Sample Category Title

(BOE) Bank Rate Held at 0.25%, Government Bond Purchases at £435bn and Corporate Bond Purchases at up to £10bn

The Bank of England's Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 15 March 2017, the Committee voted by a majority of 8-1 to maintain Bank Rate at 0.25%. The Committee voted unanimously to continue with the programme of sterling non-financial investment-grade corporate bond purchases, financed by the issuance of central bank reserves, totalling up to £10 billion. The Committee also voted unanimously to maintain the stock of UK government bond purchases, financed by the issuance of central bank reserves, at £435 billion.

As the MPC had observed at the time of the UK's referendum on EU membership, the appropriate path for monetary policy depends on the evolution of demand, potential supply, the exchange rate, and therefore inflation. The Committee expects a slowdown in aggregate demand over the course of this year, as household demand growth declines in reaction to lower real income growth. Official estimates of retail sales have weakened notably, consistent with this expectation, although other indicators of consumer demand such as consumer confidence have been steadier. Measures of overall activity growth have been resilient, with official estimates indicating a fairly steady pace of expansion around historical average rates and business surveys suggesting little change in the near term. It is possible that slowing consumption may be offset to some degree by other components of demand, such as a more supportive net trade position following last year's fall in sterling and the recent pickup in global momentum.

Consistent with prospects for stronger global growth, equity prices have generally risen internationally, and short and long-term interest rates have increased in some economies. The evolution of asset prices has been different in the United Kingdom, however, where market interest rates have fallen and the equity prices of companies with significant domestic exposure – most notably to consumers – have underperformed. Those developments seem somewhat difficult to reconcile with the ongoing resilience of most macroeconomic indicators. In addition, for some time, financial markets and households appear to have had different perspectives on UK economic prospects. This difference cannot persist indefinitely, and the nature and timing of its resolution are likely to be key factors in the MPC's policy assessment.

CPI inflation increased to 1.8% in January, and the MPC expects it to rise above the 2% target over the next few months, before peaking at around 2¾% in early 2018 and drifting gradually back down towards the target thereafter. The projected overshoot entirely reflects the expected effects of the drop in sterling. Pay growth has remained subdued, while measures of inflation expectations remain at levels broadly consistent with the achievement of the inflation target.

Monetary policy cannot prevent either the real adjustment that is necessary as the UK moves towards its new international trading arrangements or the weaker real income growth that is likely to accompany it over the next few years. Attempting to offset fully the effect of weaker sterling on inflation would be achievable only at the cost of higher unemployment and, in all likelihood, even weaker income growth. For this reason, the MPC's remit specifies that, in such exceptional circumstances, the Committee must balance the trade-off between the speed with which it intends to return inflation to the target and the support that monetary policy provides to jobs and activity. At its March meeting, the MPC continued to judge that it remained appropriate to seek to return inflation to the target over a somewhat longer period than usual. Eight members thought that the current stance of monetary policy remained appropriate to balance the demands of the Committee's remit. Kristin Forbes considered it appropriate to increase Bank Rate by 25 basis points.

As the Committee has previously noted, there are limits to the extent that above-target inflation can be tolerated. The continuing suitability of the current policy stance depends on the trade-off between above-target inflation and slack in the economy. The projections described in the February Inflation Report depend in good part on three main judgements: that the lower level of sterling continues to boost consumer prices broadly as expected, and without adverse consequences for expectations of inflation further ahead; that regular pay growth does indeed remain modest, consistent with the Committee's updated assessment of the remaining degree of slack in the labour market; and that the hitherto resilient rates of household spending growth slow as real income gains weaken, without a sufficient offset by other components of demand.

