Sample Category Title

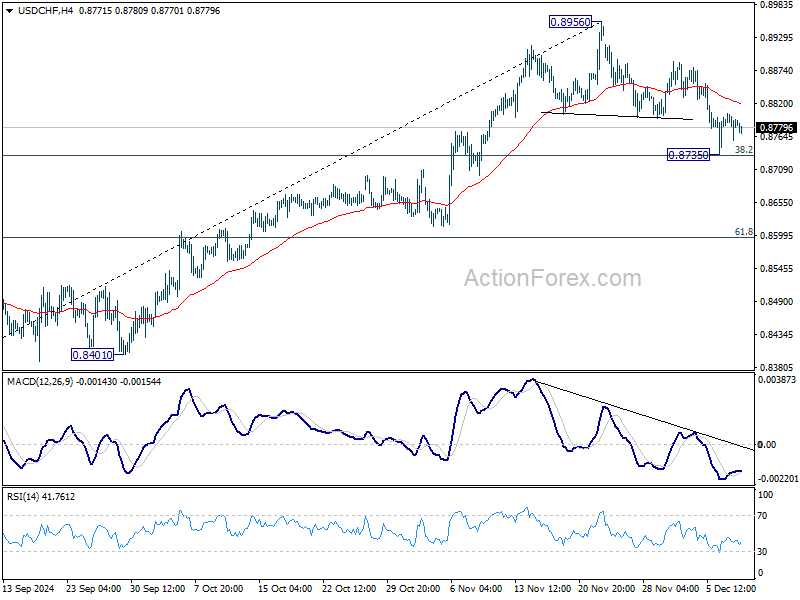

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8763; (P) 0.8784; (R1) 0.8808; More…

Outlook in USD/CHF remains unchanged for now. Corrective fall from 0.8956 could have completed at 0.8735 after hitting 55 D EMA. Further rally is in favor to retest 0.8956 high first. However, considering head and shoulder top pattern, firm break of the EMA will argue that whole rise from 0.8401 might have completed, and bring deeper decline to 61.8% retracement of 0.8401 to 0.8956 at 0.8613 next.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

