Sample Category Title

West Texas Crude Edges Lower on Mixed US Data

West Texas crude has edged lower in the Thursday session, as WTI/USD stays close to the $49 level. In North American trade, WTI crude futures are trading at $48.69. Brent Crude is trading at $51.81, as the Brent premium stands at $3.11. On the release front, Building Permits fell to 1.21 million, missing the estimate of 1.26 million. The Philly Fed Manufacturing Index dropped sharply to 32.8, above the forecast of 30.2 points. On the labor front, unemployment claims ticked down to 241 thousand, beating the forecast of 245 thousand. On Friday, the US will publish the UoM Consumer Sentiment report.

WTI crude remains under pressure and continues to trade below the $50 level. WTI plunged 8.7 percent last week and dipped below the $47 level on Tuesday. This was in response to reports that Saudi Arabia has increased oil production above 10 million barrels a day, raising concerns about a global oil glut. Meanwhile, US Crude Oil Inventories finally reversed directions, posting a drawdown of 0.2 million barrels, compared to an estimate of 3.3 million. This decline comes after the indicator posted 11 surpluses in the past 12 weeks, reflective of increasing US shale production. The string of surpluses has dampened OPEC's hopes of raising prices, as the cartel cut production levels at the beginning of January. OPEC's cuts had raised expectations that crude would rise above $60 a barrel, but oil prices continue to lose ground in 2017.

There were no raised eyebrows when the Federal Reserve raised rates by a quarter-point on Wednesday, as the markets had priced a rate hike at over 90%. The rate hike, the second in just three months, raised the raised the benchmark lending rate to a 0.75%-1% range. What was not expected, however, was the sharp drop of the dollar against its major rivals. The markets were hoping that a red-hot US economy would propel the Fed to accelerate its pace of monetary tightening. There was disappointment as Fed Chair Janet Yellen reiterated that further rate hikes would be done gradually, pushing the dollar on Wednesday. As well, the US dollar may have lost ground due to traders and investors acting on "buy on rumor, sell on fact". This larges-scale selling of US dollars after the Fed hike has sent the US dollar broadly lower, with the pound gaining 1.7 percent since the Fed announcement.

Sterling Supported by Somewhat Hawkish BoE Minutes

Headlines

European equity markets gain moderate ground today, but are off intra-day highs in the wake of yesterday's WS gains. US equities open slightly higher.

The BoE held its benchmark rate steady, with one dissenter in favour of higher rates, but signalled that an increase may not be far off: "Some members noted that it would take relatively little further upside news on the prospects for activity or inflation for them to consider that a more immediate reduction in policy support might be warranted".

US eco data printed close to consensus. The Philly Fed Business Outlook declined less than expected from a historically high 43.3 in February to 32.8 in March. Weekly jobless claims stabilised at 241k. Housing data were mixed with higher housing starts than forecast, but weaker building permits, a reversal from last month.

Norway's central bank kept its key interest rate on hold as expected, and said it expects to keep the deposit rate at 0.5% for longer than previously forecast, even while recognising that "persistently low interest rates may lead to financial system vulnerabilities". EUR/NOK rose from 9.10 to 9.15.

The Swiss National Bank highlighted continued global political uncertainty as it stuck to its ultra-loose monetary policy designed to stem demand for the safe-haven Swiss franc. The central bank is braced for the outcome of European elections this year which could trigger an upsurge in demand for the franc should nationalists perform well.

The Trump administration unveiled a "hard-power budget" plan that slashes spending at the Environmental Protection Agency by 30% and at the state department by 29%. Those cuts would help fund a huge increase for the Pentagon and the department of homeland security, which would see their budgets rise by 9% and 7% respectively.

The protectionist stance of the new US administration could complicate G20 talks this week and force policymakers to leave out the disputed trade issue, German FM Schaeuble told Reuters in an interview.

British PM May told the Scottish government "now is not the time" for a second independence referendum, saying it would be unfair for people to vote without knowing the conclusion of Brexit talks. Scottish First Minister Sturgeon has called for a referendum before the end of the two years of talks set out under Article 50.

