Sample Category Title

Japanese Yen Loses Ground on Shifting Interest Rate Expectations

The Japanese Yen has lost 2.3% against the US dollar since the end of last week, roughly twice as much as the rise in the dollar index against a basket of six developed market currencies. This change is due to a shift in interest rate expectations, with investors increasingly doubting an imminent rate hike in Japan and seeing fewer rate cuts from the Fed next year.

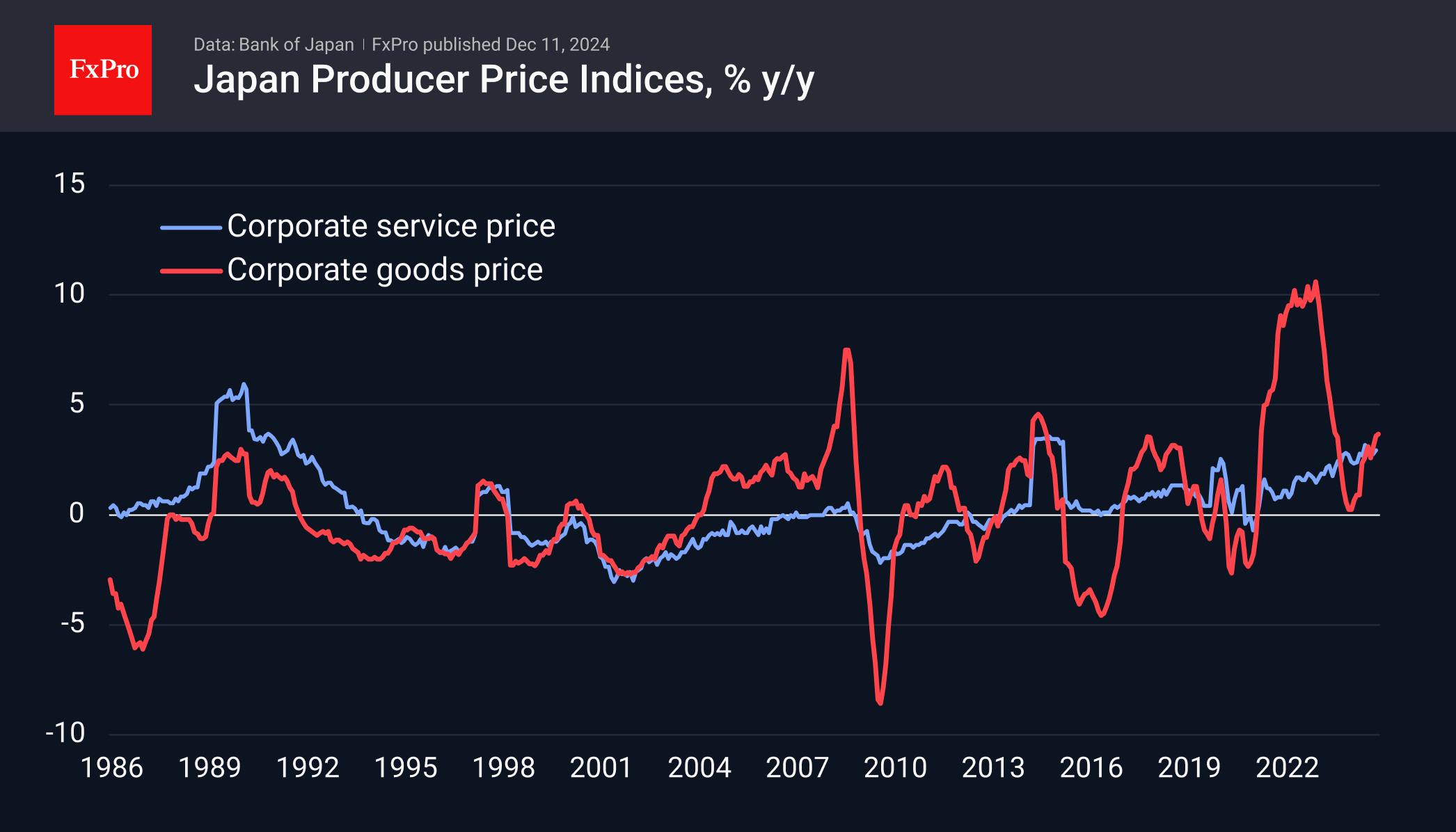

Interestingly, the latest inflation data does not help the Yen. November data showed an acceleration in Japanese business input prices to 3.7% y/y, the highest since the middle of last year. Corporate services price growth (October data) jumped 0.8% m/m to an annualised pace of 2.9%, maintaining levels near 3% y/y since April. These indices are important leading indicators of inflation, pointing to increasing pressure on retail prices and supporting a policy rate hike by the Bank of Japan.

