Sample Category Title

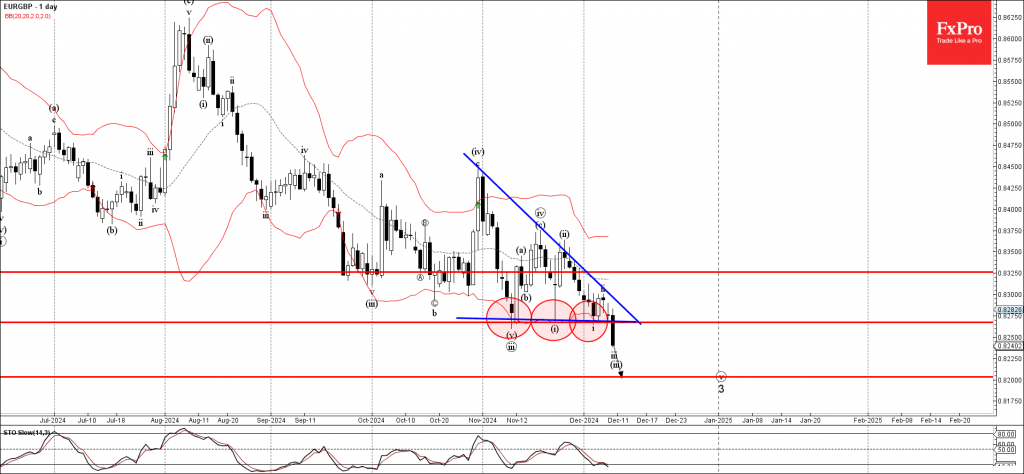

EURGBP Wave Analysis

- EURGBP under bearish pressure

- Likely to fall to support level 0.8200

EURGBP currency pair under bearish pressure after breaking the support zone between the key support level 0.8265 (which stopped previous waves iii, (i) and i) and the support trendline of the Descending Triangle from November.

The breakout of this support zone accelerated the active impulse waves 3 and v – which belong to the impulse wave (3) from January.

Given the clear daily downtrend, EURGBP currency pair can be expected to fall toward the next support level 0.8200, the target for the completion of the active impulse wave 3.

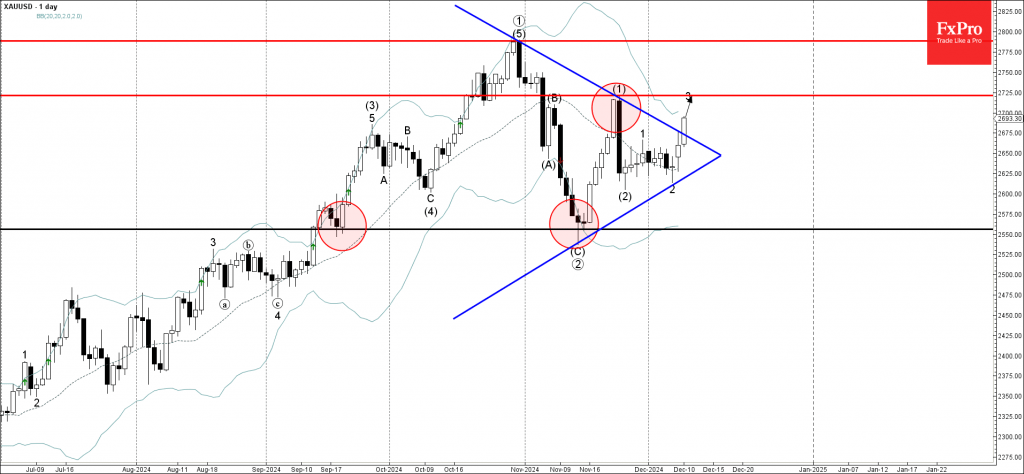

Gold Wave Analysis

- Gold broke daily Triangle

- Likely to rise to resistance level 2750.00

Gold recently broke the resistance trendline of the daily Triangle, inside which it has been moving from the middle of October, as can be seen from the daily Gold chart below.

The breakout of this Triangle accelerated the active short-term impulse wave 3 – which belongs to the intermediate impulse wave (3) of the primary impulse wave 3 from last month.

Given the strong multi-month uptrend, Gold can be expected to rise to the next resistance level 2750.00, top of the previous impulse wave (1) from November and the forecast price for the completion of the active impulse wave 3.

