Sample Category Title

RBA holds rates steady, dovish shift raises odds of Feb cut

RBA held its cash rate steady at 4.35% as widely expected, but the accompanying statement marked a clear pivot towards a more dovish stance. While May remains the more likely timing for the first rate cut, February is now emerging as a real possibility, depending on upcoming Q4 jobs and inflation data from Australia.

The most striking change in the RBA's statement was its removal of the phrase "not ruling anything in or out" regarding future monetary policy decisions. This change aligns with the board's growing "confidence that inflationary pressures are declining." RBA acknowledged that some upside risks to inflation have eased and noted the gap between aggregate demand and supply capacity is continuing to narrow.

Recent activity data, according to the RBA, has been “on balance softer than expected,” with the central bank pointing out risks of a slower-than-anticipated recovery in consumer spending. These factors collectively suggest a step away from inflation vigilance and a move closer to easing policy.

Governor Michele Bullock later emphasized that the wording adjustments in the statement were deliberate. While she clarified that a rate cut was not discussed during today's meeting, she acknowledged uncertainty over whether one could occur as early as February.

Markets responded swiftly, with swaps traders raising the probability of a February rate cut to over 60%, up from 50% the previous day. Market expectations now fully price in two rate reductions by May.

(RBA) Statement by the Reserve Bank Board: Monetary Policy Decisions

At its meeting today, the Board decided to leave the cash rate target unchanged at 4.35 per cent and the interest rate paid on Exchange Settlement balances unchanged at 4.25 per cent.

Underlying inflation remains too high.

Inflation has fallen substantially since the peak in 2022, as higher interest rates have been working to bring aggregate demand and supply closer towards balance. Measures of underlying inflation are around 3½ per cent, which is still some way from the 2.5 per cent midpoint of the inflation target.

The most recent forecasts published in the November Statement on Monetary Policy (SMP) do not see inflation returning sustainably to the midpoint of the target until 2026. The Board is gaining some confidence that inflationary pressures are declining in line with these recent forecasts, but risks remain.

The outlook remains uncertain.

While underlying inflation is still high, other recent data on economic activity have been mixed, but on balance softer than expected in November.

Growth in output has been weak. National accounts for the September quarter show that the economy grew by only 0.8 per cent over the past year. Outside of the COVID-19 pandemic, this is the slowest pace of growth since the early 1990s. Past declines in real disposable income and the ongoing effect of restrictive financial conditions continued to weigh on household consumption spending, particularly on discretionary items.

A range of indicators suggest that labour market conditions remain tight; while those conditions have been easing gradually, some indicators have recently stabilised. The unemployment rate was 4.1 per cent in October, up from 3.5 per cent in late 2022. That said, employment grew strongly over the three months to October, the participation rate remains close to record highs, vacancies are still relatively high and average hours worked have stabilised. At the same time, some cyclical labour market indicators, including youth unemployment and underemployment rates, have recently declined.

Wage pressures have eased more than expected in the November SMP. The rate of wages growth as measured by the Wage Price Index was 3.5 per cent over the year to the September quarter, a step down from the previous quarter, but labour productivity growth remains weak.

Taking account of recent data, the Board’s assessment is that monetary policy remains restrictive and is working as anticipated. Some of the upside risks to inflation appear to have eased and while the level of aggregate demand still appears to be above the economy’s supply capacity, that gap continues to close.

The central projection is for growth in household consumption to increase as income growth rises. September quarter data suggest that both incomes and consumption had recovered a little slower than forecast, but more recent information has suggested a pick-up in consumption in October and November. There is a risk that any pick-up in consumption is slower than expected, resulting in continued subdued output growth and a sharper deterioration in the labour market. More broadly, there are uncertainties regarding the lags in the effect of monetary policy and how firms’ pricing decisions and wages will respond to the slow growth in the economy and weak productivity outcomes at a time of excess demand, and while conditions in the labour market remain tight.

There remains a high level of uncertainty about the outlook abroad. Most central banks have eased monetary policy as they become more confident that inflation is moving sustainably back towards their respective targets. They note, however, that they are removing only some restrictiveness and remain alert to risks in both directions, namely weaker labour markets and stronger inflation. Geopolitical uncertainties remain pronounced.

Sustainably returning inflation to target is the priority.

Sustainably returning inflation to target within a reasonable timeframe remains the Board’s highest priority. This is consistent with the RBA’s mandate for price stability and full employment. To date, longer term inflation expectations have been consistent with the inflation target and it is important that this remains the case.

While headline inflation has declined substantially and will remain lower for a time, underlying inflation is more indicative of inflation momentum, and it remains too high. The November SMP forecasts suggest that it will be some time yet before inflation is sustainably in the target range and approaching the midpoint. Recent data on inflation and economic conditions are still consistent with these forecasts, and the Board is gaining some confidence that inflation is moving sustainably towards target.

The Board will continue to rely upon the data and the evolving assessment of risks to guide its decisions. In doing so, it will pay close attention to developments in the global economy and financial markets, trends in domestic demand, and the outlook for inflation and the labour market. The Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that outcome.

