Sample Category Title

Swiss National Bank Cuts by Half-Point, Swissy Dips

The Swiss franc is down on Thursday following the Swiss National Bank rate announcement. In the North American session, USD/CHF is trading at 0.8880, up 0.43% 80on the day at the time of writing.

Swiss National Bank chops by 50 basis points

Today’s Swiss National Bank meeting was live, with the market uncertain as whether the SNB would cut rates by 25 or 50 basis points. In the end, the central bank opted for a jumbo 50-bp cut, bringing the cash rate to 0.50%.

The driver for the today’s oversized cut was the November inflation report, which came in at -0.1% for a second straight month. Inflation hasn’t posted a gain in six months and the SNB is concerned that inflation could fall below the 0%-2% target.

The 50-bp cut marks the SNB’s biggest rate reduction in 10 years. In its statement, the Bank pointed to lower-than-expected inflation, risks over US economic policy and political uncertainty in Europe. The statement was somewhat dovish, noting that “the forecast for Switzerland, as for the global economy, is subject to significant uncertainty”.

Today’s rate cut marks the fourth reduction this year. The SNB has been aggressive in its easing cycle, with the twin goals of avoiding deflation and combating the Swiss franc’s appreciation. The SNB does not want a highly-valued Swiss franc as this hurts the critical export sector. The central bank implemented a negative rate policy until mid-2022 and the SNB has not ruled out a return to negative rates. After the meeting, SNB President Martin Schlegel said that today’s 50-bp cut had reduced the probability of negative rates.

The SNB also released its updated inflation forecast at today’s meeting. The September inflation report was revised downwards, with a forecast of 1.1% in 2024 and 0.3% in 2025.

USD/CHF Technical

- USD/CHF has pushed above resistance at 0.8860 and is testing resistance at 0.8879. Above, there is resistance at 0.8903

- 0.8836 and 0.8817 are the next support levels

EURUSD – ECB’s Rate Cut and Dovish Shift Add to Negative Fundamentals

EURUSD – choppy post-ECB trading keeps the price within a 50-pips range and lacks clearer near term direction signal.

Rate cut by 25 basis points and dovish shift by the central bank which signals that the door for further easing remains open, due to weak growth outlook, fueled by negative economic data and political instability (primarily in Germany and France) keep near-term risk at the downside.

On the other hand, technical picture on daily chart is mixed (positive momentum continues to strengthen and stochastic is about to penetrate oversold territory, countered by MA’s in full bearish setup) suggests that the price action may remain in current range for some more time.

Markets shift focus to next week’s top economic events (Fed rate decision and EU inflation report) which may generate stronger signals.

The price found solid support at 1.0475 (broken Fibo 23.6% of 1.0936/1.0332 bear-leg) which so has far contained several attacks and still marks the base for potential fresh attempts higher, but increased downside risk to be expected in case loss of this support.