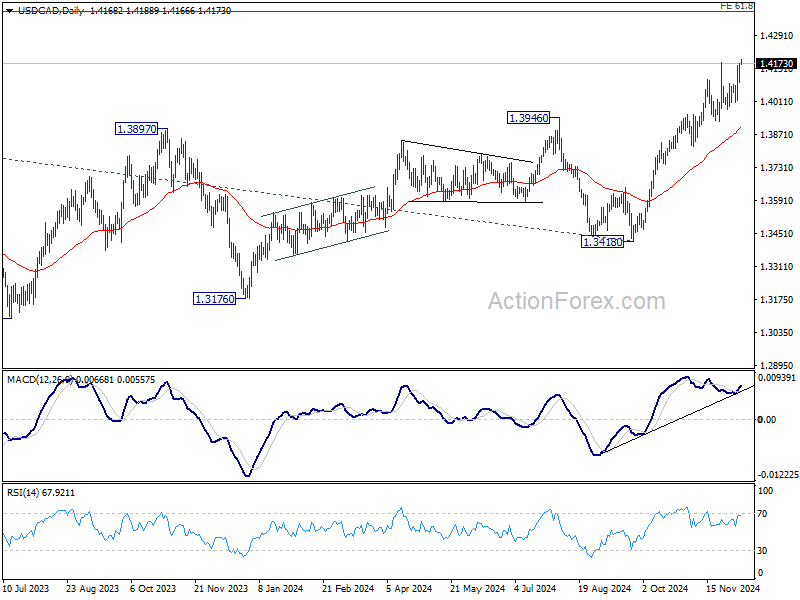

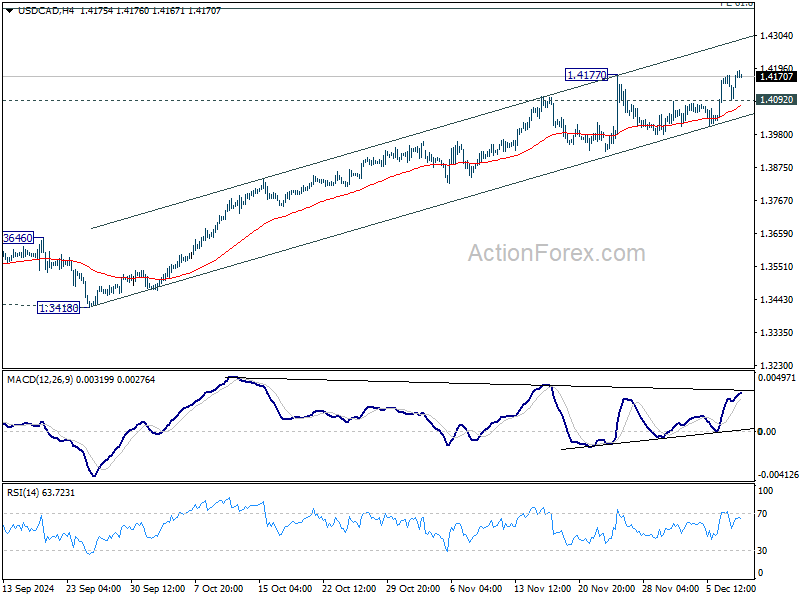

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4118; (P) 1.4147; (R1) 1.4200; More...

USD/CAD's breach of 1.4177 resistance suggests that larger up trend is resuming. Intraday bias is back on the upside for further rally to 1.4391 projection level. On the downside, below 1.4092 minor support will delay the bullish case, and bring more consolidations first, before staging another rally.

In the bigger picture, up trend from 1.2005 (2021) is in progress. Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391. Now, medium term outlook will remain bullish as long as 1.3418 support holds, even in case of deep pullback.

Expect More Sentiment-Driven Trading Today

Markets

The Chinese Politburo’s directive changed risk sentiment at the start of European trading from slightly risk-off because of developments in Syria to mildly risk-on given the firm commitment to support the ailing economy. Extraordinary countercyclical fiscal measures will be complemented by a “moderately loose” monetary policy stance (“prudent” since 2011) with a firm commitment to stabilize both the stock market and the property sector. The Chinese annual Central Economic Work conference starts on Wednesday and could offer more clues on targeted measures to boost growth. Risk sentiment deteriorated into the European close as US stock markets corrected especially in the tech/AI-sector. EUR/USD hovered up and down 1.0550 without clear direction. US Treasuries underperformed German Bunds without specific driver. The NY Fed consumer survey (see below) might have played in the run-up to tomorrow’s November CPI print. Daily changes on the US yield curve ranged between +2.1 bps (2-yr) and + 5.1 bps (7-yr). The German yield curve bear steepened with yields rising up to 3.2 bps (30-yr). The very long end of the European curve shows some early signs of fatigue following an astonishing rally since the end of October.

Today’s agenda is again very thin with only NFIB small business optimism and the start of the US Treasury’s mid-month refinancing operation ($58bn 3-yr Note). Tomorrow’s $39bn 10-yr Note and Thursday’s $22bn 30-yr Bond auction will draw more attention in light of the uncertain spending agenda by US president-elect next year. We expect more sentiment-driven trading today going into US CPI and the ECB meeting later this week. Especially European bonds could be prone for some technical correction at the longer end of the curve. The euro’s rebound potential is blocked around EUR/USD 1.06 by a likely dovish ECB outcome.

News & Views

The NY Fed’s November consumer inflation survey showed expectations rising slightly (+0.1 ppt) at the short-, medium- and longer-term horizons. One-year-ahead inflation expectations increased to 3%, the three-year-ahead gauge increased to 2.6% and the five-year-ahead one to 2.9%. Uncertainty around future outcomes picked up as well. Polled about the labour market, US consumers anticipate their earnings to grow by 3% (+0.2 ppts), extending the narrow 2.7-3% range in place since the start of the year. Expectations of the unemployment rate being higher one year from now rose to 35%, remaining well below the trailing 12-month average of 37%. On the topic of household finances, US families think their income will gain by 3.1%, the mid of the 2.9-3.3% range since January 2023. They believe spending will grow less quickly than in October but at a pace still above pre-pandemic levels (4.7%). The US consumer is optimistic on its financial situation one year ahead from now. The share of households expecting it to be better rose to the highest level since February 2020.

