Sample Category Title

Trade Idea Update: GBP/USD – Hold short entered at 1.2465

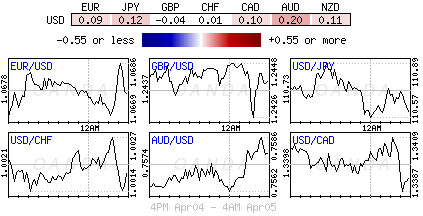

GBP/USD - 1.2483

Original strategy :

Sold at 1.2465, Target: 1.2365, Stop: 1.2500

Position : - Short at 1.2465

Target : - 1.2365

Stop : - 1.2500

New strategy :

Hold short entered at 1.2465, Target: 1.2365, Stop: 1.2500

Position : - Short at 1.2465

Target : - 1.2365

Stop : - 1.2500

As cable has rebounded again after holding above support at 1.2419, suggesting further consolidation above this level would be seen, however, as long as indicated resistance at 1.2496 holds, mild downside bias remains for another fall, below said support at 1.2419 would bring test of 1.2400 but break there i needed to add credence to our view that the rebound from 1.2377 has ended at 1.2559, bring further fall towards support at 1.2377. Looking ahead, only a drop below 1.2377 would confirm the fall from 1.2616 is still in progress for subsequent decline towards key support at 1.2335.

In view of this, we are holding on to our short position entered at 1.2465 but one should exit on such decline. Only break of said resistance at 1.2496 would abort and suggest an intra-day low is formed instead, risk a stronger rebound to 1.2525-30.

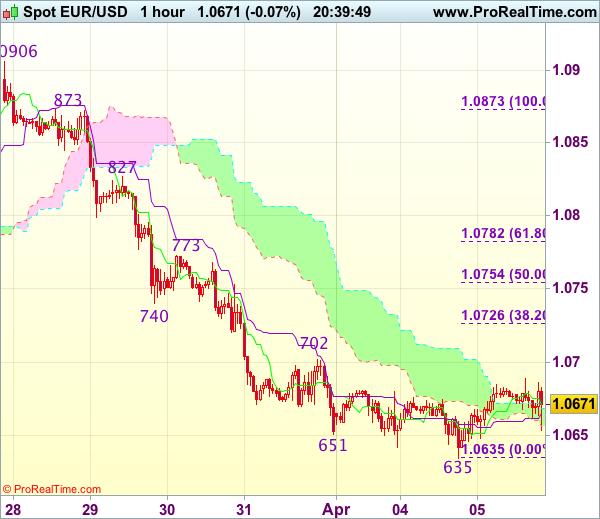

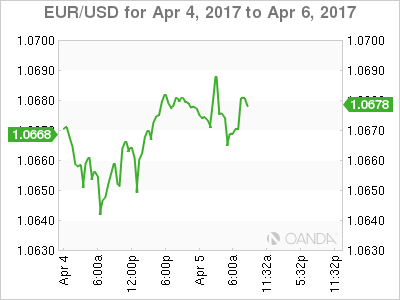

Trade Idea Update: EUR/USD – Sell at 1.0730

EUR/USD - 1.0669

Original strategy :

Sell at 1.0730, Target: 1.0610, Stop: 1.0765

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0730, Target: 1.0610, Stop: 1.0765

Position : -

Target : -

Stop : -

As the single currency has recovered after falling to 1.0635 yesterday, suggesting minor consolidation above this level would be seen and corrective bounce to 1.0702 cannot be ruled out, however, reckon 1.0730-40 would limit upside and bring another decline, below said support at 1.0635 would add credence to our bearish view that the decline from 1.0906 top is still in progress and extend further weakness to 1.0620, then test of previous chart support at 1.0600, however, a sustained breach below the latter level is needed to retain downside bias for subsequent selloff to 1.0570-75 first.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 1.0730-40 should limit upside. Only a firm break above resistance at 1.0773 would suggest low is formed instead, bring a stronger rebound to 1.0800 but resistance at 1.0827 should remain intact.

