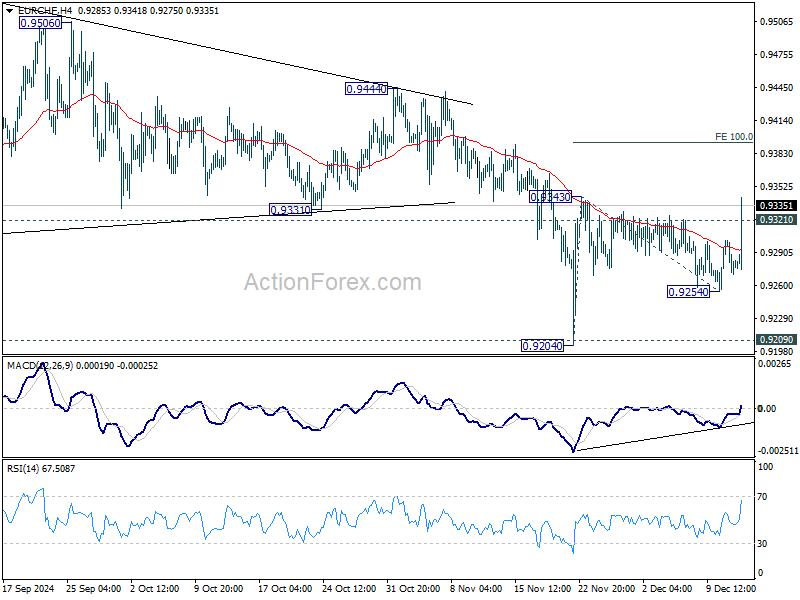

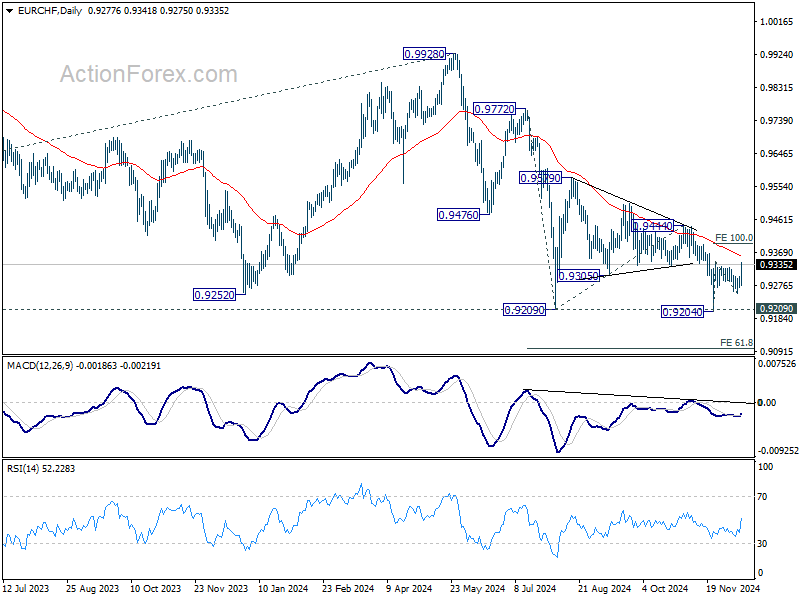

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9267; (P) 0.9286; (R1) 0.9299; More....

EUR/CHF's strong rally and break of 0.9321 minor resistance suggests that rebound from 0.9204 short term bottom is resuming. Intraday bias is back on the upside. Firm break of 0.9343 will target 100% projection of 0.9204 to 0.9343 from 0.9254 at 0.9393 next. For now, risk will stay on the upside as long as 0.9254 support holds, in case of retreat.

In the bigger picture, outlook will stay bearish as long as 0.9444 resistance holds. Decisive break of 0.9209 low will resume long term down trend to 61.8% projection of 0.9772 to 0.9209 from 0.9444 at 0.9096 next.