The Reserve Bank of Australia’s rate status quo was accompanied by some dovish twists. It took note of the recently published Q3 GDP growth figures which were - outside of the pandemic period - the slowest since the early 1990s. Data in general since the November policy meeting has been “on balance softer than expected”. The RBA said underlying inflation remains too high (3.5% in the September quarter). It referred to the November forecasts which penciled in a return to the 2.5% midpoint target not before 2026. While recent data are still consistent with these projections, the RBA said it is gaining some confidence that inflation is moving sustainably towards target. Policy is working as intended and some of the upside risks are easing. The level of aggregate demand is still above supply capacity but that gap is easing. The combination of these additions to the statement led to the removal of the sentence “This reinforces the need to remain vigilant to upside risks to inflation and the Board is not ruling anything in or out”. The clear dovish accents didn’t go by unnoticed. Australian swap yields tumble more than 10 bps at the front end of the curve with bets for a February rate cut rising. The Aussie dollar wipes out yesterday’s China-driven gains to trade back to the recent lows around AUD/USD 0.64. RBA governor Bullock in the press conference tried to offer some counterweight. She expected the current market repositioning but does not endorse it.

The Best Defense is a Good Offense

Sentiment in Chinese equities reversed suddenly to a significantly more bullish state after the Politburo – which is the highest-decision making bodies within the Communist Party – pledged to embrace a ‘moderately loose’ monetary policy in 2025. This is a meaningful dovish shift from the ‘prudent’ stance of the past 14 years, hinting that further interest and reserve rate cuts are on the menu of next year. As a result, the Chinese 10-year bond yield slipped to a record high, and the Chinese equities jumped more than 3% at the open. Now, all eyes are on the Central Economic Work Conference, where the Chinese officials will discuss behind closed doors and ideally complement the monetary support with juicy fiscal support.

Time to buy? It’s tempting to buy Chinese assets at significant discount. Alibaba, for example, jumped more than 7% on stimulus news yesterday in New York trading, but – or if you prefer ‘and’ – the company is down by 70% since its 2020 peak. Its PE ratio is just around 12 right now, compared to Amazon that trades more than 46 times its earnings. But it will take at least a few good economic reports to convince long-term investors that what’s been put in place is bearing fruit. After all, 2024 was marked by stimulus hints that led to a market rally, but resulted in disappointing stimulus measures and a selloff.

The best defense is a good offense

Chinese companies reportedly cut off key supplies to the US and Europe necessary to build unmanned aerial vehicles for example, and the country opened a probe into Nvidia accusing the company for breaking their antimonopoly laws in the acquisition of Mellanox Technologies back in 2020. The latter could cost Nvidia as much as 10% of its prior year revenue of around $60bn – a massive $6bn fine. Nvidia shares took the hit yesterday: they fell 2.6%. Good news is, the percentage of Nvidia revenues that come from China has more than halved compared to pre-chip war levels. Being left in the crossfire is never good news, but the impact of the additional events decreases as the company gradually steps out of a market that’s once been so promising and lucrative.

FX and commodities

Gold is up after a few stagnant weeks on news that the People’s Bank of China (PBoC) resumed buying gold after a 6-month pause – certainly to back a looser monetary policy and maybe to decrease exposure to US treasuries. The price of an ounce is testing the 50-DMA offers right now, near $2700 level, with potential to extend gains on the back of strong global political, geopolitical and economic uncertainties.

Crude oil, on the other hand, remained capped into the $69pb level at yesterday’s rally fueled by Syrian uncertainty and hopes of Chinese stimulus. The bulls' inability to capitalize on this mix of geopolitical tension and economic optimism underscores the prevailing strength of the bearish tide in the oil market. A further selloff to $65/67ob range is plausible.