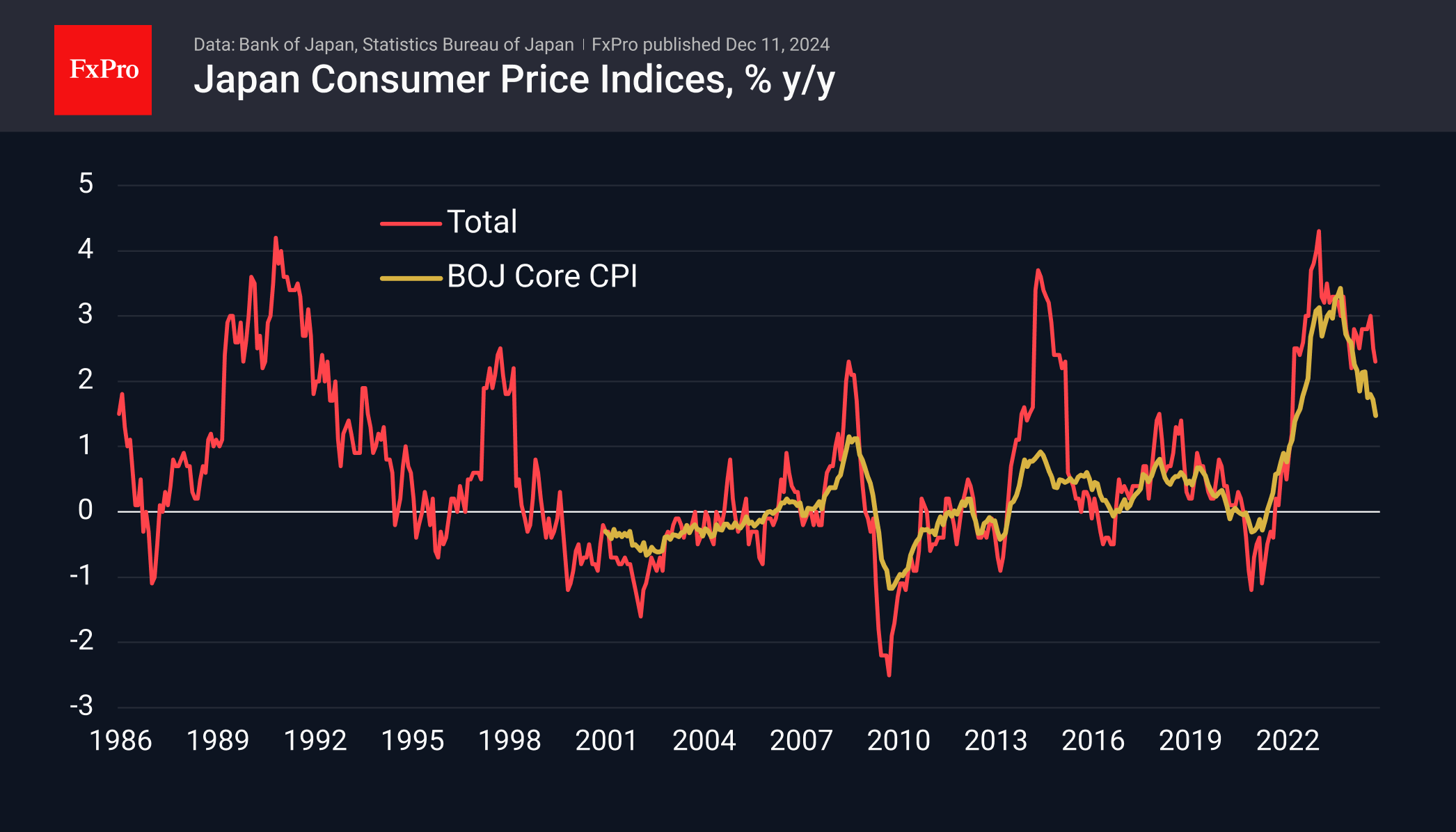

At the same time, the decline in core consumer inflation to 1.5%, as tracked by the BoJ, provides room to delay policy tightening. The BoJ can use this time to assess the economic outlook considering potential trade tariffs from the Trump administration.