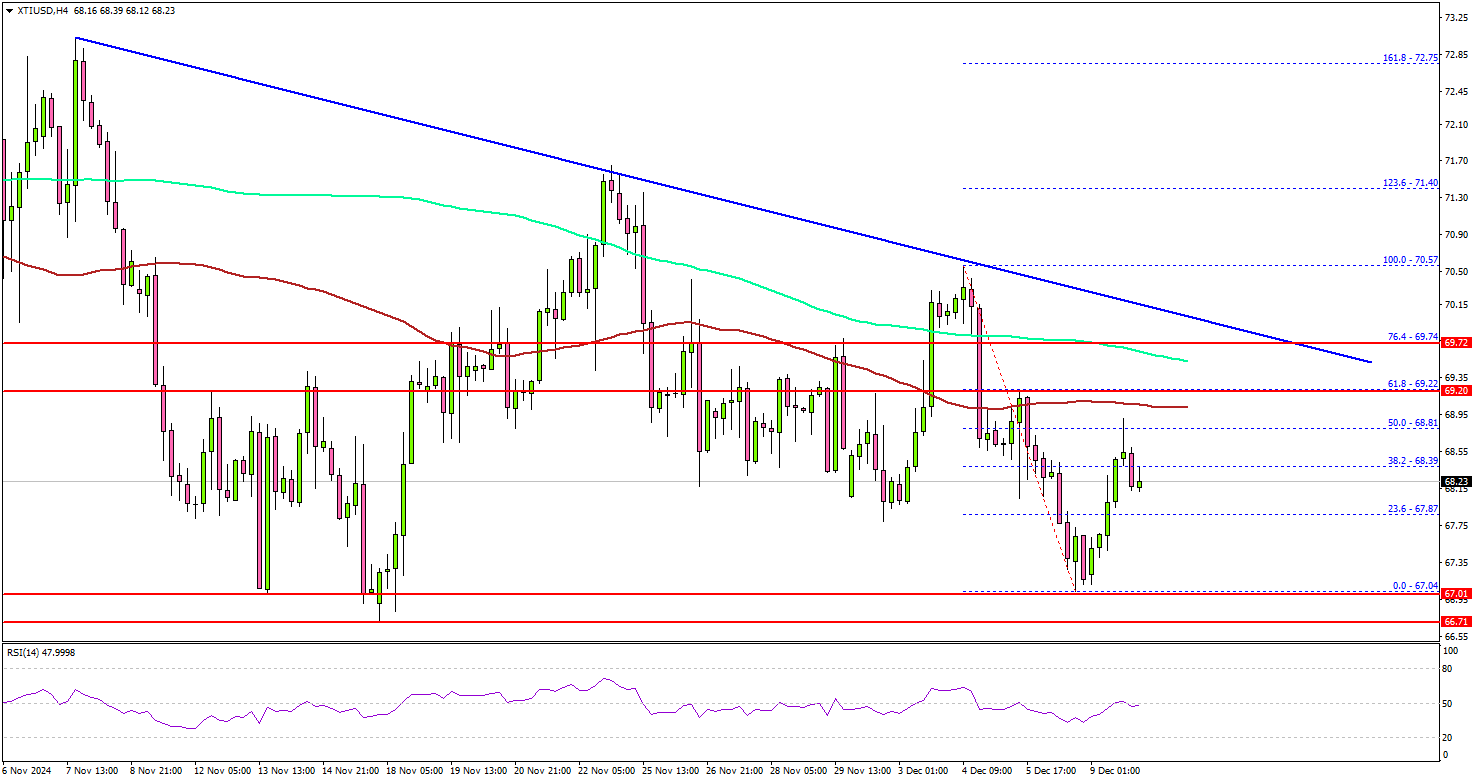

WTI Crude Oil Faces Resistance: Can Recovery Take Hold?

Key Highlights

- WTI Crude Oil prices are struggling to recover above the $70.00 resistance zone.

- A connecting bearish trend line is forming with resistance at $69.75 on the 4-hour chart.

- Gold prices could advance if there is a clear move above $2,700.

- EUR/USD must surpass 1.0700 to gain bullish momentum.

WTI Crude Oil Price Technical Analysis

WTI Crude Oil price found support near the $67.00 zone. A base was formed and the price started a short-term recovery wave above $68.00.

Looking at the 4-hour chart of XTI/USD, the price traded above the 38.2% Fib retracement level of the downward move from the $70.57 swing high to the $67.04 low. It seems like the bulls are facing hurdles near the $70.00 zone.

The price is also below the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). There is also a connecting bearish trend line forming with resistance at $69.75 on the same chart.

The trend line is close to the 76.4% Fib retracement level of the downward move from the $70.57 swing high to the $67.04 low. The main hurdle is still near the $70.00 zone, above which the price may perhaps accelerate higher.

In the stated case, it could even visit the $71.50 resistance. Any more gains might call for a test of the $72.80 resistance zone in the near term.

On the downside, the first major support sits near the $67.80 zone. A daily close below $67.80 could open the doors for a larger decline. The next major support is $66.00. Any more losses might send oil prices toward $65.00 in the coming days.

Looking at Gold, there was a steady increase above the $2,650 level and the bulls could now aim for a move above $2,700.

Economic Releases to Watch Today

- US Nonfarm Productivity for Q3 2024 - Forecast +2.2%, versus +2.2% previous.