Res: 1.0528; 1.0563; 1.0597; 1.0630

Sup: 1.0475; 1.0432; 1.0400; 1.0332

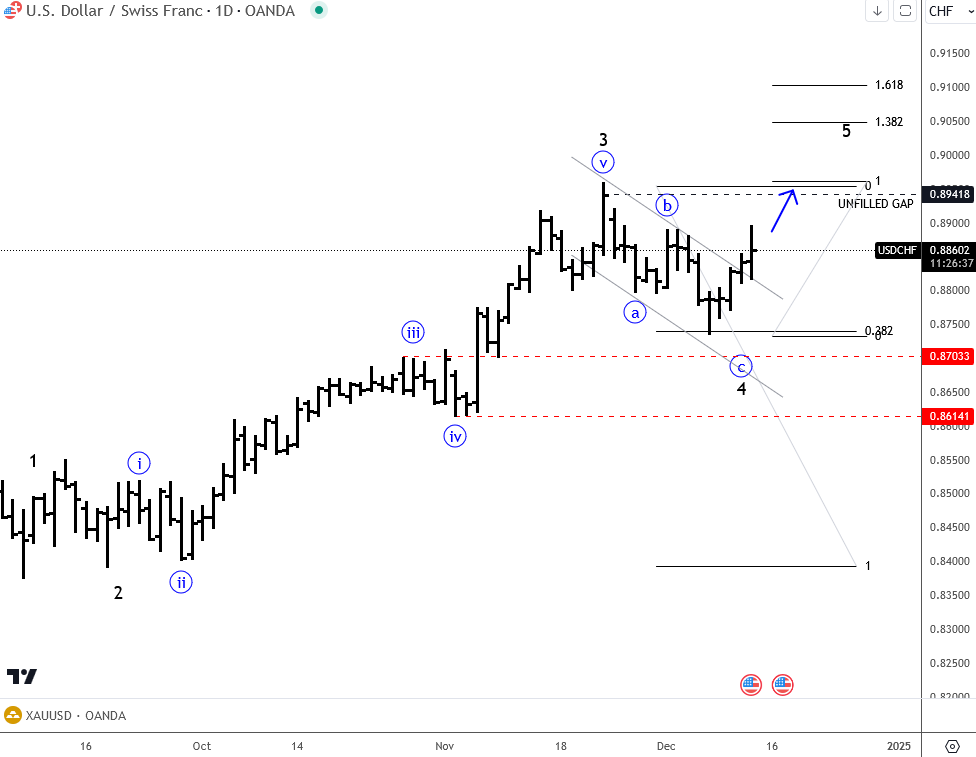

USD/CHF: Bullish Momentum Continues After SNB RateCut

So far this week, USD/CHF has shown a strong rebound following the spike to the downside last Friday when US jobs data came out slightly higher than expected. However, we viewed this move as only a temporary reaction, as the USDCHF pair had been trading at strong support.

From an Elliott Wave perspective, this drop was tracked as a three-wave correction, suggesting it was part of a broader uptrend. The potential for a continuation higher was supported by the incomplete Elliott Wave bullish pattern and the presence of an unfilled gap near recent highs, which remains unfilled today.

The Swiss National Bank’s surprising 50 basis point rate cut further bolstered the pair’s bullish outlook. The SNB chairman also hinted that additional rate cuts could be on the table heading into 2025, adding to the Swiss franc’s weakness.Technically, the break above channel resistance signals that a fifth wave is underway, potentially targeting the 0.90–0.91 area. This zone could mark a limited upside later this month or in early January when the broader US dollar cycle may conclude as Trump takes office.

Sunset Market Commentary

Markets

The ECB as expected lowered the policy rates by 25 bps to 3% (deposit). The ECB will no longer reinvest some of the maturing PEPP bonds, allowing for a natural roll-off of the pandemic bond portfolio in fashion identical to APP. The central bank in its statement said disinflation is well on track. CPI forecasts for this year and the next were marginally revised down to 2.4% and 2.1%. The 2026 projection was left unchanged at 1.9% and the first estimate for 2027 came in at 2.1%. Core inflation for 2025 is seen at 2.3% (unch) and at 1.9% for both 2026 (-0.1 ppt) and 2027. Inflation is thus expected to be very close to target over the policy horizon. These projections are based on ECB market expectations probably dating from around mid-November (cut-off date). Easing bets have increased even further since with an even-lower terminal rate of between 1.5-1.75%. Growth forecasts were bleaker than in September. The economy would expand between 1.1-1.4% over 2025-2027 with the hoped-for recovery still assumed to arise from rising real incomes (supporting consumption and investment). President Lagarde noted the latest data suggest slowing momentum and firms holding back investment amid uncertainty. Growth risks are tilted to the downside. The combination of desinflation and sluggish growth led the ECB to scrap a pledge “to keep policy rates sufficiently restrictive for as long as necessary”. It suggests more cuts are coming although the ECB does not pre-commit to anything. Neither would Lagarde give a flavour of where she thinks the neutral rate is located. It probably served as quid pro quo for policymakers that wanted a bigger (50 bps) rate cut today. Asked whether it was discussed, Lagarde said it’s not yet “mission accomplished” on inflation. Services prices is preventing policymakers to feel totally confident. The ECB did not (yet) return to a forward-looking approach as suggested by chief economist Lane a few weeks ago but sticks to a data-dependent strategy. Markets react stoic. The ECB meeting does not change a lot to expectations going forward with 25 bps cuts priced in for the next several meetings. Front-end European yields soon reversed a knee-jerk dip lower. European swap yields even rise between +2.2 bps (2-yr) to +3.8 bps (30-yr). The euro trades a tad lower against most G10 peers. EUR/USD eases towards 1.048 vs yesterday’s close just south of 1.05.