Trade Idea Update: USD/JPY – Sell at 111.55

USD/JPY - 111.13

Original strategy :

Sell at 111.55, Target: 110.35, Stop: 111.90

Position : -

Target : -

Stop : -

New strategy :

Sell at 111.55, Target: 110.35, Stop: 111.90

Position : -

Target : -

Stop : -

As the greenback has rebounded again in European morning, suggesting near term upside risk remains for the rebound from 110.27 (yesterday’s low) to bring retracement of the decline from 112.20, hence further gain to previous support at 111.12 cannot be ruled out, however, resistance at 111.59 would cap upside and bring another decline later, below 110.50-55 would suggest the rebound from 110.27 has ended, bring retest of this level, break there would extend the fall from 112.20 to last week’s low at 110.11. Looking ahead, break there is needed to retain downside bias and confirm medium term decline has resumed for further subsequent fall to 109.80-85 (1.618 times projection of 112.20-111.12 measuring from 111.59) which is likely to hold on first testing.

In view of this, would not chase this fall here and would be prudent to sell dollar on further subsequent recovery as 111.59 resistance should limit upside. Above 111.80 would shift risk to upside and signal the fall from 112.20 has ended, bring subsequent rise to 112.00-05 first.

Canadian Dollar Dips as Canada Posts Trade Deficit

USD/CAD has taken a pause on Wednesday, as the pair trades slightly below the 1.34 line. On the release front, there are no Canadian events. In the US, ADP Nonfarm Payrolls as well as the ISM Non-Manufacturing PMI. As well, the Federal Reserve releases its minutes from the March policy meeting.

The Canadian dollar briefly fell to 3-week lows on Tuesday, following a disappointing trade balance report. Canada recorded its first trade deficit in four months, with a decline of C$1.0 billion. The markets had expected a surplus of C$0.7 billion. On Friday, Canada will release key employment data, with the markets expecting a modest gain of 5.7 thousand jobs. An unexpected reading could trigger some movement from USD/CAD.

What's next for the Federal Reserve? With the US economy continuing to perform well, the discussions around the monetary policy tables are not whether the Fed will raise rates, but how many hikes we will see in 2017. The markets will be paying close attention to the minutes of the March meeting, when the Fed raised rates by a quarter-point, to a range of 0.75%-1.00%. Any hints about the timing of the next hike, as well as the tone of the minutes are factors which could move the currency markets on Wednesday. The markets considered the rate statement overly cautious, and this sentiment sent the US dollar broadly lower in March. If the reaction to the minutes is one of disappointment, the dollar could again experience broad losses.

USD Direction Depends on FOMC Minutes and Turmp-Xi Summit

Wednesday April 5: Five things the markets are talking about

Two and two are not adding up - softer U.S data is flying in the face of consumer sentiment, now at 17- and 11-year highs.

The retreat in the U.S auto sector report on Monday mirrors the lackluster broader consumer spending data released last Friday. Will the Fed shed some light on their fears in today's March FOMC minutes? (2:00 pm EST). Investors want to know how much the Fed has discussed its balance sheet reductions.

For various reasons market moves have been rather limited for the start of this month, however there are many crowded trades across the various asset classes - FX, debt, equity, and commodity markets - whose unwinding will surely trigger sharp moves in financial markets.

Expect Thursday's high profile meeting with President Trump and China counterpart China counterpart Xi to be more significant now that North Korea continues to defy U.S warnings to suspend its nuclear program with another missile test overnight.

In Europe, the results from France's second Presidential television debate seem to have reduced the demand for safe-haven bonds.

With Easter break around the corner and the reduced hope of U.S Congress moving forward on economic policy, market risk attractiveness continues to decrease.

1. Global stocks find support after holidays

Global equities rose as Chinese shares soared the most since August, while other markets fluctuated before a meeting between the U.S and China leaders.

Returning after two-days of holidays, the Shanghai Composite (+1.5%) was the best performing index in Asia overnight. Reports of a new special economic zone in Xiongan helped lift local property and industrials names. The Hang Seng rose +0.2%.

Note: The rally comes even as the PBoC continues to pull liquidity out of the market with no reverse repo operations for an eight consecutive day.

In Japan, the Nikkei share average gained (+0.3%) as the yen (¥110.94) rally paused, although investors remain cautions ahead of the U.S/China summit. The broader Topix index ended flat, while Australia's S&P/ASX 200 Index added +0.3%.

In Europe, equity indices are trading mixed. The DAX is underperforming weighed by shares of car manufacturers. Energy stocks are trading notably higher on higher oil prices. Homebuilder stocks are trading notably lower in the FTSE 100.

U.S stocks are set to open in the red (-0.1%).