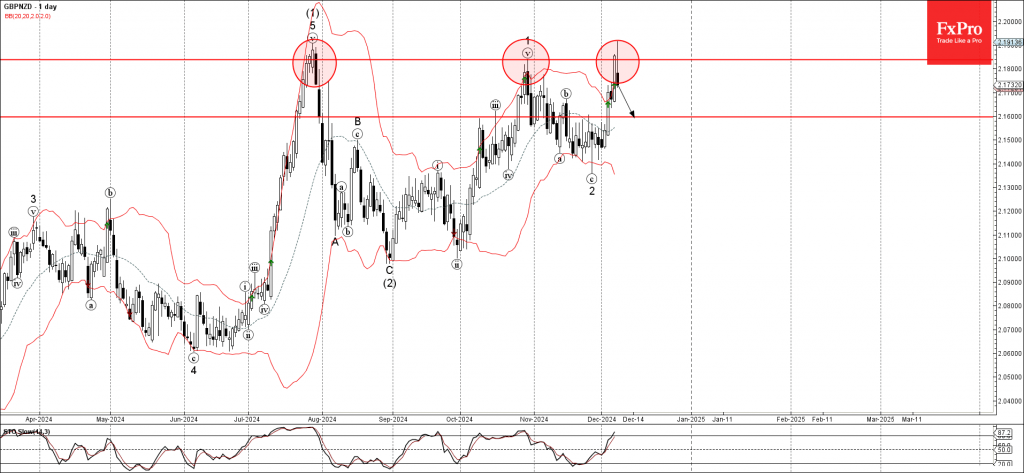

GBPNZD Wave Analysis

- GBPNZD reversed from key resistance level 2.1840

- Likely to fall to support level 2.1600

GBPNZD currency pair recently reversed down from the resistance zone between the key resistance level 2.1840 (which has been reversing the pair from July) and the upper daily Bollinger Band.

The downward reversal from this resistance zone will likely form the daily Japanese candlesticks reversal pattern Shooting Star.

Given the strength of the resistance level 2.1840 and the overbought daily Stochastic, GBPNZD currency pair can be expected to fall toward the next support level 2.1600.

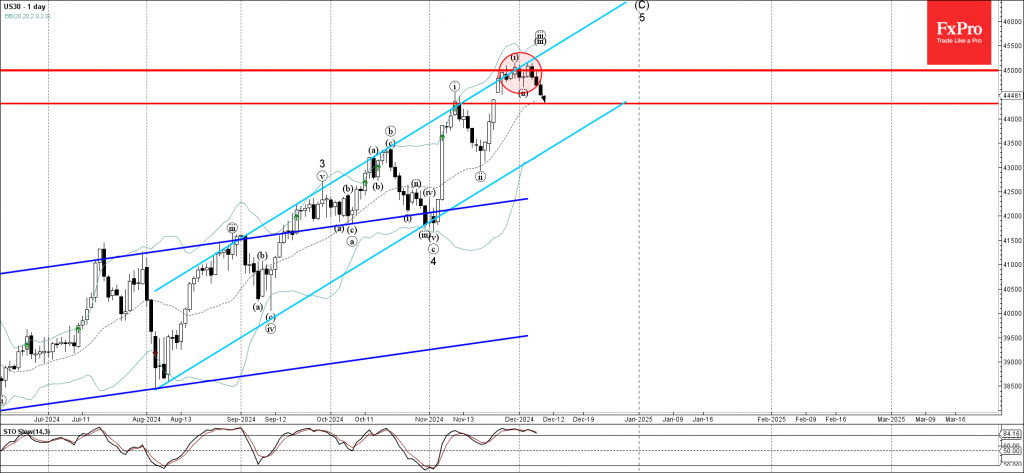

Dow Jones Wave Analysis

- Dow Jones reversed from resistance area

- Likely to fall to support level 44300.00

Dow Jones index previously reversed down from the resistance area between the resistance level 45000.00 (which has been reversing the index from the end of November), resistance trendline of the daily up channel from August and the upper daily Bollinger Band.

The downward reversal from this resistance zone started the active minor correction iv of the higher impulse wave 5 from last month.

Given the overbought daily Stochastic, Dow Jones index can be expected to fall toward the next support level 44300.00 (former resistance which stopped wave i at the start of November).

