Sample Category Title

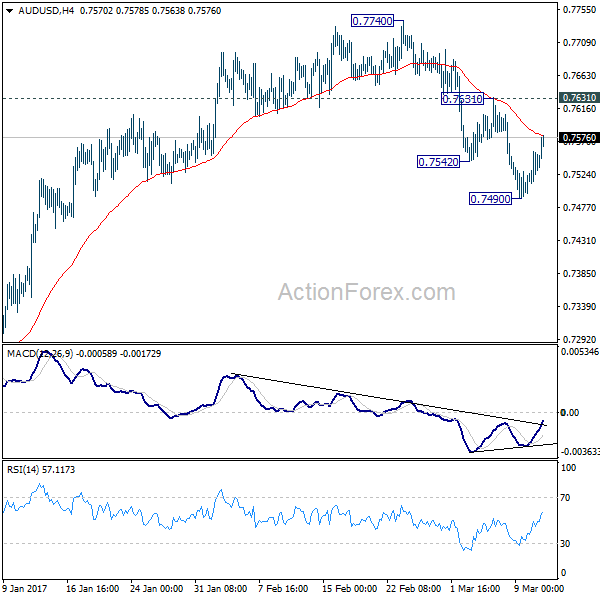

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7506; (P) 0.7531; (R1) 0.7564; More...

AUD/USD's rebound from 0.74900 continues today and further rise could be seen. But such rise is seen as a correction at this point. And intraday bias remains neutral. We'd expect upside to be limited by 0.7631 resistance and bring fall resumption. As noted before, rise from 0.7150 has completed at 0.7740 already. Below 0.7490 will turn bias back to the downside and target 0.7144/7158 support zone. However, break of 0.7631 resistance will dampen our bearish view and turn bias back to the upside for 0.7740 instead.

In the bigger picture, we're still treating price actions from 0.6826 low as a correction. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seek to 55 month EMA (now at 0.8185) and above.

AUD/USD: Aussie Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the AUD rose 0.52% against the USD and closed at 0.7539 on Friday.

LME Copper prices rose 1.1% or $59.5/MT to $5714.5/MT. Aluminium prices rose 2.0% or $37.5/MT to $1884.5/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7567, with the AUD trading 0.37% higher against the USD from Friday's close.

The pair is expected to find support at 0.7525, and a fall through could take it to the next support level of 0.7483. The pair is expected to find its first resistance at 0.7592, and a rise through could take it to the next resistance level of 0.7617.

Looking ahead, traders will await the release of Australia's NAB business confidence index for February, due to release tomorrow.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

EUR/USD: Euro Trading Higher In The Morning Session, Ahead Of A Speech By The ECB President

For the 24 hours to 23:00 GMT, the EUR rose 1.08% against the USD and closed at 1.0691 on Friday, after news emerged that some European Central Bank policymakers raised the possibility of an interest rate hike before the end of its bond purchase programme.

On the data front, Germany's seasonally adjusted trade surplus surprisingly expanded to a level of €18.5 billion in January, following a revised trade surplus of €18.3 billion in the prior month, while markets expected the nation's trade surplus to narrow to a level of €18.0 billion. Moreover, the nation's seasonally adjusted exports rebounded more-than-expected by 2.7% MoM in January, compared to a revised drop of 2.8% in the previous month. Also, the nation's seasonally adjusted imports climbed higher-than-expected by 3.0% on a monthly basis in January, after recording a revised rise of 0.1% in the prior month.

The greenback lost ground against a basket of major currencies, after the latest US jobs report revealed that wage growth was softer than expected in February, tempering expectations for aggressive interest rate hikes by the Federal Reserve this year.