In judging the appropriate policy stance, the Committee will be monitoring closely the incoming evidence regarding these and other factors. At present, the Committee's best collective view is that the central judgements underpinning the February projections remain broadly on track, and so the conditioning assumption underpinning the February projections – that there will be some modest withdrawal of monetary stimulus over the course of the forecast period – remains appropriate. There are risks in both directions. For example, if aggregate demand growth remains resilient, monetary policy may need to be tightened sooner and to a greater degree than that implied path. A more marked slowdown in activity than currently anticipated by the Committee, by contrast, could warrant additional policy support relative to that implied path. Monetary policy can respond, in either direction, to changes to the economic outlook as they unfold to ensure a sustainable return of inflation to the 2% target.

Dollar Sees Red, But the Bleeding is Slowing

Thursday March 16: Five things the markets are talking about

As expected, the Fed raised rates by +25bps, but the outlook of the accompanying statement and Fed Chair Yellen's press conference was very much less 'hawkish' than anticipated.

Absent from the statement was any language indicating an acceleration of interest rate hikes. Market forecast for this year remains at +1.375%, which implies only two more rate hikes in 2017, reversing hints of markets anticipating a potential fourth hike.

Note: The 2018 median forecast was also left unchanged with three more hikes, as the Fed judged near-term outlook as "roughly balanced" and market-based inflation compensation remaining low.

The committee stated inflation was close to their +2% target, but that it was "symmetrical," meaning there may be a willingness to let prices run higher slightly faster.

In reality, the Fed's outlook has not changed much since December; it's the market that needs to adjust to the Fed's rate hike expectations, by again selling the dollar, buying treasuries and stocks.

Investors will now turn their attention to President Trump's fiscal 2018 budget request to congress today - he is proposing deep cuts to most federal agencies to boost defense and security spending.

1. Global equities given the green light

The Fed's move to raise interest rates without accelerating the timeline for future tightening has sent global stocks higher.

In Japan, stocks eked out small gains in choppy trade. The Nikkei rose +0.1%, after trading mostly in negative territory on the back of a stronger yen (¥113.43). Investors ignored the BoJ's no rate policy change (see below).

In Hong Kong, the Hang Seng Index closed at a 19-month high on the Fed 'slow but steady' rate view. Trading up +2.1%, its highest close since Aug. 2015.

In China, the Shanghai Composite Index closed up +0.8%, a three-month high, thanks to sharp gains led by brokerage, manufacturing and banking stocks. Investors seized on the Fed's perceived good news, and chose to ignore the People's Bank of China (PBoC) increase in money-market rates (see below).

In Europe, equity indices are trading sharply higher. Investors are waiting for the BoE monetary policy decision and post-decision comments scheduled in a couple of hours. Banking stocks leading the gains on the Eurostoxx, while energy, commodity and mining stocks are trading notably higher in the FTSE 100.

U.S stocks are set to open in the black (+0.2%).

Indices: Stoxx50 +1.1% at 3,447, FTSE +1.0% at 7,439, DAX +1.0% at 12,134, CAC-40 +0.8% at 5,025, IBEX-35 +1.6% at 10,142, FTSE MIB +1.6% at 20,085, SMI -0.3% at 8,666, S&P 500 Futures +0.2%

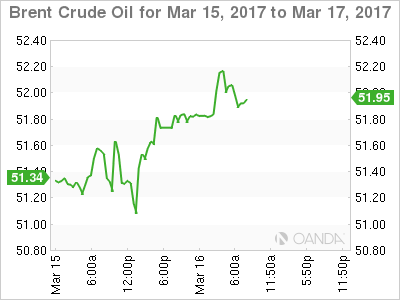

2. Oil prices extend gains after drop in U.S. stockpiles

Crude oil prices have extended its gains overnight after data yesterday showed U.S. stockpiles had eased from their record highs.

Brent futures have climbed +47c, or +0.9% to +$52.28 - They had their first increase in seven days yesterday, gaining +1.7%. West Texas Intermediate (WTI) crude is up +39c, or +0.8%, at +$49.25 a barrel. On Wednesday, it rallied +2.4%, its first increase in eight-days.

Data from the EIA yesterday showed U.S stocks falling last week, the first weekly decline after nine straight increases. Crude inventories fell -237k barrels in the week to March 10 - the market was expecting another increase of +3.7m barrels.