Indices: Stoxx50 flat at 3,479, FTSE +0.2% at 7,335, DAX -0.3% at 12,245, CAC-40 flat at 5,102, IBEX-35 +0.4% at 10,401, FTSE MIB +0.1% at 20,276, SMI -0.1% at 8,640, S&P 500 Futures -0.1%

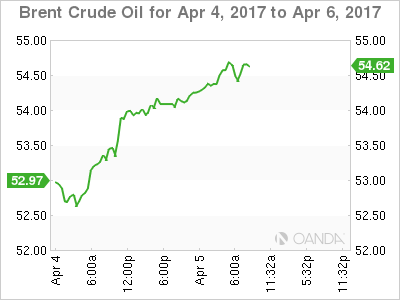

2. Oil hits one-month high on tighter supplies

Ahead of the U.S open, oil has hit a one-month high near $55 a barrel as a drop in U.S. crude inventories Tuesday raised hopes that OPEC-led supply restraint is clearing a global glut. Also lending support is an outage at a U.K North Sea oilfield.

Note: API data yesterday reported that U.S. crude inventories fell by a more-than-expected -1.8m barrels last week. The focus is now on whether today's U.S government's supply report confirms the decline (10:30 am EST).

Brent crude futures have risen +50c to +$54.67 a barrel. It reached +$54.80 intraday, the highest since March 8, while U.S. crude (WTI) was up +47c at +$51.50.

Both benchmarks have recovered from last week's four-month lows on expectations that OPEC would manage to tighten supply by cutting production.

Nevertheless, global inventories remain stubbornly high and the market bears continue to bet that it will take months for oil prices to respond convincingly to lower OPEC output.

Gold prices are holding steady (+0.1% to +$1,256.38 per ounce) near one-month highs as appetite for riskier assets ease ahead of a meeting between U.S/China. Market focus is also turning towards the FOMC minutes; investors are looking for any clues on the pace of further U.S. interest rate rises.

3. Fixed income looks for Fed guidance

The demand for safer haven bonds has eased a tad overnight after a second televised debate of French presidential hopefuls. Early poll results suggest that Melenchon, Macron, Fillon and Le Pen showed the most convincing performance, but Mr. Macron seems to remain in front when it comes to voting preference. The 10-year German Bund yield is currently trading at +0.25%, unchanged from yesterday's close.

Note: Bund yields have declined from highs of almost +0.5% in March to current levels. Aside from political concerns in France, investors are paring their fears of a rate rise by the ECB.

U.S Treasury yields trade atop of their five-week lows. The yield on U.S 10's fell -1 bps to +2.35%, after rising +4 bps Tuesday. Expect the shape of the U.S curve to change after today's March FOMC minutes (2:00 pm EST).

Elsewhere, Aussie 10-year yields are flat at +2.61% after dropping -7 bps yesterday.

4. Dollar prices show caution

The FX market is retaining a cautious tone after North Korea fired a ballistic missile into the sea ahead of a two-day summit between U.S and Chinese leaders tomorrow.

The USD/JPY (¥110.94) is little changed ahead of the U.S open despite the traditional 'safe-haven status' of the yen in such a scenario. The U.K's pound (£1,2475) has found some early traction after this morning's U.K data for Mar. PMI services beat expectations (see below).

Note: Sterling watchers are currently following European Parliament members debate its position in the Brexit negotiations.

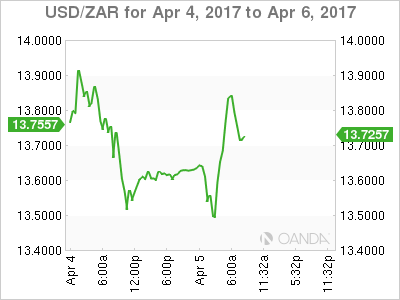

Elsewhere, the USD/ZAR ($13.8375) is +1.5% higher after reports that South African President Jacob Zuma again survived calls to resign by members of the ruling ANC.

5. Euro Services PMI's produce a mixed bag

Major European PMI's Services numbers remain in expansion, but most are succumbing to a slower pace - France and Eurozone are revised lower in their final readings, while the U.K handily beats expectations.

Despite hitting a 15-month high of 55.6 in March, Germany's services PMI highlights rising cost pressure in the sector due to higher wages and fuel prices. Input price inflation hit "a near-six year high," while output prices rise at the sharpest rate in three-years. The data underpin expectations of a pickup in economic growth during Q1.

In the U.K, the Services Sector was lifted by financial services. The headline print registered 55 in Mar., up from 53.3 in Feb. and the strongest reading in three-months. A weakened pound continues to aid exporters, however, quickening inflation is beginning to squeeze consumer-facing sectors. Businesses reported rising costs and tepid job growth.