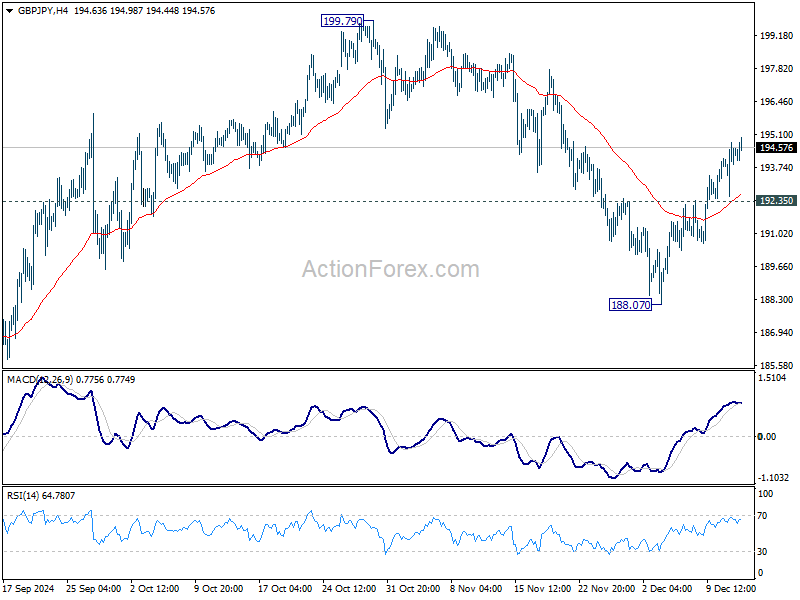

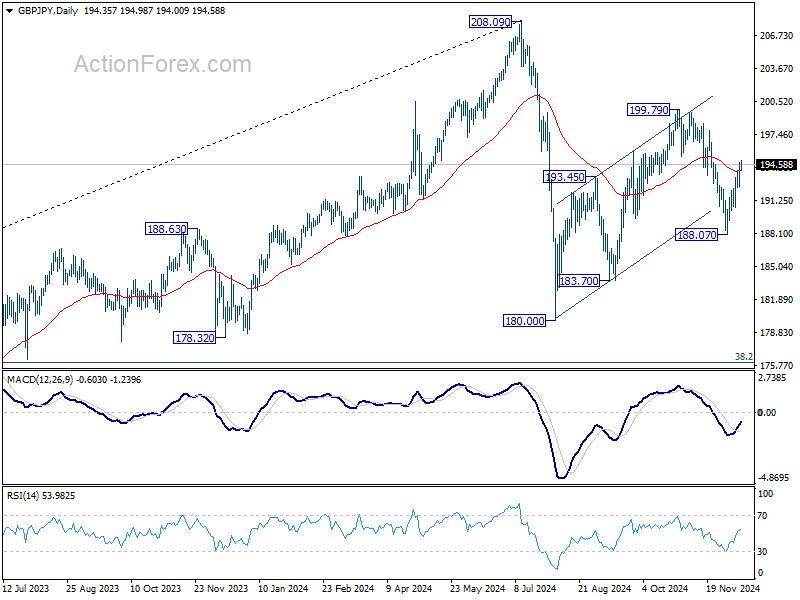

GBP/JPY Daily Outlook

Daily Pivots: (S1) 193.03; (P) 193.92; (R1) 195.31; More...

GBP/JPY's break of 55 D EMA mixes up the original bearish outlook. Intraday bias is now mildly on the upside and further rise could be seen towards 199.79 resistance. On the downside, break of 192.35 support will bring deeper fall back to 188.07.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