News & Views

The Swiss National Bank unexpectedly accelerated its easing cycle with a 50 bps rate cut to 0.50%. Underlying inflation decreased further and the SNB stands ready to adjust monetary policy if necessary. That’s a subtle, but important change from the promise of “further cuts” in September. We see it as a reckoning of the limited remaining policy space which argues in favour of a more gradual approach/end game going forward. SNB chair Schlegel at the press conference said that they would tolerate inflation dropping below the lower bound of the 0%-2% inflation band if it is deemed temporary. He also thinks that the likelihood of negative rates has become smaller. The new conditional inflation forecast (on a 0.5% policy rate) was lower than in September (1%) with CPI expected to average 1.1% this year (from 1.2%), 0.3% next year (0.6%) and 0.8% in 2026 (0.7%). Inflation prognosis would have been even lower if it weren’t for today’s cut. The central bank anticipates growth of around 1% for the current year and between 1% and 1.5% for 2025. The SNB repeats its willingness to be active in the FX market as necessary to counter the impact of a historically strong Swiss franc, though policy rate cuts continue to be the main instrument for any potential further policy easing. EUR/CHF rose from 0.9280 to 0.9340 in a first reaction, but the changed SNB-tone erased those gains somewhat.

The International Energy Agency published its monthly oil market report. World oil demand is set to accelerate from 840k b/d (from 921k previously) to 1.1mn b/d in 2025 (from 990k), lifting consumption to 103.9mn b/d. The increase will be dominated by petrochemical feedstocks. Geographically, emerging Asia continues to lead gains. The IEA’s oil demand growth forecasts remain significantly below the OPEC ones. The cartel earlier this week prognosed 1.6mn b/d growth this year and 1.4mn b/d for 2025. The IEA said that the decision by OPEC+ to delay the unwinding of its additional voluntary production cuts by another three months and extend the ramp-up period by nine months through September 2026 has materially reduced the potential supply overhang that was set to emerge next year. Total oil supply is on track to increase by 630k b/d this year and 1.9mn b/d in 2025, to 104.8mn b/d. Brent crude prices hover between $70/b and $75/b since mid-October.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0471; (P) 1.0505; (R1) 1.0531; More...

No change in EUR/USD's outlook and intraday bias stays neutral first. On the downside, break of 1.0471 support will suggest that corrective recovery from 1.0330 has completed at 1.0629, and fall from 1.1213 is ready to resume. Intraday bias will be back on the downside for 1.0330 first, and then 61.8% projection of 1.0936 to 1.0330 from 1.0629 at 1.0254. Also, in this case, sustained trading below 1.0404 key fibonacci level will carry larger bearish implication.

In the bigger picture, focus stays on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.

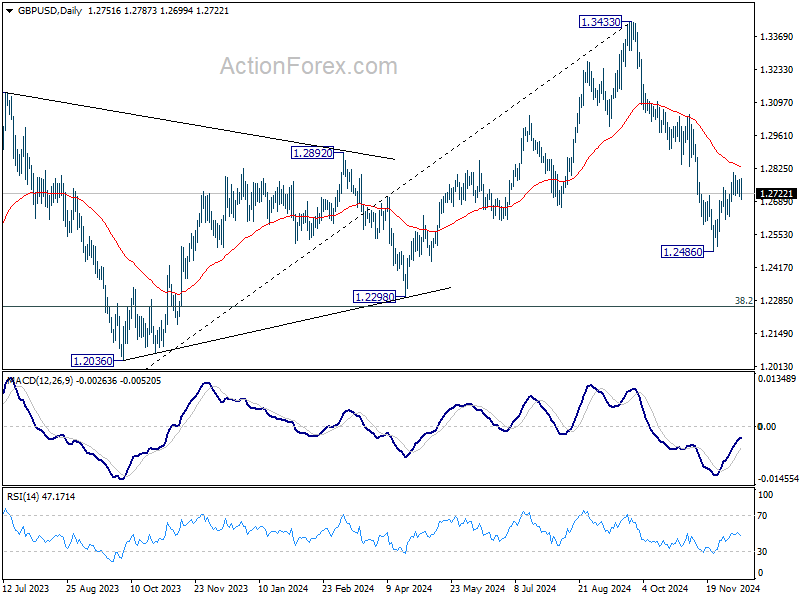

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2715; (P) 1.2749; (R1) 1.2784; More...

Intraday bias in GBP/USD remains neutral and outlook is unchanged. Corrective rebound from 1.2486 short term bottom could still extend higher. But outlook will stay bearish as long as 55 D EMA (now at 1.2834) holds. On the downside, below 1.2615 minor support will bring retest of 1.2486 first. Firm break there will target 1.2298 cluster support zone. However, sustained break of 55 D EMA will argue that the near term trend has reversed, and targets 1.3047 resistance for confirmation.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern.

