Sample Category Title

US Inflation and Dollar Index (DXY) : A Pre-CPI Analysis

- The upcoming US CPI data release on December 11th is a key event for markets, as it could influence the Fed’s decision on interest rates at its December 18th meeting.

- While a rate cut is widely expected, a higher-than-forecast CPI print could raise questions about the Fed’s path forward.

- The US Dollar has strengthened recently, partly due to positive economic data and a risk-off sentiment in markets. Can the Dollar continue its rise?

The upcoming release of the US Consumer Price Index (CPI) data on December 11, 2024, is set to draw the attention of market participants. Scheduled for release at 8:30 a.m. EST, Inflation may be starting to play on the minds of the Fed once more following an uptick in average hourly earnings as well.

Another factor raising inflation concerns are comments by President Elect Trump who stated that he is not sure he will be available to control the potential inflationary impact of his tariff proposals. However, as many have pointed out, tariffs may just be a negotiating tactic.

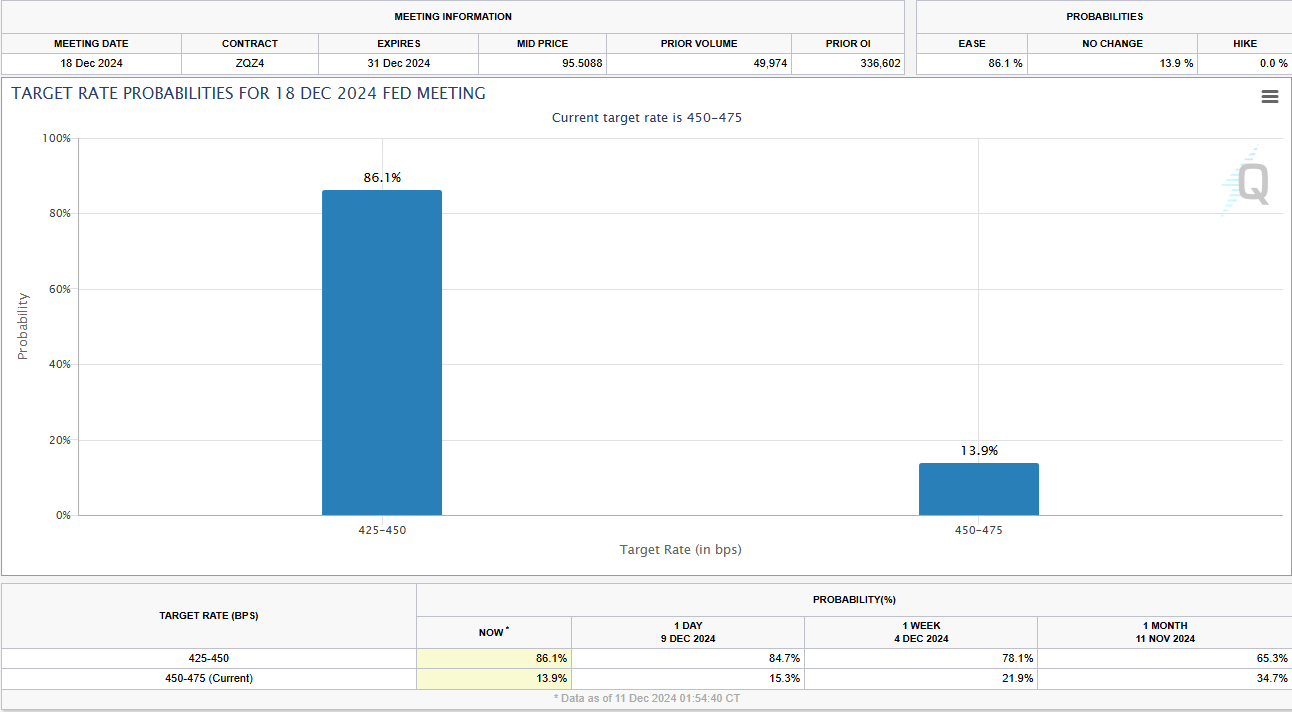

Heading toward the Fed meeting on December 18, market participants are pricing in around an 86% probability of a 25 bps rate cut. Inflation in my opinion is unlikely to change that narrative with any change to policy likely to come at the Feds January meeting.

Source: CME FedWatch Tool (click to enlarge)

What is the Expected CPI Print?

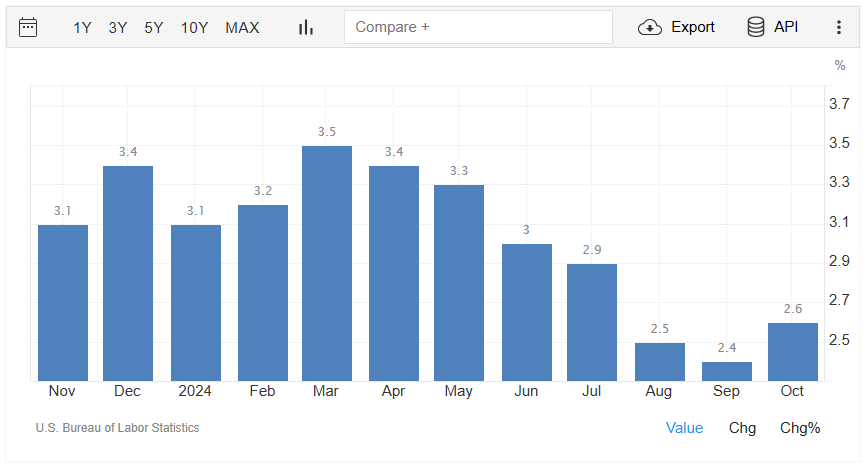

Analysts predict that overall inflation (headline CPI) will go up slightly to 2.7% from 2.6% over the last year. Core inflation, which ignores food and energy price changes, is expected to stay the same at 3.3%. On a monthly basis, both measures are likely to rise by 0.3%.