Iron ore extended its advance to a 2-month high on Chinese stimulus hope but reversed early gains, while the AUDUSD couldn’t benefit from the Chinese news as the Reserve Bank of Australia (RBA) kept its policy rate unchanged at today’s meeting as expected, but sounded more dovish than expected. The officials, there, said that they are gaining some confidence that inflation pressures are easing. As a result, the AUD bulls may be losing an important ally but the RBA’s hawkish stance so far did little to limit the Aussie’s selloff. China’s ability to boost growth is more influent than what the RBA does.

Elsewhere, the US dollar extended gains yesterday, driven higher by flight to safety, but the greenback is softer this morning. The EURUSD saw support near 1.0530 on Monday, the USDJPY is preparing to test the 50-DMA to the upside – near 151 level and Cable is flirting with the 1.28 offers. While the Bank of England’s (BoE) more cautious stance due to the government’s pledge to extend spending looks supportive, the negative impact of the tax rises are being felt before the positive impact of spending on the economy. The latter could convince the BoE to adopt a more supportive policy and cap sterling’s upside potential against the greenback. But the pound should remain bid against the euro, aiming a further advance toward the 82 cents level as the US tariffs are expected to hit the EU economies more than they are expected to hit the UK’s.

Scandi Releases and China in Focus Overnight

In focus today

In Norway, we expect core inflation to remain unchanged at 2.7% y/y in November, a tad lower than consensus at 2.8%. If we are proven right, this will once again be below Norges Bank's forecast from the latest MPR at 3.0%, and in isolation contribute to a downward revision of the rate path in the upcoming MPR. The risk to our forecast is if the increase in prices ahead of Black Week was larger than last year.

In Sweden, at 08:00 CET the SCB releases October GDP, production and consumption indicators. With both PMIs above 50 and consumer confidence going in a more positive direction in recent months, we expect positive m/m readings.

Overnight China starts the annual Central Economic Work Conference (CEWC) where the top leadership discusses and lays out economic priorities for the next year. It is a two-day meeting so we will likely not hear much until tomorrow (for more details see below).

Economic and market news

What happened overnight

In Australia, the Reserve Bank of Australia (RBA) kept its monetary policy unchanged overnight as expected. Markets were pricing in a very slim probability of a rate cut ahead of the meeting, but Governor Bullock noted that RBA did not even discuss cutting rates today. However, RBA's forward guidance was more dovish than before. It delivered no new economic forecasts, but still confirmed that the board had gained more confidence on inflation returning to target. RBA also acknowledged the recent downside surprise in Q3 GDP and Bullock did not write off the possibility of a cut at the next meeting in February. This pushed AUD/USD lower near 0.64, as markets are now pricing in 55% likelihood of the first cut in February. We have maintained a downward-sloping forecast profile for AUD/USD, but the current level is not far away from our 12M target of 0.63.

In China, exports slowed in November to 6.7% y/y (cons: 8.5%), while imports fell markedly below expectations to -3.9% y/y (cons: 0.3%) - the weakest print in nine months. This points to economic strain amid looming U.S. tariffs under incoming President Trump, highlighting the need for stronger domestic stimulus measures. More clarity on this may emerge following yesterday's Politburo meeting and the upcoming CEWC meeting.

What happened yesterday

In the euro area, the Sentix indicator declined to -17.5 in December from -12.8, marking the lowest level this year after rebounding in the past months.

In China, the Politburo held a meeting ahead of the CEWC meeting overnight, where they vowed to implement a "more active" set of tools to expand domestic demand in 2025. They also cited that the property market would stabilise. Interestingly, the Politburo altered course - for the first time since 2009 - emphasizing that monetary policy would be moderately loose, in contrast to their usual expression of "prudent". At the same time, they also stated that fiscal policy would become more active in tandem with a strengthening of the extraordinary counter-cyclical adjustment.

In continuation of the akin policy message in September, this underscores that the economy now has a higher priority for China's top leadership. With the outlook of trade war with the US, China's leaders likely see an even bigger need to deal with the struggling domestic economy more forcefully. Hence, a looming trade war could be a blessing in disguise for China.

