Sample Category Title

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.72; (P) 113.80; (R1) 114.44; More...

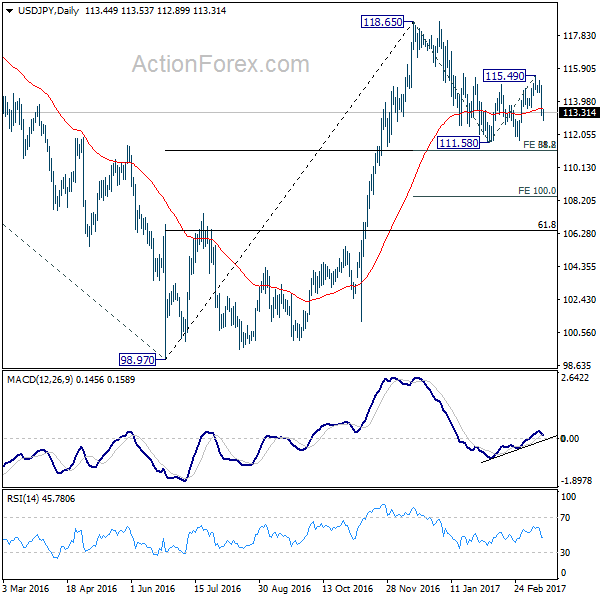

Intraday bias in USD/JPY remains on the downside for 111.58 low. Current development argues that consolidation from 111.58 has completed with three waves to 115.49. And larger decline from 118.65 is resuming. Break of 111.58 will target 61.8% projection of 118.65 to 111.58 from 115.49 at 111.12. That coincides with 38.2% retracement of 98.97 to 118.65 at 111.13. We'd tentatively expect strong support from there to bring rebound. But firm break there will target 100% projection at 108.42. On the upside, outlook will stays bearish as long as 115.49 holds, in case of recovery.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Rejection from 125.85 and below will extend the consolidation with another falling leg before up trend resumption.

Trade Idea Update: USD/CHF – Sell at 1.0030

USD/CHF - 0.9967

Original strategy :

Sell at 1.0050, Target: 0.9950, Stop: 1.0085

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0030, Target: 0.9930, Stop: 1.0065

Position : -

Target : -

Stop : -

As the greenback has fallen again after brief recovery, suggesting the decline from 1.0171 top is still in progress and bearishness remains for further weakness to 0.9930-35, however, loss of near term downward momentum should prevent sharp fall below 0.9900, risk from there has increased for a strong rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as the Kijun-Sen (now at 1.0030) should limit upside and bring another decline. Only above previous support at 1.0060 (now resistance) would abort and signal low is formed instead, risk rebound to 1.0090-95 first.

SNB Pledges to Carry On Intervention as Political Risks Raise Franc’s Demand

As widely anticipated, SNB left the sight deposit rate unchanged at -0.75%. The target range for the three-month Libor stayed at between -1.25% and -0.25%. Reiterating the excessive strength in Swiss franc, the central bank pledged that it would "remain active in the foreign exchange market as necessary, while taking the overall currency situation into consideration. Policymakers acknowledged ongoing improvements in the global economy but noted that it is "is still subject to considerable risks", among which the key is political uncertainty with "respect to the future course of economic policy in the US, upcoming elections in Europe, and the complex exit negotiations between the UK and the EU".

On the economic outlook, SNB forecasts CPI to increase +0.3% this year, up from +0.1% projected in December, before rising to +0.4% (December +0.5%) and +1.1% in 2018 and 2019, respectively. the upward revision in this year's inflation was mainly driven by the rally in oil prices. The central bank forecast GDP to expand +1.5% in 2017, although there is "considerable uncertainty emanating from international risks". Regarding the weaker-than-expected GDP growth in 4Q17, SNB noted that "a more extensive analysis of the available economic indicators points to an ongoing moderate recovery in the final months of the year; developments on the labor market support this view".

Earlier this month, Governor Thomas Jordan cautioned that, citing Trump's trade policy, Brexit and general elections in Germany and France, "increased political uncertainty" is "always delicate for us because Switzerland is increasingly viewed as a safe haven". SNB's FX reserves rose to a record high of CHF 668B. Total balance sheet is over 115% of GDP. This signals that the central bank intervened to suppress franc's appreciation by selling it for foreign currencies.