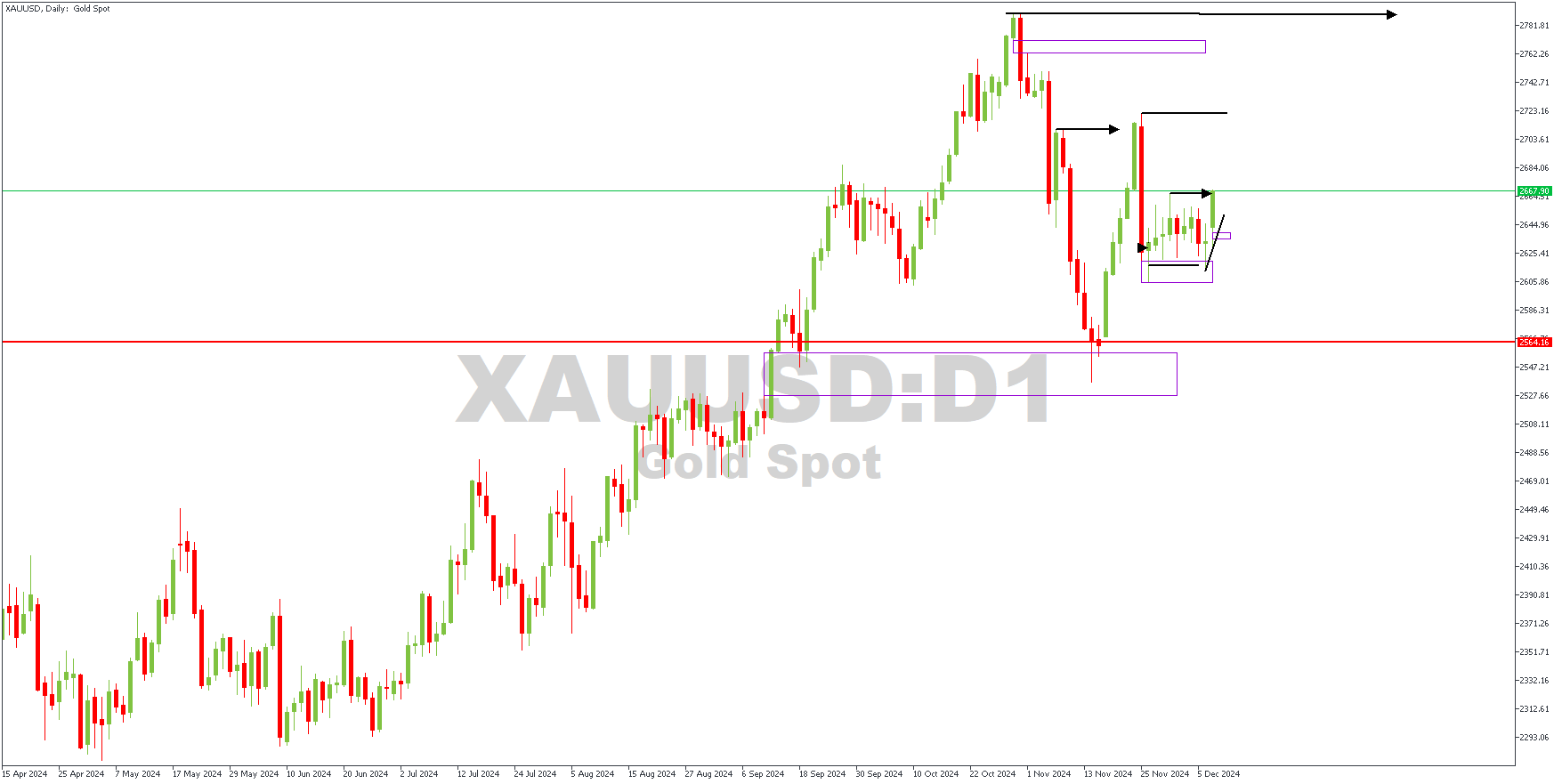

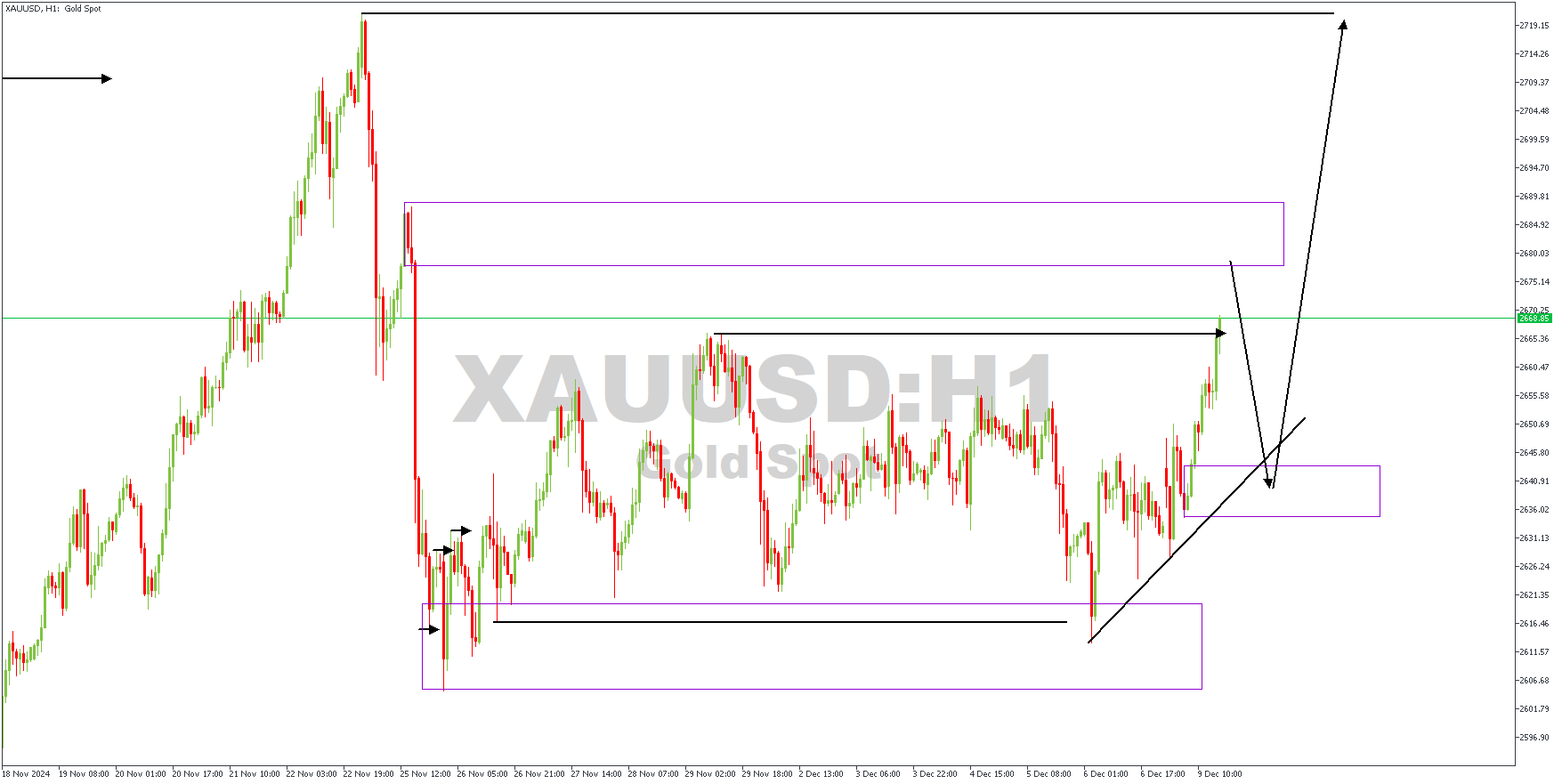

Gold (XAUUSD) Goes Bullish

Gold (XAUUSD) continues to show a positive trend during the European session but stays below the $2,650-2,655 range it has been stuck in for the past two weeks. Friday's US jobs report boosted expectations that the Federal Reserve will cut interest rates in December, keeping US Treasury yields low and supporting gold prices.

Additionally, political instability in South Korea, global tensions, and trade war concerns drive demand for gold as a safe-haven asset. However, a slightly stronger US Dollar, supported by speculation that President-elect Donald Trump's policies could push inflation higher, limits gold's gains.

XAUUSD – D1 Timeframe

The price action on the daily timeframe chart of XAUUSD shows a recent bullish break of structure, followed immediately by a retracement and consolidation. The consolidation range has created a base; however, the lower timeframe is expected to help bring the requisite details to light.

H1 Timeframe

In the 1-hour timeframe of XAUUSD, we see a double break of structure pattern formed around the base of the consolidation range, with a recent upthrust from the pattern's demand zone. The price has also created trendline support that could serve as the confirmed entry for the next bullish impulse.

Analyst's Expectations:

- Direction: Bullish

- Target: 2695.30

- Invalidation: 2633.61

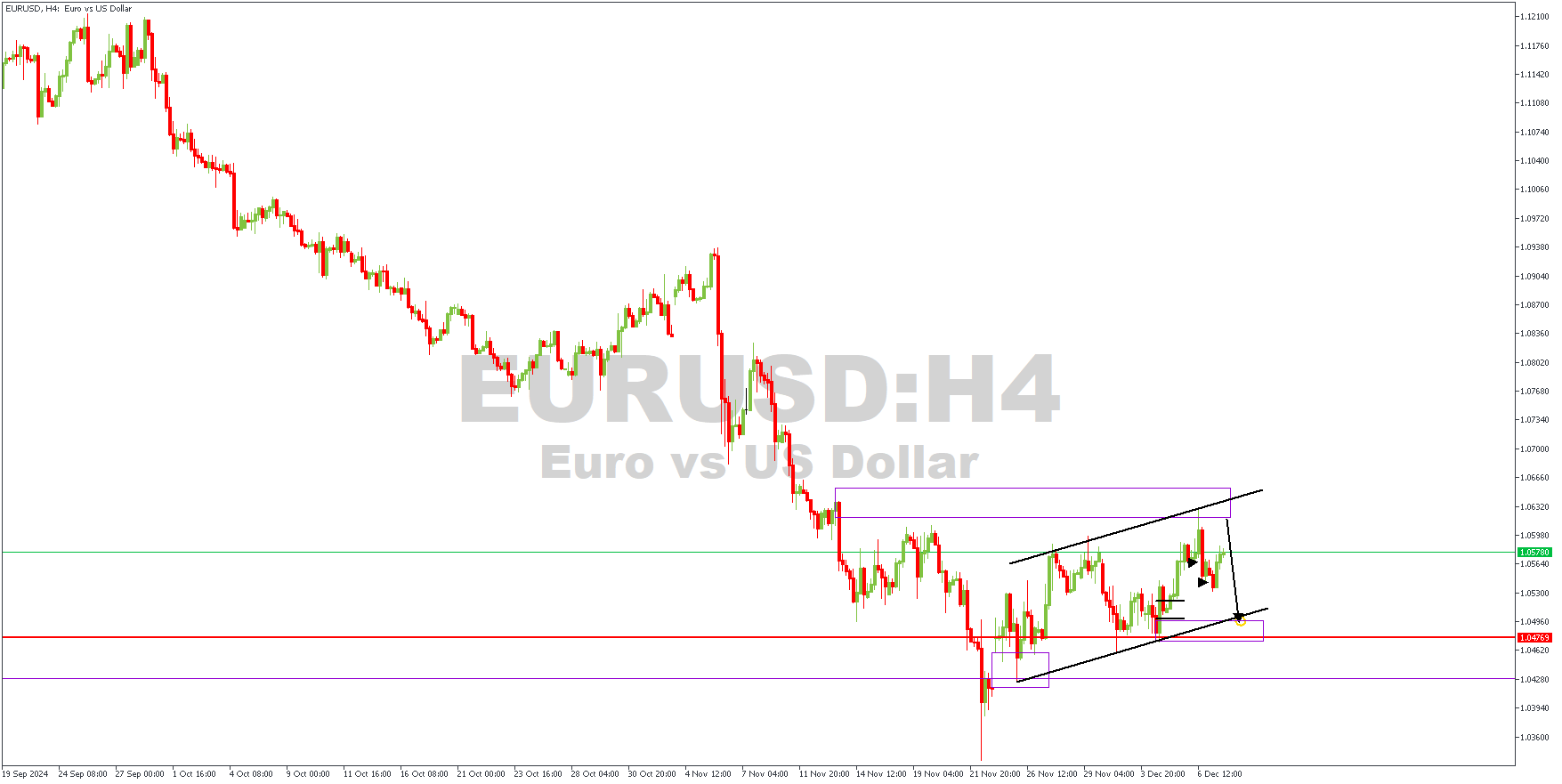

EURUSD Breakdown, 9th December

This Monday, as part of the weekly market review and analysis, we examined the price action on the EURUSD chart across the different timeframes. While the short-term direction appears to be bearish, the long-term sentiment remains bullish, especially on the weekly and daily timeframe charts. Here is my interpretation of the price action on these timeframes.

EURUSD – H4 Timeframe

The EURUSD price action on the 4-hour timeframe chart is consolidating within a channel. The confluence region of the supply zone and the trendline resistance have recently reacted, although the price seems to be returning to the area of interest. In this case, the lower timeframe could provide insights into whether or not the price action has sufficient momentum to break above the area of interest.