Crude bulls are taking solace in the IEA's statement that 'demand should overtake supply in H1 this year' and in OPEC's level of compliance with the cuts.

Note: There are early signs that OPEC's March compliance data will be stronger than the previous two-months.

Ahead of the U.S open, gold (+0.6% to +$1,226.21 per ounce) has hit a one-week high after the Fed signaled a cautious stance on interest rate policy this year, pushing the dollar to its lowest level in a month.

3. Central Banks being kept busy

Overnight, the People's Bank of China (PBoC) also eased off the monetary accommodation in the wake of the Fed's decision, raising rates it charges in open-market operations and on its medium-term lending facility. It's not a shift in policy, but rather reflect changes in markets, firmer domestic economy, and strong credit expansion. The PBoC also strengthened the Yuan in its daily fix by the biggest margin in two-months.

In Japan, the Bank of Japan (BoJ) maintained its policy stance with more upbeat view of longer-run inflation. Officials, as expected, left interest rates (IOER) unchanged at -0.10% and has maintained its 10-yr JGB yield target around +0%. The BoJ has also kept its JGB buying target at about +¥80T per year, while maintaining its overall assessment of their economy to continue its moderate recovery trend.

Earlier this morning, there were no surprises from the Swiss National Bank (SNB) who left their deposit rate at -0.75% and repeated its long-held view that the CHF ($0.9994) is "significantly overvalued."

The Bank of England (BoE) is up next (08:00aam EST) and no changes are expected to monetary policy.

The yield on U.S 10's has backed up +3bps to +2.52% after tumbling -11bps yesterday. Similarly, Aussie yields have fallen -10bps to +2.82% and Kiwi -10bps to +3.26%.

4. Dollar sees red, but the bleeding is slowing

The mighty USD is weaker across the board, particularly against JPY as it fell as much as -140 pips to below the psychological ¥113 handle (¥112.90). Investors remain somewhat cautious ahead of this weekends G20 meeting. What will U.S say about China's yuan policy? Ahead of the U.S session its trading atop of ¥113.40.

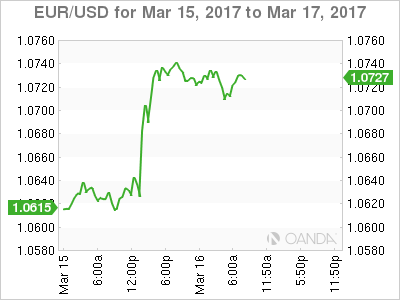

The EUR has rallied to above €1.0720, helped by a weaker showing for the Eurosceptic party in the Dutch elections (see below).

Sterling (£1.2269) will take its cues from the Bank of England (BoE) later this morning.

5. Dutch populist vote easily beaten

The Dutch political establishment held on to power, despite losing votes to anti-immigrant nationalists. Prime Minister Rutte's center-right People's Party for Freedom and Democracy gained the most votes, putting him in a strong position to form a new ruling coalition.

The VVD has won 33 seats, eight fewer than in 2012, while the far-right populist Party for Freedom of Wilders is second with 20 seats, five more than the last time but still a stinging setback for Euro populist vote. They will now start a long process of coalition talks.

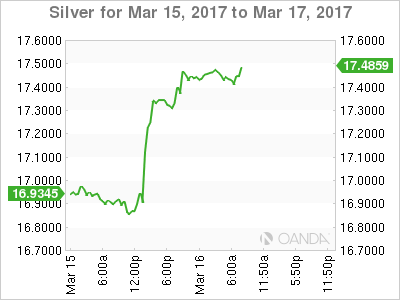

GOLD Surging, SILVER Strong Increase, Crude Oil Short-Squeeze.

GOLD (in USD) Surging.

Gold's weakness has paused as the precious metal surged yesterday out of the Fed rate hike. Strong support is given at 1177 (11/01/2017 low). The short-term momentum seems strong and it would not be abnormal to see an increase again towards resistance at 1263 (27/02/2017 high).