Equities: Global equities were lower yesterday, primarily dragged down by the US, while other regions, including Europe were higher. It was a relatively slow start to the week, but we anticipate busier days ahead with a focus on central banks. With the US underperforming, we also had defensives outperforming cyclicals following a significant underperformance last week. Similarly, the VIX ticked higher, which could be seen as indicative of a risk-off mode. However, we interpret this more as a sign that recent movements have been overly rapid, rather than a fundamental shift in the narrative. In the US yesterday: Dow -0.5%, S&P 500 -0.6%, Nasdaq -0.6%, and Russell 2000 -0.7%. This morning, the picture is mixed in Asia, with China outperforming, buoyed by renewed hopes for stimulus. US and European futures are currently lower.

FI: Global rates rose through yesterday's uneventful session, reversing the declines seen on Friday following the NFP. The 10Y US Treasury yield rose 5bp throughout the day, while the short end of the US curve was less changed with markets still discounting 22bp of cuts at next week's meeting. EGB yields saw only marginal moves throughout Monday with no important data releases and the ECB in silence mode ahead of the Thursday decision. The 5y5y EUR inflation swap rate crept back below 2% as energy prices declined. This is certainly being noticed at the ECB, where the risk of undershooting medium-term target has gained attention recently.

FX: A quiet start to the week with no significant moves in G10 FX. EUR/USD remains range-bound in the mid-1.05 to 1.06 area. The JPY weakened as markets question whether the Band of Japan will proceed with a hike next week. Scandies gained against the EUR, with EUR/SEK dropping below 11.55 and EUR/NOK slipping below 11.75.

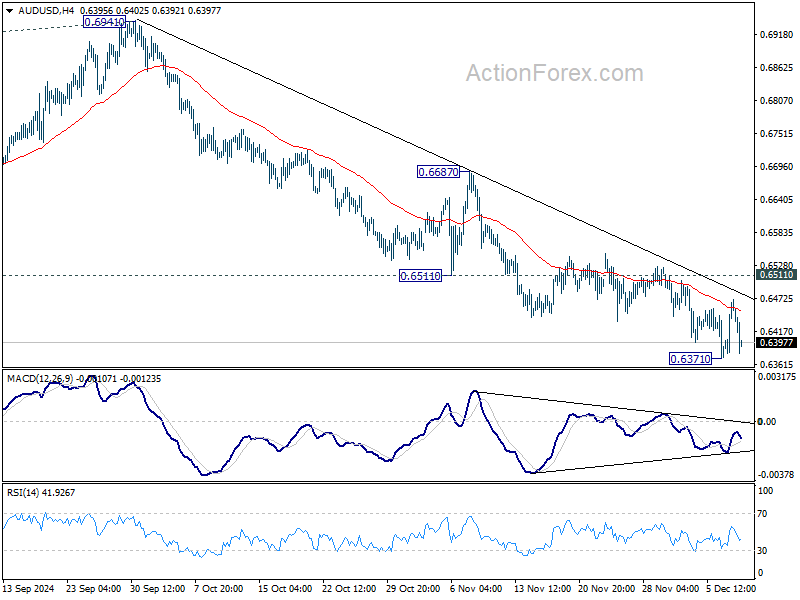

AUD/USD Daily Report

Daily Pivots: (S1) 0.6390; (P) 0.6430; (R1) 0.6481; More...

Volatility continues in AUD/USD but it's still staying in range above 0.6371 temporary low. Intraday bias remains neutral and further decline is expected with 0.6511 resistance intact. On the downside, below 0.6371 will resume the fall from 0.6941 to 0.6348 support, and then 0.6269. Nevertheless, considering bullish convergence condition in 4H MACD, firm break of 0.6511 will confirm short term bottoming, and turn bias back to the upside for 55 D EMA (now at 0.6568) next.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006. More sideway trading could be seen above 0.6169, but overall outlook will stay bearish as long as 0.6941 resistance holds. Firm break of 0.6169 will resume the down trend to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next.