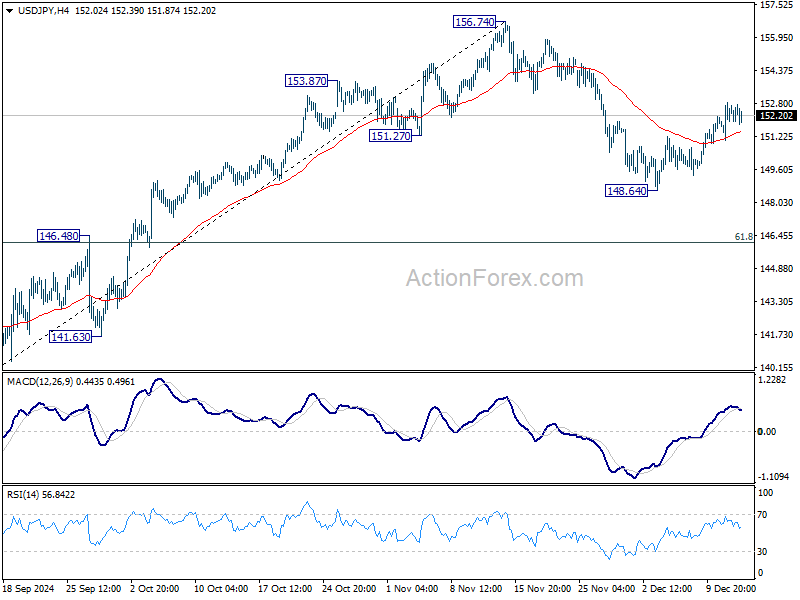

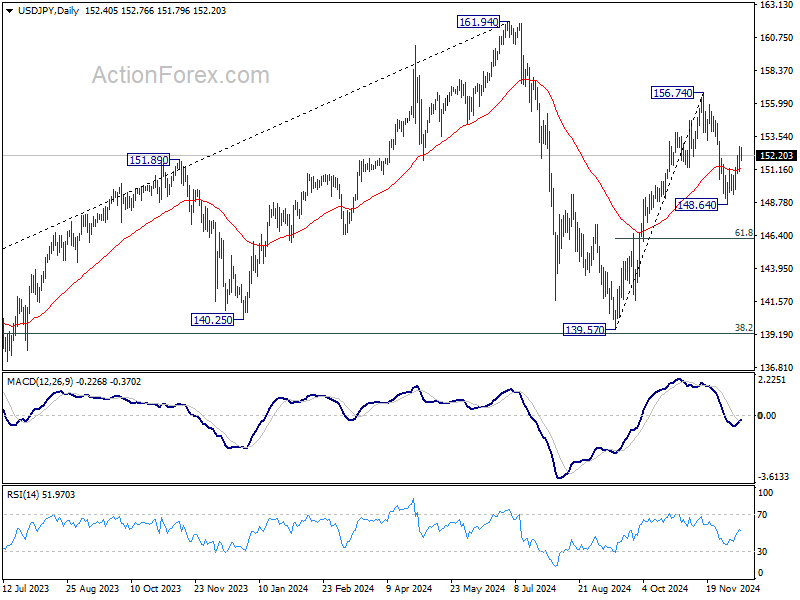

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.37; (P) 152.11; (R1) 153.20; More...

No change in USD/JPY's outlook and intraday bias stays on the upside. Further rally should be seen to retest 156.74 high. Current development suggests that rise from 139.57 might still be in progress and break of 156.74 will confirm resumption. For now, this will be the favored case as long as 148.64 support holds, in case of retreat.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