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

SILVER (in USD) Strong increase.

Silver's selling pressures have stopped below 17.00. Strong support is given at 16.63 (27/01/2016 low). Hourly resistance is now given at 17.52 (intraday high). Expected to further consolidate,

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

Crude Oil (in USD) Short-squeeze.

Crude oil's bearish pressures continues despite ongoing consolidation due to some shortsqueeze. The commodity had been unable to mount a serious challenge to 55.24 (03/01/2017 high) resistance. Strong support given at 49.61 (08/12/2016) has been broken. Expected to see deeper selling pressures.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 24.82 (13/11/2002) while resistance can now be found at 55.24 (03/01/2017 high).

FTSE Hits Fresh Record Highs On Post-Fed Bullish Acceleration

FTSE hit a series of fresh record highs after 7382/7254 correction was fully retraced and strong bullish acceleration commenced above previous high at 7382.

The rally was inspired by surge in commodity stocks on Fed’s rate hike.

Strong bullish setup of technical studies is complementing positive environment after Fed that would result in further upside action.

The price is eyeing its Fibo 161.8% projection at 7461 as next target, after previous one at 7431 (Fibo 138.2%) was taken out.

Rally could extend towards psychological 7500 barrier and 7511 (Fibo 200% projection of the upleg from 7254 trough).

Former top at 7382 now acts as good support, followed by rising 10SMA at 7352.

Res: 7440, 7461, 7500, 7511

Sup: 7400, 7389, 7382, 7352

Dovish Fed Sends USD Lower, SNB On Hold

News and Events:

The Fed’s three-hike pipe dream

As widely expected, the Federal Reserve increased borrowing rates by 25bps to 0.75%-1%. This is the second interest rate lift in four months and nobody got it wrong. So, no surprise here, however the greenback plunged sharply during Yellen's press conference with rates collapsing along the yield curve. Monetary sensitive 2-year treasury yields as well as the 10-year slid 9bps to 1.30% and 2.48% respectively. In the FX market, the single currency hit 1.0746 against the dollar as investors unwound their long USD positions. Interestingly, the disappointing defeat of Geert Wilders’ Freedom Party provided an additional boost.

So what exactly happened? Just as we wrote yesterday, the market mis-priced the tightening path beyond the March rate hike and when Janet Yellen adopted a dovish tone and wording during the press conference, investors quickly caught on that the three rate hikes promised for 2017 were in fact a pipe dream. Yes, the US economy is still in recovery in that growth is positive, however dark clouds have begun to gather on the horizon. One of the most disconcerting of all - as also mentioned in our report yesterday - is the negative trend in real wage growth. In February, data showed that real wages contracted 0.5% compared to a year ago. This is a major issue as consumer spending accounts for roughly 70% of the US GDP. Moreover, less disposable money for consumers means less price pressure, which translates into falling consumer prices, which ultimately means that the Fed will have to increase rates slowly if not taking a break during the process altogether.

The greenback is staring down the barrel of some complicated times ahead as investors slowly switch to risk-on mode and move towards higher yielding assets. In the short-term, EUR/USD will continue to suffer from the political uncertainty stemming from the French election. CHF and JPY have room for further appreciation against the USD.

SNB maintains course

Unsurprisingly, the Swiss central bank has decided to steer straight ahead, holding interest rates unchanged at -0.75%. Even though defending the franc is a clear SNB priority, rates will not be pushed much lower out of fear of boosting capital outflows. Recent strong intervention from the Swiss central bank pushed the EURCHF towards 1.0800 before bouncing lower.

These periods of uncertainty of having more margins to defend the Swiss franc seem to define the SNB’s strategy as the currency is still largely seen as overvalued.

In terms of data, retail sales saw a drop in January at -1.4% y/y, while Switzerland’s Q4 2016 printed below expectations at 0.6%.