Rates

FOMC gains partly erased; Dutch election relief

Global core bonds lost ground today with Bunds underperforming US Treasuries. Markets were relieved that Dutch candidate Wilders failed to win the Dutch elections, while they also lost some of yesterday exaggerated (?) post-FOMC gains. At the time of writing, the German yield curve trades 3.5 bps (2-yr) to 5 bps (30-yr) higher. The US yield curve bear steepens with yields 2.7 bps (2-yr) to 4 bps (30-yr) higher. On intra-EMU bond markets, 10-yr yield spread changes versus Germany are nearly unchanged with Portugal underperforming (+25 bps), perhaps in the run-up to tomorrow's rating decision by S&P (BB+, stable outlook).

Intraday, European equity markets started on a bright note. The relief rally after Rutte's Dutch election victory weighted on the Bund. US Treasuries partly returned some of the post-FOMC gains. After all, the FOMC still intends to accelerate its tightening cycle. Short term, key US yield resistance levels just proved to be a bridge too far. The acceleration of EMU inflation to the ECB's 2% inflation target in February was confirmed. US eco data printed near consensus (see headlines) and also failed to inspire trading. After opening losses, US Treasuries stabilized before Bunds. Deteriorating risk sentiment and declining oil prices eventually also put a floor for the Bund though.

The French treasury taps the on the run 3-yr OAT (€3.98B 0% Feb2020), on the run 5-yr OAT (€2.1B 0% May2022) and off the run OAT (€0.92B2.25% Oct2022). The combined amount sold was the maximum of the targeted €6-7B. The auction bid cover was 1.87, slightly below the average at French auctions. Additionally, the French treasury raised €1.82B via inflation-linked bonds. The Spanish debt agency sold the on the run 5-yr Bono (€1.67B 0.4% Apr2022), on the run 30-yr Obligacion (€0.67B 2.9% Oct2046) and two off the run Obligacions (€1.39B 1.3% Oct2026 & €1.08B 5.15% Oct2028). The total amount raised was near the upper bound of the €4-5B target range with a plain vanilla auction bid cover of 1.47.

Currencies

USD stabilizes after post-FOMC losses

Today, the dollar managed to stabilize versus euro and yen, following substantial losses in the aftermath of the FOMC decision yesterday eve. The USGerman yield differential was little changed today after narrowing yesterday. US eco data were close to expectations and thus largely ignored. European equities started strongly in the wake of WS gains, but eased, giving back half of the initial gains. Similarly, peripheral spread narrowing was soon erased. So, no full-blown risk-on session. EUR/USD moved in a 1.0710 to 1.0740 range and trades currently at 1.0730, 5 pips below opening levels. Aside of a brief dip lower at the European open, USD/JPY traded in the 113.20 to 113.55 range and is now quoted at 113.32, virtually unchanged from opening levels.

Overnight, Asian equities joined the post-Fed equity rally in the US yesterday eve. The dollar held near yesterday's lows. The decline of core bond yields and of the dollar supported equities. Commodities/commodity related assets also performed well. The BOJ left its policy rate (-0.1%) and the target level for the 10y government bond yield (0.0%) unchanged. The market reaction was very limited. USD/JPY traded in a 113.55/15 sideways range. EUR/USD maintained its post-Fed gains, trading sideways in a narrow 1.0720/45 range.

The Fed decision and the outcome of the Dutch parliamentary election (with a "bad" result for the far-right anti-euro PVV party of Wilders) caused a nice risk-on environment at the European open. Equities showed gains of 1% (or more). Core European yields gradually rebounded, contrary to the drop of US yields yesterday evening. Intra-EMU sovereign spreads narrowed modestly, but gradually lost gains. Even so, it didn't provide a clear driver for USD or euro trading. EUR/USD held a very tight range in the lower part of the 1.07 big figure. Post-Fed USD softness initially pushed USD/JPY briefly to the 113 area, but the rise in core yields and the equity rally propelled the pair back to the mid 113.50 area.

During the US session, the US eco data (see headlines) were again close to expectations. US Treasuries stabilized and US equity futures lost the Asian gains. In this context EUR/USD and USD/JPY meandered in their tight intraday range, but to its soft dollar side.

Sterling supported by somewhat hawkish BoE Minutes

EUR/GBP and cable held very tight ranges this morning as investors awaited the BoE policy decision. The BoE as expected left its policy unchanged. However, Kristin Forbes dissented in favour of a rate hike and the Minutes contained a note of concern on inflation. "some members noted that it would take relatively little further upside news on the prospects of activity or inflation for them to consider that a more immediate reduction in policy support might be warranted." This took sterling traders awry and triggered some frenetic sterling buying. EUR/GBP dropped from 0.8740 to about 0.8680, where a pause occurred. Cable jumped from about 1.2260 to 1.2360, prolonging yesterday's post-FOMC dollar triggered cable rally. The moves are technically insignificant, but a short term high in EUR/GBP (around 0.8790) may now be in place.