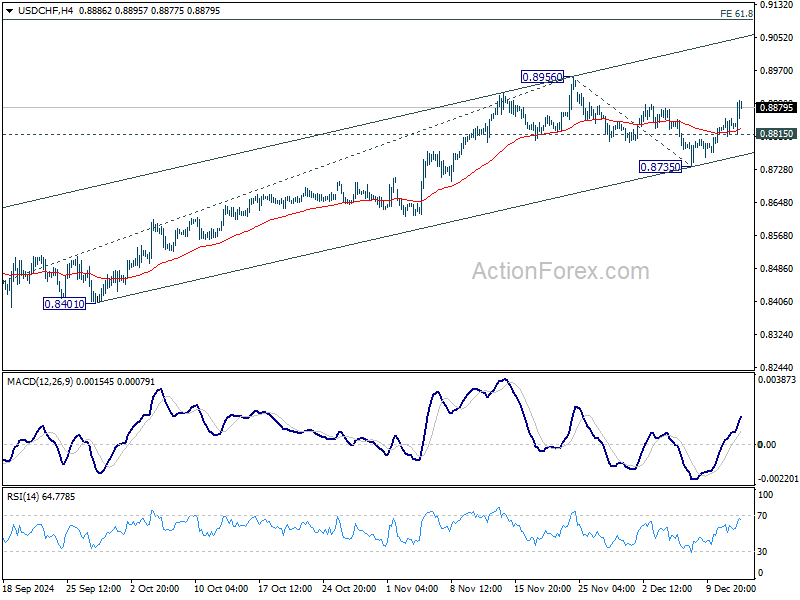

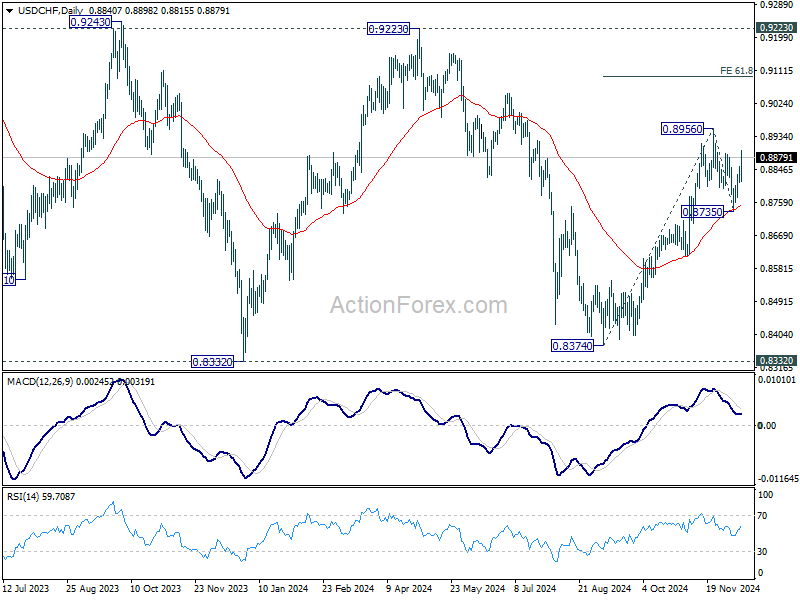

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8817; (P) 0.8836; (R1) 0.8860; More…

Intraday bias in USD/CHF remains on the upside for the moment. Corrective fall from 0.8956 should have completed at 0.8735 after hitting 55 D EMA. Further rally should be seen to retest 0.8956 high first. Firm break there will resume the whole rise from 0.8374. Next target is 61.8% projection of 0.8374 to 0.8956 from 0.8735 at 0.9095. On the downside, below 0.8815 minor support will turn intraday bias neutral first. But risk will stay on the upside as long as 0.8735 support holds, in case of retreat.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

European Majors Struggle After SNB, ECB Cuts

European majors are broadly under pressure today, with Swiss Franc leading losses. SNB’s unexpected 50bps rate cut caught markets off guard, and its significantly downgraded inflation projections suggest more easing is on the table for 2025. Meanwhile, Euro managed to hold steady after ECB’s widely anticipated 25bps cut. ECB demonstrated clear confidence in its inflation trajectory. Despite its professed "data-dependent" stance, the path toward a neutral rate now seems well-defined.

In contrast, Australian Dollar is shining as the strongest performer, driven by robust domestic job data that dashed hopes for a February rate cut by RBA The Yen follows closely ahead of BoJ’s closely watched Tankan survey. Kiwi also shows strength, while Dollar and Canadian Dollar trade mixed for the session.