This shows that inflation is steady but still a concern. Factors like stable housing costs and lower energy prices are expected to play a role in these changes.

Source: TradingEconomics (click to enlarge)

The big question is whether this will be enough to result in any change to the Fed decision this month? Most Fed members have recently said they plan to cut interest rates by 0.25% at the December meeting. The Fed are also in their ‘blackout period’ at present, which means we have nothing else but the CPI data to go on ahead of the Fed meeting.

It’s easy to think the Fed is done worrying about inflation, but if core inflation goes above the expected 0.3% for the month, this could lead to a change in the probability of a rate cut even if it might not delay it. A high core CPI reading could make it more of a 50/50 proposition although i would still lean toward a rate cut.

An increase in the CPI prints, particularly the core reading could then in theory be responsible for another leg higher in the US Dollar index (DXY).

Technical Analysis – US Dollar Index (DXY)

From a technical standpoint, the dollar has strengthened this week, partly because of the very positive small business optimism report released yesterday. It’s not surprising that US business owners are excited about possible tax cuts and fewer regulations next year.

This coupled with a risk of tone at the start of the week which helped boost the US Dollars safe haven appeal have left the US Dollar Index eyeing acceptance above the 107.00 handle.

There is a trendline break which has come to fruition and hints at further US Dollar upside. Based on the rules of a trendline break the overall target of the breakout is around the 107.50 which could come into play on a higher US CPI reading.

The implications of this on other assets could be broad ranging with it likely to effect US equities, currencies and bond markets.

US Dollar Index (DXY) Daily Chart, December 11, 2024

Source: TradingView.com (click to enlarge)