Crude Oil Nears Resistance Ahead Of Inventories Report

Oil prices have rebounded since March 27, trading above the short term 10 and 20 SMAs on the 4-hourly chart. The rally was helped by OPEC’s consideration of a 6-month output cut extension, and a noticeable drop in EIA crude oil inventories figure (the week ending March 24).

Although OPEC member states have executed the output cut effectively since the agreement was made in December. However, the drop in oil supply has been slower than expected, mainly because the US shale oil industry has been thriving helped by the rising oil prices. Saudi Arabia’s energy minister has warned that 'no free ride' for non-OPEC oil producer competitors.

OPEC will likely decide whether to extend the output cut in their scheduled meeting on May 25 in Vienna. It was reported on March 30 that Kuwait and some other OPEC member states support an extension of output cut, providing oil prices some support. At present, the supply remains high, whether OPEC will extend output cut is still vague.

The trend of spot WTI remains bullish, as it still trades above the short term SMAs. However, the current price is nearing the short-term major resistance level at 52.00. The selling pressure is heavy above the level. Be aware that the bullish momentum is likely to be restrained here.

Both the 4-hourly and the daily Stochastic Oscillators are above 80, suggesting a retracement.

Crude oil inventory (the week ending Mar 31) will be released at 15:30 BST today – always a major influencer in Oil price volatility. It will likely cause volatility for oil prices.

The resistance level is at 52.00, followed by 52.50 and 52.80.

The support line is at 51.50, followed by 51.00 and 50.50.

British Pound Buoyed By Solid Services PMI, ADP And FOMC Minutes In Focus

Sterling received a lifeline on Wednesday following March's solid Service PMI figure of 55.00 which boosted some confidence towards the health of the British economy. UK services activity in March has logged its strongest increase this year and such may mitigate the Brexit jitters as concerns momentarily ease over a slowdown in economic momentum. While the sharp jump in UK services is undeniably impressive given the Brexit uncertainty, some fears may linger over the decline seen in manufacturing and construction PMI this week. Although economic data from the UK continues to display post-Brexit resilience occasionally, the possibility of growth decelerating in the first quarter of 2017 may weigh heavily on sentiment. Despite today's upsurge in prices, Sterling could still be destined to sink lower as the Brexit fueled uncertainties haunt attraction towards the currency.

Speaking of uncertainty, the battle of words between politicians on the Brexit topic has started with a bang as debates take place in Strasbourg. With the European Union setting out its “red lines” for the Brexit negotiations and emphasizing how the divorce terms must be agreed before striking any new trade deals, a rocky road may lie ahead. The worrying fact that the EU continues to demand a £50 billion Brexit divorce bill before any proper talks are in place may heighten concerns over the bloc playing hardball in the negotiation. With Manfred Weber who is a member of the European Parliament already demanding that Britain must give up the right to clear euros once it leaves the European Union adding to the messy mix, Sterling bears remain in close proximity to attack.

Focusing on the foreign exchange outlook, Sterling/Dollar trades within a sticky range with 1.2370 acting as a support and a resistance at1.2570. Although Dollar weakness has the ability to elevate prices higher, the uncertainty and tepid buying sentiment towards Sterling could inspire sellers to attack prices lower in the medium to longer term. On the daily charts, bears must conquer the 1.2370 support level for a further decline towards 1.2200.

In an alternative scenario, a breakout above 1.2570 may signal a defeat to the bears in the short term with the next target at 1.2650. Investors should keep in mind that the Brexit developments and concerns of a hard Brexit may ensure Sterling remains depressed for prolonged periods. Based on this hypothesis, when zooming out onto the weekly timeframe, the long-term bears remain in control below the major 1.2775 resistance level.

ADP and FOMC minutes in focus

The Greenback was on standby on Wednesday with the Dollar Index hovering around 100.50 ahead of the ADP report and FOMC minutes this evening. It is becoming quite clear that Dollar bullish investors are in need of inspiration to elevate the Greenback higher with the pending ADP report acting as a catalyst. A positive ADP that exceeds expectations and heightens speculation of further rate hikes this year could pump some life back into the Dollar.

Investors will be paying very close attention to the Fed minutes this evening which could offer some insights on how the Federal Reserve's plan to unwind its $4.5 trillion balance sheet. Although the “dovish hike” in March exposed the Dollar to downside shocks, any signs of hawks in the pending minutes could offer the Greenback a boost.