For the bond markets, this slowness has the effect of pushing back expectations for a rate hike in Japan from mid-December to the end of January. For currency markets, this puts pressure on the JPY as accelerating inflation that does not lead to a rate hike leads to capital outflows from yen debt markets.

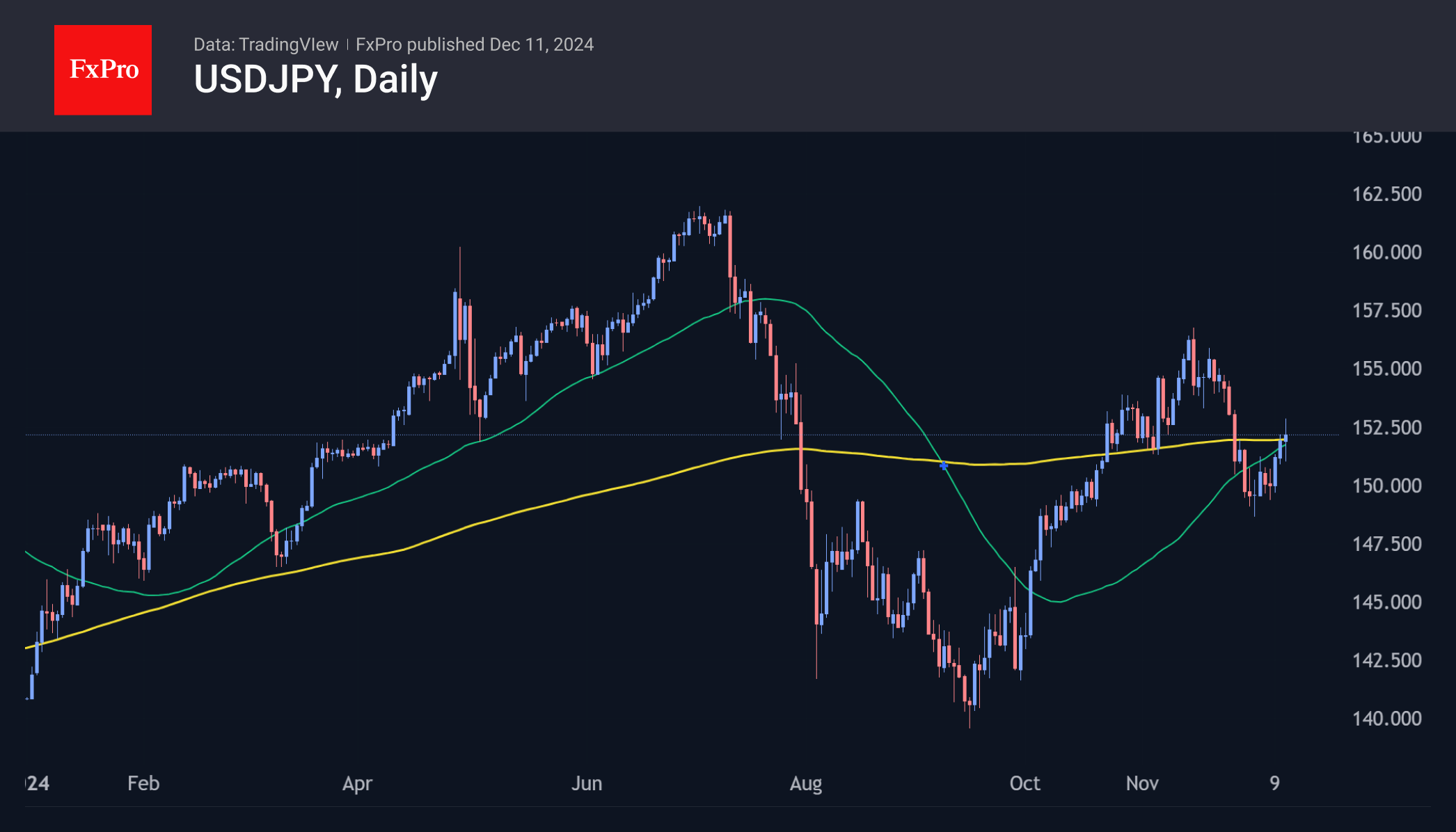

It would not be surprising to see an accelerated rise in the USDJPY. The technical picture has also turned bullish in recent days, as the pair has broken above its 200 and 50-day moving averages. In addition, a “golden cross” is forming as the 50-day is about to cross above the 200-day, which is a strong technical signal for further upside. The USDJPY could potentially reach levels of 156 before the end of the year and exceed 160 in the first quarter of 2025.