Bank of England Review – Maintains Neutral Stance with Hawkish Twist

In line with our expectations the Bank of England (BoE) made no policy changes at its March meeting and reiterated its neutral stance by repeating it could move 'in either direction'.

However, there was a hawkish twist. First, Kristin Forbes (a known hawk) voted for a March hike. Note, though, that she is leaving the BoE on 30 June 2017, which makes her hawkish stance less important. Second, the statement revealed that 'some members noted that it would take relatively little further upside news…for them to consider that a more immediate reduction in policy support might be warranted'.

We still expect the BoE to remain on hold for the next 12 months. While we think it is unlikely the BoE will tighten monetary policy in a time of elevated political uncertainty, we think we need to see substantially slower growth and/or higher unemployment before easing becomes likely again. Also, BoE Governor Mark Carney has said that one of the reasons the UK has been resilient to Brexit uncertainties so far is due to the significant monetary easing from the BoE.

Note that the BoE reaction function has changed since the financial crisis: BoE puts more weight on growth/unemployment relative to inflation(see also a speech by former Monetary Policy Committee member Martin Wealehere, 18 July 2016). In our view, the BoE seems to be more worried about slower growth than too-high inflation if this is only temporary.

We still see risks skewed on the upside for EUR/GBP

EUR/GBP moved slightly lower and Gilt yields ticked 4bphigher driven by the more hawkish tone in the statement, where Kristin Forbes voted for a 25bp rate hike this time. Note, however, that Forbes is a known hawk and leaves the BoE this summer.

The market is now pricing in an accumulated 8bprate hike from the BoE in 2017 and 26bpby the end of 2018. We still think the market's pricing is too hawkish, suggesting little support for the GBP driven by higher UK interest rates ahead. Hence, relative rates, in our view, favour lower GBP/USD, as the Fed is slightly underpriced, while risks stemming from relative rates are more balanced for EUR/GBP, as the market has turned too hawkish on the ECB pricing as well, with a 10bp rate hike priced by March 2018.

EUR/GBP has fallen back below our 1-3M target of 0.87. As such, we still see risks skewed on the upside for EUR/GBP, as we expect GBP to underperform vis-à-vis the USD and EUR in coming weeks and following the triggering of Article 50.

However, the Brexit risk premium priced on GBP has increased over the past two to three weeks and, given that investors are very short GBP, according to IMM, further GBP short covering could pave the way for a short-term correction lower in EUR/GBP.

Three main triggers for BoE

The summary of the BoE meeting in March contained three main triggers for changes to the BoE's current monetary policy stance.

- CPI inflation.

- Wage growth.

- Private consumption.

Higher CPI inflation and/or higher wage growth than currently expected would increase the likelihood of a hike.

Slower private consumption growth than expected would increase the likelihood of a cut.

Too hawkish BoE pricing, in our view

BoE February Projections

BoE expects CPI inflation to move higher from here

In connection with its March meeting, the BoE stated that its 'February projections remained broadly on track'.

In the latest Inflation Report, the BoE projects CPI inflation will increase significantly from here due to the weaker GBP, which has pushed up import prices.

The BoE expects inflation to peak around 2.8%.

The BoE expects the overshooting of inflation to be temporary, i.e. it expects inflation to fall back to 2% beyond the forecast horizon.

BoE expects GDP growth to slow in coming years to around 1.5%

The BoE now expects GDP growth of 0.6% in Q1 17, which is 0.1pp higher than projected in the February Inflation Report.

We are more pessimistic on GDP growth than the BoE. Note that PMIs suggest that GDP growth has been in the range of 0.3-0.4% in Q1 17 - see page 13.

The BoE projects GDP growth will slow in coming years due to the following.

- Slower private consumption growth.

- Slower business investments.

BoE expects unemployment rate to stabilise above NAIRU

At the March meeting, the BoE stated that its 'February projections remained broadly on track'.

The BoE no longer expects the unemployment rate to rise significantly as in previous inflation reports.