Data indicated that non-farm payrolls in the US jumped 235.0K in February, surpassing market consensus for an advance of 200.0K, thus painting an improving picture of the nation's labour market. Non-farm payrolls had recorded a revised increase of 238.0K in the prior month. Moreover, the nation's unemployment rate eased to 4.7% in February, in line with market expectations and compared to a reading of 4.8% in the previous month. However, the nation's average hourly earnings of all employees grew less-than-estimated by 0.2% on a monthly basis in February, falling short of market expectations for an advance of 0.3% and compared to a revised similar rise in the previous month. Meanwhile, the nation's budget deficit narrowed less-than-expected to a level of $192.0 billion in February, compared to a surplus of $51.3 billion in the previous month.

In the Asian session, at GMT0400, the pair is trading at 1.0697, with the EUR trading 0.06% higher against the USD from Friday's close.

The pair is expected to find support at 1.0622, and a fall through could take it to the next support level of 1.0547. The pair is expected to find its first resistance at 1.0736, and a rise through could take it to the next resistance level of 1.0775.

Moving ahead, investors' will look forward to a speech by the European Central Bank's (ECB) President, Mario Draghi along with German Buba monthly report, both due later today. Additionally, the US labour market conditions index for February, slated to release later in the day, will be on investor's radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

GBP/USD: UK’s Manufacturing, Industrial And Construction Output, All Dropped In January

For the 24 hours to 23:00 GMT, the GBP rose 0.18% against the USD and closed at 1.2175 on Friday.

On the macro front, Britain's manufacturing production dropped more-than-anticipated by 0.9% on a monthly basis in January, following a revised rise of 2.2% in the prior month, while investors had envisaged for a fall of 0.7%. Further, the nation's industrial production registered a less-than-expected drop of 0.4% MoM in January, compared to a revised rise of 0.9% in the previous month. Moreover, the nation's construction output eased 0.4% in January, higher than market expectations for a drop of 0.2% and following a rise of 1.8% in the prior month. However, the nation's total trade deficit narrowed to a level of £1.97 billion in January, following a revised deficit of £2.03 billion in the prior month, whereas markets were anticipating the nation to register a deficit of £3.1 billion.

In other economic news, NIESR estimated that UK's gross domestic product (GDP) rose 0.6% in the three months to February, meeting market expectations and compared to a revised rise of 0.8% in the November 2016-January 2017 period.

In the Asian session, at GMT0400, the pair is trading at 1.2177, with the GBP trading marginally higher against the USD from Friday's close.

The pair is expected to find support at 1.2147, and a fall through could take it to the next support level of 1.2116. The pair is expected to find its first resistance at 1.2198, and a rise through could take it to the next resistance level of 1.2218.

With no economic releases in the UK today, investors will look forward to global macroeconomic news for further direction.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

USD/JPY: Japan’s Tertiary Industry Index Came In Flat In January

For the 24 hours to 23:00 GMT, the USD declined 0.25% against the JPY and closed at 114.79 on Friday.

In the Asian session, at GMT0400, the pair is trading at 114.81, with the USD trading marginally higher against the JPY from Friday's close.

Overnight data revealed that Japan's machinery orders unexpectedly dropped 3.2% MoM in January, compared to a revised advance of 2.1% in the prior month, whereas markets were expecting machinery orders to gain 0.5%.

Separately, early morning data showed that the nation's tertiary industry index surprisingly remained flat in January, compared to a revised drop of 0.3% in the prior month and defying market expectations for the index to advance 0.1%.

The pair is expected to find support at 114.45, and a fall through could take it to the next support level of 114.10. The pair is expected to find its first resistance at 115.33, and a rise through could take it to the next resistance level of 115.86.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

USD/CHF: Swiss Franc Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.32% against the CHF and closed at 1.0092 on Friday.

In the Asian session, at GMT0400, the pair is trading at 1.0082, with the USD trading 0.1% lower against the CHF from Friday’s close.

The pair is expected to find support at 1.0059, and a fall through could take it to the next support level of 1.0037. The pair is expected to find its first resistance at 1.0121, and a rise through could take it to the next resistance level of 1.0161.