Technical Outlook: FTSE 100 – Daily Cloud Top Needs To Contain Dips To Maintain Bullish Signals From Diamond Bottom...

FTSE eased on fresh strength of pound on Wednesday, pulling back from cracked 7280 barrier (Fibo 38.2% of 7444/7179 correction).

Mixed technical studies are lacking clear direction signal for now, however, near-term action off 7179 (27 Mar low) remains supported by rising daily cloud that keeps alive hopes of fresh upside attempts.

Such scenario requires daily Tenkan-sen (7247) and daily cloud top (7241) to hold current easing, as near-term action has formed Diamond bottom pattern which is seen as reversal signal.

Recovery attempts then need to clear initial barrier at 7280 to trigger fresh upside, with break above daily Kijun-sen (7311) that previously capped recovery, needed to confirm reversal.

Conversely, violation of daily cloud top and diamond’s lower boundary (bull-trendline) would generate negative signal and risk further weakness

Res: 7280, 7311, 7343, 7367

Sup: 7247, 7241, 7222, 7190

EURUSD – Halts Weakness, Eyes Recovery Higher

EURUSD - With the pair closing marginally higher on Tuesday, more strength is expected as long as it trades above the 1.0635 level. Resistance comes in at 1.0700 level with a cut through here opening the door for more upside towards the 1.0750 level. Further up, resistance lies at the 1.0800 level where a break will expose the 1.0850 level. Conversely, support lies at the 1.0600 level where a violation will aim at the 1.0550 level. A break of here will aim at the 1.0500 level. All in all, EURUSD faces more bear threats.

French Presidential Debate Brings Forth Slings and Arrows

- US manufacturing slowing

- British Retail Consortium (BRC) Shop Price Index slips

- French Presidential debate brings forth slings and arrows

The latest French Presidential debate delivered fireworks between front-runner Emmanuel Macron and his main rival, Marine Le Pen. Macron was scathing of Le Pen's nationalist agenda, while Le Pen accused Macron of "speaking like old fossils." It is generally considered that Macron performed better than Le Pen and remains ahead in the polls. The EU will be watching with keen interest as Le Pen is still staunchly anti-Euro and anti-EU. The Euro was unmoved by the events, but this morning's EU Service Sector Purchasing Managers' Index (PMI) has the capacity to shift the Euro.

The US Dollar was similarly unmoved by data showing a slowdown in the US manufacturing sector, to its slowest level of growth for six months. The data was still in positive territory, but the US economy is certainly not romping away at the moment. This afternoon's Service Sector Index is expected to be stronger than March's and that will boost the USD - if the forecasts are right - but the minutes from the Federal Reserve meeting being released later in the day will be more influential. When US interest rates will next rise, how many rises will come after it; and how much will the US base rate rise over the next year? This is all the markets really want to know. They won't get all their answers today, but hints will be enough to shift the USD. Dollar buyers may wish to move ahead of that release.

Sterling should probably have fallen this morning after the BRC's Shop Price Index fell by 0.8% after a 0.1% fall in February 2017, but the Service Sector PMI Index is likely to be a little more upbeat; and that will stabilise the Pound.

Other than these snippets, the day is a quiet one... a sunny one in London... and probably a thinly traded one ahead of the US data and Federal Reserve minutes.

Have a terrific Wednesday.

Blind flight crew

The passengers have all been seated on a commercial airliner when the pilot and co-pilot finally appear in the rear of the plane and begin walking up to the cockpit through the centre aisle. Both have dark glasses on; the pilot is using a white cane, bumping into passengers right and left as he stumbles down the aisle. The co-pilot is using a guide dog. At first, the passengers do not react, thinking that it must be some sort of practical joke. After a few minutes, though, the engines start revving, and the plane is shifted into the taxi area before starting to move down the runway. The passengers look at each other with some uneasiness. They start whispering among themselves and look desperately to the stewardesses for reassurance. The plane continues to accelerate and people begin panicking. Some passengers are praying and, as the plane gets closer and closer to the end of the runway, the voices are becoming more and more hysterical with screams and loud prayers being offered up to a number of different deities. When the plane has fewer than 50 yards of runway left, there is a noticeable change in the pitch of the shouts as everyone screams at once. At that very moment, the plane rotates on its axis, lifts off and is airborne. Up in the cockpit, the co-pilot breathes a sigh of relief and turns to the pilot: "You know, one of these days the passengers aren't going to scream, and we won't know when to lift the nose. "