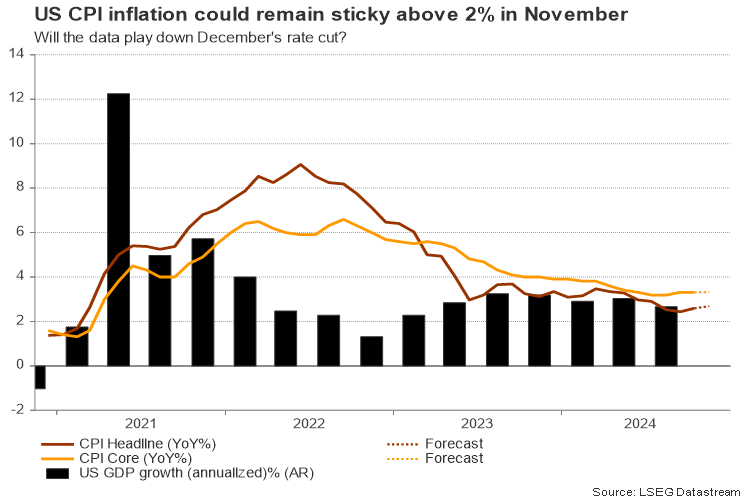

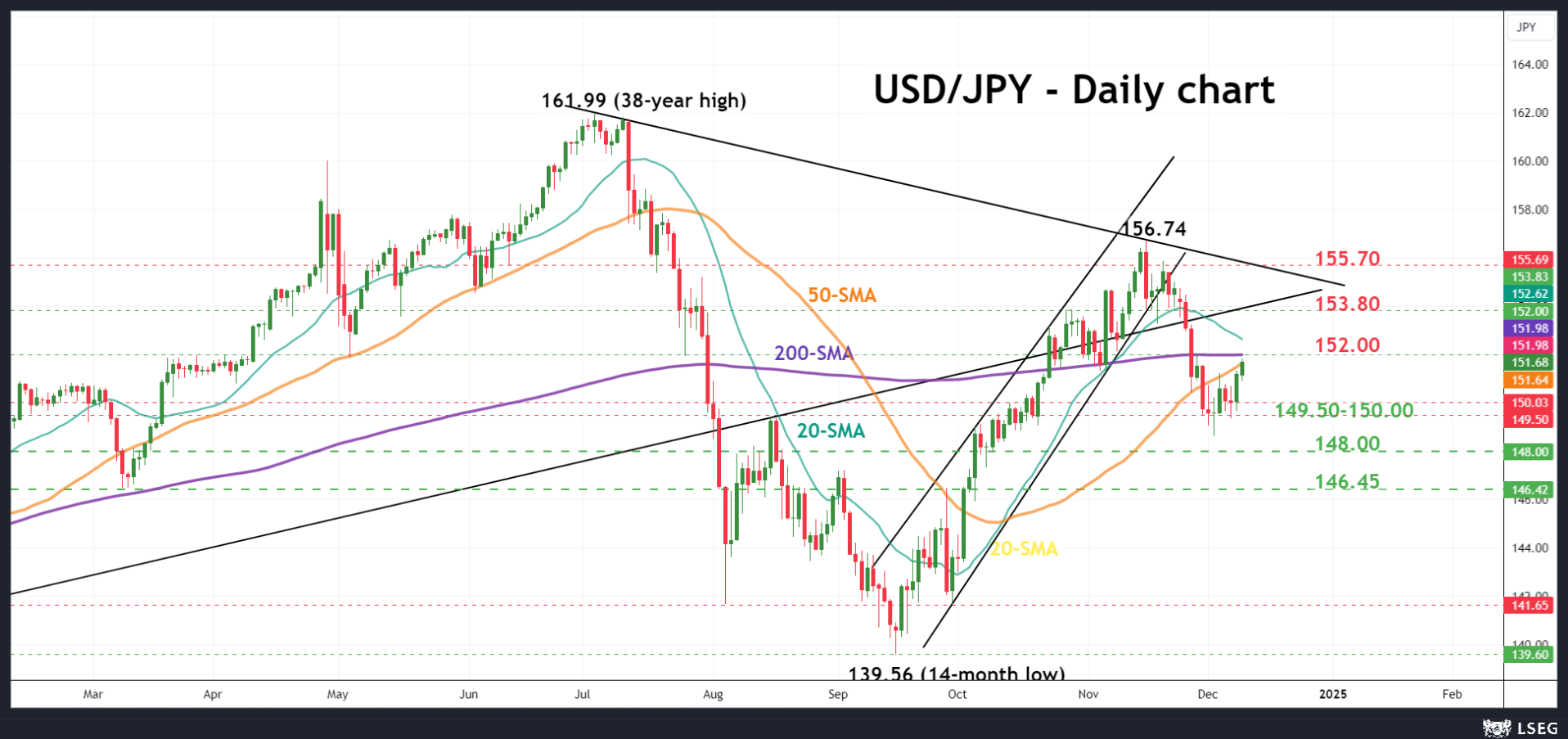

US CPI Inflation: A Potential Headwind for a Rate Cut?