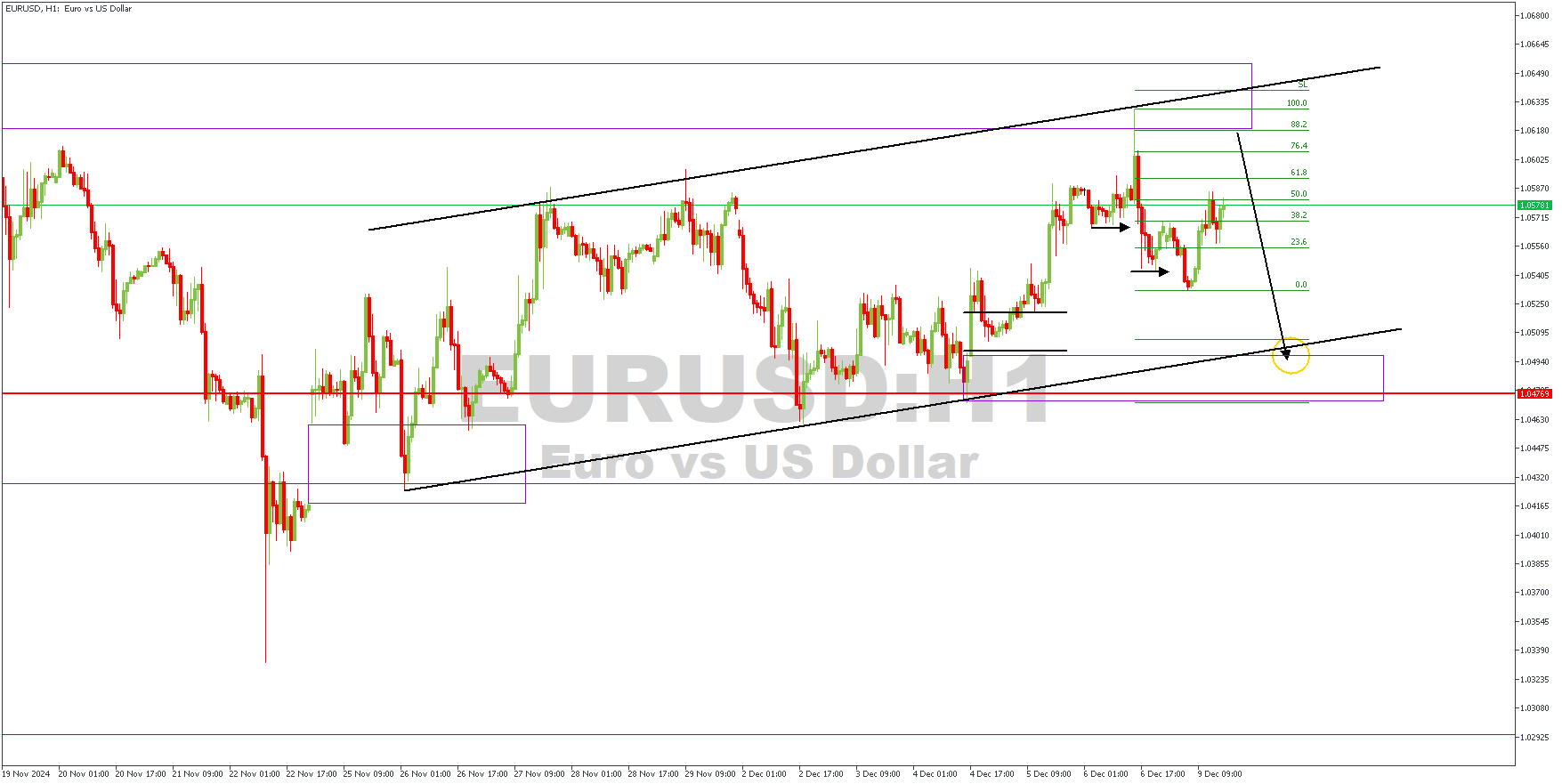

H1 Timeframe

On the 1-hour timeframe chart of EURUSD, we see that the initial reaction from the supply zone created a double break-of-structure pattern, confirming increased bearish momentum. In the meantime, the price is expected to retest the 76%—88% area of the Fibonacci retracement tool before the bearish sentiment resumes. The primary target is the highlighted demand zone overlapping the trendline support.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.05045

- Invalidation: 1.06555

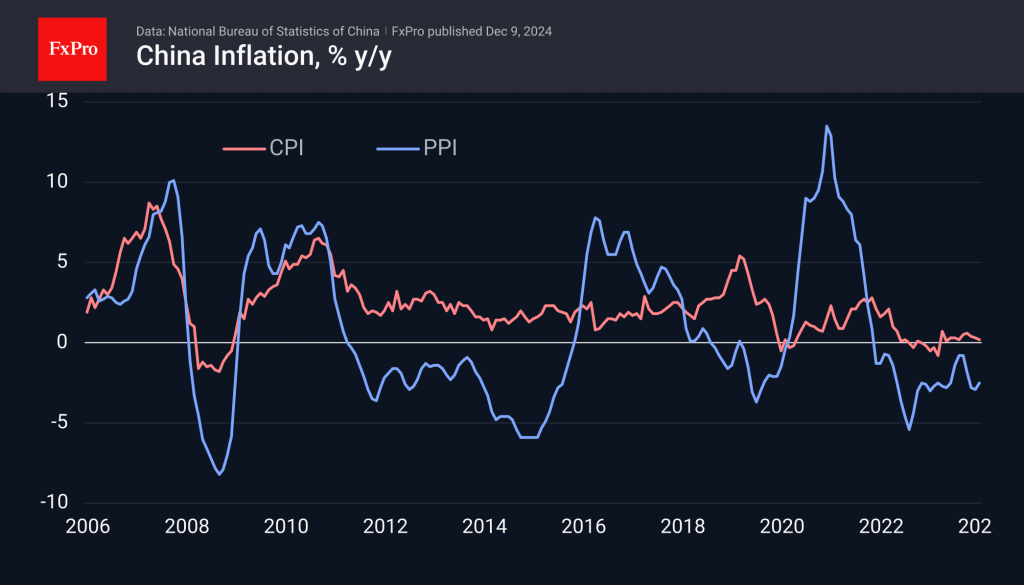

Soft Inflation and Policy Shift Helped Chinese Stocks

Chinese stock indices led the gains on Monday following reports that the government will adopt a ‘moderately loose’ monetary policy, as opposed to the ‘prudent’ one previously in place. This change in tone saw the Hang Seng Index rise by almost 6%. Admittedly, it only helped bring it back to where it was a month ago.

The latest change was likely a reaction to fresh inflation data released on Monday morning. According to the latest data, China’s consumer inflation slowed to 0.2% y/y after decelerating since August, contrary to expectations of an acceleration of 0.4%.

However, the producer price index beat expectations. Its decline slowed to 2.5% y/y from 2.9% the previous month, and 2.5% was expected. This index had come close to positive territory in June and July but turned down again. The stimulus has been too cautious and limited.