Sunset Market Commentary

Markets

Today’s November US CPI inflation numbers convinced final doubters that the Fed would stick to the plan set out in the September dot plot and lower rates by 25 bps at its policy meeting next year. The data printed bang in line with expectations: a 0.3% monthly increase in both headline and core CPI with annual readings respectively rising from 2.6% to 2.7% on a headline level and stabilizing at 3.3% for the core gauge. The stalling disinflation process equally boosts the case for a January pause by the Federal Reserve, awaiting the inauguration of president-elect Trump on January 20. Uncertainty on his future (fiscal) agenda favours erring on the side of keeping some powder dry. Other elements in favour of such scenario are stronger-than-expected growth, enthusiastic survey data since the Republican sweep, rising short term inflation expectations and Fed talk on a gradual approach. The US yield curve bull steepens today with yield changes ranging between -4.2 bps (2-yr) and -0.8 bps (30-yr). The long end of the curve still has an eye on tonight’s $39bn 10-yr Note auction and on tomorrow’s $22bn 30-yr Bond sale. Are investors keen to load up on more US Treasuries at current levels with a potential debt bonanza looming? The US dollar is marginally weaker on a trade-weighted basis. EUR/USD spiked very temporarily towards 1.0540, but is already back at 1.05 in anticipation of a dovish 25 bps rate cut at tomorrow’s ECB meeting. USD/JPY rose from 151.50 to 152.50 before returning some gains after the US CPI report. A Bloomberg report suggesting that BoJ official see a small cost to waiting before raising interest rates caused the initial JPY-weakness. Speculation on a December BoJ rate hike was recently rising following higher inflation & stronger growth numbers and some BoJ talk. At the same time, the article suggested that some aren’t against a rate hike on Friday if it is proposed, adding some ambiguity. USD/CAD tends to weaken after the Bank of Canada’s expected 50 bps rate cut to 3.25%. YtD highs around 1.42 hold and the recent failed test of this resistance area triggers some rebound action lower towards 1.4140. The BoC sees a gradual approach from here if the economy evolves broadly as expected. The central bank will be looking at core inflation to assess the inflation trend after some government tax breaks. BoC governor Macklem labels the US tariff threats as major new uncertainties.

News & Views

Chinese leaders and policymakers are contemplating to allow the yuan to depreciate in 2025, a Reuters exclusive reported citing people with knowledge of the matter. Doing so would mean breaking with the usual policy goal of keeping the exchange rate stable. The shift comes as China braces for US import duties under a second Trump presidency. The president-elect during his campaign threatened with tariffs up to 60% on Chinese imports. Allowing CNY depreciation would blunt some of the impact and protect the one sector (ie export) of the economy that has been doing well. The matter is all the pressing given that Chinese authorities are said to set next year’s growth target in the same ambitious 5% range as this year’s. China’s yuan slid after Reuters ran the report with USD/CNY jumping from the 7.25 area towards 7.275 before paring gains (CNY losses) to 7.264 currently. A source tapped by Reuters said the PBOC has considered the possibility the yuan could drop to USD/CNY 7.5 to counteract any trade shocks. That would be the weakest level since 2007.

Strike 5. OPEC for a fifth straight month slashed its oil demand forecasts for this year and the next. Lowering consumption growth by 210k barrels a day to 1.6mn for 2024 marked the deepest cut so far. Demand growth has been reduced 27% since it started adjusting projections downwardly from July on. For 2025 it reduced growth by 90k barrels a day to 1.4mn. The move “takes into account recently received bearish data” for Q3 including “downward revisions to OECD Americas and OECD Asia Pacific”. Despite the string of cuts, OPEC remains considerably more bullish on oil demand compared to others in the oil industry, including the IEA. OPEC+ last week decided for a third time to postpone the removal of some oil production curbs while also slowing the pace of increases once they start doing so somewhere next year. Oil prices grind higher in choppy trading. Brent currently is sold for $73/b.

Bank of Canada Delivers Another Supersized Cut

The Bank of Canada (BoC) cut its overnight rate by 50 basis points, to 3.25%, while stating that it will continue with Quantitative Tightening (QT).