- US CPI inflation could inch higher for the second month

- A December rate cut could stay a close call

- USDJPY pushes for some recovery, needs a break above 152.00

US nonfarm payrolls could not play down the odds of a 25bps December rate cut despite clocking in stronger than expected last week. But could a rise in the US CPI inflation data derail those expectations?

Forecasts

The figures will be out on Wednesday at 13:30 GMT and analysts are forecasting a slight uptick in monthly CPI inflation, from 0.2% to 0.3%, which would push the annual rate up to 2.7% from 2.6% previously. The core CPI, which strips out volatile food and energy prices, is expected to remain steady at 0.3% month-over-month and 3.3% year-over-year.

Could CPI inflation derail a rate cut?

If inflation proves more persistent than anticipated, holding above the Fed’s 2.0% target, particularly in housing and shelter—a category that contributed over half of October’s gains—it could dampen hopes for an immediate rate cut. Recall that Donald Trump reassured investors that he has no intention of firing Fed Chair Jay Powell, signaling a continuity of the existing monetary guidance. Therefore, the Fed may feel less stressed to rush into rate cuts.

Even with these inflation concerns, there is still a compelling case for a rate cut in December. Investors are uncertain about the timing and scale of Trump’s proposed tax cuts and import tariffs, which could stir inflationary pressures, keeping interest rates in restrictive territory longer than expected. This would continue to weigh on growth, forcing the Fed to frontload rate cuts before political uncertainty kicks in.

How would markets react?

With futures markets providing a strong probability of 85% for a December 25bps rate cut in December, a soft negative surprise in the data could moderately press the US dollar. In this case, USDJPY could slide back to the 149.50-150.00 support area, while the 148.00 territory will be watched in the event of a significant slowdown in inflation, which could open the door to a January reduction. Note that the blackout period is already underway. Hence, there won’t be any directional comments from FOMC members in the aftermath.

In the opposite case, where the figures speed up faster than analysts think, the greenback could surpass the 152.00-yen barrier with scope to reach the crucial 153.80 resistance. Yet, given the uncertain 2025 political and economic policy outlook, policymakers could deliver a hawkish rate cut, signaling a potential pause in January.

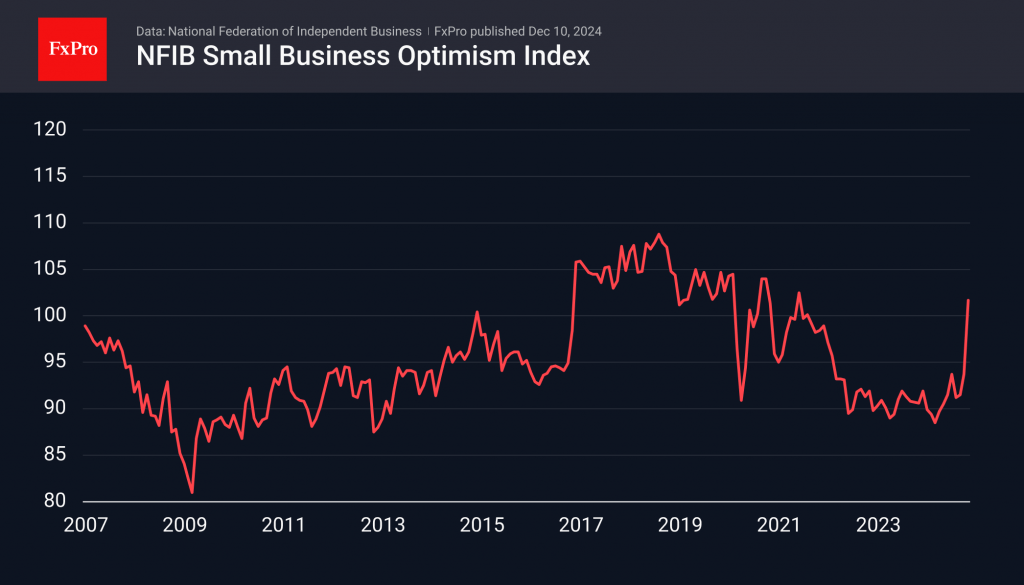

US: Small Business Optimism Index Improves Significantly in November

The NFIB's Small Business Optimism Index rose 8.0 points to 101.7 in November, exceeding market expectations for a smaller increase to 95.3.