Aussie Falls on RBA Dovish Shift; China’s Stimulus Optimism Wanes

Australian Dollar dropped sharply in Asian session following a significant dovish turn in RBA's communication. After holding rates steady at 4.35%, the central bank signaled growing confidence that inflationary pressures are easing, marking a departure from its previously vigilant tone. While May remains the most likely timing for a rate cut according to many economists, traders are increasingly pricing in a February reduction, now seen as a real possibility.

Meanwhile, optimism around China's economic stimulus faded as markets shrugged off state media reports of President Xi Jinping's “full confidence” in achieving economic growth targets. Hong Kong stocks remained subdued, reflecting the market's demand for more concrete and actionable measures from policymakers. The upcoming Central Economic Work Conference is now in focus, with investors seeking clarity on 2025 economic priorities and strategies. Without substantive developments, sentiment around China’s recovery efforts may remain tepid.

Overall in the currency markets, Aussie is the day’s weakest currency so far, closely followed by Kiwi and then Dollar. On the other hand, Swiss Franc is the strongest performer, with Euro and Sterling also gaining ground. Canadian Dollar and Yen showed mixed performances.

Technically, USD/CAD's breach of 1.4177 resistance suggests that larger up trend is resuming. Further rise is now in favor as long as 1.4092 support holds. Next target is medium term projection level at 1.4391.

In Asia, Nikkei rose 0.43%. Hong Kong HSI is up 0.17%. China's Shanghai SSE is up 0.74%. Singapore Strait Times is up 0.56%. Japan 10-year JGB yield is up 0.0223 at 1.064. Overnight, DOW fell -0.54%. S&P 500 fell -0.61%. NASDAQ fell -0.62%. 10-year yield rose 0.048 to 4.199.

RBA holds rates steady, dovish shift raises odds of Feb cut

RBA held its cash rate steady at 4.35% as widely expected, but the accompanying statement marked a clear pivot towards a more dovish stance. While May remains the more likely timing for the first rate cut, February is now emerging as a real possibility, depending on upcoming Q4 jobs and inflation data from Australia.

The most striking change in the RBA's statement was its removal of the phrase "not ruling anything in or out" regarding future monetary policy decisions. This change aligns with the board's growing "confidence that inflationary pressures are declining." RBA acknowledged that some upside risks to inflation have eased and noted the gap between aggregate demand and supply capacity is continuing to narrow.

Recent activity data, according to the RBA, has been “on balance softer than expected,” with the central bank pointing out risks of a slower-than-anticipated recovery in consumer spending. These factors collectively suggest a step away from inflation vigilance and a move closer to easing policy.

Governor Michele Bullock later emphasized that the wording adjustments in the statement were deliberate. While she clarified that a rate cut was not discussed during today's meeting, she acknowledged uncertainty over whether one could occur as early as February.

Markets responded swiftly, with swaps traders raising the probability of a February rate cut to over 60%, up from 50% the previous day. Market expectations now fully price in two rate reductions by May.

Australia’s NAB confidence turns negative to -3 as business conditions deteriorate

Australia’s NAB Business Confidence index slid sharply to -3 in November, down from 5 in October, returning to below average levels. Business conditions also weakened notably, dropping from 7 to 2, marking declines across trading, profitability, and employment metrics. Trading conditions fell to 5 from 13, profitability shifted into negative territory at -1 from 5, and employment conditions edged down to 2 from 3.

Cost pressures showed little relief, with input costs largely unchanged. Labor cost growth held steady at 1.4% in quarterly terms, while purchase cost growth edged slightly higher by 0.2 percentage points to 1.1%. On the pricing side, output price growth remained unchanged at 0.6% in quarterly terms, with retail price growth retreating to 0.6% and recreation and personal services easing slightly to 0.7%.

China's trade data highlights persistent import weakness amid export slowdown

China's trade data for November showed weak signals as exports grew 6.7% yoy to USD 312.3B, down sharply from October's 12.7% yoy expansion and missing expectations of 8.5% growth.

