Sample Category Title

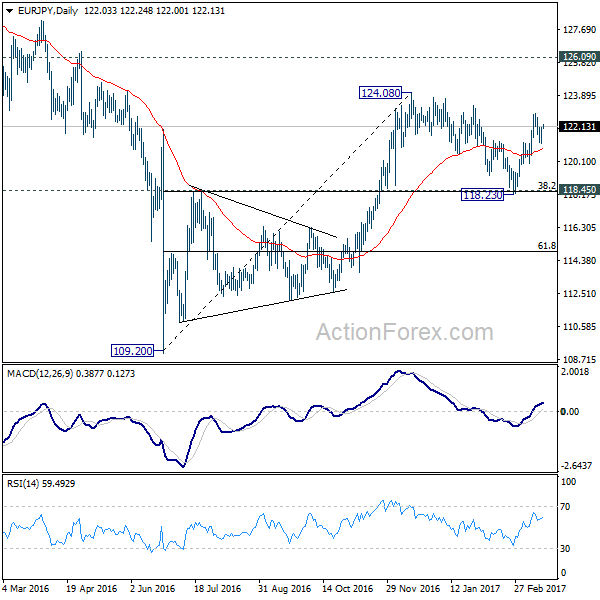

EUR/JPY Daily Outlook

Daily Pivots: (S1) 121.36; (P) 121.70; (R1) 122.27; More...

EUR/JPY recovered after breaching 121.18 resistance turned support and intraday bias remains neutral. No change in the bullish outlook for the moment and another rise is expected. Above 122.88 will target 124.08. Decisive break there will extend larger rise from 109.20 and target 126.09 key resistance next. However, firm break of 121.18 will likely extend the whole corrective pattern fro 124.08 with another falling leg towards 118.23 low again.

In the bigger picture, current development suggests that medium term rise from 109.20 is still in progress. Focus is now on 126.09 key resistance level. Sustained break will confirm completion of the whole decline from 149.76. And rise from 109.20 is of the same degree as the fall from 149.76. In such case, further rally would be seen to 104.04 resistance and possibly above before topping. Meanwhile, rejection from 126.09 will extend the fall from 149.76 through 109.209 low.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 138.73; (P) 139.67; (R1) 140.25; More...

GBP/JPY had another attempt at 138.53 support but rebounded from there again. The cross is staying in range of 138.53/142.79 and intraday bias remains neutral first. Price actions from 148.42 are viewed as a consolidation pattern. On the downside, break of 138.53 support will bring deeper decline to 136.44 support and possibly below. However, we'd expect strong support at 50% retracement of 122.36 to 148.42 at 135.39 to bring rebound. On the upside, above 142.79 will turn bias back to the upside for 144.77 and above.

In the bigger picture, price actions from 122.36 medium term bottom are still seen as a corrective pattern. Main focus is on 38.2% retracement of 195.86 to 122.36 at 150.42. Rejection from there will turn the cross into medium term sideway pattern with a test on 122.36 low next. Though, sustained break of 150.42 will extend the rebound towards 61.8% retracement at 167.78.

Dollar to End the Week as the Weakest Major, Euro Follows

Dollar is set to end the week as the worst performing major currency as post FOMC weakness continues. Meanwhile, Euro follows as the second weakest one after the positive impact of ECB and then Dutch election fades. Meanwhile, Australia dollar is leading the way high on solid risk appetite. And that is followed by Sterling which was lifted by hawkish BoE minutes yesterday. The forex markets are mixed elsewhere.

In other markets, the boost from FOMC to stocks was rather short lived as major indices ended mixed overnight. DJIA closed down -15.55 pts, or -0.07%, kept well below historical high at 21169.11. S&P 500 also closed down -3.88 pts, or -0.16%, at 2381.38, well below historical high at 2400.98. NASDAQ, on the other hand, attempted to hit record high at 5911.79 but reached 5911.48 only and closed at 5900.76, up 0.71 pts or 0.01%.

Treasury yields stabilized with TNX ended up 0.014 at 2.522. Meanwhile, WTI crude oil extends this week's consolidation and hovers around 49. Gold rebounded strongly on Dollar weakness and is back at around 1230.