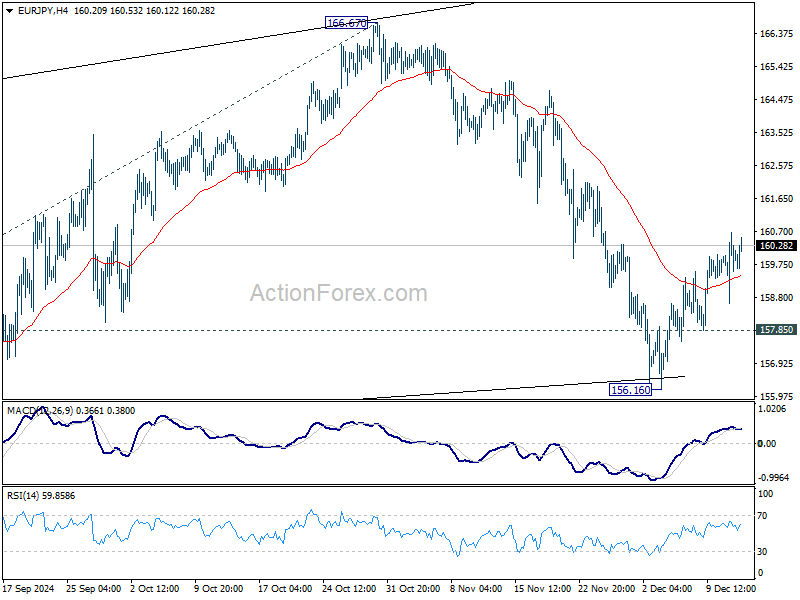

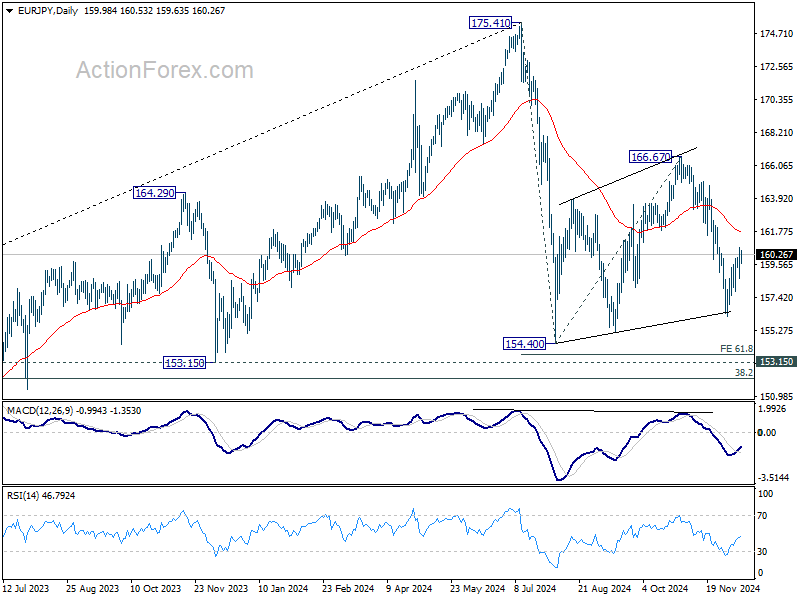

EUR/JPY Daily Outlook

Daily Pivots: (S1) 158.88; (P) 159.79; (R1) 160.93; More...

Outlook in EUR/JPY remains unchanged as rise from 156.16 is seen as a corrective recovery. Further decline is expected as long as 55 D EMA (now at 161.76) holds. On the downside, below 157.85 minor support will bring retest of 156.16 first. Break there will target 154.40 low next.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