Trade Idea Update: GBP/USD – Buy at 1.2300

GBP/USD - 1.2357

Original strategy :

Buy at 1.2200, Target: 1.2310, Stop: 1.2165

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2300, Target: 1.2400, Stop: 1.2265

Position : -

Target : -

Stop : -

As cable rallied again after finding renewed buying interest at 1.2241, adding credence to our view that the rise from 1.2109 low is still in progress for retracement of recent decline, hence further gain to previous support at 1.2384 would be seen, however, near term overbought condition should prevent sharp move beyond 1.2410-15 and price should falter well below resistance at 1.2471, bring retreat later.

In view of this, we are looking to buy cable on pullback but at a higher level as 1.2300-10 should limit downside and bring another rise. Below 1.2265-70 would suggest top is possibly formed, risk test of said support at 1.2241 which is likely to hold on first testing.

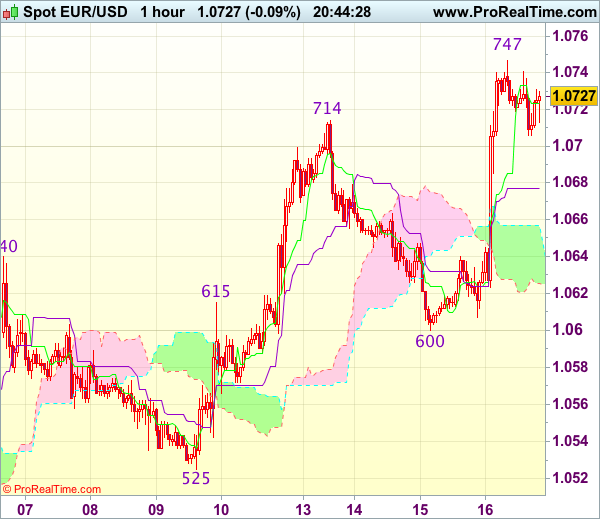

Trade Idea Update: EUR/USD – Buy at 1.0675

EUR/USD - 1.0732

Original strategy :

Buy at 1.0675, Target: 1.0775, Stop: 1.0640

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0675, Target: 1.0775, Stop: 1.0640

Position : -

Target : -

Stop : -

As the single currency found renewed buying interest at 1.0600 yesterday and has rallied, reviving our bullishness for recent erratic upmove from 1.0493 low to extend further gain to 1.0755, break there would encourage for headway to 1.0775-90 but reckon resistance at 1.0799 would limit upside and price should falter well below resistance at 1.0829, bring retreat later.

In view of this, would not chase this rise here and we are looking to buy euro on pullback as the Kijun-Sen (now at 1.0677) should limit downside. Below the upper Kumo (now at 1.0657) would signal top is formed, bring weakness to 1.0620-25 but said support at 1.0600 should remain intact.