Support

- 106.13

- 105.63

- 105.00

Resistance

- 107.00

- 107.50

- 108.00

USDCAD Gears Down as BoC Rate Decision Looms

- USDCAD slows pace after fresh four-year high

- Bears wait below 1.4150, but uptrend could stay intact

- BoC rate announcement due at 14:45 GMT

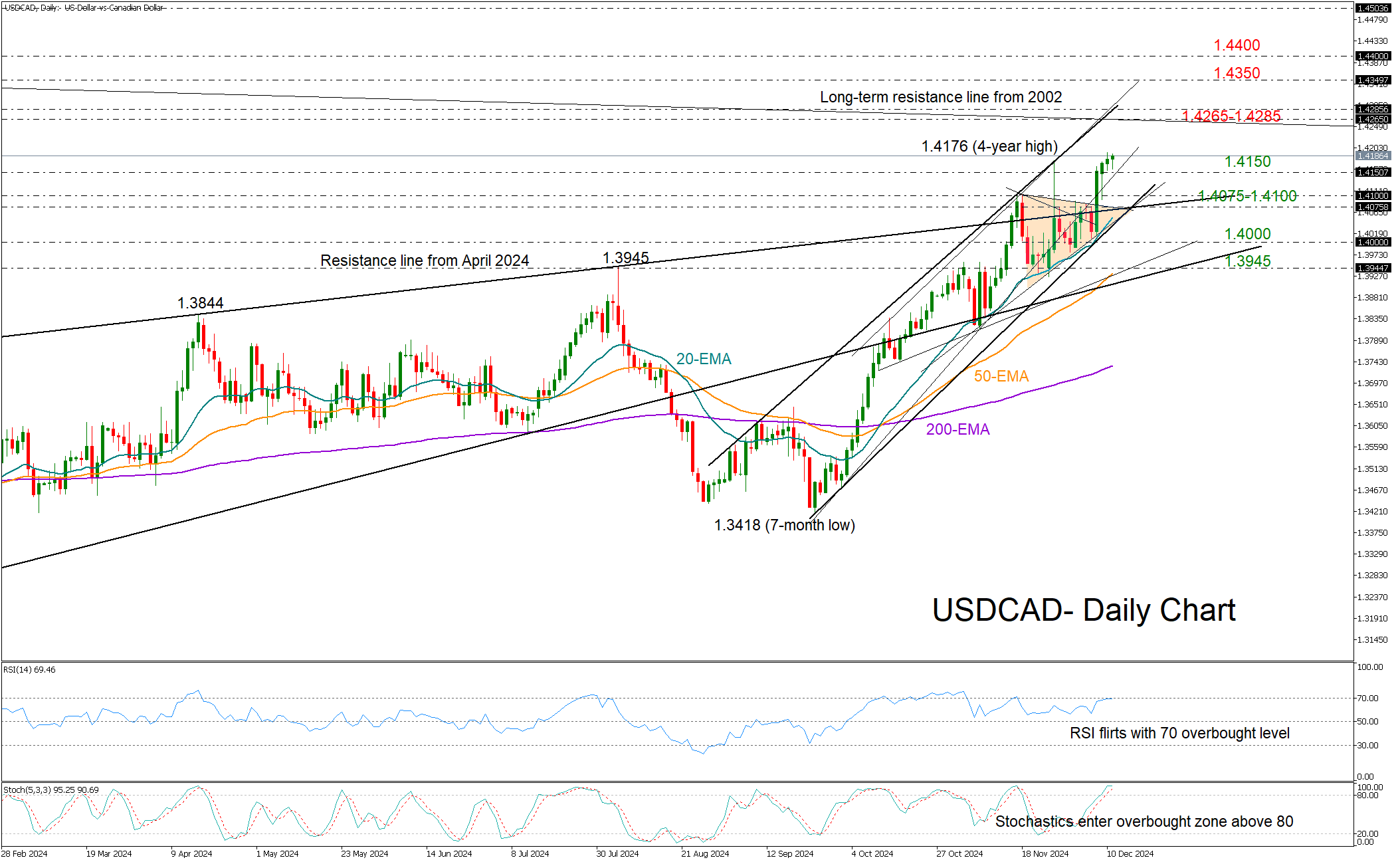

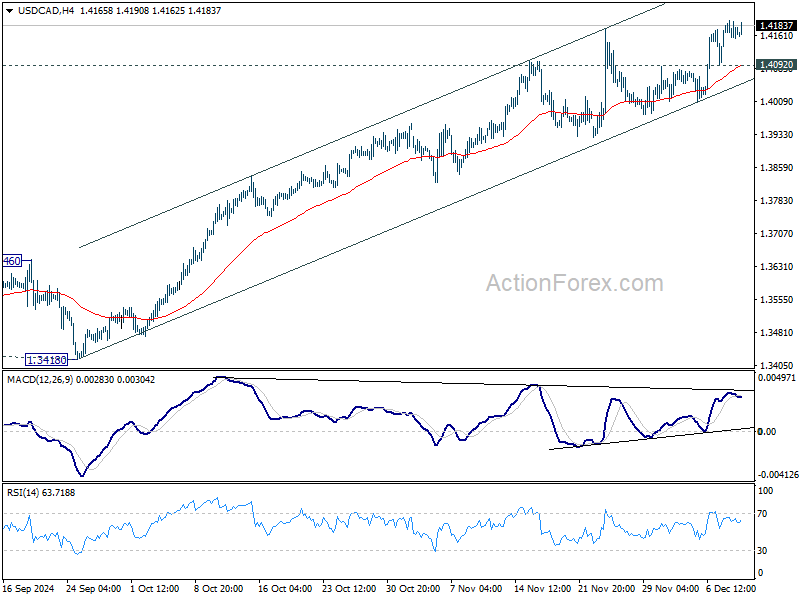

USDCAD broke above a neutral symmetrical triangle with a bang last Friday, surpassing November's four-year high of 1.4176, but since then the pair has been losing pace, raising questions about whether the rally is nearing a peak.

With the RSI and the stochastic oscillator hanging near overbought levels, a slowdown is likely. Yet only a drop below the 1.4150 barrier could activate fresh selling orders toward the 1.4075-1.4100 area. Another failure there could confirm additional losses toward the 1.4000 level, while a steeper decline could push toward the 50-day exponential moving (EMA) at 1.3945.

On the upside, if the bulls successfully claim the 1.4200 number, they could next target the 1.4265-1.4285 resistance trendline zone. A continuation above 1.4300 could take a halt near 1.4350 or around the 1.4400 mark.

Overall, USDCAD is still in a positive trajectory and any potential declines could present a “buying the dip” opportunity. A move below 1.4150 could trigger the next bearish action, whilst a move above 1.4200 could shift the attention back to the upside.

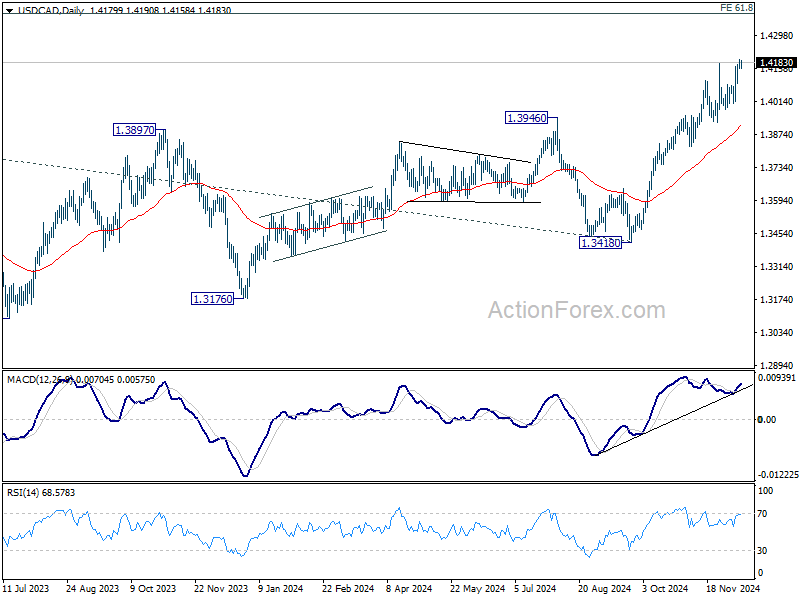

USD/CAD at a 56-Month High

As evidenced by the USD/CAD chart, yesterday the rate climbed above 1.4190 – a level not seen since April 2023, when the world was gripped by panic over the spread of the coronavirus.