Nine out of ten subcomponents improved on the month, with the share of businesses reporting current inventories to be too low being the only unchanged category. The largest increases came from the share of businesses expecting the economy to improve (up 41 points to 36%), those expecting higher real sales in six months (up 18 points to 14%), and those reporting that now is a good time to expand (up 8 points to 14%).

The net share of businesses planning to increase employment rose 3 points to 18%, reaching its highest level in a year. The share of firms with unfilled job openings ticked up by 1 point to 36%. Quality of labor concerns declined in November, with 19% of business owners identifying this as their top business problem, as they are now roughly tied with inflation concerns which also fell on them month.

The net share of firms currently increasing employee compensation rose 1 point to 32%, while the net share planning to do so over the next three months rose 5 points to 28% - the highest level of the year. The share of businesses 'raising' average selling prices increased by 3 points to 24% while the share of those 'planning’ to raise average selling prices increased by 2 points to 28%.

Key Implications

Small business confidence hit its highest level in over three years in November as the Republican sweep in Washington enhanced expectations for a more accommodative fiscal and regulatory environment in the coming years. This shift in sentiment was borne out across the survey's subcomponents related to expectations, with most notching multi-year highs. However, relatively slim Congressional majorities and higher trade uncertainty kept the small business uncertainty index at a historically elevated level.

On a more concerning note for the Federal Reserve, the share of small businesses raising average selling prices has become stuck at an elevated level, similar to the recent trend in core PCE inflation. This appears to be in part driven by a recent uptick in plans to raise employee compensation, however with labor market conditions continuing to come into better balance it is unlikely this will pose a material risk to the Fed's current rate cut trajectory. We expect interest rate cuts to continue with another 25 basis-point cut in December, followed by additional easing through 2025.

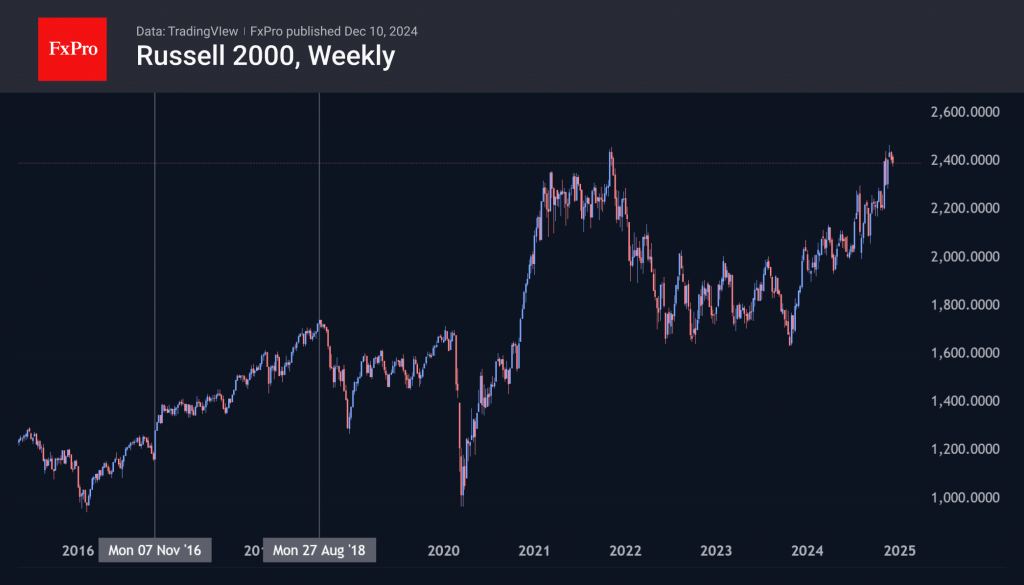

US Small Business Optimism Soars

Small businesses have become more optimistic since the November election, as evidenced by an eight-point jump in the Small Business Optimism Index. There was a similar jump in 2016 following Donald Trump’s victory.

The index jumped to 101.7, above its historical average of 98, with improvements in nine out of ten components (current inventory unchanged). The biggest gains were driven by expectations of an improving economy.