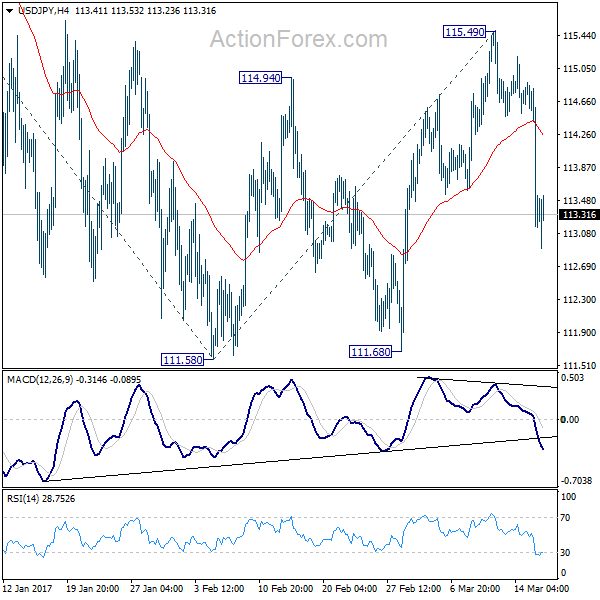

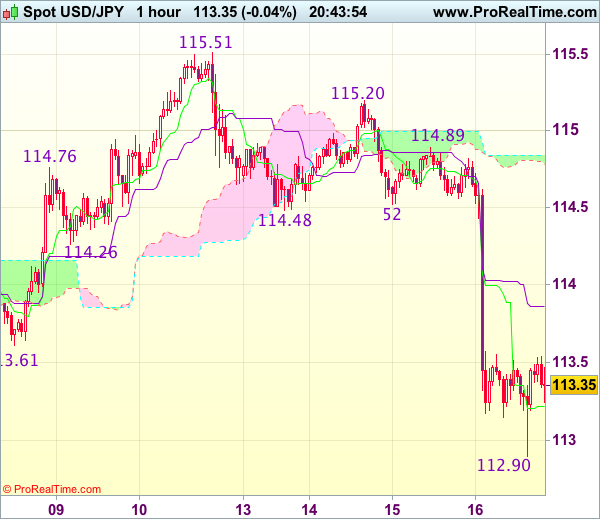

Trade Idea Update: USD/JPY – Sell at 114.00

USD/JPY - 113.35

Original strategy :

Sell at 114.00, Target: 113.00, Stop: 114.35

Position : -

Target : -

Stop : -

New strategy :

Sell at 114.00, Target: 113.00, Stop: 114.35

Position : -

Target : -

Stop : -

Although the greenback tumbled today and dropped below 113.00 level, lack of follow through selling and current rebound suggest consolidation above support at 112.90 would be seen and recovery to 113.55-60 cannot be ruled out, however, reckon 114.00-05 would limit upside and bring another decline later. A break of said support at 112.90 would extend the fall from 115.51 to 112.76-77, then towards 112.50 but reckon downside would be limited to 112.00-10, bring rebound later.

In view of this, we are looking to sell dollar on recovery as 114.00 should limit upside. Only above previous support at 114.48-52 would abort and signal low is formed instead, risk a stronger rebound to 114.89 resistance first, break there would signal the retreat from 115.51 has ended, then gain to 115.20 resistance would follow.

Yen Improves to 2-Week Gains as Fed Raises Rates

USD/JPY is almost unchanged in the Thursday session, after declining 1.1% on Wednesday. Currently, the pair is trading at 113.30. On the release front, the BoJ stood pat and maintained interest rates at -0.10%. The US, will release three key indicators – Building Permits, Philly Fed Manufacturing Index and unemployment claims. The week wraps up with consumer confidence data, with the release of UoM Consumer Confidence on Friday.

As expected, the Bank of Japan rate announcement on Wednesday was a non-event. The central bank opted to leave rates at -0.10%, where they have been pegged for over a year. The Japanese economy has showed improvement, recording four consecutive quarters of growth. However, the BoJ is unlikely to feel pressure to raise rates anytime soon, as inflation levels are still well below the central bank's target of around 2 percent. The BoJ is comfortable maintaining its ultra-loose monetary policy for the time being. However, if the yen again falls below the 120 line, the US will likely complain of currency manipulation and unfair trade practices by Japan. It wasn't that long ago, when yen was trading close to the 100 level, that the shoe was on the other foot, and Japan was warning that it would take unilateral action to combat what it viewed as currency manipulation. Clearly then, a "fair" exchange rate depends on the eye of the beholder.

There were no surprised faces when the Federal Reserve raised rates by a quarter-point on Wednesday. The hike, the second in just three months, raised the benchmark rate to the 0.75%-1.00% range. What was not expected, however, was the sharp drop of the dollar against its major rivals, including the yen. The markets were hoping that a red-hot US economy would propel the Fed to accelerate its pace of monetary tightening. There was disappointment as Fed Chair Janet Yellen reiterated that further rate hikes would be done gradually, pushing the dollar on Wednesday. As well, the US dollar may have lost ground due to traders and investors acting on "buy on rumor, sell on fact". This larges-scale selling of US dollars after the Fed hike has sent the US dollar broadly lower.