The SNB’s wait-and-see approach is clearly set to continue as Europe remains on tenterhooks despite Geert Wilder’s Populist Party defeat. In the short-term, it is likely that we will see further euro weakness against the CHF.

Today's Key Issues (time in GMT):

- 4Q Labour Costs YoY, last -0,50% EUR / 08:00

- mars.16 SNB Sight Deposit Interest Rate, exp -0,75%, last -0,75% CHF / 08:30

- mars.16 SNB 3-Month Libor Lower Target Range, exp -1,25%, last -1,25% CHF / 08:30

- mars.16 SNB 3-Month Libor Upper Target Range, exp -0,25%, last -0,25% CHF / 08:30

- Feb Unemployment Rate, exp 7,30%, last 7,30% SEK / 08:30

- Feb Unemployment Rate Trend, last 6,90% SEK / 08:30

- Feb Unemployment Rate SA, exp 6,80%, last 6,80% SEK / 08:30

- mars.16 Deposit Rates, exp 0,50%, last 0,50% NOK / 09:00

- Feb CPI MoM, exp 0,40% EUR / 10:00

- Feb F CPI YoY, exp 2,00%, last 2,00% EUR / 10:00

- Bank of Italy's Visco Speaks in Milan on EU Treaties EUR / 10:00

- Feb F CPI Core YoY, exp 0,90%, last 0,90% EUR / 10:00

- mars.15 FGV CPI IPC-S, exp 0,34%, last 0,34% BRL / 11:00

- mars.16 Benchmark Repurchase Rate, exp 8,00%, last 8,00% TRY / 11:00

- mars.16 Overnight Lending Rate, exp 9,25%, last 9,25% TRY / 11:00

- mars.16 Overnight Borrowing Rate, exp 7,25%, last 7,25% TRY / 11:00

- mars.16 Late Liquidity Lending Rate, exp 11,75%, last 11,00% TRY / 11:00

- mars.10 Foreigners Net Bond Invest, last -$99m TRY / 11:30

- mars.10 Foreigners Net Stock Invest, last $134m TRY / 11:30

- mars.16 Bank of England Bank Rate, exp 0,25%, last 0,25% GBP / 12:00

- Mar BOE Asset Purchase Target, exp 435b, last 435b GBP / 12:00

- Mar BOE Corporate Bond Target, exp 10b, last 10b GBP / 12:00

- Jan Int'l Securities Transactions, last 10.23b CAD / 12:30

- Feb Housing Starts, exp 1264k, last 1246k USD / 12:30

- Feb Housing Starts MoM, exp 1,40%, last -2,60% USD / 12:30

- Feb Building Permits, exp 1268k, last 1285k, rev 1293k USD / 12:30

- Feb Building Permits MoM, exp -1,90%, last 4,60%, rev 5,30% USD / 12:30

- mars.11 Initial Jobless Claims, exp 240k, last 243k USD / 12:30

- mars.04 Continuing Claims, exp 2050k, last 2058k USD / 12:30

- Mar Philadelphia Fed Business Outlook, exp 30, last 43,3 USD / 12:30

- mars.10 Gold and Forex Reserve, last 393.4b RUB / 13:00

- mars.12 Bloomberg Consumer Comfort, last 50,6 USD / 13:45

- Mar Bloomberg Economic Expectations, last 50 USD / 13:45

- Jan JOLTS Job Openings, exp 5562, last 5501 USD / 14:00

- Revisions: Job Openings and Labor Turnovers USD / 14:00

- ECB's Praet speaks in Brussels EUR / 18:00

- Feb BusinessNZ Manufacturing PMI, last 51,6 NZD / 21:30

- 4Q BoP Current Account Balance, exp -$12.00b, last -$3.40b INR / 22:00

- Feb Foreign Direct Investment YoY CNY, exp -4,20%, last -9,20% CNY / 23:00

- Feb Industrial Production YoY, exp 1,30%, last 2,30% RUB / 23:00

- Feb Tax Collections, exp 93244m, last 137392m BRL / 23:00

The Risk Today:

EUR/USD is strengthening. The pair is lying in an uptrend channel. Key resistance is still given at a distance 1.0874 (08/12/2017 high). Strong support can be found at 1.0493 (22/02/2017 low). The technical structure suggests deeper increase towards resistance at 1.0874. In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD is moving up but the pair remains around support given at 1.2254 (19/01/2017 low). The road is still wide-open for further decline. Hourly resistance is given at 1.2300 (05/03/2017 high). The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY has failed to break key resistance given at 115.62 (19/01/2016 high). Hourly support given at 113.56 (06/03/2017 low) has been broken. Expected to push lower. We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

USD/CHF has exited uptrend channel. Hourly support given at 1.0075 (13/03/2017 low) has been broken. Key resistance can be found at a distance at 1.0344 (15/12/2016 high). Expected to consolidate. In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

| EURUSD | GBPUSD | USDCHF | USDJPY |

| 1.1300 | 1.3445 | 1.1731 | 121.69 |

| 1.0954 | 1.3121 | 1.0652 | 118.66 |

| 1.0874 | 1.2771 | 1.0344 | 115.62 |

| 1.0721 | 1.2267 | 0.9985 | 113.44 |

| 1.0454 | 1.1986 | 0.9967 | 111.36 |

| 1.0341 | 1.1841 | 0.9862 | 106.04 |

| 1.0000 | 1.0520 | 0.9550 | 101.20 |

EUR/CHF Moving Sideways Between 1.0700 And 1.0750, EUR/JPY Bearish Pressures Increase, EUR/GBP Moving Sideways.

EUR/CHF Moving sideways between 1.0700 and 1.0750.

EUR/CHF's renewed bearish pressures continues to increase. The medium-term pattern suggests us to see continued bearish pressures towards key support that can be found at 1.0623 (24/06/2016 low). Temporary surges seem the new normal for the CHF.

In the longer term, the technical structure is mixed. Resistance can be found at 1.1200 (04/02/2015 high). Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

EUR/JPY Bearish pressures increase.

EUR/JPY's demand has ended. Hourly support lies at 121.13 (intraday low). Strong resistance is given at a distance at 123.31 (27/01/2017 high). Expected to show further decrease.

In the longer term, the technical structure validates a medium-term succession of lower highs and lower lows. As a result, the resistance at 149.78 (08/12/2014 high) has likely marked the end of the rise that started in July 2012. Strong support at 94.12 (24/07/2012 low) looks nonetheless far away.

EUR/GBP Moving sideways.

EUR/GBP is trading mixed. Selling pressures increase around 0.8800. Key resistance is given at 0.8854 (15/01/2017 high). Yet, the road is wide-open for further weakness as there is no close support.

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.

USD/CHF Bearish Breakout, USD/CAD Bullish Pressures Have Faded, AUD/USD Strong Short-Term Bullish Pressures.

USD/CHF Bearish breakout.

USD/CHF has exited uptrend channel. Hourly support given at 1.0075 (13/03/2017 low) has been broken. Key resistance can be found at a distance at 1.0344 (15/12/2016 high). Expected to consolidate.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/CAD Bullish pressures have faded.

USD/CAD's bullish pressures have ended abruptly. The road seems now wide-open for larger decline. Key resistance is given at 1.2969 (31/01/2017 low).

In the longer term, there is a golden cross with the 50 dma crossing the 200 dma indicating further upside pressures. Strong resistance is given at 1.4690 (22/01/2016 high). Long-term support can be found at 1.2461 (16/03/2015 low).

AUD/USD Strong short-term bullish pressures.

AUD/USD's technical structure has changed. Support is given at 0.7494 (19/01/2017 low). Expected to target key resistance can be found at 0.7778 (08/11/2016 high).

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.

EUR/USD Surging, GBP/USD Trading Higher Within Downtrend Channel, USD/JPY Selling Pressures Surged.

EUR/USD Surging.