One reason for this is that the BoE has revised down its NAIRU estimate from 5.0% to 4.5%, i.e. there is currently more slack left in the labour market than it estimated previously.

Macro Charts

GDP growth has been resilient to Brexit uncertainties

PMIs suggest Q1 GDP growth in the range of 0.3-0.4% q/q

Inflation expected to rise supported by weak GBP

End of food and energy deflation

Inflation expectations have rebounded

Netherlands Election: Populism Faces First Defeat at the Polls

Election Highlights

Yesterday Dutch voters rejected the populist, right-wing rhetoric of Geert Wilders of the Freedom Party (PVV), choosing to stand with the tried and true rule of a coalition of centrist parties. The People's Party for Freedom and Democracy (VVD), the centre-right leaning party whose leader is the incumbent prime minister, is currently projected to have won the most seats at 33 – eight seats less than it previously held (final results on the distribution of seats are expected within a week). While the PVV is projected to win the second most seats at 20, they are unlikely to be invited to participate in coalition talks. The Labour Party (PvdA) suffered a historic defeat, as voters supported less established left-leaning parties.

While talks to form a new coalition government have begun, it could take months before a government is in place. In fact, since World War II it has taken an average of 72 days for a coalition government to form in the Netherlands. Although we won't know the exact composition of the coalition government, we do know that it will likely require the participation of at least four parties. Note that in the Netherlands a coalition government needs 76 out of 150 seats in the Dutch parliament for an absolute majority.

Financial markets have reacted positively to the election result, with the EURUSD firming after exit polls in the Netherlands suggested that the PVV was not on pace to win much more than 20 seats. Moreover, bond spreads between Dutch and German bunds have narrowed a touch.

The focus now shifts to the French Presidential elections, with the first round slated for April 23rd.

Next steps for the new coalition government: budget finances, euro, and immigration

Now that the election is over, the difficult task of governing begins. The larger number of coalition partners will make it more difficult for the new government to appoint a cabinet and push through the structural economic reforms necessary to counter headwinds to growth from an aging labour force and weak productivity growth.

Fortunately, government finances in the Netherlands have improved considerably since the Great Recession, with the primary budget deficit turning to a surplus for the first time last year. Undoubtedly, the return to surplus was largely driven by economic growth about twice its trend pace, estimated at about 1% in 2016.

Despite this improvement, there are some signs of economic slack in the Netherlands. Most evidently, the unemployment rate has yet to return to its pre-recession average despite a pronounced decline in the participation rate similar to that experienced in the United States. Estimates of the output gap confirm that there is still excess supply. However, another year of 2% growth – twice the pace of trend – will likely eliminate it.

Looking further ahead, the consensus forecast suggests that economic growth will slow to 1.3% by 2019, suggesting that the improvement in government finances coming from above-trend growth will soon have to yield to a more cost conscious, active management by fiscal authorities. This too could prove very challenging given the need for approval by a multitude of parties.

The two main issues that the populist PVV heavily campaigned on were a referendum on the Netherlands remaining part of the EU and immigration reform. At this time, there is no indication that a coalition government will consider holding a referendum on EU or euro membership in the near future. However, in late February the Dutch legislature approved the investigation by the Council of the State (its legal advisor) to have it review whether it's legally possible for the Netherlands to withdraw from the euro. It should be noted that referendums in the Netherlands are advisory only, as stated in the Advisory Referendum Act. Moreover, referenda can only be held over newly adopted laws or treaties, making a referendum on changes to any past EU treaties illegal, barring legislative changes. Given the legislative challenges and lack of support in both houses of parliament, it's unlikely that the Netherlands will be able to hold a binding referendum on the euro or EU membership in the next couple of years.

The other common theme amongst populist political parties in advanced economies involves a reduction in immigration. Population statistics for the European Union (EU) (as of January 1, 2015) suggest that about 11.8% of the Dutch population was born abroad: 3.1% in the EU, and the remaining 8.7% born in a country outside of the EU. The percentage of non-EU born citizens is similar to that of its immediate neighbours (Belgium: 8.5%; France: 8.6%). Much of the immigration into the Netherlands and elsewhere in core EU nations has been in the key 16-35 year old demographic, and the influx of youth is needed to help stave off the secular decline in the labour force. However, the perception of the newcomers' lack of desire to integrate will continue to sow anxiety amongst native born Dutch, particularly those who see themselves competing for jobs and housing. Should the Netherlands materially slow immigration, it would work against efforts to boost its labour force. According to OECD estimates, trend labour force growth has fallen from about 1.0% in the early 2000s to 0.4% in 2016. Given its importance to sustaining the labour force and helping the supply side of the economy, immigrant settlement and naturalization will have to become a priority not only for the new coalition government in the Netherlands, but other core EU nations facing similar structural declines.