ECB Nowotny: Could raise deposit rate earlier than prime rate

There has been some recent speculations that ECB would raise interest rate before ending the quantitative easing program. ECB governing council member Ewald Nowotny said in a newspaper interview that the central bank "will decide when the time comes". He explained that "there is the American model to end the bond purchases first. Whether this model can be applied to Europe on a like-for-like basis would need to be discussed." Meanwhile, "the structure of the interest rates does not always need to remain constant." And, "the ECB could also raise the deposit rate earlier than the prime rate."

The result of the Dutch elections was welcomed by European leaders in general. European Commission President Jean-Claude Juncker responded to the result of Dutch election and said that "the people of the Netherlands voted for "free and tolerant societies in a prosperous Europe". German Chancellor Merkel noted that she believed "many people are [glad] that a high turnout led to a very pro-European result". Centrist French presidential candidate Emmanuel Macron described it as "a breakthrough for the extreme right is not a foregone conclusion". Dutch Mark Rutte retained power and his pro-EU centre-right VVD remained the biggest party. Meanwhile, the anti-EU PVV party received just 13% of the vote share. The next closely-watched political event is the French presidential election is scheduled on April 23.

The Queen gave Royal Assent to Brexit bill

In UK, the Queen has given her Royal Assent to the Brexit bill. And, Prime minister Theresa May is reading to trigger Article 50 for Brexit negotiation with EU. Brexit Secretary David Davis said that "by the end of the month we will invoke Article 50, allowing us to start our negotiations to build a positive new partnership with our friends and neighbors in the European Union, as well as taking a step out into the world as a truly Global Britain."

Sterling remains supported by the hawkish BoE minutes released yesterday. To our, and the market's, surprise, BOE's Kristin Forbes voted in favor of a 25 bps rate hike. While this had not altered the decision of keeping the Bank rate unchanged at 0.25%, the overall message sent to the public has now become more hawkish. The members voted unanimously to leave the government bond purchases at 435B pound and corporate bond purchases at up to 10B pound. Adding to the rising speculations of tightening is the minutes, which suggested that some of those who voted for unchanged policy believed 'it would take relatively little further upside news on the prospects for activity or inflation for them to consider that a more immediate reduction in policy support might be warranted'. More in Forbes' Dissent Would Unlikely Speed Up BOE's Rate Hike Schedule

On the data front...

New Zealand business NZ manufacturing index rose to 55.2 in February. Eurozone will release Trade balance in European session. In US session, Canada will release manufacturing shipments. US will release industrial production, capacity utilization, U of Michigan sentiment and leading indicators.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 138.73; (P) 139.67; (R1) 140.25; More...

GBP/JPY had another attempt at 138.53 support but rebounded from there again. The cross is staying in range of 138.53/142.79 and intraday bias remains neutral first. Price actions from 148.42 are viewed as a consolidation pattern. On the downside, break of 138.53 support will bring deeper decline to 136.44 support and possibly below. However, we'd expect strong support at 50% retracement of 122.36 to 148.42 at 135.39 to bring rebound. On the upside, above 142.79 will turn bias back to the upside for 144.77 and above.

In the bigger picture, price actions from 122.36 medium term bottom are still seen as a corrective pattern. Main focus is on 38.2% retracement of 195.86 to 122.36 at 150.42. Rejection from there will turn the cross into medium term sideway pattern with a test on 122.36 low next. Though, sustained break of 150.42 will extend the rebound towards 61.8% retracement at 167.78.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ Manufacturing Index Feb | 55.2 | 51.6 | 52.2 | |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Jan | 22.3B | 24.5B | ||

| 12:30 | CAD | Manufacturing Shipments M/M Jan | 2.30% | |||

| 13:15 | USD | Industrial Production Feb | 0.30% | -0.30% | ||

| 13:15 | USD | Capacity Utilization Feb | 75.50% | 75.30% | ||

| 14:00 | USD | U. of Michigan Confidence Mar P | 97 | 96.3 | ||

| 14:00 | USD | Leading Indicators Feb | 0.20% | 0.60% |

Three Reasons Why Bond Bears Should Be Careful

The Fed is hiking, core inflation is heading higher and the job market is robust. So bond yields are going higher, right? At least these are some of the typical arguments we hear for being short duration in fixed income now. As it has been in the past when the Fed is hiking and unemployment going lower. However, history suggests that this can be a dangerous analysis.