Promises of protectionist policies and tax cuts have fuelled these expectations. Between November 2016 and September 2018, the Russell 2000 index of small-cap companies gained almost 50%, compared with around 35% for the S&P 500. The initial surge in the Russell 2000 on Trump’s victory explains the expectation of outperformance by smaller companies. However, since early December, this index has been falling based on expectations of tighter monetary policy for the foreseeable future. In contrast, the Nasdaq100 and the S&P500, which are filled with giants and less sensitive to interest rate movements, are regularly hitting all-time highs.

Will this divergence continue, or will we see a return to the 2016-2018 pattern? We are leaning towards the latter scenario but would prefer to see confirmation first in the form of the Russell2000 updating highs above 2460.

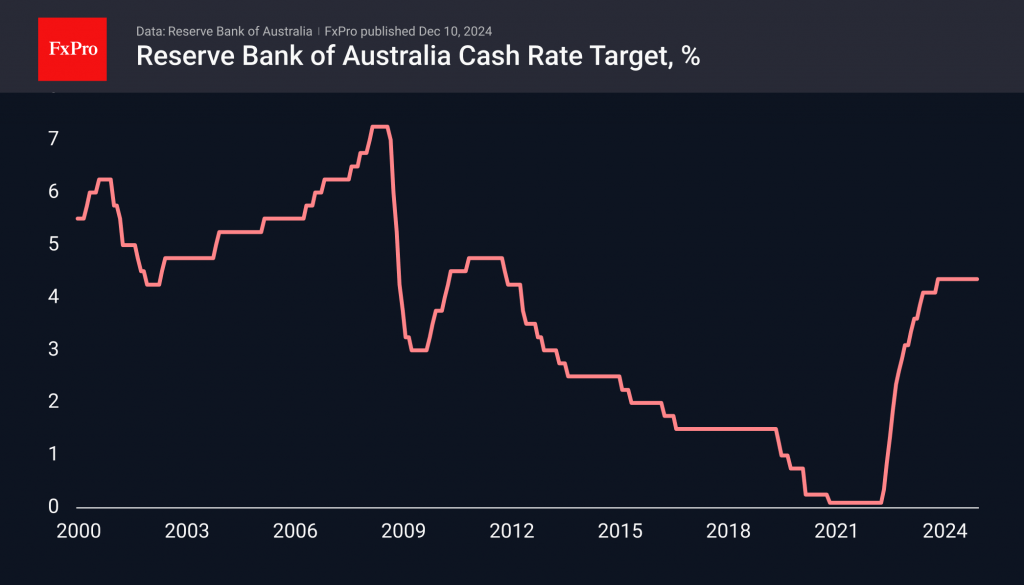

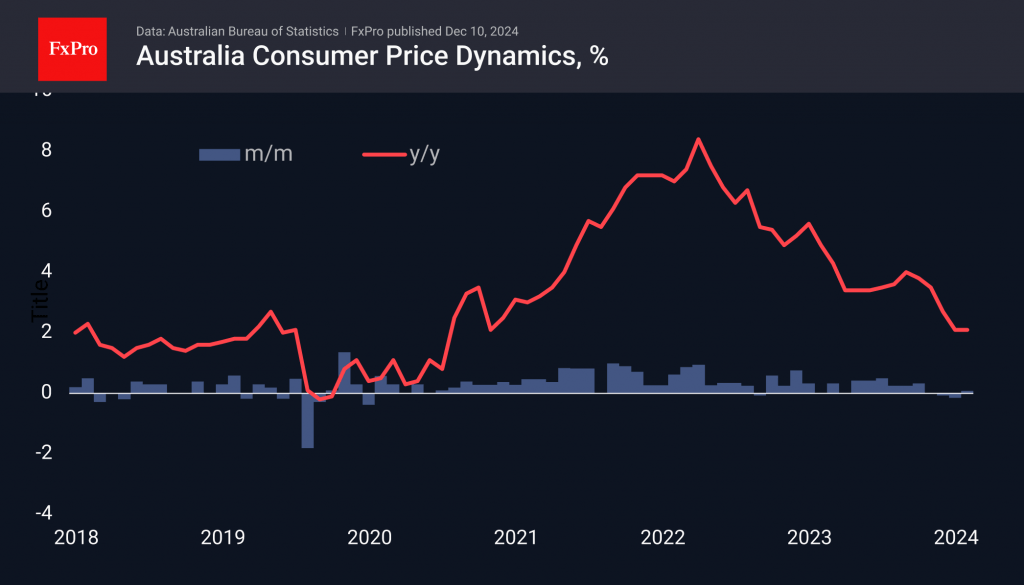

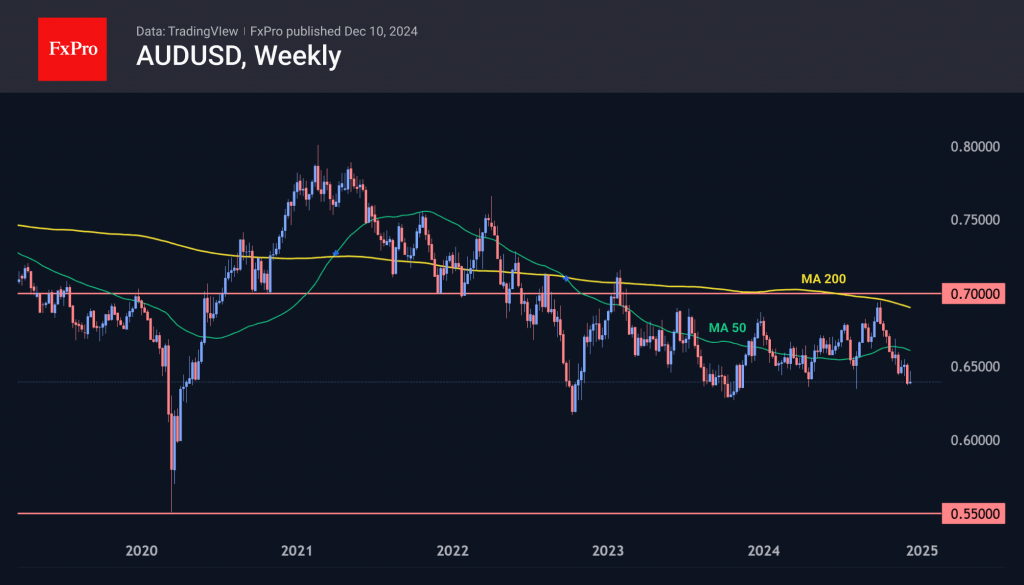

RBA Kept Rate Unchanged But Failed to Stop AUD Slide

The Reserve Bank of Australia kept its cash rate unchanged at 4.35%, maintaining it at a 13-year high for the past 13 months.

Most of the RBA’s peers have moved to ease monetary policy at various points this year, including aggressive cuts by neighbouring RBNZ, suggesting that inflation is on a downward trajectory. Australian consumer inflation was 2.1% in September and October (latest data available). However, this is not enough for the RBA, which noted that the core inflation rate of 3.5% is still above the 2.5% target.

However, the RBA has indicated growing confidence that inflation will return to target, seemingly opening the door to an easing of policy soon. Weak economic growth is also a case for easing. GDP growth slowed to just 0.8% last year. Barring a double dip, this is the slowest pace since 1991, the last time the economy was in a natural recession.

On the news of the rate, the AUD temporarily lost its footing and returned to the local lows of the last three trading sessions below 0.6400. Conventional logic would suggest that tighter monetary policy should cause the Aussie to strengthen against rivals that are cutting rates. But in Australia’s case, traders are more likely to be swayed by the outlook for the economy and monetary tightening promises to further suppress economic growth.

The AUDUSD, at 0.6400, is trading at the lower end of its range of the past two years, having lost around 8% over the past 10 weeks. Technically, this was a reversal to the downside from the 200-week moving average. Now, it is important to watch how the pair performs in the coming weeks. A break of the long-term support will open the way for a decline to 0.55. The ability to hold above will trigger a scenario of a return to the 0.70 area.

