Sample Category Title

DAX Steady On Higher German, Eurozone Services PMI

The DAX Index has edged lower on Wednesday, after an uneventful Tuesday session. Currently, the DAX is trading at 12,242.25. On the release front, services reports are in focus. German Final Services PMI improved to 55.6, matching the forecast. Eurozone Final Services PMI climbed to 56.5, short of the forecast of 56.0 points. In the US, the Federal Reserve releases its minutes from the March policy meeting. On Thursday, Germany releases Factory Orders, and ECB President Mario Draghi speaks at a conference in Frankfurt.

Eurozone indicators continue to point upwards, indicative of an improving eurozone economy. In March, German and Eurozone Services PMIs pointed to expansion. The German release hit a 15-month high, while the Eurozone indicator jumped to a 71-month high, although it missed expectations. The euro shrugged off these strong numbers, as it continues to have an uneventful week. EUR/USD dropped 1.9 percent last week, marking its worst weekly decline since November 2016. Soft inflation numbers late in the week disappointed the markets and soured sentiment on the continental currency. German Preliminary CPI posted a weak gain of 0.2%, short of the forecast of 0.4%. This was followed by Eurozone Flash CPI Estimate, which slipped to 1.5%, missing the forecast of 1.8%. Although inflation levels have improved to their highest levels in years, they remain below the ECB target of 2.0%, so the central bank still has some breathing room and isn’t under immediate pressure to tighten monetary policy. The ECB’s asset purchase program of EUR 60 billion/mth is scheduled to expire in December.

What’s next for the Federal Reserve? With the US economy continuing to perform well, the discussions around the monetary policy tables are not whether the Fed will raise rates, but how many hikes we will see in 2017. The markets will be paying close attention to the minutes of the March meeting, when the Fed raised rates by a quarter-point, to a range of 0.75%-1.00%. Any hints about the timing of the next hike, as well as the tone of the minutes are factors which could move the currency markets on Wednesday. The markets considered the rate statement overly cautious, and this sentiment sent the US dollar broadly lower in March. If the reaction to the minutes is one of disappointment, the dollar could again experience broad losses.

Technical Outlook: BRENT Pressures $54.99 Barrier On Extension Of Strong Bullish Acceleration

Brent oil extends strong bullish acceleration from Tuesday (the biggest one-day gains since 20 Jan), gaining slightly over 1% in early Wednesday's trading.

Tuesday's strong rally closed well above $53.98 (Fibo 61.8% of larger $56.62/$49.70 fall), generating strong bullish signal that resulted in fresh bullish extension that is approaching next barrier at $54.99 (Fibo 76.4% retracement).

Daily technical studies are now in full bullish setup and supportive for further upside action. Break above $54.99 would open way towards key short-term barrier at $56.62 (07 Mar high).

Minor resistance en-route is thin daily cloud that twists next week and would also support bulls.

Broken 55SMA offers immediate support at $54.37, followed by session low at $54.19 and strong supports at $53.98/87 (broken Fibo 61.8% / broken 100SMA) which should contain extended dips, as strongly overbought daily chart slow stochastic suggests a pause in strong rally, but no firmer bearish signal being generated so far.

Res: 54.99, 55.75, 56.06, 56.62

Sup: 54.37, 53.98, 53.87, 53.37

Market Update – European Session: South Africa President Zuma Survives Ruling Party Meeting; UK Services PMI Beats Expectations

Notes/Observations

FOMC Minutes in Focus; looking for indications on how much the Fed has discussed balance sheet reduction

Major European PMI Services numbers remain in expansion but most succumbing to a slower pace; France and Euro Zone revised lower in their final readings; UK handily beats

Overnight:

Asia:

North Korea launches missile into waters off Korean peninsula's east coast (towards Japan) ahead of China-US leader meeting

PBoC skipped open market operations for 8th straight session; drained CNY90B

Europe:

Eurogroup Chief Dijsselbloem: Good progress being made in talks with Greece

Elabe Presidential survey, Melenchon seen as most convincing candidate in Tuesday's election debate, Macron second

Americas:

Richmond Fed President Lacker resigned effective Apr 4th over improper disclosure of confidential FOMC information, earlier than planned

Energy:

Weekly API Oil Inventories: Crude: -1.8M v +1.9M prior; first draw in 3 weeks

Economic Data

(IE) Ireland Mar Services PMI: 56.9 v 60.6 prior (56th month of expansion), Composite PMI: 59.1 v 57.8 prior

(RU) Russia Mar PMI Services: 56.6 v 55.0e (14th month of expansion), PMI Composite: 56.3 v 55.4 prior

(SE) Sweden Mar PMI Services: 61.3 v 59.5e

(ZA) South Africa Mar PMI (Whole Economy): 50.7 v 50.5 prior

(ES) Spain Mar Services PMI: 57.4 v 57.4e (41st month of expansion), Composite PMI: 56.8 v 57.0e

(SE) Sweden Feb Industrial Production M/M: 0.2% v 0.1%e; Y/Y: 4.1% v 1.8%e

(IT) Italy Mar Services PMI: 52.9 v 54.3e (10th month of expansion), Composite PMI: 54.2 v 54.9e

(FR) France Mar Final Services PMI: 57.5 v 58.5e (9th month of expansion and highest since May 2011), Composite PMI: 56.8 v 57.6e

(DE) Germany Mar Final Services PMI: 55.6 v 55.6e (confirms 45th month of expansion and highest reading since Dec. 2015), Composite PMI: 57.1 v 57.0e

(EU) Euro Zone Mar Final Services PMI: 56.0 v 56.2e (confirms 45th month of expansion); Composite PMI: 56.4 v 56.7e

(UK) Mar Services PMI: 55.0 v 53.4e (8th month of expansion), Composite PMI: 54.9 v 53.8e v 53.8 prior

Fixed Income Issuance:

(DK) Denmark sold total DKK2.02B in 2021 and 2027 Bonds

(IN) India sold total INR140B vs. INR140B indicated in 3-month and 6-month Bills

(SE) Sweden sold SEK2.5B vs. SEK2.5B indicated in 0.75% 2028 bonds; Avg Yield: 0.8090% v 0.9444% prior; Bid-to-cover: 2.58x v 1.86x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Index snapshot (as of 10:00 GMT)

Indices [Stoxx50 flat at 3,479, FTSE +0.2% at 7,335, DAX -0.3% at 12,245, CAC-40 flat at 5,102, IBEX-35 +0.4% at 10,401, FTSE MIB +0.1% at 20,276, SMI -0.1% at 8,640, S&P 500 Futures -0.1%]

Market Focal Points/Key Themes: European equity indices are trading mixed despite an overall positive end to the Asian session overnight; Dax underperforming weighed by shares of car manufacturers Volkswagen, Daimler and BMW; energy stocks across Europe trading notably higher as oil trades sharply higher intraday; homebuilder stocks trading notably lower in the FTSE 100; banking stocks trading mostly higher providing some support across some of the major indices.

Upcoming scheduled US earnings (pre-market) include Greenbrier Companies, Monsanto, and Walgreens Boots Alliance.

Equities (as of 09:50 GMT)

Consumer Discretionary: [Bovis Homes BVS.UK +2.1% (operational update, new CEO, Galliford Try confirms no longer interested in combination), DCC Plc DCC.UK +1.7% (to acquire Shell's LPG business, CEO transition), Galliford Try GFRD.UK +0.6% (confirms no longer interested in Bovis combination), Hollywood Bowl Group BOWL.UK +2.9% (H1 sales)]

Energy: [Premier Oil PMO.UK +4.1% (sales of Pakistan business for $65.6M)]

Industrials: [John Wood Group WG.UK +3.3% (Increased cost synergies as a result of offer for Amec Foster Wheeler), Obrascon Huarte Lain OHL.ES +1.4% (FY17 and FY18 outlook), Telford Homes TEF.UK +2.5% (trading update)]

Speakers

South Africa President Zuma retained support of ANC following key meeting (Zuma survived calls to resign as President)

ECB's Likanen (Finland): Reiterates General Council view that interest rates would remain low beyond end of asset purchases. Improvements not seen big enough to fundamentally change guidance, strong monetary support was still required

European Parliament members debated on a resolution setting out its position in the negotiations

EU's Weber: EU was ready for negotiations; must prepare for hard stance

EU's Verhofstadt: EU-UK relationship had never been easy

EU's Barnier: No deal scenario was NOT the one the EU was looking for

German Economy Ministry report on ECB monetary policy: Zero interest rates damaged the financial system

Italy Stats Agency (ISTAT) Monthly Economic Note: Q2 GDP growth seen slower but likely to continue at same pace going forward

Russia Central Bank (CBR) Gov Nabiullina: Regardless of oil price, GDP growth to stabilize around 1.5-2.0% without structural reformseasy

Russia Econ Min Oreshkin: Domestic economy is actively growing

Currencies

FX markets retained a cautious tone after North Korea fired a ballistic missile into the sea ahead of a summit between US and Chinese leaders. The USD/JPY was little changed at 110.65 area despite the traditional safe-haven status of the Japanese currency under such siotuations.

The GBP/USD found some traction after UK Mar PMI Services beat expectations. Pair higher by 0.3% just ahead of the NY morning as it approached the 1.25 handle. The FX market was watching the European Parliament members debate its position in the Brexit negotiations

The USD/ZAR pair was higher after reports that South African President Jacob Zuma again survived calls to resign by members of the ruling African National Congress

Fixed Income:

Bund futures trade at 162.38 down 15 ticks reversing earlier gains after mixed European PMI data. Support moves to 162.07 initially followed by 161.52 then 161.02. A move back higher targets 162.72 followed by 162.98 then Feb contract high at 163.12.

Gilt futures trade at 128.06 down 31 ticks pressured by stronger UK Services PMI data which came ahead of consensus and marked an 8th month of expansion. Support remains at 127.75 then 127.34 followed by 127.05. Resistance remains at 128.96 followed by 129.24. Short Sterling futures have steepened following the stronger data with Jun17Jun18 coming of day lows to trade at 13.5/14bp

Wednesday's liquidity report showed Tuesday's excess liquidity rose sharply to €1.575T a rise of €131B from €1.444T prior. Use of the marginal lending facility fell to €114M from €212M prior.

Corporate issuance saw $8.4B come to market via 5 issuers headlined by European Banking name Banco Santander 3 part $2.5B offering and ABN Amro 2 part $1.25B offering alongside Cenovus Energy $2.9B 3 part offering. This puts weekly issuance at $11.2B.

Looking Ahead

(RO) Romania Central Bank (NBR) Interest Rate Decision: Expected to leave Interest Rates unchanged at 1.75%

05:30 (ZA) South Africa Mar Sacci Business Confidence: No est v 95.5 prior

05:30 (DE) Germany to sell €4.0B in 0% Apr 2022 BOBL

06:00 (PL) Poland Central Bank (NBP) Interest Rate Decision: Expected to leave Base Rate unchanged at 1.50%

06:00 (IE) Ireland Feb Industrial Production M/M: No est v 3.4% prior; Y/Y: No est v -9.4% prior

07:00 (US) MBA Mortgage Applications w/e Mar 31st: No est v -0.8% prior

07:00 (RU) Russia to sell combined RUB43B in OFZ bonds

07:30 (CL) Chile Feb Economic Activity Index (Monthly GDP) M/M: -1.0%e v +0.4% prior; Y/Y: -1.4%e v +1.4% prior (revised from 1.7%)

08:00 (BR) Brazil Mar PMI Services: No est v 46.4 prior; PMI Composite: No est v 46.6 prior

08:00 (UK) EU Commissioner Oettinger (Germany) speaks on Brexit

08:00 (RO) Romania Central Bank Gov Isarescu post rate decision press conference

08:15 (US) Mar ADP Employment Change: +185Ke v +298K prior

08:15 (UK) Baltic Dry Bulk Index

08:30 (UK) BOE Vlieghe speaks in London

09:00 (MX) Mexico Mar Consumer Confidence: 79.0e v 75.7 prior

09:00 (MX) Mexico Jan Gross Fixed Investment: 0.8%e v 0.9% prior

09:45 (US) Mar Final Markit Services PMI: 53.1e v 52.9 prelim, Composite PMI: No est v 53.2 prelim

10:00 (US) Mar ISM Non-Manufacturing Composite: 57.0e v 57.6 prior

10:00 (PL) Poland Central Bank Gov Glapinski post rate decision press conference

10:30 (US) Weekly DOE Crude Oil Inventories

13:00 (EU) Germany Fin Min Schaeuble speaks on EU crisis as an opportunity

14:00 (US) FOMC Minutes from Mar 15th Meeting

15:00 (MX) Mexico Citibanamex Survey of Economists

Technical Outlook: US OIL – Strong Bullish Sentiment On Supply Tightening Drives Oil Price To Nearly One–Month High

US oil is maintaining strong bullish sentiment and extends gains on Wednesday. Strong rally of the previous day started after brief probe below psychological $50.00 support proved to be short-lived and stronger bullish acceleration was triggered by stronger than expected draw in US crude stocks.

American Petroleum Institute data, released on Tuesday, showed surprise fall of 1.8 million barrels in crude stocks vs forecasted draw of 0.5 million barrels and 1.9 million barrels build previous week.

Initial signs of gradual tightening in global /rates-charts/dbwti/trading-positions inventories and concerns about a supply outage from North Sea oil fields, gave strong boost to the oil prices.

Resumption of broader recovery rally from $47.06 base on Tuesday’s 1.7% gains and close above $51.00 handle, was seen as strong bullish signal for today’s fresh extension higher.

WTI contract for May delivery hit the highest level in nearly one month and pressuring next barrier at $51.68 (55SMA), break of which would open next pivot at $51.97 (Fibo 61.8% of $55.01/$47.06 descend).

However, strongly overbought slow stochastic on daily chart warns of possible hesitation ahead of key barriers, but no firmer bearish signal being generated so far.

Broken 100SMA marks initial support at $51.29, ahead of session low at $51.10 and broken daily Kijun-sen at $50.73, which should contain extended dips.

Res: 51.68, 51.97, 52.53, 52.90

Sup: 51.29, 51.10, 50.73, 50.10

SNB Continues Intervention, But With Greater Tolerance Over Swiss Franc’s Strength

EURCHF recovered after declining over the past three weeks. Political uncertainty and diminished expectations of ECB's QE tapering has pressured the single currency and raised demand for safe-haven assets. Despite the selloff to as low as 1.0629 in February, EURCHF had then rebounded to a 3-month high of 1.0825 in mid-March, before settling at 1.068 at end-1Q17. This came in line with over forecast of 1.07 for the first quarter. Movement of USDCHF was, however, more volatile than we had anticipated. The currency pair indeed broke below 1, plunging to a 4.5-month low of 0.9812 on March 27 before returning to parity on March 31.

We attribute the sharper-than-expected weakness in US dollar over the past quarter to the inability of US President Donald Trump's administration. Indeed, the market has turned less optimistic over the president's pro-growth policy, after the withdrawal of the healthcare bill. However, the price movements in the first quarter do not alter our view that SNB has turned more tolerable to franc's appreciation, although FX intervention would continue should euro's selloff accelerate.

SNB new exchange rate index

SNB unveiled in its latest quarterly bulletin a new method to calculate Swiss franc's exchange rate index. The central bank indicated that the new method "allows the Swiss economy's competitive and trading relationships to be replicated in a more comprehensive and up-to-date way". It laid down three key differences between the new and old methods.

- First, the weighting of a specific country in the new method is based both on exports to and imports from this country as well as on so-called third-market effects. As such, the new method gives greater consideration to competitive relationships between Switzerland and its trading partners than the previous one.

- Second, the calculation of the country weightings includes global trade in both goods and services, compared with only goods in the old one.

- Finally, the new index is chained, in contrast to the fixed base period of the previous index. SNB suggested that this allows the group of countries taken into consideration in the index to be reviewed every year.

With the December 2000 reading set at 100, the nominal effective exchange rate index using the new method was 156.5 in early March, compared with 155 under the old method. Meanwhile the real exchange rate index was revised to around 114, compared with the previous reading around 120.

The real index at December 2000 was set at zero. According to SNB, the new indices continue to show that the Swiss franc is "significantly overvalued". In our opinion, the downward revision of the real index signals that the degree of overvaluation is less extreme, offering SNB more rooms to avoid aggressive intervention.

SNB bought CHF 67.1b of foreign currencies in 2016

Indeed, SNB was more constrained in FX intervention last year, when compared with the prior year. The latest statistics show that the central bank bought CHF 67.1B worth of foreign currencies in 2016, compared with CHF 86.1B in 2015 when it intervened aggressively soon after removing the EURCHF floor of 1.2.

According to SNB, FX intervention "occurred mainly at times of heightened uncertainty, when the Swiss franc was particularly sought after as a safe investment". The March FX reserve data, due Friday, is closely watched. The market currently expects a widening of +CHF 5.8B to CHF 674B for the month.

Euro Subdued As German, Eurozone Service PMIs Improve

EUR/USD is unchanged in the Wednesday session, as the euro continues to have a quiet week. Currently, the pair is trading at 1.0680. On the release front, services reports are in focus. German Final Services PMI improved to 55.6, matching the forecast. Eurozone Final Services PMI climbed to 56.5, short of the forecast of 56.0 points. The US will release ADP Nonfarm Payrolls as well as the ISM Non-Manufacturing PMI. As well, the Federal Reserve releases its minutes from the March policy meeting.

Eurozone indicators continue to point upwards, and German and Eurozone Services PMIs pointed to expansion in March. The German release hit a 15-month high, while the Eurozone indicator jumped to a 71-month high, although it missed expectations. The euro shrugged off these strong numbers, as it continues to have an uneventful week. EUR/USD dropped 1.9 percent last week, marking its worst weekly decline since November 2016. Soft inflation numbers late in the week disappointed the markets and soured sentiment on the continental currency. German Preliminary CPI posted a weak gain of 0.2%, short of the forecast of 0.4%. This was followed by Eurozone Flash CPI Estimate, which slipped to 1.5%, missing the forecast of 1.8%. Although inflation levels have improved to their highest levels in years, they remain below the ECB target of 2.0%, so the central bank still has some breathing room and isn’t under immediate pressure to tighten monetary policy. The ECB’s asset purchase program of EUR 60 billion/mth is scheduled to expire in December.

What’s next for the Federal Reserve? With the US economy continuing to perform well, the discussions around the monetary policy tables are not whether the Fed will raise rates, but how many hikes we will see in 2017. The markets will be paying close attention to the minutes of the March meeting, when the Fed raised rates by a quarter-point, to a range of 0.75%-1.00%. Any hints about the timing of the next hike, as well as the tone of the minutes are factors which could move the currency markets on Wednesday. The markets considered the rate statement overly cautious, and this sentiment sent the US dollar broadly lower in March. If the reaction to the minutes is one of disappointment, the dollar could again experience broad losses.

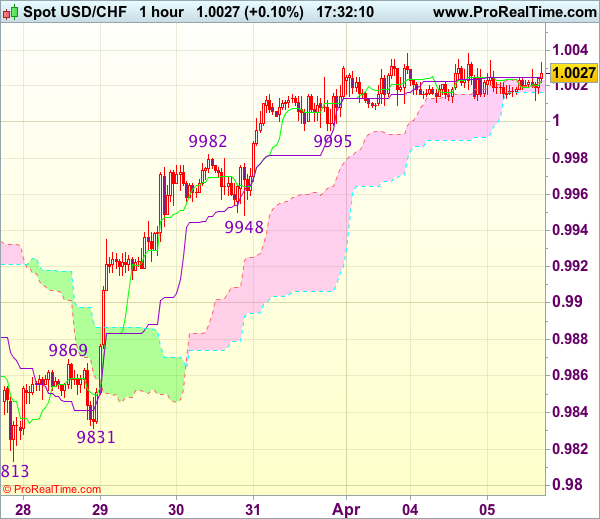

Trade Idea Update: USD/CHF – Buy at 0.9950

USD/CHF - 1.0027

Original strategy :

Buy at 0.9950, Target: 1.0050, Stop: 0.9915

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9950, Target: 1.0050, Stop: 0.9915

Position : -

Target : -

Stop : -

As the greenback has continued trading with a firm undertone after last week’s rally above 1.0003 resistance, suggesting recent rise from last week’s low at 0.9813 is still in progress and bullishness remains for this move to extend gain to previous support at 1.0060 (now resistance), however, loss of upward momentum should prevent sharp move beyond resistance at 1.0109, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy dollar on pullback as said support at 0.9948 should limit downside. Below 0.9931 (50% Fibonacci retracement of 0.9831-1.0031) would abort and signal top is formed instead, bring correction to 0.9905-10 (61.8% Fibonacci retracement) but reckon previous resistance at 0.9869 would hold from here.

Trade Idea Update: GBP/USD – Hold short entered at 1.2465

GBP/USD - 1.2481

Original strategy :

Sold at 1.2465, Target: 1.2365, Stop: 1.2500

Position : - Short at 1.2465

Target : - 1.2365

Stop : - 1.2500

New strategy :

Hold short entered at 1.2465, Target: 1.2365, Stop: 1.2500

Position : - Short at 1.2465

Target : - 1.2365

Stop : - 1.2500

As cable has rebounded again after holding above support at 1.2419, suggesting further consolidation above this level would be seen, however, as long as indicated resistance at 1.2496 holds, mild downside bias remains for another fall, below said support at 1.2419 would bring test of 1.2400 but break there i needed to add credence to our view that the rebound from 1.2377 has ended at 1.2559, bring further fall towards support at 1.2377. Looking ahead, only a drop below 1.2377 would confirm the fall from 1.2616 is still in progress for subsequent decline towards key support at 1.2335.

In view of this, we are holding on to our short position entered at 1.2465 but one should exit on such decline. Only break of said resistance at 1.2496 would abort and suggest an intra-day low is formed instead, risk a stronger rebound to 1.2525-30.

FOMC Minutes And ADP Employment In Focus, Oil Prices Rise

News and Events:

US Dollar subject to downside risk heading into FOMC minutes

Most currency pairs have been trading sideways so far this week as investors remained reluctant to choose sides between Dollar bears or bulls. Obviously against this backdrop of uncertainties, the Japanese Yen took the best of the situation and extended gains as it returned below the 111 threshold. Investors will however slowly get out of the rut as a few pieces of key economic data are due for release before Friday, as well as the minutes of the March FOMC meeting.

The ADP job report is due for release at GMT 12:15 today. The market is expecting a much lower reading compared to February, when the pace of hiring exploded and printed at 298k versus 187k median forecast. For March, the market is expecting a reading closer to 185k. On our side, we believe that there is a substantial chance that February's reading will be revised downwards. Over the last few months, the Federal Reserve has been slowly shifting its communication, putting less emphasis on the headline unemployment rate and the pace of job creation, but rather stressing developments in the underemployment rate and core inflation.

Today's job report, just as Friday's NFPs, will therefore have little impact on the course of the USD. On the other hand, March's FOMC minutes that are due for release at GMT 18:00 could matter. Especially in the event of a dovish surprise which would eventually weigh on the greenback. The risk is definitely a downwards shift for the USD as we head into the minutes.

French Elections: Mélenchon risk to single currency is underestimated

The second debate of the French Presidential Election was broadcast yesterday, during which the 11 candidates had the chance to expose their views on many different topics. Emmanuel Macron was widely expected to win and he was hardly attacked by the other candidates. No candidate performed badly and so it was very hard to find a winner.

In the markets, we can see the CAC 40 is improving more slowly than the Euro Stoxx 50. We try to measure investors' fear and we believe banks' stocks price are a good proxy for that. It is clear that their volatility is increasing.

Currency-wise, we do not see the single currency improving should Macron or Francois Fillon get elected. There is also a growing risk for the single currency as we believe Jean-Luc Mélenchon's chance of winning is underestimated. His performances in the debates are always one of the most accomplished, if not the best. And his “Plan B” is that in the case of negotiation failure, he would not hesitate to ask for a Frexit referendum. So we now assume that Euro downside risks are not anymore only due to Marine Le Pen.

Oil-linked FX gets a boost

Oil prices rallied to a one-month high as expectations increased ahead of today's EIA inventories reports. There are clear signs that U.S inventories have fallen from record high levels. WTI crude today has reached $51.50 in early European trading on tightening supplies speculation. Improving US consumer health has seen a deeper draw on gasoline stockpiles. Gasoline supplies fell 3.7 million barrels while distillates stockpiles dropped 2.5 million barrels last week. In addition, potential supply disruptions in Libya and an unscheduled production outage in the North Sea provide further support for higher crude prices.

Crude bullish sentiment has given oil-linked FX a boost. Global storage inventories have been a overhang to higher prices. As glut is substantially reduced, crude prices can move higher. Mexican Peso (MXN) and Ruble (RUB) have led the gainers on the Emerging Markets side. Oil and gas stocks were the second best sector in equities. We are constructive on the complete crude trade since global economic conditions (improvement in trade and manufacturing) are driving additional crude demand. OPEC capped production limits by 1.2 million barrels and any extension (unlikely to end in May) might have seemed trivial at the time. However, with global fundamentals strengthening and heading to the summer driving season every barrel counts.

Today's Key Issues (time in GMT):

- Bank of Russia Governor Speaks at Moscow Exchange Forum

- RUB / 07:00Mar Standard Bank South Africa PMI, last 50,5 ZAR / 07:15

- Mar Markit Spain Services PMI, exp 57,4, last 57,7 EUR / 07:15

- Mar Markit Spain Composite PMI, exp 57, last 57 EUR / 07:15

- Feb Industrial Production MoM, exp 0,10%, last 2,00%, rev 3,30% SEK / 07:30

- Feb Industrial Production NSA YoY, exp 1,80%, last 1,30%, rev 4,30% SEK / 07:30

- Feb Industrial Orders MoM, last -2,60%, rev -3,30% SEK / 07:30

- Feb Industrial Orders NSA YoY, last 0,00%, rev 0,50% SEK / 07:30

- Feb Service Production MoM SA, exp -1,00%, last 1,10%, rev 0,90% SEK / 07:30

- Feb Service Production YoY WDA, last 7,70%, rev 6,80% SEK / 07:30

- RBA's Heath Bloomberg Panel Participation AUD / 07:30

- Mar Markit/ADACI Italy Services PMI, exp 54,3, last 54,1 EUR / 07:45

- Mar Markit/ADACI Italy Composite PMI, exp 54,9, last 54,8 EUR / 07:45

- Mar F Markit France Services PMI, exp 58,5, last 58,5 EUR / 07:50

- Mar F Markit France Composite PMI, exp 57,6, last 57,6 EUR / 07:50

- Mar F Markit Germany Services PMI, exp 55,6, last 55,6 EUR / 07:55

- Mar F Markit/BME Germany Composite PMI, exp 57, last 57 EUR / 07:55

- Mar F Markit Eurozone Services PMI, exp 56,5, last 56,5 EUR / 08:00

- Mar F Markit Eurozone Composite PMI, exp 56,7, last 56,7 EUR / 08:00

- Mar New Car Registrations YoY, last -0,30% GBP / 08:00

- Spain Reserves EUR / 08:00

- Istat Releases the Monthly Economic Note EUR / 08:00

- Mar Markit/CIPS UK Services PMI, exp 53,4, last 53,3 GBP / 08:30

- Mar Markit/CIPS UK Composite PMI, exp 53,8, last 53,8 GBP / 08:30

- Mar Official Reserves Changes, last $360m GBP / 08:30

- 4Q Unit Labor Costs YoY, exp 2,00%, last 2,30%, rev 2,50% GBP / 08:30

- Mar SACCI Business Confidence, last 95,5 ZAR / 09:30

- mars.31 MBA Mortgage Applications, last -0,80% USD / 11:00

- Mar Markit Brazil PMI Composite, last 46,6 BRL / 12:00

- Mar Markit Brazil PMI Services, last 46,4 BRL / 12:00

- Mar ADP Employment Change, exp 185k, last 298k USD / 12:15

- BOE Policy Maker Gertjan Vlieghe Speaks in London GBP / 12:30

- Apr 3 CPI WoW, last 0,00% RUB / 13:00Apr 3 CPI Weekly YTD, last 1,00% RUB / 13:00

- Mar F Markit US Services PMI, exp 53,1, last 52,9 USD / 13:45

- Mar F Markit US Composite PMI, last 53,2 USD / 13:45

- Mar ISM Non-Manf. Composite, exp 57, last 57,6 USD / 14:00

- mars.31 DOE U.S. Crude Oil Inventories, exp -150k, last 867k USD / 14:30

- mars.31 DOE Cushing OK Crude Inventory, exp 125k, last -220k USD / 14:30

- Mar Commodity Price Index YoY, last -9,91% BRL / 15:30

- Mar Commodity Price Index MoM, last -2,37% BRL / 15:30

- Currency Flows Weekly BRL / 15:30

- mars.15 FOMC Meeting Minutes USD / 18:00

- Mar CPI YTD, exp 1,00%, last 0,80% RUB / 22:00

- Mar CPI MoM, exp 0,20%, last 0,20% RUB / 22:00

- Mar CPI YoY, exp 4,30%, last 4,60% RUB / 22:00

- Mar CPI Core MoM, exp 0,20%, last 0,20% RUB / 22:00

- Mar CPI Core YoY, exp 4,60%, last 5,00%, rev 5,00% RUB / 22:00

- 1Q Consumer Confidence Index, last -18 RUB / 22:00

The Risk Today:

EUR/USD is getting lower despite ongoing consolidation. The pair is heading lower since the pair failed to hold above former resistance given at 1.0874 (08/12/2017 high). Hourly support can be found at 1.0643 (03/04/2017 low). Stronger support can be found at 1.0493 (22/02/2017 low). The short-term technical structure indicates further weakness.. In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD's bullish pressures have faded abruptly. Hourly resistance is located at 1.2615 (27/03/2017 high) while hourly support can be found at 1.2324 (03/17/2017 low). Expected to show continued strengthening towards resistance at 1.2775 (06/12/2016 high) if support area around 1.24 stands. The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY's bearish pressures are fading. Hourly resistance is given at 112.20 (31/03/2017 high). Stronger resistance can be located at 113.57 (16/03/2017 high) while support is given at 110.11 (27/03/2017 low). We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

USD/CHF is strengthening. Hourly support is given at 0.9814 (27/03/2017 low). Key resistance can be found at a distance at 1.0344 (15/12/2016 high). Expected to show further consolidating. In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

| EURUSD | GBPUSD | USDCHF | USDJPY |

| 1.1300 | 1.3121 | 1.0652 | 118.66 |

| 1.0954 | 1.2775 | 1.0344 | 115.62 |

| 1.0906 | 1.2706 | 1.0171 | 112.20 |

| 1.0669 | 1.2504 | 1.0024 | 110.80 |

| 1.0494 | 1.2377 | 0.9814 | 108.50 |

| 1.0341 | 1.2110 | 0.9550 | 106.04 |

| 1.0000 | 1.1986 | 0.9444 | 101.20 |

Trade Idea Update: EUR/USD – Sell at 1.0730

EUR/USD - 1.0668

Original strategy :

Sell at 1.0730, Target: 1.0610, Stop: 1.0765

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0730, Target: 1.0610, Stop: 1.0765

Position : -

Target : -

Stop : -

As the single currency has recovered after falling to 1.0635 yesterday, suggesting minor consolidation above this level would be seen and corrective bounce to 1.0702 cannot be ruled out, however, reckon 1.0730-40 would limit upside and bring another decline, below said support at 1.0635 would add credence to our bearish view that the decline from 1.0906 top is still in progress and extend further weakness to 1.0620, then test of previous chart support at 1.0600, however, a sustained breach below the latter level is needed to retain downside bias for subsequent selloff to 1.0570-75 first.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 1.0730-40 should limit upside. Only a firm break above resistance at 1.0773 would suggest low is formed instead, bring a stronger rebound to 1.0800 but resistance at 1.0827 should remain intact.