The bank highlighted that economic growth has been weaker than they expected, stating that "the economy grew by 1% in the third quarter, somewhat below the Bank’s October projection, and the fourth quarter also looks weaker than projected."

Inflation is less of a concern for the central bank, which was made clear when it stated "inflation has been about 2% since the summer, and is expected to average close to the 2% target over the next couple of years."

The bank referenced the confluence of factors that are muddying the outlook. These included the impact of the government's new immigration strategy, new mortgage rules, the GST holiday and one-time payments from governments, and the threat of tariffs.

On the future path of policy, the bank seems more cautious, stating that is has already "reduced the policy rate substantially since June" and that it "will be evaluating the need for further reductions in the policy rate one decision at a time."

Key Implications

The recent rise in the unemployment rate alongside weaker-than-expected GDP was enough to convince the BoC that another supersized rate cut was warranted. We think this misses the forest for the trees. The rise in the unemployment rate is missing the fact that hiring has reaccelerated over the last few months, while underlying growth momentum has been robust with consumer spending driving fundamental demand. Not to mention, the real estate market has caught fire once again.

We don't think the BoC will keep cutting at this current pace. The policy rate is in the bank's 'neutral' range (2.25% to 3.25%), which means it probably thinks its rate is no longer weighing on economic growth. The central bank will also be getting more evidence over the coming months that economic growth is stabilizing around trend. Stronger growth will validate that it can cut at a slower pace. If it doesn't, policy rate differentials with the U.S. will widen even more. And with tariffs potentially coming on Jan. 20th, the combination would likely push the loonie into the mid-60 U.S. cent range.

Australian Dollar Hits Four-Week Low Amid RBA Stance and US Dollar Strength

The AUD/USD pair continues its downward trajectory, reaching a four-week low of 0.6386 on Wednesday. This decline is primarily influenced by the Reserve Bank of Australia's (RBA) decision to maintain interest rates at 4.35% per annum for the ninth consecutive meeting. This decision, which was widely expected, reflects the central bank's cautious approach despite ongoing inflation concerns.

RBA Governor Michelle Bullock emphasised that the central bank's current stance on inflation is deliberate, aiming to signal responsiveness to softening economic indicators. The market currently anticipates a high likelihood of an RBA rate cut in February, with a 63% probability of a 25-basis-point reduction. Expectations are set for further cuts at subsequent meetings through May as investors and analysts factor in potential easing measures.

AUD supporters' focus is shifting towards Thursday's release of Australian employment data, which could provide further clues about the economic outlook and influence RBA policy decisions.

The Australian dollar is also experiencing significant pressure from a strengthening US dollar, which adds to its challenges.

Technical analysis of AUD/USD

H4 chart: the AUD/USD is navigating a wide consolidation range centred around 0.6450. The pair is currently forming a downward movement towards 0.6347. Upon reaching this level, a corrective rise to 0.6450 is expected, potentially testing this resistance from below before possibly initiating a new decline towards 0.6215. This bearish outlook is supported by the MACD indicator, whose signal line is below zero and continues to trend downwards.

H1 chart: the market is actively developing a downward wave towards 0.6347. After hitting this target, a corrective movement towards 0.6450 could occur. The Stochastic oscillator, with its signal line below 50 and moving towards 20, confirms this scenario, indicating the potential for further downward pressure before any corrective rebound.

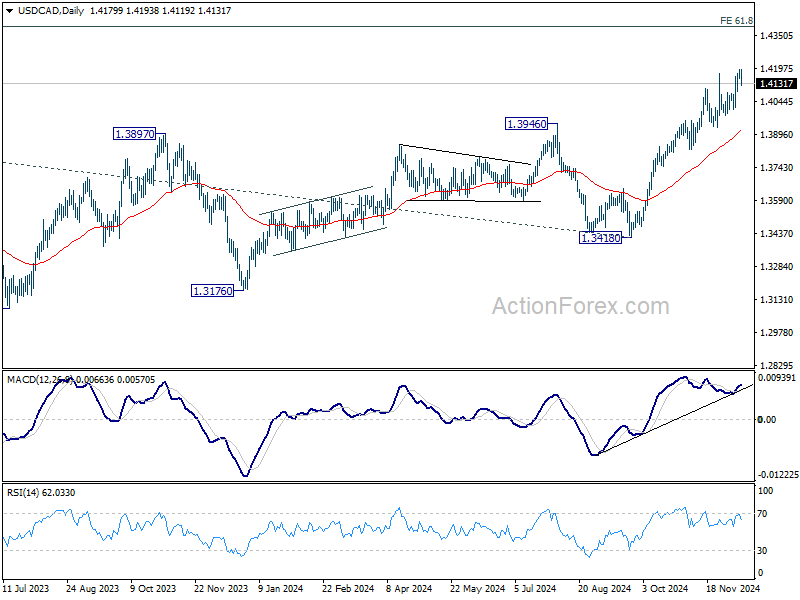

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.4160; (P) 1.4178; (R1) 1.4199; More...