Amid a lack of economic releases in Switzerland today, trading trend in the CHF is expected to be determined by global macroeconomic events.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

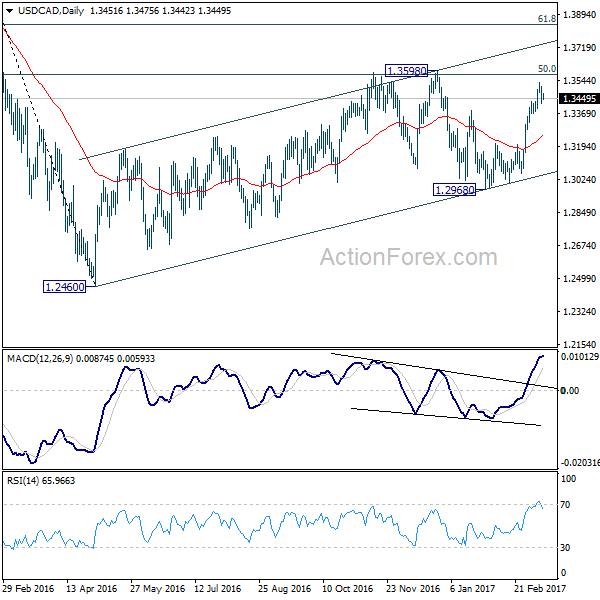

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3418; (P) 1.3466; (R1) 1.3512; More...

Intraday bias in USD/CAD remains neutral for the moment as the consolidation from 1.3534 continues. Deeper retreat could be seen back to 4 hour 55 EMA (now at 1.3391). But downside should be contained by 38.2% retracement of 1.3008 to 1.3534 at 1.3333 and bring another rally. Above 1.3534 will turn bias to the upside for retesting 1.3598 high next.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg, started from 1.2460 is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. Break of 1.2968 wold at least bring at retest of 1.2460 low. However, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

USD/CAD: Canada Unemployment Rate Declined To A 2-Year Low Level In February

For the 24 hours to 23:00 GMT, the USD declined 0.33% against the CAD and closed at 1.3464 on Friday.

The Canadian Dollar gained ground, after Canada's unemployment rate unexpectedly fell to 6.6% in February, hitting its lowest level in two-years, whereas markets were expecting the unemployment rate to remain steady at 6.8%.

In the Asian session, at GMT0400, the pair is trading at 1.3447, with the USD trading 0.13% lower against the CAD from Friday's close.

The pair is expected to find support at 1.3406, and a fall through could take it to the next support level of 1.3366. The pair is expected to find its first resistance at 1.35, and a rise through could take it to the next resistance level of 1.3554.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Dollar Extends Pre-FOMC Pullback, Four Central Bank Meeting Featured This Week

Dollar weakens broadly today as markets await a busy week ahead with four central bank meetings. Fed is widely expected to hike interest rate by 25bps this week. However, such expectation should be fully priced in, traders are looking through the FOMC meeting and turning cautious. In particular, Fed's updated Summary of Projections (SEP) and the monetary policy outlook for the rest of the year would be crucial to Dollar's trend in near term. Technically, the dollar index could dip further towards 100.66 key near term support before FOMC announcement on Wednesday.

BoJ, BoE, SNB to meet

In addition to FOMC meeting, BoJ, BoE and SNB will announce monetary policy decisions this week. All are scheduled for Thursday and thus, we'll have a 24 hours of central bank frenzy from Wednesday to Thursday. All, BoJ, BoE and SNB are expected to stand pat. BoJ is expected to maintain the so called yield curve control framework. BoE's bias would likely stay neutral but may adjust its view on upside risks in inflation. The SNB is expected to leave its sight deposit rate unchanged at -0.75%. These three central bank announcements could end up being non-events.

Oil slump could drag down CAD

Oil's extended decline is a development to watch in the financial markets this week. WTI crude oil dips to as low as 47.9 so far today, comparing to 54.94 high made last month. Oil price is current reversing the rally triggered by OPEC's agreement to cut production since December. It's now being weighed down by the surge in US productions and slower than expected fall in global supplies. WTI crude oil could now dip further to 44.07 fibonacci level. And that's possibly a factor to push USD/CAD through 1.3598 key resistance.