Today, the weakness of the Canadian dollar relative to the USD is being influenced by a rich fundamental backdrop. As reported by the media:

→ Formerly elected President Donald Trump has previously stated that he would impose a 25% tariff on all goods from Mexico and Canada as soon as he takes office on 20 January, joking that Canada should become the 51st state. Yesterday, Trump posted on social media that he looks forward to meeting with Canadian Prime Minister Trudeau again to "continue our in-depth discussions on tariffs and trade."

→ At 17:45 GMT+3 today, the Bank of Canada will announce its decision. It is expected to cut its interest rate by 50 basis points to 3.25% and likely signal that further rate cuts are possible in light of the sharp rise in unemployment levels.

→ At 16:30 GMT+3 today, the Consumer Price Index (CPI) data will be released. It is expected that US inflation will remain unchanged.

As a result, heightened volatility is highly likely today, which could significantly affect the nature of the current upward trend.

Note that on 25–26 November, a spike in volatility was observed on the USD/CAD chart, visible through the ATR indicator, which caused the channel's slope to become less steep. Today’s batch of news carries the highest significance: traders should prepare for both the scenario of a new 56-month high being reached and an attempt by bears to reverse the trend.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

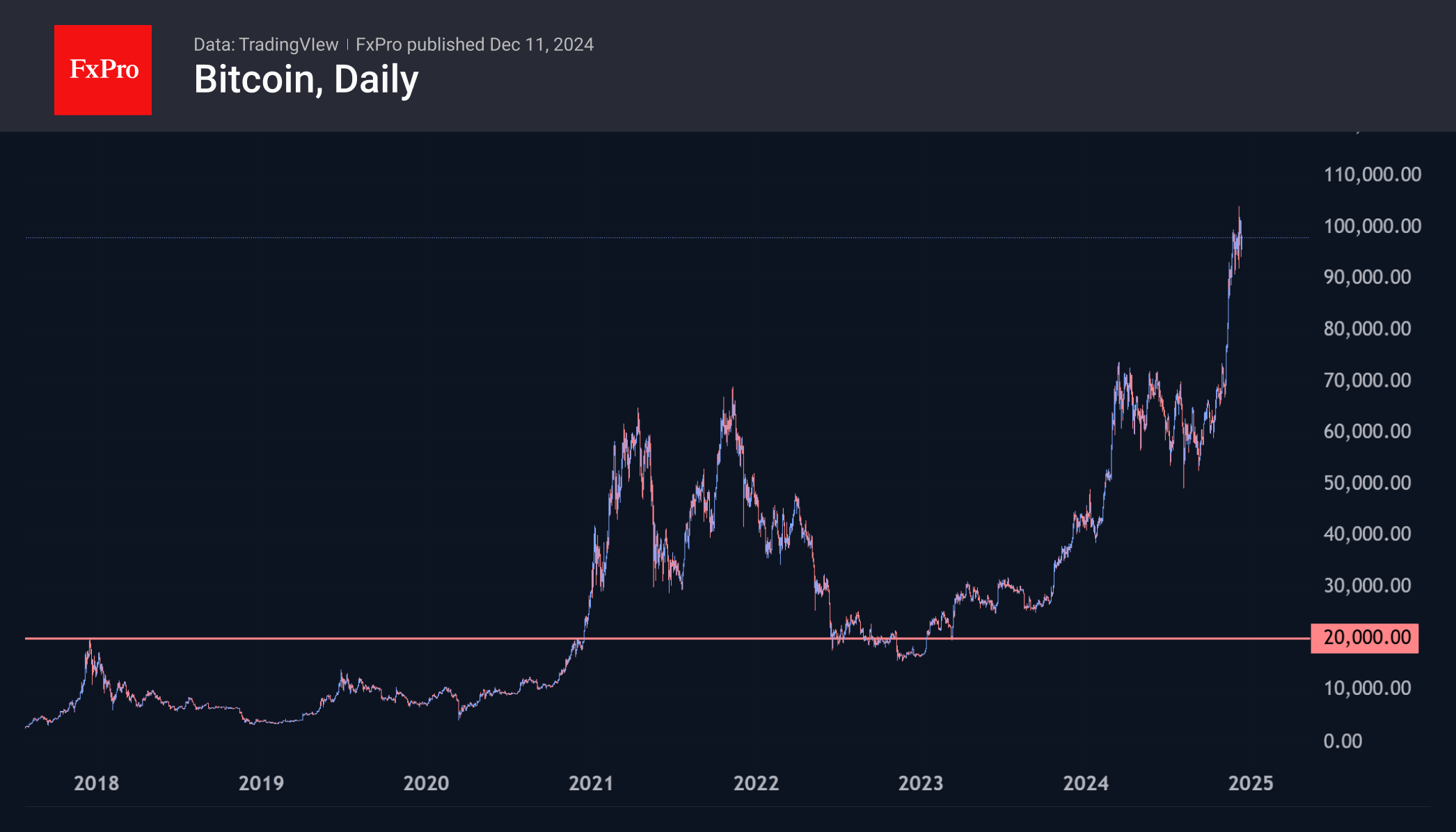

Between $95K and $100K, Bitcoin Changes Long-Term Holders

Market Picture

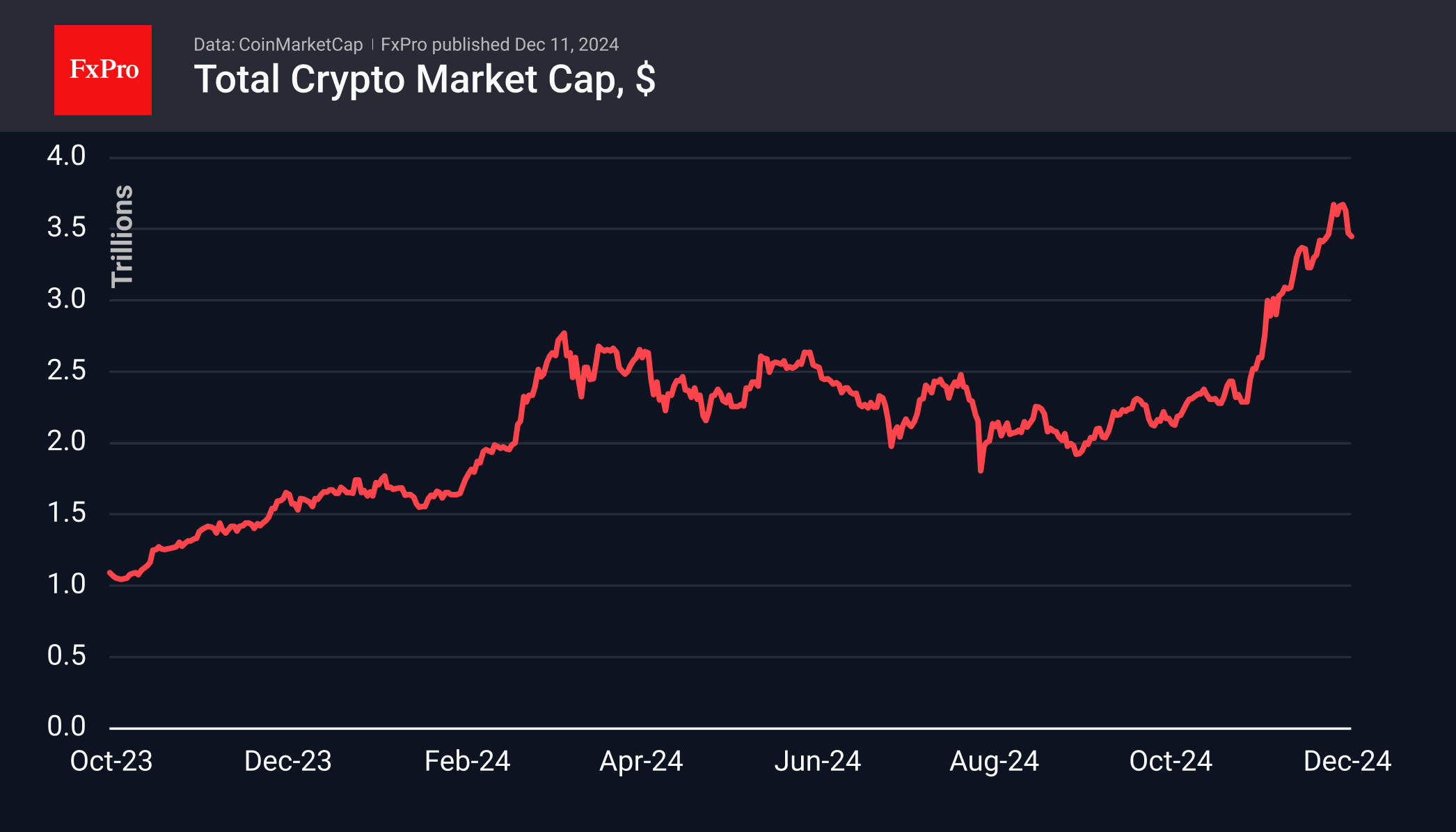

The cryptocurrency market remained roughly the same as the day before at $3.45 trillion, down 7% from its peak levels at the start of the week. The sentiment index rolled back to 74, in ‘greed’ territory. The altcoin season index has pulled back to 63 from a peak of 87 a week earlier. This is a typical story where Bitcoin’s inability to grow soon translates into pressure on altcoins.

There is a meaningful change of ownership for Bitcoin in the $95-100k range. Bitcoin experienced another wave of selling in the US session on Tuesday, just as it did the day before. Once again, buyers retook the initiative when the price dipped under $95k, and at the time of writing, the price has recovered to $98k. The meaningful round level has prompted long-term private holders to sell. At the same time, there is a growing appetite for corporations to buy on their balance sheets. Then, there is the key to how governments holding impressive amounts of confiscated Bitcoins will behave.