Intraday bias in USD/CAD is turned neutral first with current retreat, and some consolidations would be seen. But outlook will remain bullish as long as 1.4009 support holds. Break of 1.4194 will resume larger up trend to 1.4391 projection level. However, considering bearish divergence condition in 4H MACD, firm break of 1.4009 will indicate short term topping, and turn bias back to the downside for correction to 55 D EMA (now at 1.3916).

In the bigger picture, up trend from 1.2005 (2021) is in progress. Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391. Now, medium term outlook will remain bullish as long as 1.3418 support holds, even in case of deep pullback.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0495; (P) 1.0531; (R1) 1.0565; More...

EUR/USD is staying in range trading and intraday bias remains neutral. On the downside, break of 1.0471 support will suggest that corrective recovery from 1.0330 has completed, and fall from 1.1213 is ready to resume. Intraday bias will be back on the downside for 1.0330 first, and then 61.8% projection of 1.0936 to 1.0330 from 1.0629 at 1.0254. Also, in this case, sustained trading below 1.0404 key fibonacci level will carry larger bearish implication.

In the bigger picture, focus stays on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.

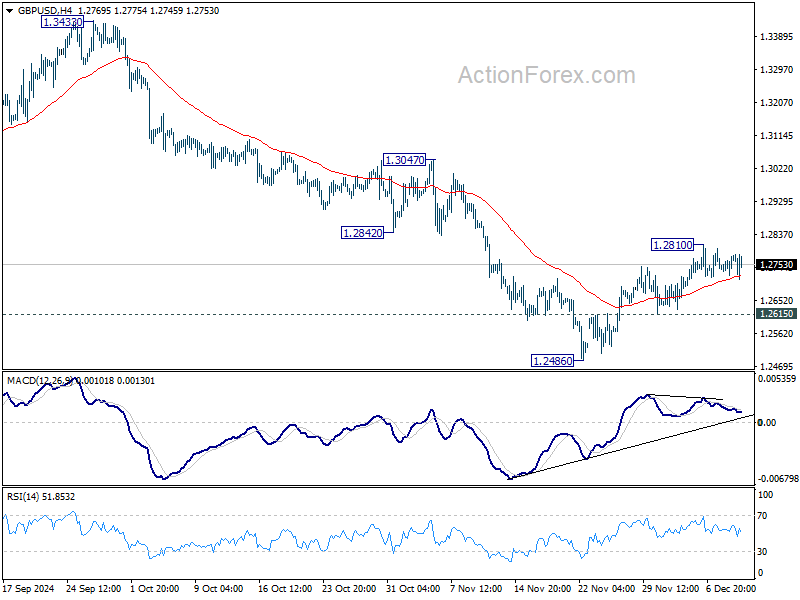

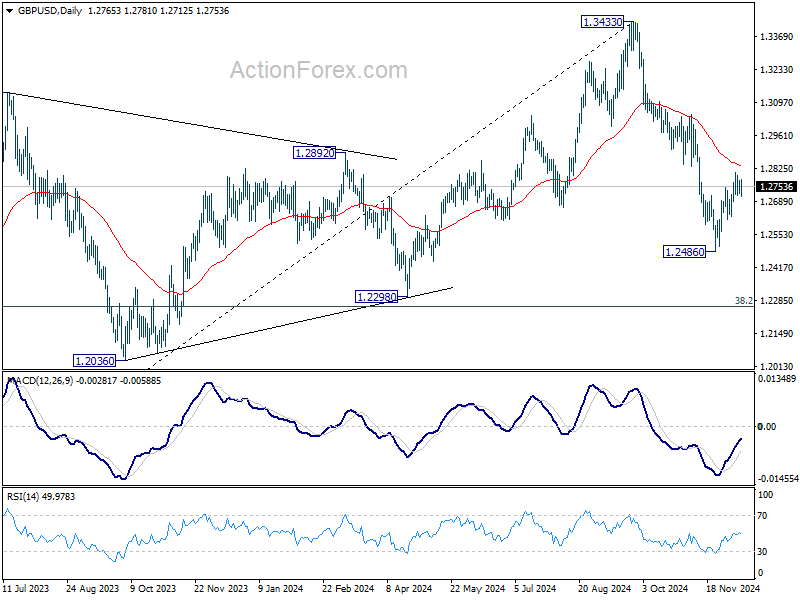

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2737; (P) 1.2758; (R1) 1.2791; More...