Elsewhere...

Japan domestic CGPI dropped -3.2% yoy in February, well below expectation of 1.0% yoy. Machine orders rose 1.0% mom in January, above expectation of 0.0% mom. Tertiary industry index rose 0.0% mom in January versus expectation of 0.2% mom. The rest of the calendar is light together with US labor market condition index featured.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3418; (P) 1.3466; (R1) 1.3512; More...

Intraday bias in USD/CAD remains neutral for the moment as the consolidation from 1.3534 continues. Deeper retreat could be seen back to 4 hour 55 EMA (now at 1.3391). But downside should be contained by 38.2% retracement of 1.3008 to 1.3534 at 1.3333 and bring another rally. Above 1.3534 will turn bias to the upside for retesting 1.3598 high next.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg, started from 1.2460 is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. Break of 1.2968 wold at least bring at retest of 1.2460 low. However, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Domestic CGPI Y/Y Feb | -3.20% | 1.00% | 0.50% | |

| 23:50 | JPY | Machine Orders M/M Jan | 1.00% | 0.00% | 6.70% | |

| 4:30 | JPY | Tertiary Industry Index M/M Jan | 0.00% | 0.20% | -0.40% | -0.30% |

| 14:00 | USD | Labor Market Conditions Index Change Feb | 1.3 |

Volatile Week Ahead For The USDJPY

Key Points:

- USDJPY Facing interest rate decision from the Fed and BOJ in the coming week.

- Possibility that the Federal Reserve could alter their current policy position.

- Watch for sharp volatility due to the level of current uncertainty around a rate hike.

The USDJPY rose throughout most of last week as the pair reacted initially to a rise in U.S factory orders and a weak Japanese Account Balance result of 66.0B. Subsequently, the pair ending up finishing the week around 75 pips higher. However, there are some significant risk events looming on the horizon as the Bank of Japan and the U.S. Federal Reserve get ready to set announce their interest rate policies in the week ahead. Subsequently, let's review the pair's major events in the past week and take a look at the possible outcomes for the pending events.

The USDJPY rose steadily throughout most of last week as the pair benefitted from a range of stronger U.S economic data. In particular, a surprise rise in factory orders to 1.2% m/m buoyed the pair, as did the ADP NFP figure of 298k. In addition, the JPY Account Balance figures proved disappointing at 66.0B which further exacerbated the greenback's rise. However, the official NFP result of 235k, released late Friday, saw a surprising trend reversal as the market had been prepared for a much larger figure following the ADP beat. Subsequently, the pair gave back some of its gains but still closed the week out around 75 pips higher at 114.79.

The week ahead will be a busy one for the USDJPY with some sharp volatility likely to be present in the wake of multiple central bank interest rate decisions. In particular, the unpredictable U.S. Federal Reserve is set to meet to determine their near term rate outlook. Although most estimates have the central bank remaining on hold it is still a live meeting where anything could occur. In addition, the Bank of Japan is also set to meet but the chance of a further rate decline, from the present -0.10% rate, is relatively small. However, the statements following both events are likely to bring with them plenty of volatility and some sharp moves for the pair.

From a technical perspective, price action appears to have formed a temporary top around the 115.49 mark before retreating back to its current level. In addition, the RSI Oscillator remains predisposed to the upside, but it should be noted that the indicator is nearing overbought levels. Subsequently, our initial bias for the week ahead is neutral as the current phase could turn consolidative. Support is currently in place for the pair at 113.57, 112.47, and 111.60. Resistance exists on the upside at 115.48, 116.11, and 118.63.

Ultimately, it's likely to be the U.S. Federal Reserve's decision on rates that drives the pair in the coming week. This is especially the case considering that a policy reversal from the central bank is a real possibility given some of the delivered speeches of late. Subsequently, watch the FOMC vote closely as I expect to see plenty of price volatility as the market ultimately moves to digest the decision.