For now, we believe Bitcoin is meeting psychological resistance like 2020, when it hesitated to cross $20K at year-end but eventually broke through, doubling in price shortly after. In this cycle, we see upside potential to $120-140K in the next couple of months before the next major shakeout.

News Background

CryptoQuant notes that on 5 December, when the price was at an all-time high, significant transfers from holders could have caused a sharp drop to $90,500.

Stablecoin market capitalisation has surpassed $200 billion, adding 3% in the last seven days. Coinbase attributed the dynamics to a sharp rise in on-chain lending rates.

Mining company MARA Holdings used the proceeds from the bond sale to buy 11,774 BTC for ~$1.1bn at an average price of around $96K per coin. The firm has 40,435 BTC worth $3.9bn in reserves.

Another mining company, Riot Platforms, plans to float $500 million in convertible bonds, using the funds to buy more bitcoins and for general corporate purposes.

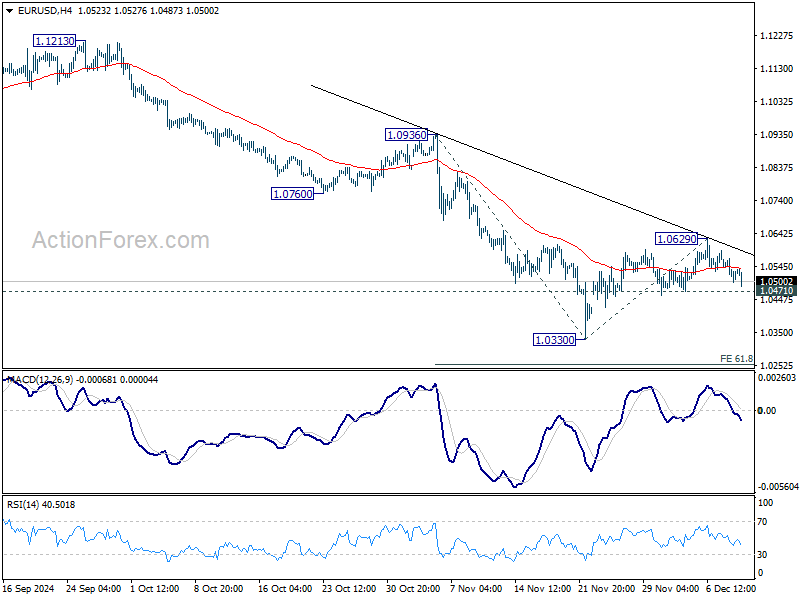

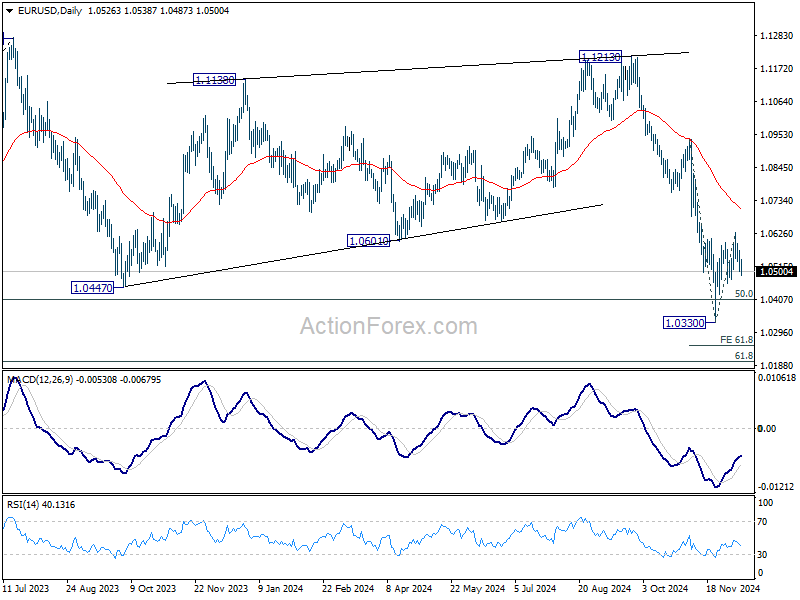

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0495; (P) 1.0531; (R1) 1.0565; More...

Intraday bias in EUR/USD remains neutral for the moment. On the downside, break of 1.0471 support will suggest that corrective recovery from 1.0330 has completed, and fall from 1.1213 is ready to resume. Intraday bias will be back on the downside for 1.0330 first, and then 61.8% projection of 1.0936 to 1.0330 from 1.0629 at 1.0254. Also, in this case, sustained trading below 1.0404 key fibonacci level will carry larger bearish implication.

In the bigger picture, focus stays on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.