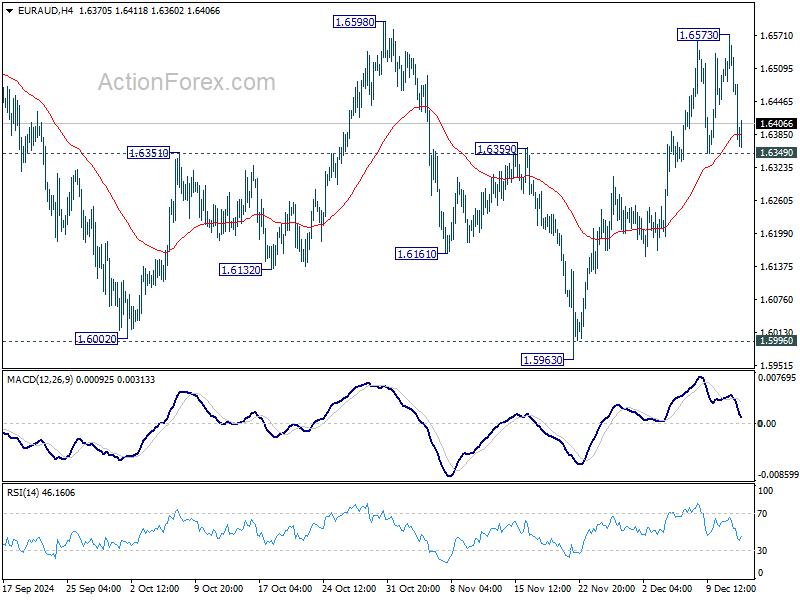

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6436; (P) 1.6506; (R1) 1.6551; More...

Intraday bias in EUR/AUD is turned neutral again with current retreat. But further rally remains in favor as long as 1.6349 support holds. On the upside, decisive break of 1.6598 resistance should confirm that whole fall from 1.7180 has complete with three waves down to 1.5963. Further rise should then be seen to retest 1.7180 next. Nevertheless, firm break of 1.6359 will indicate rejection by 16598, and turn bias back to the downside.

In the bigger picture, EUR/AUD is still holding on to 1.5996 key support despite brief breach. Larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5995 will indicate that such up trend has completed. Deeper decline would be seen to 61.8% retracement of 1.4281 to 1.7180 at 1.5388, even as a correction.