GBP/USD is still bounded in sideway trading and intraday bias stays neutral. Rebound from 1.2486 short term bottom could still extend higher. But outlook will stay bearish as long as 55 D EMA (now at 1.2840) holds. On the downside, below 1.2615 minor support will bring retest of 1.2486 first. Firm break there will target 1.2298 cluster support zone. However, sustained break of 55 D EMA will argue that the near term trend has reversed, and targets 1.3047 resistance for confirmation.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern.

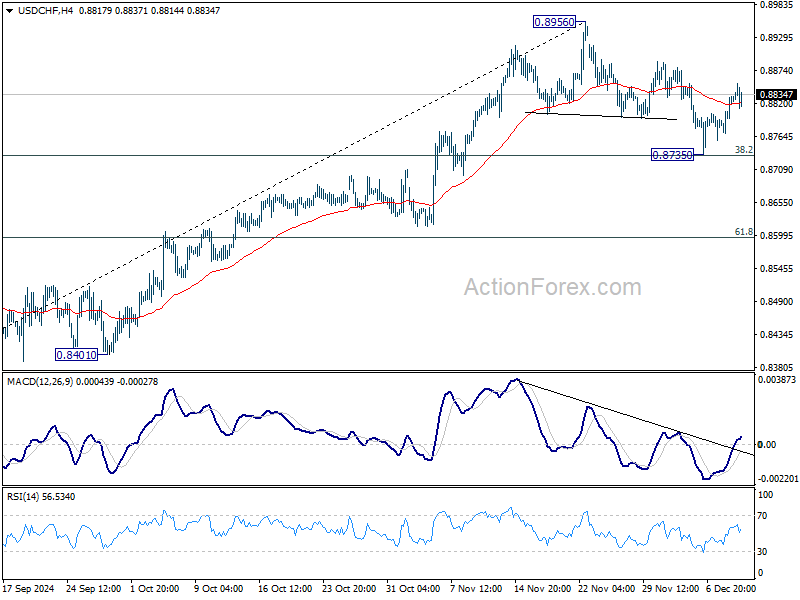

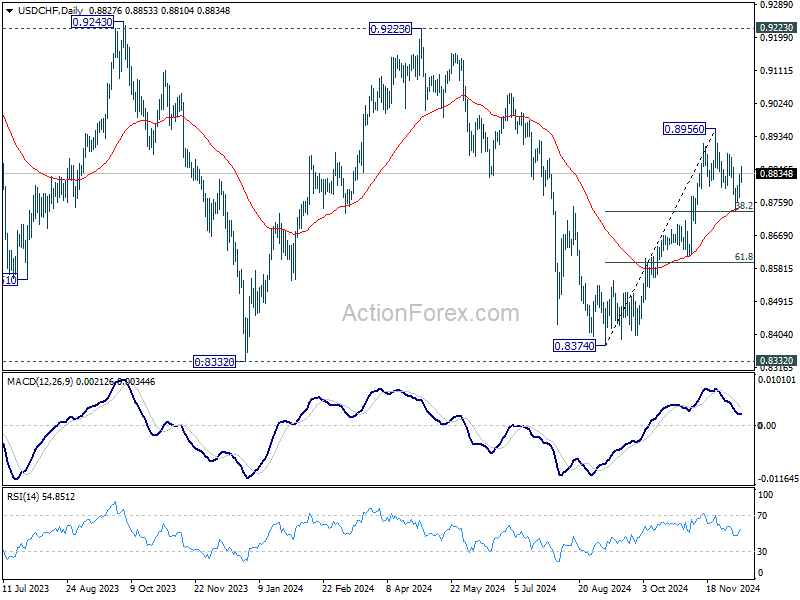

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8787; (P) 0.8810; (R1) 0.8853; More…

Intraday bias remains on the upside for the moment. As noted before, corrective fall from 0.8956 could have completed at 0.8735 after hitting 55 D EMA. Further rally is in expected to retest 0.8956 high first. Firm break there will resume the whole rise from 0.8374. This will remains the favored case as long as 0.8735 support holds, in case of retreat.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

BoC eases 50bps but signals end to continuous rate reductions

BoC cut its overnight rate by 50 basis points to 3.25% as anticipated, but a notable shift in tone suggests a loosening of its easing bias. The central bank stated that interest rates have been reduced "substantially" since June, signaling that future cuts would be evaluated "one decision at a time." This marks a clear pivot toward a more cautious, data-dependent approach, and rate reduction is no longer in auto-pilot.