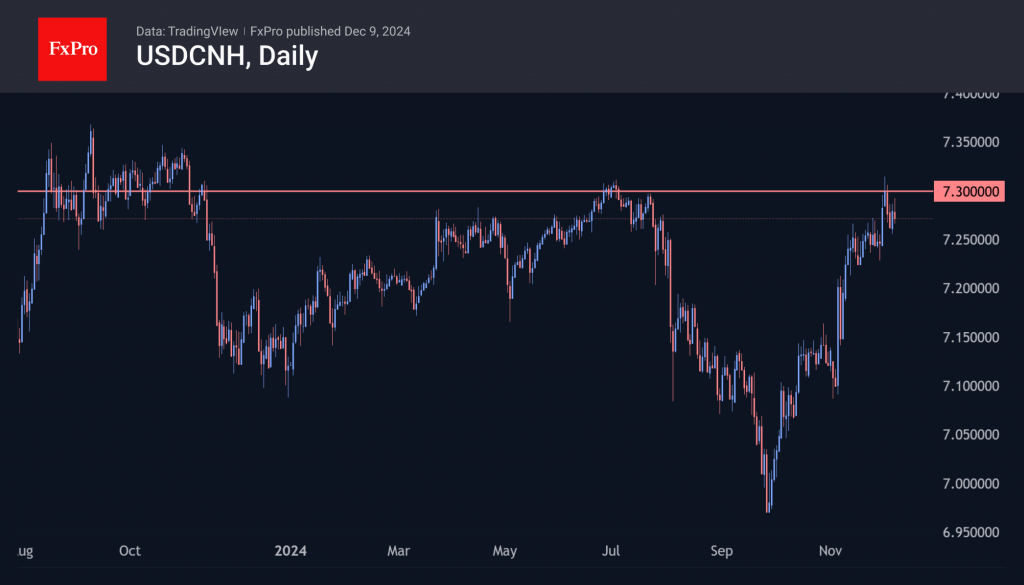

An important consequence of the shift to looser monetary policy is pressure on the local currency. Nevertheless, the USDCNH returned below 7.29 during the day on Monday. Since the beginning of last week, the pair has been under pressure near the upper end of the range since November 2023, near 7.30. Inflation figures, monetary policy and fears of tariff wars are setting the stage for pressure on the Chinese currency. The ability to create resistance so far seems to indicate the authorities’ intention to stabilise the exchange rate, which is unlikely to deter market speculators for long.

Sunset Market Commentary

Markets

The Chinese Politburo’s announcement around the end of Asian dealings and the beginning of European ones was quite an opener of the trading week. Led by president Xi Jinping, the country’s top leaders signaled bolder support for next year. The “extraordinary countercyclical” measures included, amongst others, a change in the monetary policy stance from “prudent” to “moderately loose”. In a sign of its importance, such a shift hasn’t happened since 2011. It may be the prelude to big rate cuts and asset buying. The Politburo also embraces a more proactive fiscal stance and promised to “forcefully lift consumption” and drive domestic consumption “in all aspects”. The news follows this morning’s inflation numbers that highlighted once again the ongoing economic swamp China is trapped in. It also immediately raises the stakes (and hopes) for Wednesday’s larger Central Economic Work Conference. This is where leaders discuss next year’s growth target as well as the strategies to reach it. Chinese bourses enjoyed a late-session boost and helped European equities overcome geopolitical (Syria) concerns. Wall Street opens mixed with tech underperforming on another, less market-positive Chinese decision to launch a monopoly probe into Nvidia over a 2020 deal. The yuan is cautiously optimistic, gaining towards USD/CNY 7.262. Being major trading partners to China, the Australian and kiwi dollar benefit from the stimulus announcement as well. Other G10 currency crosses show little changes, the JPY being the underperforming exception (USD/JPY 151.9). EUR/USD ekes out a small gain towards but below 1.06 as markets await Wednesday’s final input for the Fed meeting next week (CPI) and Thursday’s ECB policy meeting. The Australian, Canadian, Swiss and Brazilian central banks all gather too. Core bonds show no clear direction. Bunds marginally underperform US Treasuries with yield changes varying between flat and -1.8 bps across the curve. US rates rise no more than 2 bps.

News & Views

Industrial production in the Czech republic in October decreased -0.7% m/m in real terms. The Y/Y measure dropped from 1.6% to -2.1%. The Czech Statistical Office commented that the yearly decline was negatively affected by a higher yearly comparison base for some key components, including manufacturing of transport equipment and of motor vehicles. Positive contributions were reported in fabricated metal products and food products. Orders data (current prices) showed a slightly better, but still subdued picture. Orders decreased by 0.5% M/M but were 2.0% higher Y/Y. Non-domestic orders increased by 3.1% Y/Y. Domestic orders grew 0.2%. The average registered number of employees in industry October was also 2.0% lower compared to the same month last year. A bit different from today’s modest supply-side data, better retail sales and higher than expected wage growth data last week suggested a further improvement in consumer demand. These data supported recent CNB ‘guidance’ that a pauze in its rate cut cycle might occur soon. December inflation to be released tomorrow is a final key input for the CNB policy meeting on Dec 19. Today, CNB’s Kubekova indicated CNB is more concerned about an slight increase in inflation than a ST deflationary development. She will decide between a further rate reduction an stability and wait for the full-year data to get a better picture. The koruna recently improved from the EUR/CZK 25.45/40 area to trade near 25.09, with the 25.00 area first key support (CZK resistance) on the technical charts.

A survey of the UK Recruitment & Employment confederation and KMPG compiled by S&P global signaled a further deterioration of the UK labour market conditions during November. Permanent placements continued to decline, this time at the steepest pace since August 2023. Firms were reassessing staffing needs and put a pause on recruitment activity as they considered the impact of the late October government budget. Salary growth remained modest and was little changed on October's 44-month low. Demand for staff also declined at the fastest since August 2020, whilst overall staff availability continued to rise amid reports of increased redundancies. KPMG’s Jon Holt said downward pressure on wage inflation will be encouraging for BoE ahead of this month’s meeting, although it may not be enough to counter wider inflationary pressures in the economy. ‘However, the prospect of further rate cuts through 2025, alongside the Government’s investment plans, both point to improved growth in the near term. This should give businesses greater confidence which may help stabilise the labour market.’