We find that there is mainly one key driver for a bond bear market: whether the cycle is accelerating or not. Below we use the US ISM index as a gauge of this. As the chart below shows, over the past 25 years the 11 bear markets have all taken place while ISM was rising. The level has not been important. A high level of ISM is not enough to push yields higher if ISM is moving lower. Actually, a rise in ISM has been a necessary, but not always sufficient, condition for a bear market.

An acceleration in the cycle has also been a key ingredient in the latest ‘reflation' selloff in bonds. ISM has increased sharply over the past three-five months. It's also been a key ingredient in the reflation case we have pushed since November. Here we presented a checklist of four key factors for reflation with acceleration in the cycle being a key factor. Rising commodity price inflation was another one.

With this in mind, we see three reasons investors should be careful with short duration positions currently:

1. We are close to a peak in ISM manufacturing

2. Headline inflation is heading lower from here

3. Short duration is a crowded trade

AUD/USD: Aussie Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the AUD declined 0.42% against the USD and closed at 0.7669.

LME Copper prices rose 1.0% or $61.0/MT to $5911.0/MT. Aluminium prices rose 1.7% or $32.0/MT to $1895.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7684, with the AUD trading 0.2% higher against the USD from yesterday’s close.

The pair is expected to find support at 0.7656, and a fall through could take it to the next support level of 0.7628. The pair is expected to find its first resistance at 0.7714, and a rise through could take it to the next resistance level of 0.7744.

Next week, market participants will focus on the Reserve Bank of Australia’s (RBA) March meeting minutes, along with Australia’s house price index for 4Q and Westpac leading index for February.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving averages.

EUR/USD: Euro-Zone’s Annual Inflation Confirmed At A 4-Year High Level In February

For the 24 hours to 23:00 GMT, the EUR rose 0.38% against the USD and closed at 1.0771, after the Dutch Prime Minister, Mark Rutte's party won over anti-Islam lawmaker, Geert Wilders, in an election that many viewed as a defeat for the forces of political populism.

The Euro was boosted further, after the Euro-zone's final consumer price index (CPI) climbed 2.0% on an annual basis in February, confirming the preliminary print and maintaining its highest level in four-years. The CPI had registered a rise of 1.8% in the previous month.

The greenback lost ground against most of its key peers, as the US Federal Reserve's slightly cautious tone continued to weigh on investor sentiment.

In economic news, housing starts in the US jumped 3.0% on a monthly basis, to an annual rate of 1288.0K in February, climbing to a four-month high level, as unseasonably warm weather boosted the pace of single-family homebuilding to its strongest level in nearly a decade. Investors had envisaged housing starts to rise to a level of 1264.0K, following a revised level of 1251.0K in the prior month. On the other hand, the nation's building permits fell more-than-expected by 6.2% MoM, to an annual rate of 1213.0K in February, compared to market expectations of a fall to a level of 1268.0K and following a revised level of 1293.0K in the prior month.

Other economic data revealed that the number of Americans filing for fresh jobless claims eased to a level of 241.0K in the week ended 11 March 2017, compared to market consensus for a drop to a level of 240.0K and following a level of 243.0K in the prior week. Further, the nation's JOLTS job openings rose to a level of 5626.0K in January, after recording a revised reading of 5539.0K in the prior month, while markets anticipated an advance to a level of 5556.0K.

In the Asian session, at GMT0400, the pair is trading at 1.0772, with the EUR trading marginally higher against the USD from yesterday's close.

The pair is expected to find support at 1.0726, and a fall through could take it to the next support level of 1.0680. The pair is expected to find its first resistance at 1.0796, and a rise through could take it to the next resistance level of 1.0820.