EUR/USD is strengthening. The pair is lying in an uptrend channel. Key resistance is still given at a distance 1.0874 (08/12/2017 high). Strong support can be found at 1.0493 (22/02/2017 low). The technical structure suggests deeper increase towards resistance at 1.0874.

In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD Trading higher within downtrend channel.

GBP/USD is moving up but the pair remains around support given at 1.2254 (19/01/2017 low). The road is still wide-open for further decline. Hourly resistance is given at 1.2300 (05/03/2017 high).

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY Selling pressures surged.

USD/JPY has failed to break key resistance given at 115.62 (19/01/2016 high). Hourly support given at 113.56 (06/03/2017 low) has been broken. Expected to push lower.

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

Dutch Election: First Defeat For Populists In Europe

The People's Party for Freedom and Democracy (VVD), the liberal, centre-right party led by incumbent Prime Minister Mark Rutte, has emerged as the biggest party, fighting back the predicted challenge of Geert Wilders' far-right PVV party. Rutte is likely to have benefited from the high voter turnout (81%) and his tough stance in the diplomatic row with Turkey over the past week. EUR/USD moved up one figure to 1.073 on the publication of the exit poll, which shows that VVD remains the largest party.

Wilders, despite a projected second place with around 20 seats, is not likely to be part of any coalition negotiations, with all major parties unwilling to work with his populist, anti-immigration MPs. The PVV is likely to spend another four to five years in the opposition.

The unexpected victor of the night was GreenLeft, led by 30-year-old Jesse Klaver, which increased its four seats to a projected 14. It could now play a crucial part in the upcoming coalition talks.

Rutte's party is likely to get 33 seats (a loss of eight versus 2012) and will need to enter into coalition talks to form a new government, although Rutte is likely to stay on as Prime Minister. The collapse of Rutte's former coalition partner, the social democratic PvdA, tumbling from 38 seats to a projected nine, means the PM will need to seek new agreements. The Christian Democrats CDA (centre-right) and Democrats 66 (centre), each with an expected 19 MPs, are the most obvious candidates to join a VVD coalition. However, that still leaves him five seats short of the 76 needed for a majority, which is why a fourth coalition partner will be needed. The Christian Union CU (centre-right) or the GreenLeft could also be candidates.

Talks are likely to last for some time – possibly months. The final official election results will be published on 21 March by the Dutch Election Commission.

The new parliament will meet for the first time on 23 March, when official coalition talks will begin. However, informal coalition talks are likely to start today.

Depending on the composition of the new governing coalition, we might see more fiscal easing in the Netherlands going forward, as most parties want to increase borrowing and lower taxes to boost jobs and growth. However, the economy is in good shape generally and there is fiscal room for growth-enhancing reforms.

The first defeat for populists in Europe might also have important repercussions for the upcoming French presidential election on 23 April and we could see Le Pen losing momentum in the polls and markets starting to reprice risk. For the short-term market implications of a Le Pen win see also Le Pen – What If? Implications for Euro and Nordic markets, 13 February 2017.

Spot Gold – Recovery Could Extend To $1237, Thickening Daily Cloud Underpins

Spot Gold peaked at $1229 on Thursday, on extension of post-Fed strong rally formed base at $1195 zone and signaled that correction from $1263 to $1195 might be over. Strong dollar's negative sentiment that came after Fed, boosted yellow metal and turned near-term bias higher. Bullish extension met initial target at $1129 (daily Kijun-sen / 50% retracement of $1263/$1195) and could extend towards next barrier at $1337 (Fibo 61.8%) after consolidation. Sustained break above $1237 is needed to confirm reversal. Broken daily Tenkan-sen offers solid support at $1215, followed by thickening daily cloud that contained correction from $1263 and is now underpinning recovery. Cloud top lies at $1210 and is expected to contain extended downticks to keep fresh near-term bulls in play.

Res: 1229, 1237, 1244, 1247

Sup: 1221, 1215, 1210, 1208