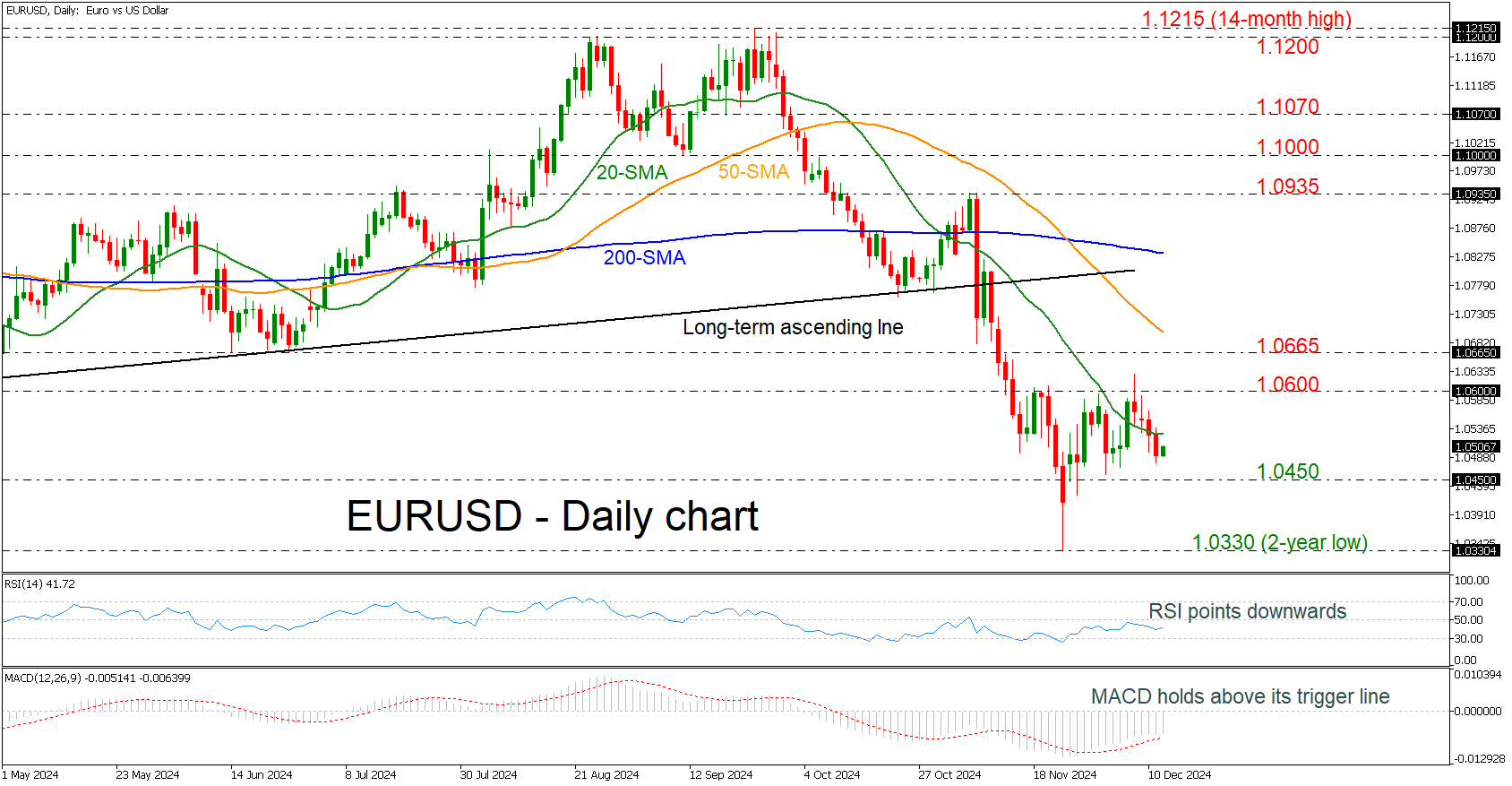

EURUSD Holds Near 1.0500 Again

- EURUSD retains neutral phase in short term

- MACD and RSI extend bearish momentum

EURUSD slides significantly after the failed attempt to surpass the 1.0600 round number and is currently challenging the 1.0500 handle. The pair has remained in a tight range of 1.0450–1.0600 over the last month, with the technical oscillators suggesting more declines. The RSI indicator is falling below the neutral threshold of 50, while the MACD is extending its negative momentum below the zero level.

More downside pressure could see traders revisiting the 1.0450 barrier ahead of the two-year low of 1.0330. Even lower, the pair may have a pause near November 2022’s low of 1.0220.

On the other hand, a climb above the 20-day simple moving average (SMA) at 1.0530 could send traders back to the 1.0600 key level again. If this time the market proves strong enough to break that area, then the next resistance could come from 1.0665.

To conclude, EURUSD has been strongly bearish since it peaked at 1.1215, and only a rally above the 200-day SMA at 1.0830 may switch the outlook to bullish.

SNB cuts by 50bps, projects weaker inflation and modest growth in 2025

SNB took a decisive step by lowering its policy rate by 50 basis points to 0.50%. In its accompanying statement, the central bank highlighted that underlying inflationary pressures have "decreased again" this quarter, warranting the larger-than-expected rate cut. SNB reiterated its commitment to "monitor the situation closely" and stated that it would "adjust its monetary policy if necessary."

The latest conditional inflation forecasts reflect a significantly subdued outlook, even with interest rate down from 1.00% to 0.50%.

For 2025, inflation is now projected at just 0.3%, a notable downgrade from the 0.6% forecast in September. However, the 2026 outlook saw a slight upward revision to 0.8%, from 0.7% previously.

Looking at some details, inflation is expected to decline sharply from 0.7% in Q4 2024 to a low of 0.2% in Q2 2025, before gradually recovering to 0.8% in 2026 and 0.7% in 2027. These figures underscore the SNB’s view of persistent deflationary risks, necessitating its proactive policy stance.

In terms of economic growth, SNB estimates GDP growth for 2024 to come in at around 1%, with a modest pickup to 1-1.5% expected in 2025. Despite this improvement, challenges remain, including slightly rising unemployment and declining utilization of production capacity.