Sample Category Title

AUD/USD Elliott Wave Analysis

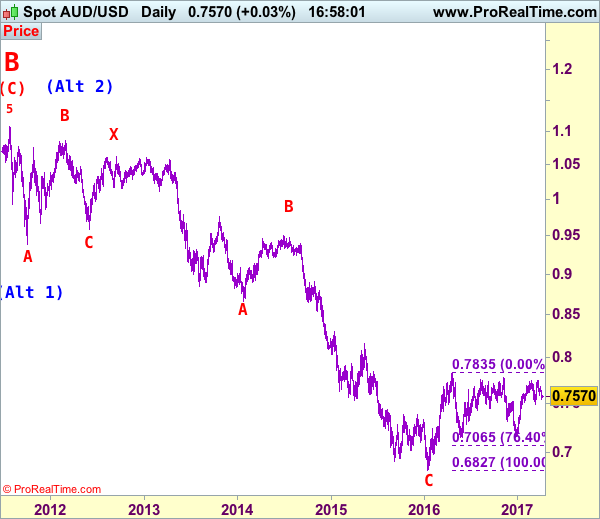

AUD/USD – 0.7574

AUD/USD – Wave 5 of C and (B) has possibly ended at 1.1081

Although aussie met resistance at 0.7680 last week and has slipped again, retaining our view that further consolidation would take place and marginal weakness from here cannot be ruled out, however, reckon 0.7540-45 would limit downside and bring rebound later, above resistance at 0.7680 would suggest low is possibly formed but break of indicated resistance at 0.7750 is needed to extend recent rise from 0.7158 to previous chart resistance at 0.7778. Having said that, a break there is needed to retain bullishness and signal another leg of major corrective upmove from 0.6827 low is underway for headway to 0.7835 resistance first, then 0.7900, however, psychological resistance at 0.8000 should hold from here.

We are keeping our count that top has been formed at 1.1081 (wave 5 of V) and major correction (A-B-C-X-A-B-C) has commenced, indicated downside targets at 0.7945 (61.8% Fibonacci retracement of entire rise from 0.6007-1.1081) and 0.7750 had been met and downside bias is seen for further weakness to 0.6800, then 0.6700 but reckon 0.6500 would hold from here.

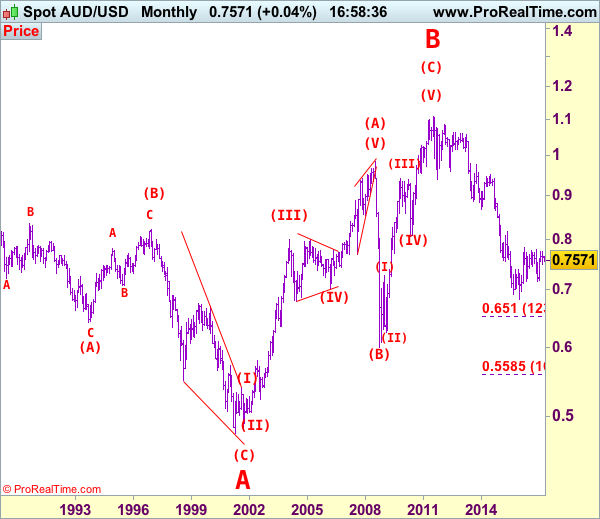

Our preferred count is that the rally from 0.6007 to 0.7270 (7 Jan 2009) is marked as wave A, the retreat to 0.6248 (2 Feb 2009) is wave B and the subsequent upmove is labeled as wave C with wave (iii) and wave (iv) ended at 0.8265 and 0.7700 respectively and wave (v) as well as 3 ended at 0.9407, then wave 4 ended at 0.8066 (instead of 0.8578). The wave 5 has met our indicated projection target of 1.1060 and could ended at 1.1081, this level is now treated as the peak of wave (C) as well as larger degree wave B, hence major fall in wave C has commenced, our initial downside target at psychological support at 0.7000 has just been met and further weakness to 0.6500 would be seen later.

On the downside, expect pullback to be limited to 0.7540-45 and bring another rise later. Only a drop below indicated support at 0.7491 would abort and signal the aforesaid rise from 0.7158 has ended, bring further fall to 0.7450, then towards 0.7400.

Recommendation: Hold long entered at 0.7600 for 0.7800 with stop below 0.7550

Our alternate count on the daily chart treated the top formed in 2008 at 0.9851 could be a larger degree wave I and was followed by a deep and sharp correction in wave II to 0.6007 and wave III is unfolding from there.

The long-term uptrend started from 0.4775 (2 Apr 2001) with an impulsive structure. Wave I is labeled as 0.4775 to 0.9851 (15 Jul 2008), wave II has ended at 0.6007 (Oct 2008) and wave III is still in progress which may extend further gain to 1.1265.

How Will FOMC Minutes And US ISM Data Affect USD ?

The dollar index hit a 3-week high of 100.59 yesterday. However, it pulled back after testing the near-term major resistance at 100.50. It currently holds above the support level at 100.30. The crucial US ISM figure will be released this afternoon at 15:00 BST; the non-manufacturing PMI (Mar). This data release will affect USD and USD crosses. US ISM non-manufacturing PMI readings have kept above 50 since February 2010, showing the service sector remains sound.

US ISM manufacturing PMI released on Monday has seen an uptrend since September 2016. The latest figure for March, released on Tuesday, was 57.2 which saw the 94th straight month above 50 indicating the manufacturing sector is still expanding. However, the figure was lower than the previous figure of 57.7. It saw a slowdown for the first time since September 2016 caused by a rise of production costs.

Although rising prices weigh on the manufacturing sector it has pushed inflation up to the Fed's 2% target. The PCE (YoY) inflation figure for February rose to 2.1% which was the first time above 2% for the past five years.

The UK Markit services PMI (March) will be released at 09:30 BST today. This figure has seen an uptrend since August 2016, however, it has declined since January 2017. GBP/USD has retraced in the past two days; the current price holding above the near-term major support line at 1.2400. The service sector accounts for over 80% of the UK economy, the UK service PMI released today will likely affect GBP and GBP crosses.

This afternoon we will see a series of important US data released – be aware that it will likely cause volatility for USD and USD crosses. ADP employment change (March) at 13:15 BST, which is regarded as a prediction of the non-farm payrolls (March) released this Friday. The Markit services and composite PMIs (Mar) at 14:45 BST. Most importantly we see the release of ISM non-manufacturing PMI (Mar) at 15:00 BST. Crude oil inventory (the week ending Mar 31) is also released at 15:30 BST – always a major influencer in Oil price volatility.

The FOMC minutes will be released this evening at 19:00 BST. The Fed raised rates in the March 15 meeting. Recently several Fed officials have commented on prospective rate hikes, mostly in an optimistic tone, with the likelihood of two more rate hikes by the end of the year. We will likely get more clues about the probability of a rate hike in upcoming FOMC meetings and from the resulting minutes. Per the CME's FedWatch tool the probability of a rate hike in June is around 59%.

The first Trump-Xi meeting is scheduled for Thursday April 6; be aware that this political event will likely outweigh the economic data performance.

Technical Outlook: AUDUSD Is Consolidating Above 200SMA – Bears Look For Break Lower

The Aussie extended weakness deep in the daily cloud on strong four-day bearish acceleration from 0.7677 (30 Mar lower top) that hit low at 0.7543 but so far failing to close below pivot at 0.7548 (200SMA) and generate another bearish signal. The pair is riding on the third wave of five-wave cycle from 0.7747 high that is eyeing target at 0.7528 (Fibonacci 100% expansion) and could extend towards 0.7472 (FE 138.2%) on break below other strong supports at 0.7507 (100SMA) and 0.7489 (09 Mar low). Daily studies are negative and favor further weakness, as formation of daily Tenkan-sen/Kijun-sen bear cross maintains bearish pressure. Consolidation above 200SMA could be anticipated, with initial barrier at 0.7585 (session high) and extended upticks expected to hold below daily Tenkan-sen (0.7610).

Res: 0.7585, 0.7610, 0.7618, 0.7638

Sup: 0.7548, 0.7528, 0.7507, 0.7489

Technical Outlook: USDJPY – Hourly Cloud Limits Recovery Attempts And Keeps Bearish Bias

The pair maintains bearish bias despite yesterday's Hammer that could be seen as initial reversal signal. Bounce from yesterday's low at 110.25 remains capped under thick falling hourly Ichimoku cloud (spanned between 110.77 and 111.25) and suggests consolidation before final attempts below key 110.00 support zone. Firm bearish setup of daily studies supports scenario. However, attack at 110.00 zone may be delayed on extension above hourly cloud and Friday's close above weekly cloud top (111.36)

Res: 110.77, 111.05, 111.14, 111.36

Sup: 110.52;110.25, 110.09, 109.91

Technical Outlook: Cable – Bears Are Pausing Ahead UK Data

Cable is consolidating above 100SMA (1.2413) which so far contained strong two-day fall from 1.2553 high. Recovery attempts were so far limited, keeping the downside at risk, as the pair is awaiting UK Services PMI data for fresh signals. Negative tone is prevailing on near-term studies and could be boosted if UK data disappoint. This could result in final break below 100SMA and attack at next supports at 1.2360 (daily Kijun-sen) and 1.2345 (daily cloud base), loss of which would generate strong bearish signals. At the upside, key barriers lay at 1.2494/97 (daily Kijun-sen / Ichimoku cloud top) and only sustained break above would sideline downside threats. Daily cloud is narrowing and lowering tops continue to weigh.

Res: 1.2446, 1.2494, 1.2529, 1.2553

Sup: 1.2413, 1.2390, 1.2374, 1.2360

Technical Outlook: EURUSD – Reversal Signals Need Sustained Break Above 1.0700 Pivot For Confirmation

Repeated failure to close below 1.0650 Fibo 61.8% support, despite yesterday’s marginally lower low at 1.0634, signal strong hesitation ahead of key supports at 1.0622 (100SMA / daily cloud top).

Long lower shadows of daily candles of past two days suggest possible basing attempt, as Tuesday’s trading was shaped in Hammer candle.

The notion is supported by slow stochastic reversal from oversold territory.

However, bounce was so far unable to clearly break above 55SMA (1.0672), despite upticks to 1.0683 (session high), keeping upper pivot at 1.0700 (daily Kijun-sen) intact for now.

Close above 1.0700 is needed to generate firmer bullish signal for stronger correction of the downleg from 1.0905 (27 Mar high).

Conversely, prolonged consolidation under 1.0700 could be expected ahead of fresh push lower.

Res: 1.0683, 1.0700, 1.0721, 1.0737

Sup: 1.0665, 1.0650, 1.0634, 1.0622

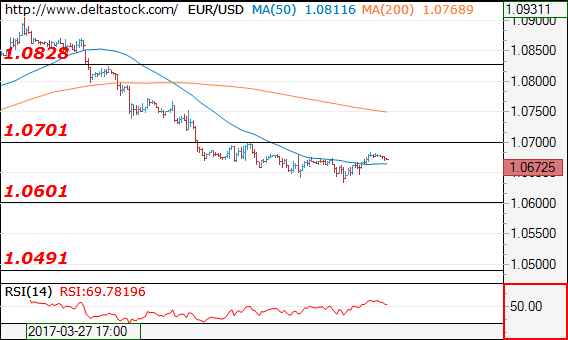

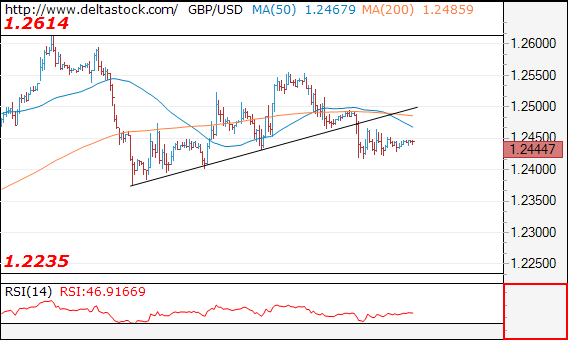

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 10672

Despite the minor rebound above 1.0635, the overall outlook remains bearish below 1.0700 resistance, for a tight test of 1.0600 support zone.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

1.0700 |

1.0904 |

1.0600 |

1.0600 |

|

1.0828 |

1.1010 |

1.0490 |

1.0490 |

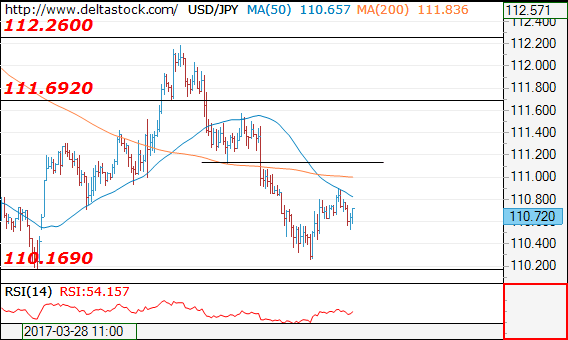

USD/JPY

Current level - 110.72

Yesterday's low at 110.26 signals a reversal of the downtrend from 112.20 and my outlook is positive, for a rise towards 111.20, en route to 112.26 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

111.20 |

113.50 |

110.16 |

109.75 |

|

112.26 |

115.65 |

108.50 |

107.80 |

GBP/USD

Current level - 1.2447

The overall outlook is still bearish after the recent break through 1.2465, for a slid towards 1.2375, en route to 1.2235 support area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

1.2465 |

1.2620 |

1.2375 |

1.2230 |

|

1.2555 |

1.2705 |

1.2235 |

1.2107 |

USDCAD Showing First Signs Of A Completed Correction, More Weakness In View

USDCAD has turned nicely down from 1.3533, clearly with five waves which is a structure of a bearish turn based on the Elliott Wave principle. As such, we will expect even more weakness since we know that impulses show direction, or change of a trend. That said, at the moment we see price making an intraday drop from around the 61.8 Fibonacci resistance zone, which could be the first sign for a completed correction. As such a breach beneath the 1.3368 level would be further evidence for more weakness to follow.

USDCAD, 1H

Currencies: USD Still Looking For A Driver. US Yields Remain Key

Sunrise Market Commentary

Rates: Will FOMC Minutes give more info on the Fed's balance sheet run-off?

FOMC Minutes could give more insight on ending the Fed's reinvestment policy, resulting in a steeper US yield curve. Last week's market reaction (bull steepening) showed that the front end of the curve is also sensitive to the debate as running off the BS is an alternative for hiking rates, according to NY Fed Dudley. We expect 2.3% yield support (US 10y) to hold.

Currencies: USD still looking for a driver. US yields remain key

The dollar still shows a mixed picture. USD/JPY came close to the recent low but no real test occurred as US yields held above key support levels. EUR/USD hovers sideways in the 1.06 big figure. Today, the focus is on the US ADP report and the services ISM. The dollar probably needs really strong data to succeed any sustained gains ahead of the payrolls

The Sunrise Headlines

- US equities managed to overcome initial weakness and eventually closed nearly unchanged in an uneventful trading session. Overnight, Asian stock markets trade mixed with China outperforming after a 2-day holiday.

- Activity in Japan's services sector expanded at the fastest pace in 19 months in March as outstanding business improved, allowing companies to charge more for their goods. The services PMI increased from 51.3 to 52.

- The cost of coal used in steel-making in China has shot up nearly 9% on expectations supply will be crimped in the wake of a cyclone that struck Australia's north-east coast last week.

- Marine Le Pen repeatedly lost her cool during a heated French presidential debate. She was rated the fourth-most-convincing candidate in two snap polls, , while communist-backed Jean-Luc Melenchon came out on top.

- Richmond Fed Lacker unexpectedly stepped down after revealing his involvement in a 2012 leak of confidential information that sparked a criminal investigation, prompted outrage on Capitol Hill and embarrassed the Fed.

- North Korea launched a medium-range ballistic missile off the east coast of the Korean Peninsula this morning, a day before US President Trump meets with Chinese President Xi for the first time.

- Today's eco calendar is interesting with services PMI/ISM's in EMU (final), the UK and the US. Additionally, the US ADP employment report and FOMC Minutes of the March meeting will be released

Currencies: USD Still Looking For A Driver. US Yields Remain Key

USD still looking for a driver. US yields remain key

On Tuesday, a cautious risk sentiment initially weighed on USD/JPY. The pair declined to the 110.30 area, but a real test of the recent low didn't occur. European yields declined while US ones rose weighing slightly on the euro. EUR/JPY touched a new correction low. However, there is no strong enough driver to give the USD clear direction. Markets await the key US eco data later this week. USD/JPY closed the session at 110.74 (from 110.90 on Monday). EUR/USD hovered around the pivot 1.0650 and closed the session at 1.0674, near the topside of the intraday range.

Overnight, Chinese markets reopen in positive territory after regional holiday's. Other regional markets show no clear trend. Japanese equities are struggling not fall in negative territory as the yen is holding strong (USD/JPY in the 110.65 area). Yesterday evening, the debate between the French presidential candidates was no success for Marine Le Pen. The euro gained slightly ground overnight, but we don't expect the theme to have a lasting impact on EUR/USD. The pair is trading in the 1.0675 area. The Aussie dollar stabilizes (AUD/USD 0.7665) after a setback yesterday. The RBA is growing ever more worried on consumer debt and stability.

Today, the EMU calendar contains only the final services PMI. In the US, March ADP employment growth is expected to return to a trend-like 185 000 following an outsized 298 000 gain. Some payback may occur. The March Nonmanufacturing ISM is expected to have eased slightly to 57 from 57.6. As the correlation with the manufacturing ISM is rather strong, we might indeed see some easing, but the level still points to a good growth. Finally, the Fed will publish the Minutes of its March meeting. We look closely to the (unfinished) discussions on future balance sheet tapering. Last week, the dollar correction slowed on decent US eco data and as Fed speakers confirmed further policy normalization in 2017. At the same time, the euro lost momentum as speculation on an early ECB policy normalization eased. However, the dollar rebound has no strong legs as US yields are holding near key support levels. Of late, we advocated that the dollar needs very strong data to regain more ground short term. This assessment remains valid and especially applies to USD/JPY. The pair struggles near the recent lows in the 110 area.

We keep a close eye on US yields nearing key support levels. For EUR/USD, the repositioning away from early ECB normalization has been worked out. We maintain a cautious EUR/USD negative bias, but the decline is slowing. Big EUR/USD gains are unlikely if sentiment would become risk-off. From a technical point of view, USD/JPY last week failed to regain the 111.36/60 previous range bottom. A decline below 110 would signal more trouble ahead. EUR/USD extensively tested the topside of the MT range, but the test was rejected last week. The 1.0874/1.0906 area now looks a solid resistance. EUR/USD might return lower in the previous 1.0875/1.05 trading range.

EUR/USD: correction slows as USD rebound fails to gain traction

EUR/GBP

Sterling corrects off the recent highs

Yesterday, sterling faced heavy selling at the onset of European trading which is a indication that the recent short squeeze has probably run its course. After the early morning repositioning sterling didn't go anywhere. Cable hovered in the mid 1.24 big figure and closed the session at 1.2440. EUR/GBP traded close to, mostly slightly north of 0.8550 for most of the session. A late session up-tick of EUR/USD pushed EUR/GBP to close the session at 0.8580 (from 0.8545 on Monday evening).

Overnight, BRC shop prices declined -0.8% M/M (from -1.0%), in line with expectations. Sterling is holding near yesterday's lows against the euro and the dollar. Later today, the UK services PMI is expected little changed at 53.4. In the past, this indicator had big market moving potential as services are the main driver for UK growth. This remains the case, but of late sterling was more sensitive to price data and, to a lesser extent, to Brexit headlines, rather than to activity data. Even so, we watch whether Brexit is having more impact on services activity. Mid-March, sterling found a better bid after higher than expected UK inflation and a more hawkish tone from the BoE. We changed our short-term bias on EUR/GBP from positive to neutral. The EUR/GBP 0.88/0.84 range should guide EUR/GBP trading medium term. Since late last week, the sterling rally/shortsqueeze shows tentative signs of running into resistance, but we see no trigger for a real change in sentiment yet. Longer term, Brexit-complications remain a potential negative for sterling. We are not convinced that the BoE will raise rates anytime soon, even not after recent higher inflation data.

EUR/GBP rebounds as sterling short-squeeze is easing

FOMC Minutes In Focus

Today, the Fed will release the minutes of the March FOMC meeting, where the Committee raised interest rates by 25bps, as was very widely expected. However, the signals we received were not particularly hawkish. Even though the Fed upgraded its forecasts for the US economy, the “dot plot” was left largely unchanged, and Chair Yellen was rather cautious in her press conference.

What we understood at the time was that this hike did not reflect heightened optimism on the economic outlook, and did not imply that future rate hikes will be faster than previously anticipated. It would be interesting to see whether the tone of the minutes is equally cautious, as something like that could push somewhat back market expectations regarding the timing of the next rate hike and thereby hurt USD a little. However, we believe that Friday's employment data will probably be a much bigger determinant of when investors will anticipate the Fed's next move and thus, of the near-term direction of the dollar.

USD/JPY traded somewhat higher yesterday, after hitting support near the 110.35 (S1) level. Nevertheless, the recovery remained limited below the 111.00 (R1) resistance. In our view, the fact that the rate fell back below the key obstacle of 111.60 (R2) on Friday shifts the short-term outlook back to cautiously negative. Therefore, we expect a cautious tone in the minutes today to encourage the bears to pull the trigger for another test near the 110.35 (S1). A dip below that line could aim for the psychological zone of 110.00 (S2), where we expect the rate to settle for a while and wait for the NFP.

Second French presidential debate has little impact on the euro

Overnight, the second French presidential debate was rather uneventful, at least in terms of market response. According to a snap poll conducted after the debate, Melenchon was the most convincing performer, followed by Macron, Fillon, and Le Pen in that order. The reaction in the euro was muted after the debate, possibly due to Le Pen's poor performance, which was in line with what happened at the first debate as well.

Moving forward, we expect EUR traders to pay an increasing amount of attention to this race as we approach Election Day. We expect new opinion polls to have a greater impact on the euro compared to previous ones, considering that polls conducted just a few days before the election may carry greater importance for investors.

Given that Le Pen has lost the first round lead in the polling battle recently, we think that fresh polls showing her behind would simply confirm that that she is unlikely to win and may thereby have little positive impact on the euro. On the other hand, polls that show Le Pen gaining back ground could cause a much larger negative reaction, as they would come as a surprise given the current consensus.

As for the rest of today's highlights:

During the European day, we get the UK services PMI for March. The forecast is for the index to have risen somewhat. Nonetheless, following the disappointing manufacturing and construction indices, we see the risks surrounding the services forecast as tilted to the downside, perhaps for an unchanged print, or even a decline. In such a case, GBP could extend its recent losses. EUR/GBP is currently trading slightly below the key resistance zone of 0.8600 (R1) following a rebound from near the long-term uptrend line taken from the lows of November 2015. A disappointing services PMI today could prove the cause for a break above that resistance zone and encourage the bulls to remain in the driver's seat. Such a break could initially open the way for the next resistance of 0.8630 (R2).

From the US, we get the US ADP employment report for March. The private sector is expected to have added 187k jobs, less than the 298k in February, though still a strong number that is likely to raise speculation for the NFP figure to meet its forecast of 185k. We also get the ISM non-manufacturing PMI for March. We don't expect a major reaction from USD on these releases though, as market participants are likely pay more attention to the Fed minutes later in the day.

USD/JPY

Support: 110.35 (S1), 110.00 (S2), 108.80 (S3)

Resistance: 111.00 (R1), 111.60 (R2), 112.20 (R3)

EUR/GBP

Support: 0.8545 (S1), 0.8500 (S2), 0.8480 (S3)

Resistance: 0.8600 (R1), 0.8630 (R2), 0.8660 (R3)