While the populist threat has been extinguished in the Netherlands, attention turns to France's election

France is set to vote in the first and second round Presidential elections on April 23rd and May 7, respectively. Recent polls suggest that Marine Le Pen, the leader of the Front Nationale (FN) party, could take the first vote, but is unlikely to win the second vote against any other candidate. While odds are low of a Le Pen victory, the experience of 2016 does suggest that anything can happen. Even if Marine Le Pen were to win the presidency, she would likely lack the support of the French legislature to push for a referendum on EU or euro membership. We will preview the French election in a forthcoming note.

Pound Gains Continue on Split BoE Rate Vote

GBP/USD has posted gains on Thursday, continuing the upward movement which marked the Wednesday session. In North American trade, the pair is trading at 1.2360. On the release front, the BoE maintained the benchmark lending rate at 0.25%. The vote was expected to be unanimous, but one MPC member voted in favor of raising rates by a quarter-point. In the US, Building Permits fell to 1.21 million, missing the estimate of 1.26 million. The Philly Fed Manufacturing Index dropped sharply to 32.8, above the forecast of 30.2 points. On the labor front, unemployment claims ticked down to 241 thousand, beating the forecast of 245 thousand. On Friday, the US will publish the UoM Consumer Sentiment report.

There was a surprise from the Bank of England on Thursday. The Monetary Policy Committee did not alter interest rates, which have been pegged at 0.25 percent since August 2016. However, one member of the MPC, Kristen Forbes, voted in favor of a 0.25% rate hike, while the other 8 members voted to maintain rates at their current level. This move helped boost the pound above 1.2350 for the first time since March 1. The markets had predicted that the vote in favor of maintaining the rate would be unanimous at 9-0. The BoE is likely to face more pressure to raise rates, as inflation continues to climb. The minutes acknowledged higher inflation levels, noting that inflation could exceed the 2% target by the summer, given the depreciation in the British pound.

There were no raised eyebrows when the Federal Reserve raised rates by a quarter-point on Wednesday, as the markets had priced a rate hike at over 90%. The rate hike, the second in just three months, raised the raised the benchmark lending rate to a 0.75%-1% range. What was not expected, however, was the sharp drop of the dollar against its major rivals. The markets were hoping that a red-hot US economy would propel the Fed to accelerate its pace of monetary tightening. There was disappointment as Fed Chair Janet Yellen reiterated that further rate hikes would be done gradually, pushing the dollar on Wednesday. As well, the US dollar may have lost ground due to traders and investors acting on "buy on rumor, sell on fact". This larges-scale selling of US dollars after the Fed hike has sent the US dollar broadly lower, with the pound gaining 1.7 percent since the Fed announcement.

Trade Idea Wrap-up: USD/CHF – Sell at 1.0020

USD/CHF - 0.9955

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9980

Kijun-Sen level : 1.0025

Ichimoku cloud top : 1.0088

Ichimoku cloud bottom : 1.0085

Original strategy :

Sell at 1.0030, Target: 0.9930, Stop: 1.0065

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0020, Target: 0.9920, Stop: 1.0055

Position : -

Target : -

Stop : -

As the greenback has fallen again after brief recovery, suggesting the decline from 1.0171 top is still in progress and bearishness remains for further weakness to 0.9920-25, however, loss of near term downward momentum should prevent sharp fall below 0.9900 and reckon 0.9870-75 would hold from here, risk from there has increased for a strong rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as the Kijun-Sen (now at 1.0025) should limit upside and bring another decline. Only above previous support at 1.0060 (now resistance) would abort and signal low is formed instead, risk rebound to 1.0090-95 first.