Also, in the accompanying statement, BoC highlights a number of factors that introduce uncertainty surrounding both growth and inflation outlook, including the array of policy measures introduced by the federal and provincial governments.

The reduction in immigration targets is expected to dampen GDP growth next year. While this lower growth could temper inflationary pressures, the Bank noted that the effect would likely be "more muted" due to immigration's impact on both demand and supply. Additional measures, such as the suspension of the GST on certain goods, direct payments to individuals, and adjustments to mortgage rules, are expected to create temporary fluctuations in demand and inflation.

The statement also highlighted increased uncertainty surrounding trade. The possibility of new tariffs from the incoming US administration adds a layer of complexity to the economic outlook, particularly given Canada’s reliance on exports to its southern neighbor.

(BOC) Bank of Canada reduces policy rate by 50 basis points to 3¼%

The Bank of Canada today reduced its target for the overnight rate to 3¼%, with the Bank Rate at 3¾% and the deposit rate at 3¼%. The Bank is continuing its policy of balance sheet normalization.

The global economy is evolving largely as expected in the Bank’s October Monetary Policy Report (MPR). In the United States, the economy continues to show broad-based strength, with robust consumption and a solid labour market. US inflation has been holding steady, with some price pressures persisting. In the euro area, recent indicators point to weaker growth. In China, recent policy actions combined with strong exports are supporting growth, but household spending remains subdued. Global financial conditions have eased and the Canadian dollar has depreciated in the face of broad-based strength in the US dollar.

In Canada, the economy grew by 1% in the third quarter, somewhat below the Bank’s October projection, and the fourth quarter also looks weaker than projected. Third-quarter GDP growth was pulled down by business investment, inventories and exports. In contrast, consumer spending and housing activity both picked up, suggesting lower interest rates are beginning to boost household spending. Historical revisions to the National Accounts have increased the level of GDP over the past three years, largely reflecting higher investment and consumption. The unemployment rate rose to 6.8% in November as employment continued to grow more slowly than the labour force. Wage growth showed some signs of easing, but remains elevated relative to productivity.

A number of policy measures have been announced that will affect the outlook for near-term growth and inflation in Canada. Reductions in targeted immigration levels suggest GDP growth next year will be below the Bank’s October forecast. The effects on inflation will likely be more muted, given that lower immigration dampens both demand and supply. Other federal and provincial policies—including a temporary suspension of the GST on some consumer products, one-time payments to individuals, and changes to mortgage rules—will affect the dynamics of demand and inflation. The Bank will look through effects that are temporary and focus on underlying trends to guide its policy decisions.

In addition, the possibility the incoming US administration will impose new tariffs on Canadian exports to the United States has increased uncertainty and clouded the economic outlook.

CPI inflation has been about 2% since the summer, and is expected to average close to the 2% target over the next couple of years. Since October, the upward pressure on inflation from shelter and the downward pressure from goods prices have both moderated as expected. Looking ahead, the GST holiday will temporarily lower inflation but that will be unwound once the GST break ends. Measures of core inflation will help us assess the trend in CPI inflation.

With inflation around 2%, the economy in excess supply, and recent indicators tilted towards softer growth than projected, Governing Council decided to reduce the policy rate by a further 50 basis points to support growth and keep inflation close to the middle of the 1-3% target range. Governing Council has reduced the policy rate substantially since June. Going forward, we will be evaluating the need for further reductions in the policy rate one decision at a time. Our decisions will be guided by incoming information and our assessment of the implications for the inflation outlook. The Bank is committed to maintaining price stability for Canadians by keeping inflation close to the 2% target.

Information note

The next scheduled date for announcing the overnight rate target is January 29, 2025. The Bank will publish its next full outlook for the economy and inflation, including risks to the projection, in the MPR at the same time.