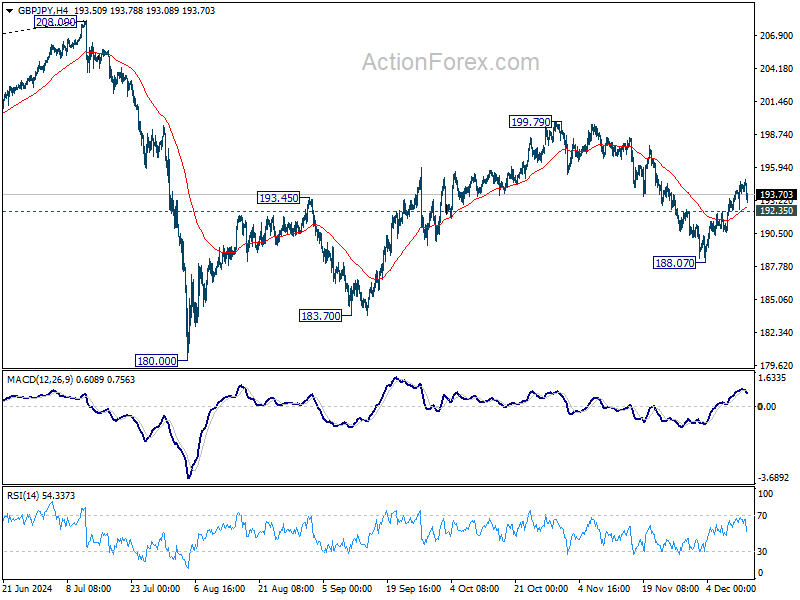

Looking ahead, Yen will likely stay in focus during the Asian session with the Tankan survey results, while UK GDP data tomorrow could impact Sterling’s direction. GBP/JPY stands at an inflection point.

Technically, near term in GBP/JPY outlook was mixed up with the stronger than expected rebound from 188.07. However, break of 192.35 minor support argues that fall from 199.79 is in progress. More importantly, that would also revive the case that while corrective rise from 180.00 has completed at 199.79. Deeper fall should then be seen to 180.00/183.70 support zone.

In Europe, at the time of writing, FTSE is up 0.07%. DAX is up 0.14%. CAC is up 0.17%. UK 10-year yield is up 0.0281 at 4.349. Germany 10-year yield is up 0.024 at 2.156. Earlier in Asia, Nikkei rose 1.21%. Hong Kong HSI rose 1.20%. China Shanghai SSE rose 085%. Singapore Strait Times rose 0.43%. Japan 10-year JGB yield fell -0.0212 to 1.051.

US PPI up 0.4% mom, 3.0% yoy, highest annual rise since Feb 2023

US PPI for final demand rose 0.4% mom in November, above expectation of 0.3% mom. Nearly 60% of the broad-based rise in final demand prices can be attributed to a 0.7% mom increase in goods. Prices for final services moved up 0.2% mom. PPI less foods, energy, and trade services inched up 0.1% mom.

On an unadjusted basis, PPI advanced 3.0% yoy for the 12 months period, well above expectation of 2.5% yoy. It's also the largest rise since moving up 4.7% yoy in February 2023. PPI less foods, energy, and trade services advanced 3.5% yoy.

US initial jobless claims rise to 242k, above exp 221k

US initial jobless claims rose 17k to 242k in the week ending December 7, above expectation of 221k. Four-week moving average of initial claims rose 6k to 224k.

Continuing claims rose 15k to 1886k in the week ending November 30. Four-week moving average of continuing claims rose 3.5k to 188k, highest sine November 27, 2021.

ECB cuts to 3.00%, projects inflation steady around target through 2027

ECB cut its deposit rate by 25bps to 3.00%, aligning with market expectations. The overall decisions and economic projections reflect confidence in the ongoing disinflation process. Yet, he Governing Council reiterated its "data-dependent and meeting-by-meeting approach," refraining from pre-committing to any specific rate path.

In its statement, the ECB highlighted that the "disinflation process is well on track." The bank's updated projections show headline inflation averaging 2.4% in 2024, moderating further to 2.1% in 2025 and 1.9% in 2026.

Inflation excluding energy and food is expected to average 2.9% in 2024, easing to 2.3% in 2025 and stabilizing at 1.9% by 2026 and 2027.

ECB added that inflation is projected to settle around its 2% target "on a sustained basis."

However, growth expectations were revised downward, reflecting continued economic challenges. ECB now forecasts the Eurozone economy to expand by just 0.7% in 2024, improving modestly to 1.1% in 2025 and 1.4% in 2026.

Growth is expected to rest primarily on rising real incomes, which should bolster household consumption, alongside gradual increases in business investment. Additionally, ECB noted that the fading effects of restrictive monetary policy should support a recovery in domestic demand over time.