Trade Idea Wrap-up: GBP/USD – Buy at 1.2300

GBP/USD - 1.2354

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2278

Kijun-Sen level : 1.2244

Ichimoku cloud top : 1.2193

Ichimoku cloud bottom : 1.2183

Original strategy :

Buy at 1.2300, Target: 1.2400, Stop: 1.2265

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2300, Target: 1.2400, Stop: 1.2265

Position : -

Target : -

Stop : -

As cable rallied again after finding renewed buying interest at 1.2241, adding credence to our view that the rise from 1.2109 low is still in progress for retracement of recent decline, hence further gain to previous support at 1.2384 would be seen, however, near term overbought condition should prevent sharp move beyond 1.2410-15 and price should falter well below resistance at 1.2471, bring retreat later.

In view of this, we are looking to buy cable on pullback but at a higher level as 1.2300-10 should limit downside and bring another rise. Below 1.2265-70 would suggest top is possibly formed, risk test of said support at 1.2241 which is likely to hold on first testing.

Trade Idea Wrap-up: EUR/USD – Buy at 1.0675

EUR/USD - 1.0735

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.0725

Kijun-Sen level : 1.0680

Ichimoku cloud top : 1.0640

Ichimoku cloud bottom : 1.0624

Original strategy :

Buy at 1.0675, Target: 1.0775, Stop: 1.0640

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0675, Target: 1.0775, Stop: 1.0640

Position : -

Target : -

Stop : -

As the single currency found renewed buying interest at 1.0600 yesterday and has rallied, reviving our bullishness for recent erratic upmove from 1.0493 low to extend further gain to 1.0755, break there would encourage for headway to 1.0775-90 but reckon resistance at 1.0799 would limit upside and price should falter well below resistance at 1.0829, bring retreat later.

In view of this, would not chase this rise here and we are looking to buy euro on pullback as the Kijun-Sen (now at 1.0677) should limit downside. Below the upper Kumo (now at 1.0657) would signal top is formed, bring weakness to 1.0620-25 but said support at 1.0600 should remain intact.

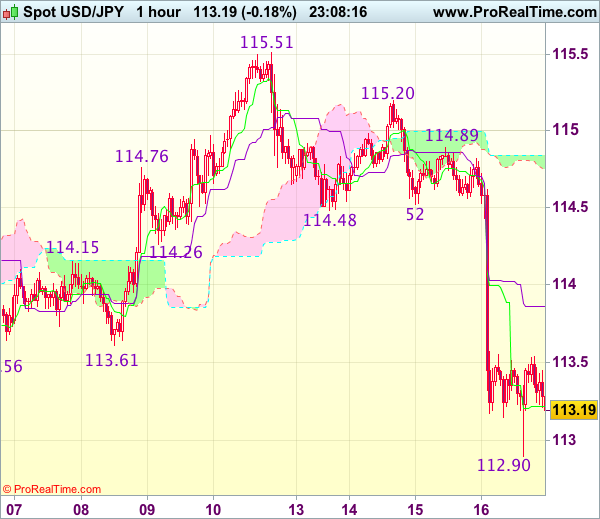

Trade Idea Wrap-up: USD/JPY – Sell at 114.00

USD/JPY - 113.15

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 113.22

Kijun-Sen level : 113.86

Ichimoku cloud top : 114.85

Ichimoku cloud bottom : 114.74

Original strategy :

Sell at 114.00, Target: 113.00, Stop: 114.35

Position : -

Target : -

Stop : -

New strategy :

Sell at 114.00, Target: 113.00, Stop: 114.35

Position : -

Target : -

Stop : -

Although the greenback tumbled today and dropped below 113.00 level, lack of follow through selling and current rebound suggest consolidation above support at 112.90 would be seen and recovery to 113.55-60 cannot be ruled out, however, reckon 114.00-05 would limit upside and bring another decline later. A break of said support at 112.90 would extend the fall from 115.51 to 112.76-77, then towards 112.50 but reckon downside would be limited to 112.00-10, bring rebound later.

In view of this, we are looking to sell dollar on recovery as 114.00 should limit upside. Only above previous support at 114.48-52 would abort and signal low is formed instead, risk a stronger rebound to 114.89 resistance first, break there would signal the retreat from 115.51 has ended, then gain to 115.20 resistance would follow.

Elliott Wave Analysis: S&P500 Showing First Signs Of A Completed Correction; More Weakness To Follow

S&P500 is showing us first signs of a completed higher degree three wave correction, that was recognized in wave B or 2. Well, current fall suggest that more weakness may in store for the S&P and ideally in a five wave sequence. That said, a break beneath the 2359 region would indicate a completed correction and more weakness to follow.

S&P500, 1H