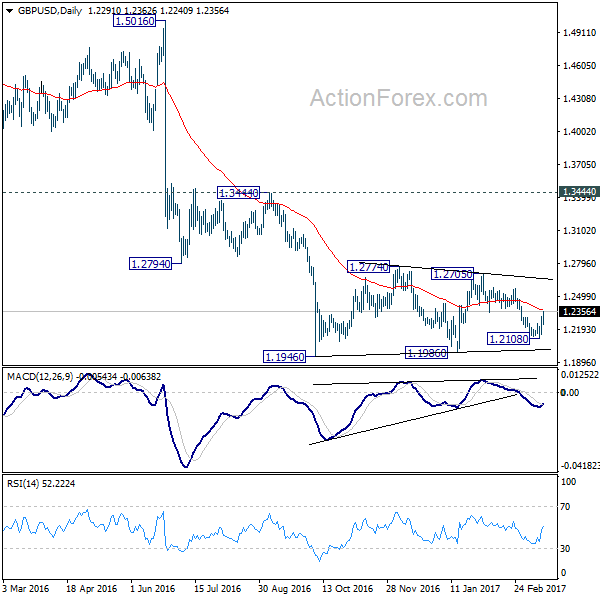

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2183; (P) 1.2246; (R1) 1.2350; More...

GBP/USD's rebound from 1.2108 extends higher today. The break of 1.2346 resistance argues that fall from 1.2705 is completed. And, the consolidation pattern from 1.1946 is extending with another rising leg. Intraday bias is turned back to the upside for 1.2569 resistance first. Break will target 1.2705/2774 resistance zone next. On the downside, below 1.2240 minor support will turn bias back to the downside for 1.2108 instead.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Sterling Surges as BoE Forbes Voted for Hike, SNB on Hold

Sterling jumps sharply after BoE left monetary policies unchanged as widely expected. That is, benchmark interest rate was kept at 0.25%, asset purchase target was kept at GBP 435b. Most importantly, the decision for interest rate was not unanimous. Kristin Forbes voted for a 25bps hike. That's seen by the markets as sign of a split in the MPC with some policymakers getting more intolerant to the surge in inflation. As noted in the minutes, "some members noted that it would take relatively little further upside news on the prospects of activity or inflation for them to consider that a more immediate reduction in policy support might be warranted." On the other hand, the majority stayed cautious on inflation outlook as wage growth has been "notably softer than expected, despite a further fall in the unemployment rate". Also, "estimates of retail sales had weakened notably" and that other indicators were "mixed".

SNB on hold, raised inflation forecast

SNB kept monetary policies unchanged as widely expected. Site deposit rate was held at -0.75%. Libor target range was kept at -1.25% to -0.25% too. The central bank noted in the statement that "a more extensive analysis of the available economic indicators points to an ongoing moderate recovery in the final months of the year; developments on the labour market support this view." Meanwhile, "compared to December, the new conditional inflation forecast is slightly higher for the next few quarters. Increased oil prices in particular contribute to the rise in inflation in the short term." SNB raised inflation forecast for 2017 to 0.3%, up from 0.1%.

On the other hand, it also pointed out that considerable risks remain for the global economy. And, "chief among these are political uncertainty with respect to the future course of economic policy in the US, upcoming elections in Europe, and the complex exit negotiations between the UK and the EU." SNB also reiterated that the Swiss Franc's exchange rate is "significantly overvalued" and kept itself open to intervention.

More in SNB Pledges to Carry On Intervention as Political Risks Raise Franc's Demand

Dollar stays as the weakest for the week

Dollar pares back some of post FOMC loss today but stays as the weakest major currency for the week. Released from US, housing start rose to 1.29m annualized rate in February. Building permits dropped to 1.21m. Initial jobless claims dropped 2k to 241k in the week ended March 11, better than expectation of 245k. Continuing claims dropped 30k to 2.03m in the week ended March 4. Philly Fed survey dropped to 32.8 in March, but beat expectation of 25.0. From Canada, international securities transactions dropped to CAD 6.2b in January.