Sunset Market Commentary

Markets

EUR/GBP set a minor YTD low today at 0.8250. The move came as UK Gilts underperformed German Bunds. UK yields currently add 2.1 bps (2-yr) to 4.6 bps (30-yr) compared with German yields sliding by up to 3.9 bps at the front end of the curve. The euro remains in the defensive going into Thursday’s ECB meeting. While ECB President Lagarde won’t find common ground to step up the pace of rate cutting (25 bps to 50 bps), we do believe that the central bank’s third consecutive rate cut will be accompanied by some dovish hints. Think about dropping the reference to sticking with a restrictive monetary policy, downward revisions to GDP/CPI forecasts and a more formal return to forward looking decision making. The UK (and sterling) are in a different spot with Bank of England governor Bailey being forced into wait-and-see mode by Chancellor Reeves’ expansive 2025 budget as it triggered an upward revision in the expected CPI peak next year (+0.5 ppt) and delay in the expected return of inflation below the BoE’s 2% inflation target (2027 instead of 2026). The BoE meets a final time this year next Thursday (Dec 19). The monetary policy split and rising UK/EU (2y) yield differential suggest that EUR/GBP is heading for a test of the post-brexit low at 0.8203. A similar dynamic is at play in EUR/USD (1.0525). The pair failed to rebound beyond 1.06 after extensively testing the downside of the 2023-2024 trading range (1.0448) in the wake of US elections. The US treasury yield curve bear steepens today with yields rising by 1.4 bps (2-yr) to 3.1 bps (30-yr). Technical charts suggest – like in Europe – some tentative bottoming out at the longer end of the curve. Upcoming 10-yr and 30-yr Note/Bond auctions are at play as well. Today’s eco calendar was extremely thin with only a consensus-beating increase in November NFIB small business optimism (101.7 from 93.7 vs 95.3 expected). The three-year high in the index is more evidence of enthusiasm after Trump’s election win. Details moreover showed that a net 28% of businesses planned to raise prices over the next three months, the largest share since May. It adds to rising short term inflation (expectations) (eg yesterday’s NY Fed Survey or Friday’s Michigan consumer confidence) and effectively hampers the Fed’s normalization plans (as set out in September) next year. We think that there’s room to pause the rate cut cycle in January 2025 after a 25 bps rate cut at next week’s final Fed meeting of the year.

News & Views

The Bank of International Settlements in its quarterly report once again warned for the threat of soaring government debt. It singled out the US, where investors are facing a potentially toxic combination of debt oversupply and stimulus spending that could boost inflation. The BIS head of the monetary and economic department Borio said there were more reasons to be worried now than when it issued a similar warning earlier this year. The BIS report mentioned there was a supply-demand imbalance in the US Treasury market, with dealers holding record amounts of unsold US bonds on their books. Estimates by the Institute of International Finance suggest that global sovereign debt could rise by a third by 2028 (to $130tn) amid continued large government budget deficits. While the so-called bond vigilantes for now keep their powder dry, the BIS warned that policymakers should not wait for markets to wake up and start adjusting policies in time.

Norwegian inflation eased less than expected in November. The headline index fell from 2.6% to 2.4% on a 0.3% m/m pace. Housing, water & energy were among the main drivers, rising 1.1% m/m, followed by health (0.5% m/m) and clothing & footwear (0.5%). Transport and household equipment were among the biggest drags (both -0.4% m/m) even though both did support the y/y print. Core inflation broke a year-long easing streak with an acceleration from 2.7% to 3%. The numbers were higher than analysts expected but didn’t come as a surprise to the Norwegian central bank. The Norges Bank had penciled in 2.6% for headline and 3% for core. The central bank in November said it expects the current policy rate to remain unchanged at 4.5% through the end of the year. Markets have been aligning neatly with this guidance and do not see today’s numbers as a key reason to change tack ahead of the December 19 meeting. Stronger-than-expected Q3 GDP growth, low & stable unemployment and especially a still-weak Norwegian krone are key arguments for the Norges Bank to proceed cautiously with rate cuts. EUR/NOK trades little changed around 11.72. This compares to the recent highs (NOK lows) around 12, surpassed only during the pandemic-driven liquidity crunch in early 2020.

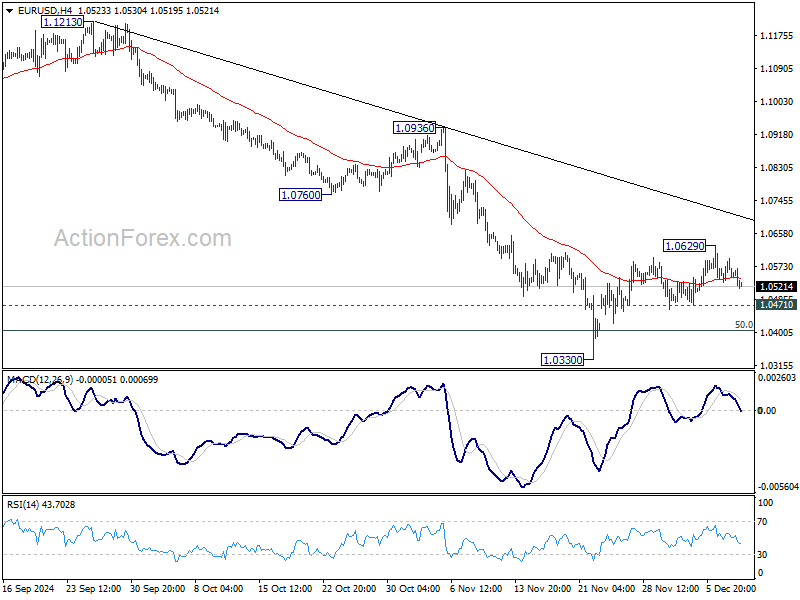

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0526; (P) 1.0560; (R1) 1.0589; More...