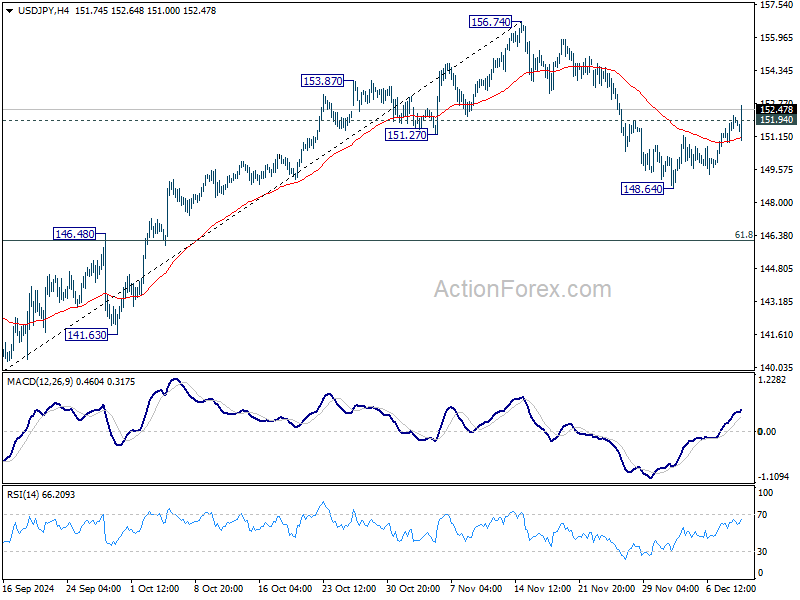

USD/JPY Daily Outlook

Daily Pivots: (S1) 151.18; (P) 151.69; (R1) 152.47; More...

USD/JPY's break of 151.94 resistance suggests that pull back from 156.74 has completed as a correction at 148.64. That is, rise from 139.57 hasn't completed yet. Intraday bias is back on the upside for retesting 156.74 first. Firm break there will target 161.94 high next. For now, this will be the favored case as long as 148.64 support holds.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

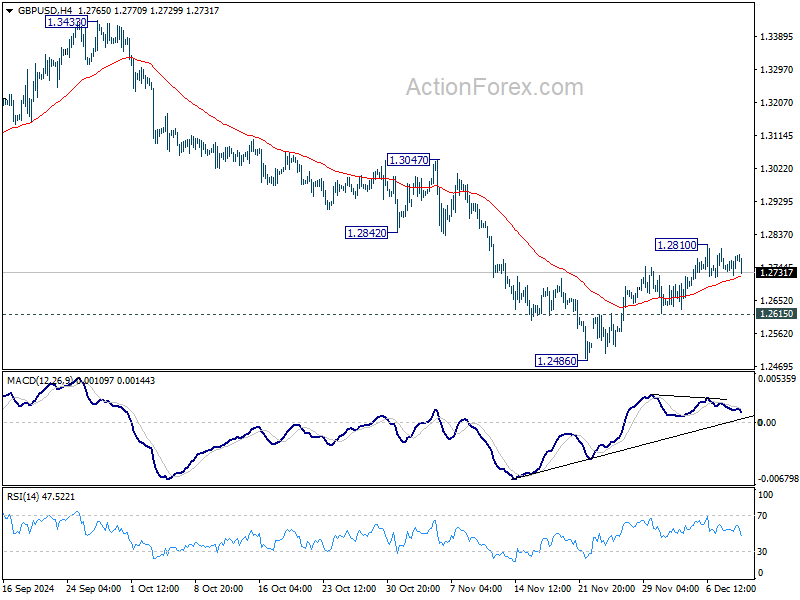

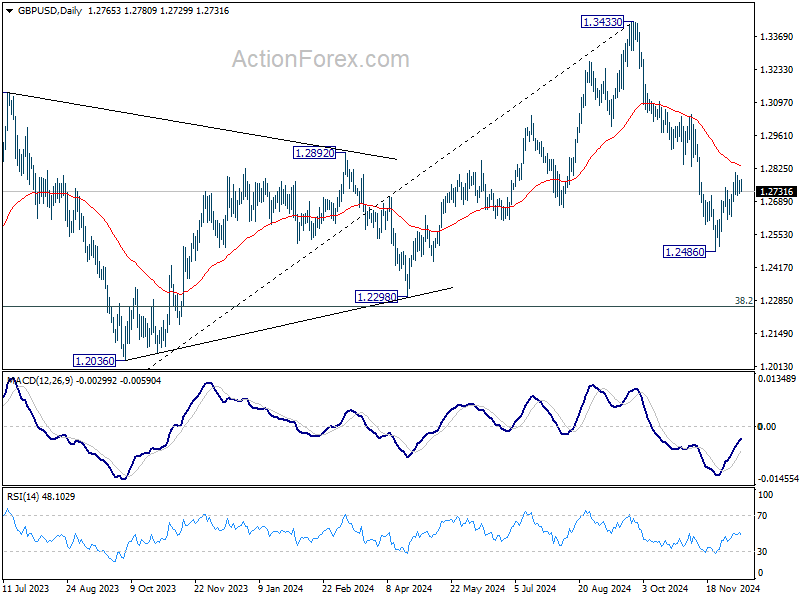

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2737; (P) 1.2758; (R1) 1.2791; More...

Intraday bias in GBP/USD remains neutral as range trading continues. Rebound from 1.2486 short term bottom could still extend higher. But outlook will stay bearish as long as 55 D EMA (now at 1.2840) holds. On the downside, below 1.2615 minor support will bring retest of 1.2486 first. Firm break there will target 1.2298 cluster support zone. However, sustained break of 55 D EMA will argue that the near term trend has reversed, and targets 1.3047 resistance for confirmation.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern.