Yesterday, FOMC raised the fed funds target range, by 25 bps, to 0.75%-1.00% with 9-1 vote. Minneapolis Fed President Neel Kashkari dissented as he favored leaving the monetary policy unchanged. The disappointments came from the fact that the Summary of Projections (SEP) shows virtually the same macroeconomic outlook. The median projection of federal fund rates was held at 1.4% by the end of 2017, same as December projection. Median projection for rate by the end of 2.18 was held at 2.1%, also same as December projection. Median projection for rate by the end of 2019 was revised by a mere 0.1% to 3.0%. Fed fund futures are pricing pricing in 49.6% chance of another hike in June, down from prior day's 53.2%. More in FOMC Delivered, Market Disappointed

Euro buoyed by Dutch elections

Euro is somewhat supported by the result of Dutch election. The election is seen by many as the first test on populism in Europe. Conservative prime minister Mark Rutte claimed victory and said that "this night is a night for the Netherlands -- after Brexit, after the American elections -- where we said stop it, stop it to the wrong kind of populism." The turnout rate for the election was 81%, highest in three decades. Rutte's Party for Freedom and Democracy is projected to win 33 seats out of 150 total. That's significantly higher than 20 seats of far rightist Geert Wilder's Freedom Party. Released from Eurozone, CPI was finalized at 0.4% mom, 2.8% yoy in February. Core CPI was finalized at 0.9% yoy.

BoJ on hold as widely expected

BoJ left monetary policies unchanged today as widely expected. Policy makers voted 7-2 to keep the Yield Curve Control unchanged. Short term policy rate is held at -0.1%. And BoJ will continue asset purchase at JPY 80T per annum. T. Sato and . T. Kiuchi voted against the decision. Regarding the economy, BoJ noted that it has "continued its moderate recovery trend", "exports have picked up". BoJ is optimistic that "Japan's economy is likely to turn to a moderate expansion." Risks to outlook include development in US and Fed's rate hikes, emerging economies, the consequences of Brexit.

BoJ governor said at the post meeting press conference that "the momentum for inflation to accelerate to 2 percent remains in place but lacks strength." And he pledged that BoJ will "continue to promote powerful monetary easing under the yield curve control framework to achieve its price target at the earliest date possible."

Aussie and Kiwi pare gains on weak data

Both Aussie and Kiwi pare some gains against Dollar after weak economic data. The Australian economy lost -6.4k jobs in February, much worse than expectation of 16.3k growth. Unemployment rate jumped 0.2% to 5.9%, above expectation of 5.7%. That's also the highest rate in more than a year. Contraction in job markets was led by -33.5k loss in part-time jobs. The 27.1k rise in full-time jobs couldn't make up the number. Some economists noted that there is basically no inflationary pressure from the labor market and wage growth. Meanwhile, further surge in unemployment rate could pressure the RBA for a rate cut despite facing bubbling in the housing markets. Also from Australia, consumer inflation expectation dropped to 4.0% in March.

New Zealand GDP rose only 0.4% qoq in Q4, slowed from prior quarter's downwardly revised 0.8 qoq. It also missed expectation of 0.7% qoq. The earthquake near Kaikoura back in November is seen as a factor skewing the data. But StatsNZ didn't directly mention any disruption to activity due to that earthquake. Meanwhile, weakness in manufacturing, which contracted by -1.6%, has trimmed -0.2% from GDP growth. For 2016 growth averaged 3.1%, which was an improvement over 2.5% in 2016. That's also the second straight year of above 3% growth.

PBoC raised short term repo and MLF rates

In China, the PBoC raised the key seven-day repo rate by 0.1% to 2.45%. The 14-day repo rate was also raised by 0.1% to 2.60%. Same amount was raised in 28-day repo rate to 2.75%. Meanwhile, For medium-term lending facility loans, the 6-month rate was raised by 0.1% to 3.05%. One-year MLF rate was raised by 0.1% to 3.2%. PBoC said that the hikes doesn't not constitute a benchmark rate increase. Instead, it's just a move to add flexibility for deleverage "deflating bubbles" and risk preventions.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2183; (P) 1.2246; (R1) 1.2350; More...