Intraday bias in EUR/USD stays neutral and outlook is unchanged. Rebound from 1.0330 short term bottom could still extend higher. But outlook will remain bearish as long as 55 D EMA (now at 1.0711) holds. On the downside, break of 1.0471 minor support will turn bias to the downside for retesting 1.0330 low. Firm break of 1.0330 will resumed the decline from 1.1213, and sustained trading below 1.0404 key fibonacci level will carry larger bearish implication.

In the bigger picture, focus stays on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.

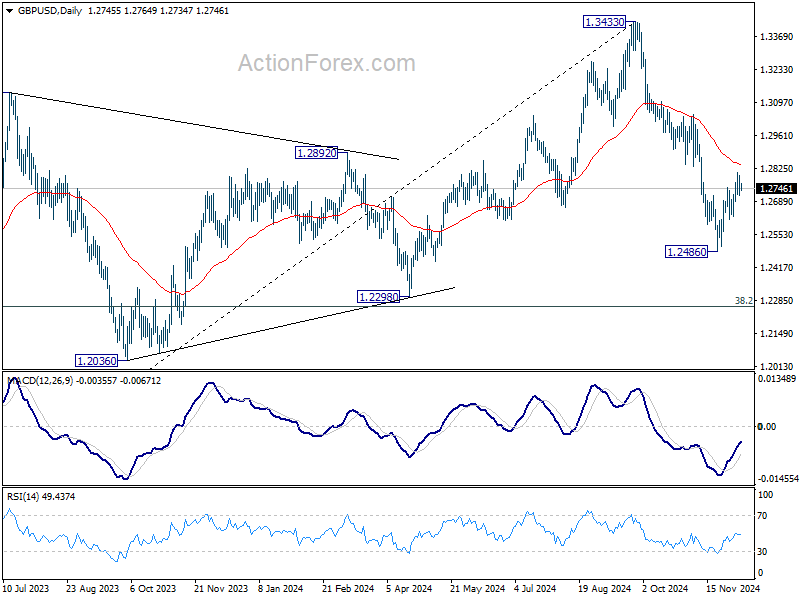

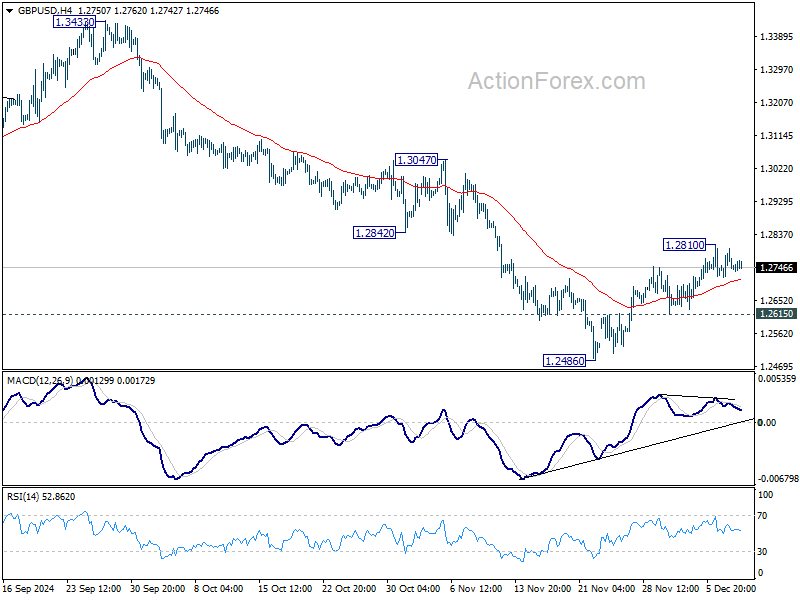

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2712; (P) 1.2756; (R1) 1.2794; More...

Intraday bias in GBP/USD stays neutral and outlook is unchanged. Rebound from 1.2486 short term bottom could still extend higher. But outlook will stay bearish as long as 55 D EMA (now at 1.2839) holds. On the downside, below 1.2615 minor support will bring retest of 1.2486 first. Firm break there will target 1.2298 cluster support zone. However, sustained break of 55 D EMA will argue that the near term trend has reversed, and targets 1.3047 resistance for confirmation.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern.