Sample Category Title

Asian Market Update: China Property Prices Edge Up Despite Curbs

China property prices edge up despite curbs

Asia Mid-Session Market Update: China property prices edge up despite curbs; G20 communique retreats on pledge to fight protectionism

Friday US markets on close: Dow +0.2%, S&P500 +0.3%, Nasdaq +0.4%

Best Sector in S&P500: Financials

Worst Sector in S&P500: Utilities

Biggest gainers: CTAS +4.7%; ADBE +3.8%; WYNN +3.8%

Biggest losers: AMGN -6.4%; IVZ -4.4%; BEN -3.9%

At the close: VIX 11.3 (+0.1pts); Treasuries: 2-yr 1.32% (flat), 10-yr 2.50% (-2bps), 30-yr 3.11% (-2bps)

Politics

(DE) President Trump tweets about meeting with Germany Chancellor Merkel, says Germany "owes vast sums of money to NATO"

(DE) German Defense Min von der Leyen: "There is no debit account in NATO" - press

(US) House Speaker Ryan: Feel confident about health bill passing the House this week after changes made provided more assistance to people in their 50s and 60's - press

(US) President Trump: Meetings on health care bill are going well; North Korea is "acting very badly" - speaking from Air Force One

Weekend US/EU Corporate Headlines

MBLY: May seek higher offers from other companies - NY Post citing analyst

SFM: Said to have held preliminary merger talks with Albertsons - press

DDC: Confirms Washington Companies discloses all-cash proposal to acquire Dominion Diamond Corporation for $13.50/shr

Key economic data:

(CN) CHINA FEB PROPERTY PRICES M/M: RISE IN 56 OUT OF 70 CITIES VS 45 PRIOR; Y/Y: RISE IN 67 OUT OF 70 CITIES V 66 PRIOR; China avg all-70 new home prices m/m: 0.3% v 0.2% prior; y/y: 11.8% v 12.2% prior

(NZ) NEW ZEALAND Q1 WESTPAC CONSUMER CONFIDENCE: 111.9 V 113.1 PRIOR

(NZ) New Zealand Feb Performance Service Index: 58.8 v 59.5 prior

(KR) SOUTH KOREA FEB PPI M/M: 0.3% V 1.4% PRIOR; Y/Y: 4.2% (5-year high) V 3.9% PRIOR

Asia Session Notable Observations, Speakers and Press

Asia equity markets are mixed after modest gain on Wall St on Friday, as investor focus turns from central bank statements last week to US policy under Pres Trump. The White House is heading for a busy week, with anticipated House health care legislation coming to the floor and the Senate starting hearings on Supreme Court nominee Gorsuch. In the mean time, there was tension at Trump's meeting with German Chancellor Merkel over the weekend as US leader claimed Germany "owes vast sums of money to NATO", to which German Defense Min replied "There is no debit account in NATO".

Economic nationalism was also on display at G20, with official Communique affirming commitment against competitive devaluation but also omitting language on promoting free trade thanks to recent threats of more protectionism from US govt. US Treasury Sec Mnuchin urged not to read into the omission, but also maintained that US is now move interested in reducing trade deficits and is prepared to re-examine certain agreements as it transitions to move "fair" trade policies. Elsewhere, US State Sec Tillerson held talks with China on his trip to Asia, discussing North Korea, Taiwan and bilateral trade. Tillerson and Trump remained scornful of North Korea's more aggressive posturing, though China called for restraint and "cool-headed" decisions.

Economic calendar was very light to start the week, with key data coming from China property sector. House prices rose m/m in 56 out of 70 cities - up from 45 last month - as markets appeared to stabilize in the wake of policy curbing excessive rise of property inflation. Across China's 70 top cities, prices rose 0.3% m/m v 0.2% prior, while y/y rise was comparable at 11.8% v 12.2% prior. China govt continues to make targeted adjustments, particularly in the first tier cities, as regulators raised the downpayment requirement for buyers of 2nd homes in Beijing from 50% to 60% on Friday.

China

(CN) Beijing raised the downpayment requirement for buyers of 2nd homes from 50% to 60% - Chinese press

(CN) China Financial News: PBoC's increase of reverse repurchase and mid-term lending facility interest rates had the effect of “targeted” measures to prevent property sector risks as developers with high debt are more sensitive to rate hikes

(CN) PBoC Gov Zhou: China's growth prospects have improved and we are focused on structural adjustment of the economy - G20 meeting

(CN) US Sec State Tillerson: US and China discussed safeguarding stability in Asia Pacific; agreed North Korea must be convinced to choose a better path

Japan

(JP) Japan PM Abe: Germany and Japan should continue as free trade champions; countries are signing "Hanover Declaration"

Australia

(AU) Goldman Sachs strategist: Expect RBA to raise rates in Nov 2017 - Australian press

Korea

(KR) South Korea Dep PM Yoo: Govt to consider ways to communicate with China about its retaliatory measures in response to THAAD deployment - Korean press

(KR) South Korea Fin Min Yoo: See the need for preemptive moves on household debt

(KR) South Korea Defense Ministry spokesperson: North Korea likely made "meaningful" progress in rocket engine test - press

Asian Equity Indices/Futures (00:00ET)

Nikkei closed, Hang Seng +0.6%, Shanghai Composite +0.1%, ASX200 -0.5%, Kospi -0.5%

Equity Futures: S&P500 -0.3%; Nasdaq -0.2%, Dax -0.2%, FTSE100 flat

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.0735-1.0765; JPY 112.45-112.75; AUD 0.7690-0.7725; NZD 0.7010-0.7040; GBP 1.2380-1.2395

Apr Gold +0.3% at 1,234/oz; Apr Crude Oil -0.8% at $48.94/brl; May Copper -0.7% at $2.67/lb

(SA) China and Saudi Arabia agree to increase cooperation in the oil sector, including Saudi oil exports to China - press

SPDR Gold Trust ETF daily holdings fall 3.0 tonnes to 834.1 tonnes; 2nd straight decline

(CN) PBOC SETS YUAN MID POINT AT 6.8998 V 6.8873 PRIOR; 2nd straight weaker setting

(CN) PBOC to inject combined CNY100B v CNY60B prior in 7,14, and 28-day reverse repos

(KR) South Korea sells 10-yr bonds at 2.215%

Asia equities/Notables/movers

Australia

Wesfarmers WES.AU -0.7%; Coles in Western Australia under investigation for asking workers to work for pizza instead of money on a Sunday - NZ press

Fletcher Building FBU.NZ -10.2%; Cuts FY17 EBIT NZ$610-650M (prior NZ$720-760M); construction division to report an EBIT loss

Hong Kong

1088.HK China Shenhua Energy Company Limited +16.0%; Reports FY16 CNY32.0B v CNY25.0B y/y; Rev CNY183.1B v CNY177.1B y/y

1184.HK S.A.S. Dragon Holdings Limited +10.3%; Guides FY16 Net +114% y/y or more

2488.HK Launch Tech Company Limited +9.0%; Reports FY16 Net profit CNY21.4M v loss CNY93.9M y/y, Rev CNY835M v CNY698M y/y

1530.HK 3SBio Inc +4.9%; Reports FY16 Net CNY714.3M v CNY526.2M y/y, Rev CNY2.80B v CNY1.67B y/y

819.HK Tianneng Power International +4.0%; Guides FY16 Net +40% y/y or more

732.HK Truly International Holdings -3.0%; Reports FY16 Net HK$581.7M v HK$845.4M y/y, Rev HK$22.1B v HK$19.4B y/y

1368.HK Xtep International Holdings Limited -9.7%; Reports FY16 Net CNY527.9M v CNY622.6M y/y; Rev CNY5.40B v CNY5.30B y/y

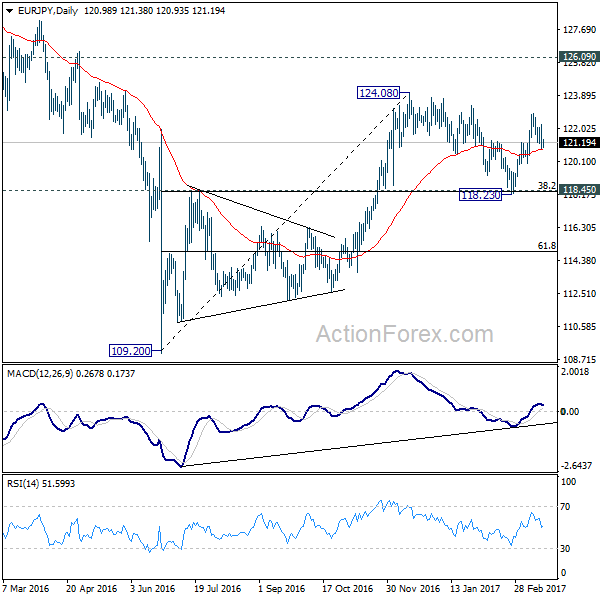

EUR/JPY Daily Outlook

Daily Pivots: (S1) 120.43; (P) 121.34; (R1) 121.87; More...

The deeper than expected fall from 122.88 dampened out immediate bullish view. And the consolidation pattern from 124.08 is possibly extending with another falling leg. Intraday bias in EUR/JPY remains mildly on the downside for 120.01 support and below. At this point, we'd expect strong support from 118.345 (38.2% retracement of 109.20 to 124.08 at 118.39) to contain downside and bring rebound. On the upside, above 122.24 minor resistance will suggest that fall from 122.88 is merely a pull back. And intraday bias will be turned back to the upside for retesting 124.08 high.

In the bigger picture, we're holding on to the view that medium term rise from 109.20 is still in progress. Focus is on 126.09 key resistance level. Sustained break will confirm completion of the whole decline from 149.76. And rise from 109.20 is of the same degree as the fall from 149.76. In such case, further rally would be seen to 104.04 resistance and possibly above before topping. Meanwhile, rejection from 126.09, or firm break of 118.45 cluster support, will likely extend the fall from 149.76 through 109.20 low.

AUD/USD: Aussie Trading On A Stronger Footing In The Morning Session

For the 24 hours to 23:00 GMT, the AUD rose 0.39% against the USD and closed at 0.7699 on Friday.

LME Copper prices declined 0.4% or $22.0/MT to $5889.0/MT. Aluminium prices rose 0.3% or $6.0/MT to $1901.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7717, with the AUD trading 0.23% higher against the USD from Friday’s close.

The pair is expected to find support at 0.7678, and a fall through could take it to the next support level of 0.7639. The pair is expected to find its first resistance at 0.7740, and a rise through could take it to the next resistance level of 0.7763.

Going ahead, investors will keep a close watch on Australia’s CB leading indicator for January, scheduled to release later today.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

EUR/USD: Euro-Zone’s Trade Surplus Shrunk In January, Construction Output Dropped Further In The Same Month

For the 24 hours to 23:00 GMT, the EUR declined 0.28% against the USD and closed at 1.0741 on Friday.

On the macro front, the Euro-zone's seasonally adjusted trade surplus narrowed more-than-expected to a level of €15.7 billion in January, compared to market expectations for the nation's trade surplus to narrow to a level of €22.0 and following a revised surplus of €23.1 billion in the prior month. Moreover, the nation's seasonally adjusted construction output fell 2.3% MoM in January. In the previous month, construction output had registered a revised drop of 0.6%.

Meanwhile, the European Central Bank (ECB) policymaker, Ewald Nowotny, stated that the ECB will decide later whether to raise interest rates before or after ending its bond purchase programme, thus hinting that an interest rate hike could be on the cards by year end.

Macroeconomic data revealed that the US flash Reuters/Michigan consumer sentiment index climbed more-than-anticipated to a level of 97.6 in March, compared to a reading of 96.3 in the previous month, while market participants anticipated for a rise to a level of 97.0. Further, the nation's leading indicator surged to its highest level in more than a decade, after it increased more-than-expected by 0.6% in February, compared to a similar rise in the previous month. Additionally, the nation's manufacturing production registered a rise of 0.5% in February, meeting market expectations and advancing for the sixth consecutive month, suggesting that recovery in the manufacturing sector was gathering speed as rising commodity prices boost demand for machinery and other equipment. In the prior month, manufacturing production had registered a revised similar rise.

Meanwhile, the nation's industrial production remained flat in February, confounding investor consensus for a rebound of 0.2%, as unseasonably warm weather again dragged down utilities. In the prior month, industrial production had registered a revised drop of 0.1%.

In the Asian session, at GMT0400, the pair is trading at 1.0759, with the EUR trading 0.17% higher against the USD from Friday's close.

The pair is expected to find support at 1.0729, and a fall through could take it to the next support level of 1.0700. The pair is expected to find its first resistance at 1.0785, and a rise through could take it to the next resistance level of 1.0812.

Moving ahead, investors will look forward to Germany's producer price index for February, slated to release in a few hours. Moreover, the US Chicago Fed national activity index for February, will also be closely watched by market participants.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

GBP/USD: UK’s Rightmove House Prices Advanced In March

For the 24 hours to 23:00 GMT, the GBP rose 0.28% against the USD and closed at 1.2388 on Friday.

In the Asian session, at GMT0400, the pair is trading at 1.2384, with the GBP trading marginally lower against the USD from Friday's close.

Overnight data indicated that UK's Rightmove house price index rose 1.3% on a monthly basis in March, following a gain of 2.0% in the previous month.

The pair is expected to find support at 1.2335, and a fall through could take it to the next support level of 1.2287. The pair is expected to find its first resistance at 1.2418, and a rise through could take it to the next resistance level of 1.2453.

With no economic releases in Britain today, traders await UK's inflation figures for February, slated to release tomorrow.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

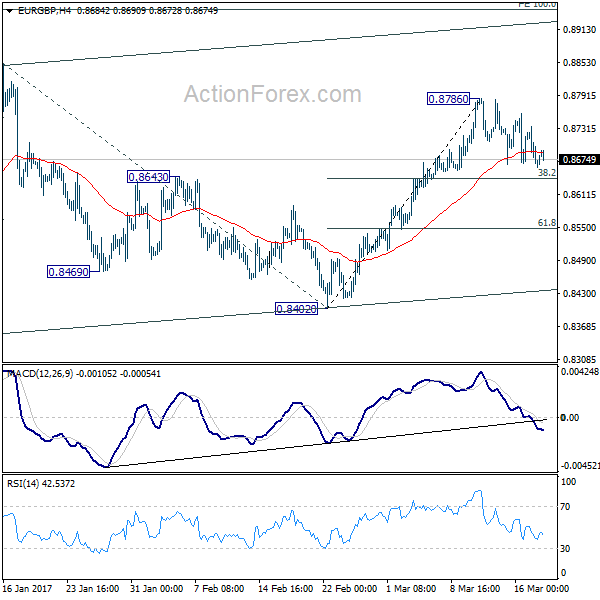

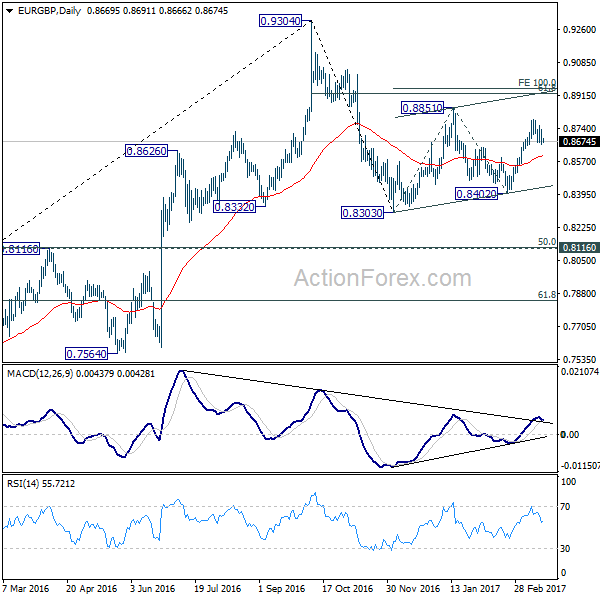

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8635; (P) 0.8686; (R1) 0.8712; More...

Intraday bias in EUR/GBP remains neutral as consolidation from 0.8786 continues. Deeper fall might be seen but we'd expect support from 38.2% retracement of 0.8402 to 0.8786 at 0.8639 to contain downside. Break of 0.8786 will target 0.8851 resistance and above. Price actions from 0.8303 are seen as the second leg of the corrective pattern from 0.9304. Hence, we'd expect strong resistance from 100% projection of 0.8303 to 0.8851 from 0.8402 at 0.8950 to limit upside. On the downside, sustained trading below 0.8693 will bring deeper fall to 61.8% retracement 0.8549 and below.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. Deeper fall cannot be ruled out yet. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Overall, the corrective pattern would take some time to complete before long term up trend resumes at a later stage. Break of 0.9304 will pave the way to 0.9799 (2008 high).

USD/JPY: Japanese Yen Trading Higher In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.59% against the JPY and closed at 112.65 on Friday.

In the Asian session, at GMT0400, the pair is trading at 112.53, with the USD trading 0.11% lower against the JPY from Friday’s close.

The pair is expected to find support at 112.17, and a fall through could take it to the next support level of 111.80. The pair is expected to find its first resistance at 113.18, and a rise through could take it to the next resistance level of 113.82.

On account of a holiday observed in Japan today, trading trend in the JPY is expected to be determined by global macroeconomic factors.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

USD/CHF: Swiss Franc Reverses Its Losses In The Asian Session

For the 24 hours to 23:00 GMT, the USD rose 0.21% against the CHF and closed at 0.9978 on Friday.

In the Asian session, at GMT0400, the pair is trading at 0.9960, with the USD trading 0.18% lower against the CHF from Friday’s close.

The pair is expected to find support at 0.9936, and a fall through could take it to the next support level of 0.9913. The pair is expected to find its first resistance at 0.9985, and a rise through could take it to the next resistance level of 1.0011.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

USD/CAD: Loonie Trading Higher In The Asian Session

For the 24 hours to 23:00 GMT, the USD rose 0.11% against the CAD and closed at 1.3336 on Friday.

In economic news, Canada’s manufacturing shipments unexpectedly climbed 0.6% MoM in January, compared to a revised rise of 2.1% in the previous month. Markets were anticipating manufacturing shipments to drop 0.3%.

In the Asian session, at GMT0400, the pair is trading at 1.3323, with the USD trading 0.1% lower against the CAD from Friday’s close.

The pair is expected to find support at 1.3291, and a fall through could take it to the next support level of 1.3259. The pair is expected to find its first resistance at 1.3366, and a rise through could take it to the next resistance level of 1.3409.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

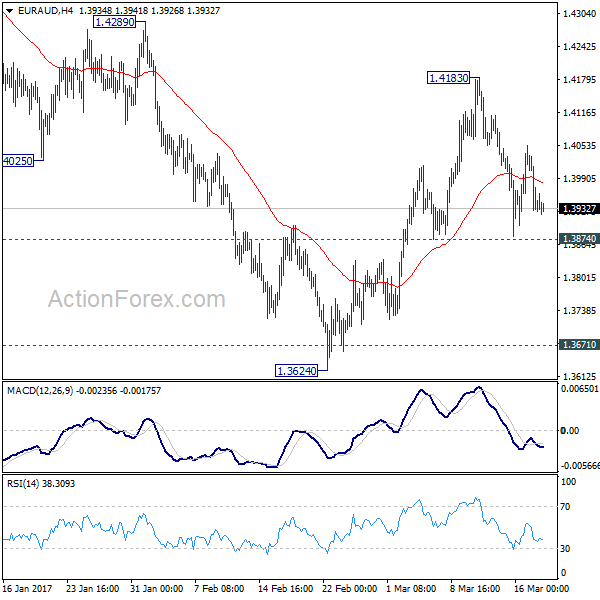

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.3883; (P) 1.3968; (R1) 1.4012; More...

Intraday bias in EUR/AUD remains neutral at this point. Outlook is unchanged and we're still slightly favoring the case of trend reversal after defending key support level at 1.3671, on bullish convergence condition in daily MACD. On the upside, above 1.4183 will turn bias to the upside for 1.4289 resistance next. Break will affirm our view and target next key resistance level at 1.4721. However, break of 1.3874 minor support will invalidate our view and turn bias back to the downside for retesting 1.3624 low.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. We'd expect strong support from 1.3671 key level to contain downside and bring rebound. Up trend from 1.1602 should not be finished and will resume later. Break of 1.4721 resistance will indicate completion of such correction and turn outlook bullish for retesting 1.6587 high. However, sustained break of 1.3671 will invalidate our bullish view and would turn focus back to 1.1602 long term bottom.