Ifo flags structural risks as German economy faces subdued 0.4% growth next year

Germany's economy is forecast to contract by -0.1% in 2024, according to the Ifo Institute. The economy has been "treading water for five years", with growth stalled amid structural challenges.

The institute presents two possible trajectories for 2025: sluggish growth of just 0.4% if structural issues persist, or a recovery to 1.1% if economic policy reforms support industrial revival.

Timo Wollmershäuser, Head of Forecasts at Ifo, stated, “It is not yet clear whether the current phase of stagnation is a temporary weakness or one that is permanent and hence a painful change in the economy.”

He noted that Germany's export sector, once a key driver of growth, has become "increasingly decoupled from global economic development," with competitiveness eroding, particularly in industrial goods outside Europe.

In a pessimistic scenario, this weakness could lead to "creeping deindustrialization," while an optimistic outcome would depend on supportive policies enabling manufacturing to expand production capacities. Such measures could, in turn, boost private consumption and reduce the high savings rate, providing further stimulus to the economy.

SNB cuts by 50bps, projects weaker inflation and modest growth in 2025

SNB took a decisive step by lowering its policy rate by 50 basis points to 0.50%. In its accompanying statement, the central bank highlighted that underlying inflationary pressures have "decreased again" this quarter, warranting the larger-than-expected rate cut. SNB reiterated its commitment to "monitor the situation closely" and stated that it would "adjust its monetary policy if necessary."

The latest conditional inflation forecasts reflect a significantly subdued outlook, even with interest rate down from 1.00% to 0.50%.

For 2025, inflation is now projected at just 0.3%, a notable downgrade from the 0.6% forecast in September. However, the 2026 outlook saw a slight upward revision to 0.8%, from 0.7% previously.

Looking at some details, inflation is expected to decline sharply from 0.7% in Q4 2024 to a low of 0.2% in Q2 2025, before gradually recovering to 0.8% in 2026 and 0.7% in 2027. These figures underscore the SNB’s view of persistent deflationary risks, necessitating its proactive policy stance.

In terms of economic growth, SNB estimates GDP growth for 2024 to come in at around 1%, with a modest pickup to 1-1.5% expected in 2025. Despite this improvement, challenges remain, including slightly rising unemployment and declining utilization of production capacity.

Australia’s employment data beats expectations, unemployment drops below to 3.9%

Australia’s labor market showed surprising resilience in November as employment grew by 35.6k, surpassing expectations of a 29.6k increase. The standout figure was the 52.6k gain in full-time jobs, offsetting a decline of -17k in part-time positions.

Unemployment rate fell significantly, dropping from 4.1% to 3.9%, well below the anticipated 4.2%. However, a slight dip in the participation rate, from a record high of 67.1% to 67.0%, tempered the optimism.

Employment-to-population ratio nudged up to 64.4%, matching levels from a year ago and maintaining its position 2.2% above pre-pandemic levels. Monthly hours worked showed no growth, indicating stability in workforce activity despite the overall gains in employment.

David Taylor, Head of Labour Statistics at the ABS, noted that an unusually high number of unemployed individuals transitioned into employment during November. This dynamic contributed to both the rise in job creation and the sharp fall in unemployment. Taylor also highlighted the role of population growth, which has bolstered labor supply and helped maintain the balance between employment growth and demographic expansion.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8817; (P) 0.8836; (R1) 0.8860; More…

Intraday bias in USD/CHF remains on the upside for the moment. Corrective fall from 0.8956 should have completed at 0.8735 after hitting 55 D EMA. Further rally should be seen to retest 0.8956 high first. Firm break there will resume the whole rise from 0.8374. Next target is 61.8% projection of 0.8374 to 0.8956 from 0.8735 at 0.9095. On the downside, below 0.8815 minor support will turn intraday bias neutral first. But risk will stay on the upside as long as 0.8735 support holds, in case of retreat.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

US PPI up 0.4% mom, 3.0% yoy, highest annual rise since Feb 2023

US PPI for final demand rose 0.4% mom in November, above expectation of 0.3% mom. Nearly 60% of the broad-based rise in final demand prices can be attributed to a 0.7% mom increase in goods. Prices for final services moved up 0.2% mom. PPI less foods, energy, and trade services inched up 0.1% mom.

On an unadjusted basis, PPI advanced 3.0% yoy for the 12 months period, well above expectation of 2.5% yoy. It's also the largest rise since moving up 4.7% yoy in February 2023. PPI less foods, energy, and trade services advanced 3.5% yoy.