GBP/USD's rebound from 1.2108 extends higher today. The break of 1.2346 resistance argues that fall from 1.2705 is completed. And, the consolidation pattern from 1.1946 is extending with another rising leg. Intraday bias is turned back to the upside for 1.2569 resistance first. Break will target 1.2705/2774 resistance zone next. On the downside, below 1.2240 minor support will turn bias back to the downside for 1.2108 instead.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | GDP Q/Q Q4 | 0.40% | 0.70% | 1.10% | 0.80% |

| 00:00 | AUD | Consumer Inflation Expectation Mar | 4.00% | 4.10% | ||

| 00:30 | AUD | Employment Change Feb | -6.4K | 16.3K | 13.5k | |

| 00:30 | AUD | Unemployment Rate Feb | 5.90% | 5.70% | 5.70% | |

| 02:54 | JPY | BoJ Monetary Policy Statement | -0.10% | -0.10% | -0.10% | |

| 08:30 | CHF | SNB Sight Deposit Interest Rate | -0.75% | -0.75% | -0.75% | |

| 08:30 | CHF | SNB 3-Month Libor Lower Target Range | -1.25% | -1.25% | -1.25% | |

| 08:30 | CHF | SNB 3-Month Libor Upper Target Range | -0.25% | -0.25% | -0.25% | |

| 10:00 | EUR | Eurozone CPI M/M Feb | 0.40% | 0.40% | 0.40% | |

| 10:00 | EUR | Eurozone CPI Y/Y Feb F | 2.00% | 1.80% | 1.80% | |

| 10:00 | EUR | Eurozone CPI - Core Y/Y Feb F | 0.90% | 0.90% | 0.90% | |

| 12:00 | GBP | BoE Rate Decision | 0.25 | 0.25 | 0.25% | |

| 12:00 | GBP | BoE Asset Purchase Target Mar | 435B | 435B | 435B | |

| 12:00 | GBP | MPC Official Bank Rate Votes | 1--0--8 | 0--0--9 | 0--0--9 | |

| 12:00 | GBP | MPC Asset Purchase Facility Votes | 0--0--9 | 0--0--9 | 0--0--9 | |

| 12:30 | CAD | International Securities Transactions (CAD) Jan | 6.2B | 9.45B | 10.23B | 10.21B |

| 12:30 | USD | Housing Starts Feb | 1.29M | 1.26M | 1.25M | |

| 12:30 | USD | Building Permits Feb | 1.21M | 1.26M | 1.29M | |

| 12:30 | USD | Initial Jobless Claims | 241K | 245K | 243K | |

| 12:30 | USD | Philly Fed Survey Mar | 32.8 | 25 | 43.3 | |

| 14:30 | USD | Natural Gas Storage | -68B |

China: Money Market Policy Rates Increased – Official Rates Left Unchanged (For Now)

China raised a range of money market borrowing rates by 10bp this morning (7, 14 and 28-day repos, medium lending facility) - not long after the Fed hiked 25bp. The move by the People's Bank of China (PBoC) follows a 10bp hike in February. The official deposit and lending rates were kept unchanged, though.

China uses the money market facilities to try to reign in too much leverage in the financial system. Official lending and deposit rates are changed when deemed necessary to steer the real economy and inflation. Currently inflation is well below the 3% target but we expect it to move above target during spring and the PBoC to raise official rates by 2x 25bp over next six months.

The 3m money market rate is now very close to the upper level in the rate corridor of official rates as the 1-year lending rate is 4.35% and the 3m money market rate now at 4.33%. However, a larger part of the money market funding has moved to short maturities using 7-day and 14-day funding as the rates are much lower here. Hence in order to increase the real cost of money market funding, the PBoC needs to push up the cost of shorter-dated repo rates. The moves of 10bp at a time are very moderate, but it has been enough to push up the cost of borrowing through the bond market. The rise in bond yields is starting to weigh on highly indebted companies, which is why the PBoC is probably careful in not taking too big steps.

The Chinese money market system has evolved gradually over the past couple of years with many different facilities and rates, making it harder to interpret moves by the PBoC. However, the recent moves are most likely targeted at dampening leverage in the financial system, which has gone up over the past year in order to get a higher return in an environment where it has become harder to deliver the promised returns in for example Wealth Management Products. This is because yields have in general declined to low levels. Lower yields drive more leverage creating more financial fragility. It is this leverage that the PBoC is trying to dampen by making it more expensive.

CNY strengthened against USD yesterday from 6.89 to 6.85 following the Fed hike as the USD weakened. This morning CNH is a bit weaker again, moving up to around 6.87 against the USD. The CNH rate is again a bit stronger than CNY (6.874 vs 6.897). Hence companies with export income in CNY can take advantage of this and convert CNY to CNH at a 1-1 rate gaining the spread between the CNH and CNY.