Export performance varied across key regions, with shipments to the US rising 8% yoy, to the EU up 7.2% yoy, and to ASEAN growing by 14.9% yoy. However, exports to Russia declined by -2.5% yoy.

On the import side, the picture was decidedly more negative. Imports fell by -3.9% yoy, marking the steepest decline since September 2023, and missing expectations of a slight 0.3% yoy increase.

Weakness was broad-based, with imports from ASEAN dropping -3% yoy, the US contracting by -11% yoy, and the EU and Russia both registering declines of -6.5% yoy. These numbers underscore persistent weak domestic demand, consistent with recent data showing subdued consumer inflation.

Trade balance widened from USD 95.7B to 97.4B, above expectation of USD 92.0B.

Looking ahead

Germany CPI final will be released in European session. Later in the day, US will release NFIB business optimism and non-farm productivity Q3.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6390; (P) 0.6430; (R1) 0.6481; More...

Volatility continues in AUD/USD but it's still staying in range above 0.6371 temporary low. Intraday bias remains neutral and further decline is expected with 0.6511 resistance intact. On the downside, below 0.6371 will resume the fall from 0.6941 to 0.6348 support, and then 0.6269. Nevertheless, considering bullish convergence condition in 4H MACD, firm break of 0.6511 will confirm short term bottoming, and turn bias back to the upside for 55 D EMA (now at 0.6568) next.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006. More sideway trading could be seen above 0.6169, but overall outlook will stay bearish as long as 0.6941 resistance holds. Firm break of 0.6169 will resume the down trend to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next.

RBA Remains on Hold, Slowly Gaining Confidence

The RBA remains on hold with the cash rate kept at 4.35%. But the Board is gaining confidence in its own forecasts that inflation is coming down.

As expected, the RBA Board held the cash rate steady at 4.35% following its meeting this week. The Board remains concerned that underlying inflation remains above target, with the key trimmed mean measure at 3.5% over the year to the September quarter. It infers from this level of inflation that aggregate demand continues to outstrip aggregate supply. The Board is therefore resolved to keep monetary policy restrictive until it is clear inflation is returning to target on the desired timetable.

It still expects that it will be ‘some time yet’ before inflation returns sustainably to the 2–3% target and approaches the midpoint of 2½%. However, it has changed its language and is no longer saying that it is ‘not ruling anything in or out’, as it had in every statement since March. The word ‘vigilant’ has also been cut from the post-meeting statement. Rather, the Board is ‘gaining some confidence that inflationary pressures are declining in line with these recent forecasts’. In other words, we are getting closer to the point that the RBA will be comfortable cutting rates. And in a shift in view that will surprise almost nobody, it no longer feels the need to flag the possibility of a rate hike. The post-meeting statement highlighted that ‘some of the upside risks to inflation appear to have eased’.

Indeed, some of the Governor’s answers in the post-meeting media conference opened the door to a more dovish view than we have seen from the Bank recently, including in her most recent speech. That said, her opening statement and answers today continued to emphasise the RBA’s assessment that aggregate demand exceeds aggregate supply and the current level of (trimmed mean) inflation is the best indicator of where that balance lies.

The Board assesses that monetary policy is ‘working as expected’ in bringing demand and supply into alignment, with the gap between the two continuing to close. Although there was still a nod to weak productivity growth, the post-meeting statement also highlighted the downside risks to household consumption and thus overall growth and the labour market.

Since the last Board meeting, Wage Price Index (WPI) and national accounts data have been released. The WPI data was noticeably softer than would be required to meet the RBA’s November forecast for growth over 2024, as we noted at the time. Similarly, although the RBA did flag that it expected consumption to be flat in the September quarter, GDP overall was softer than consensus and, we suspect, the RBA’s own expectations. (The RBA only publishes forecasts for June and December quarters, not the intervening March and September quarters.) A Q4 bounce large enough to match the RBA’s forecasts for 2024 growth is unlikely to eventuate for either series. Further downgrades to the RBA’s near-term forecasts can therefore be expected in the February round.