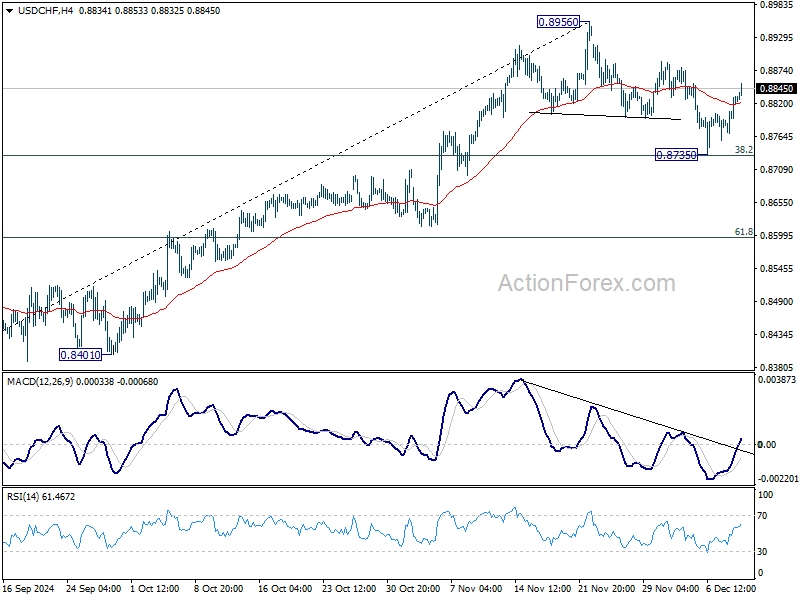

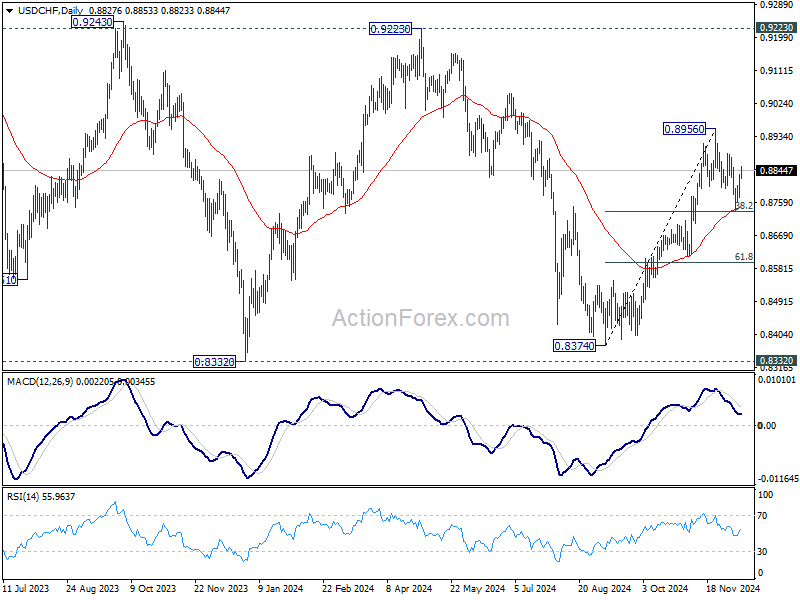

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8787; (P) 0.8810; (R1) 0.8853; More…

USD/CHF's rebound from 0.8735 continues today and intraday bias stays on the upside. As noted before, corrective fall from 0.8956 could have completed at 0.8735 after hitting 55 D EMA. Further rally is in expected to retest 0.8956 high first. Firm break there will resume the whole rise from 0.8374. This will remains the favored case as long as 0.8735 support holds, in case of retreat.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4160; (P) 1.4178; (R1) 1.4199; More...

Intraday bias in USD/CAD remains on the upside for the moment. Current rally is part of the larger up trend and should target 1.4391 projection level. On the downside, below 1.4092 minor support will delay the bullish case, and bring more consolidations first, before staging another rise.

In the bigger picture, up trend from 1.2005 (2021) is in progress. Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391. Now, medium term outlook will remain bullish as long as 1.3418 support holds, even in case of deep pullback.

RBA’s Hause: Australia more seriously affected by global trade war because of China reliance

RBA Deputy Governor Andrew Hauser addressed the implications of US President-elect Donald Trump’s proposed tariffs at an event today. He highlighted that while higher global tariffs could depress activity across supply chains, the full extent of the effects would depend on various factors, including currency adjustments and fiscal responses in affected economies.

“Given this uncertainty, it is important that we don’t prejudge the implications of tariffs for policy but monitor developments closely and stand ready to respond appropriately as the facts emerge,” Hauser stated.

Hauser pointed out Australia’s unique vulnerability due to its trade exposure, with over 80% of its iron ore exports destined for China, which accounts for three-quarters of global iron ore imports.

This heavy reliance on China increases the risk of significant disruptions if Beijing becomes the target of punitive tariffs or if global trade realigns along geopolitical lines.

“This seems to suggest that Australia could find itself more seriously affected by a global trade war than some of the average exposure data suggest,” Hauser noted.