Going ahead, investors will keep a close watch on the Euro-zone's trade balance and construction output data, both for January, slated to release in a few hours. Moreover, in the US the flash Michigan consumer confidence index for March, along with industrial as well as manufacturing production data, both for February, will keep investors on their toes.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

GBP/USD: BoE Holds Interest Rate At 0.25% But Decision Split Amid Rising Inflation Fears

For the 24 hours to 23:00 GMT, the GBP rose 0.53% against the USD and closed at 1.2353, after a Bank of England (BoE) policymaker surprised investors by voting to raise interest rates by 25 basis point, while some others indicated that they were also leaning towards raising interest rates in the foreseeable future.

The BoE, in its latest monetary policy meeting, maintained the benchmark interest rate steady at a record low of 0.25% in an 8-1 vote, with Kristin Forbes voting to raise borrowing costs immediately. Further, the central bank decided to leave the bond-purchase programme unchanged at £435.0 billion. The minutes from the meeting suggested that it would not take much for 'some'other officials to join her if inflation or economic growth rise significantly. Moreover, policymakers felt there were signs that consumers were turning more cautious as inflation rose while pay growth, which has been slowing in recent months, had turned out to be 'notably weaker'.

In the Asian session, at GMT0400, the pair is trading at 1.2352, with the GBP trading a tad lower against the USD from yesterday's close.

The pair is expected to find support at 1.2269, and a fall through could take it to the next support level of 1.2185. The pair is expected to find its first resistance at 1.2406, and a rise through could take it to the next resistance level of 1.2459.

Moving ahead, traders will look forward to the BoE's quarterly bulletin report, set to release in a few hours.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

USD/JPY: Japanese Yen Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.1% against the JPY and closed at 113.32.

Yesterday, the Bank of Japan (BoJ) Governor, Haruhiko Kuroda indicated that Japan will stick to its ultra-easy monetary policy, stating that an uptick in inflation towards 1.0% will not immediately trigger an interest rate hike.

On the data front, Japan's final machine tool orders advanced 9.1% on an annual basis in February, meeting preliminary estimates and following a rise of 3.5% in the previous month.

In the Asian session, at GMT0400, the pair is trading at 113.42, with the USD trading 0.09% higher against the JPY from yesterday's close.

The pair is expected to find support at 113.03, and a fall through could take it to the next support level of 112.64. The pair is expected to find its first resistance at 113.67, and a rise through could take it to the next resistance level of 113.92.

Looking ahead, investors look forward to the BoJ's recent meeting minutes accompanied with Japan's flash Nikkei manufacturing PMI, adjusted merchandise trade balance and all industry activity index, set to release next week.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

USD/CHF: SNB Sticks With Record-Low Interest Rate

For the 24 hours to 23:00 GMT, the USD declined 0.47% against the CHF and closed at 0.9957.

The Swiss National Bank (SNB), at its latest monetary policy meeting, kept the benchmark interest rate at -0.75% as widely expected. The central bank also reiterated that the Swiss Franc's exchange rate is “significantly overvalued” and kept itself open to intervention in the foreign exchange market. Further, the bank continues to expect GDP growth of roughly 1.5% for 2017 and raised inflation forecast for 2017 to 0.3%, up from 0.1%, on the back of an increase in oil prices.

In the Asian session, at GMT0400, the pair is trading at 0.9965, with the USD trading 0.08% higher against the CHF from yesterday's close.

The pair is expected to find support at 0.9939, and a fall through could take it to the next support level of 0.9912. The pair is expected to find its first resistance at 0.9999, and a rise through could take it to the next resistance level of 1.0032.

With no economic releases in Switzerland today, investors look forward to Switzerland's SECO economic forecast, trade balance and SNB's quarterly bulletin report, all due to release next week.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

USD/CAD: Loonie Trading A Tad Higher In The Asian Session

For the 24 hours to 23:00 GMT, the USD rose 0.19% against the CAD and closed at 1.3322.

In the Asian session, at GMT0400, the pair is trading at 1.3315, with the USD trading marginally lower against the CAD from yesterday's close.

The pair is expected to find support at 1.3275, and a fall through could take it to the next support level of 1.3236. The pair is expected to find its first resistance at 1.3353, and a rise through could take it to the next resistance level of 1.3392.

Going ahead, Canada's consumer price index and retail sales data, both due to release next week, will be on investor's radar.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.