In today’s statement, the Board acknowledged that wage pressures had eased more than it previously expected. During the media conference, the Governor initially sought to characterise the data flow as showing the ‘real-side’ data (output, consumption) as soft but the nominal side – inflation – as still too high. It was only after some further questioning that the downside surprise on wages growth – an important nominal variable – got a mention.

Similar to earlier RBA communications, the Board statement pointed to the apparent stabilisation in the unemployment rate and some other measures of labour market tightness as signs that the labour market was still in a state of more than full employment. Indeed, the language of the paragraph on the labour market was only minimally changed from last month, bar some minor factual updates and a decision not to start a sentence with ‘But’.

The concentration of recent employment growth in the non-market sector did not rate a mention in the post-meeting statement. In the media conference, however, the Governor was asked about the risk that employment growth in the non-market sector slows. So far, the RBA seems content to rely on other sectors bouncing back in time, along with household consumption. We hope it is right, but we are not confident that handover will happen quickly enough.

Overall, the tone of today’s communication was less hawkish than the November round, appropriately so given the data flow since then. The ‘more than one good quarter’ language from the November minutes has again been clarified to indicate that other data matter, too, rather than the meaning some observers took (‘at least two quarters of good CPI data from here’). As we noted at the time, even if that was the right interpretation, things can pivot quickly if the data flow demands it.

We have recently revised our view of the likely path of the cash rate to a base case of a first cut in May. As we said at the time, though, we cannot entirely rule out an earlier start date of 18 February or 1 April should outcomes continue to undershoot the RBA’s expectations, especially for trimmed mean inflation. Today’s change of language represents a welcome acknowledgement that disinflation remains on track and that we are getting closer to the point that some of the current policy restrictiveness can be withdrawn. And in the media conference, the Governor conceded that there were scenarios in which the Board ended up cutting in February, while prudently choosing not to describe one.

In acknowledging that reality, the RBA has clearly tilted the probabilities back towards an earlier start date for the rate-cutting phase than where it stood a few weeks ago. It does not, however, shift that balance of probabilities enough to change our base case to be earlier than May just yet. The RBA still assess aggregate demand as exceeding aggregate supply. While ever it continues to believe this, it will be cautious about embarking on rate cuts. Any shifts back towards an earlier timetable depend on the data flow from here, especially on the labour market and trimmed mean inflation.

China’s trade data highlights persistent import weakness amid export slowdown

China's trade data for November showed weak signals as exports grew 6.7% yoy to USD 312.3B, down sharply from October's 12.7% yoy expansion and missing expectations of 8.5% growth.

Export performance varied across key regions, with shipments to the US rising 8% yoy, to the EU up 7.2% yoy, and to ASEAN growing by 14.9% yoy. However, exports to Russia declined by -2.5% yoy.

On the import side, the picture was decidedly more negative. Imports fell by -3.9% yoy, marking the steepest decline since September 2023, and missing expectations of a slight 0.3% yoy increase.

Weakness was broad-based, with imports from ASEAN dropping -3% yoy, the US contracting by -11% yoy, and the EU and Russia both registering declines of -6.5% yoy. These numbers underscore persistent weak domestic demand, consistent with recent data showing subdued consumer inflation.

Trade balance widened from USD 95.7B to 97.4B, above expectation of USD 92.0B.

Australia’s NAB confidence turns negative to -3 as business conditions deteriorate

Australia’s NAB Business Confidence index slid sharply to -3 in November, down from 5 in October, returning to below average levels. Business conditions also weakened notably, dropping from 7 to 2, marking declines across trading, profitability, and employment metrics. Trading conditions fell to 5 from 13, profitability shifted into negative territory at -1 from 5, and employment conditions edged down to 2 from 3.

Cost pressures showed little relief, with input costs largely unchanged. Labor cost growth held steady at 1.4% in quarterly terms, while purchase cost growth edged slightly higher by 0.2 percentage points to 1.1%. On the pricing side, output price growth remained unchanged at 0.6% in quarterly terms, with retail price growth retreating to 0.6% and recreation and personal services easing slightly to 0.7%.